Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

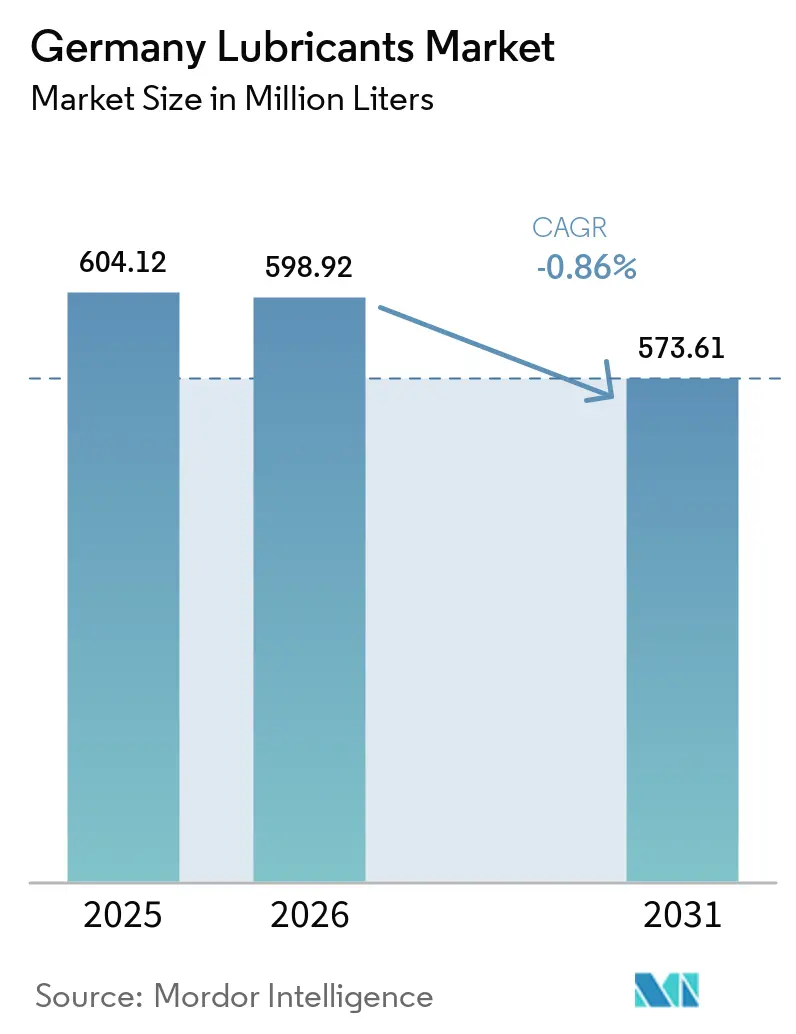

| Base Year Market Size (2025) | 604.12 Million liters |

| Market Volume (2026) | 598.92 Million liters |

| Market Volume (2031) | 573.61 Million liters |

| Growth Rate (2026 - 2031) | -0.86% CAGR |

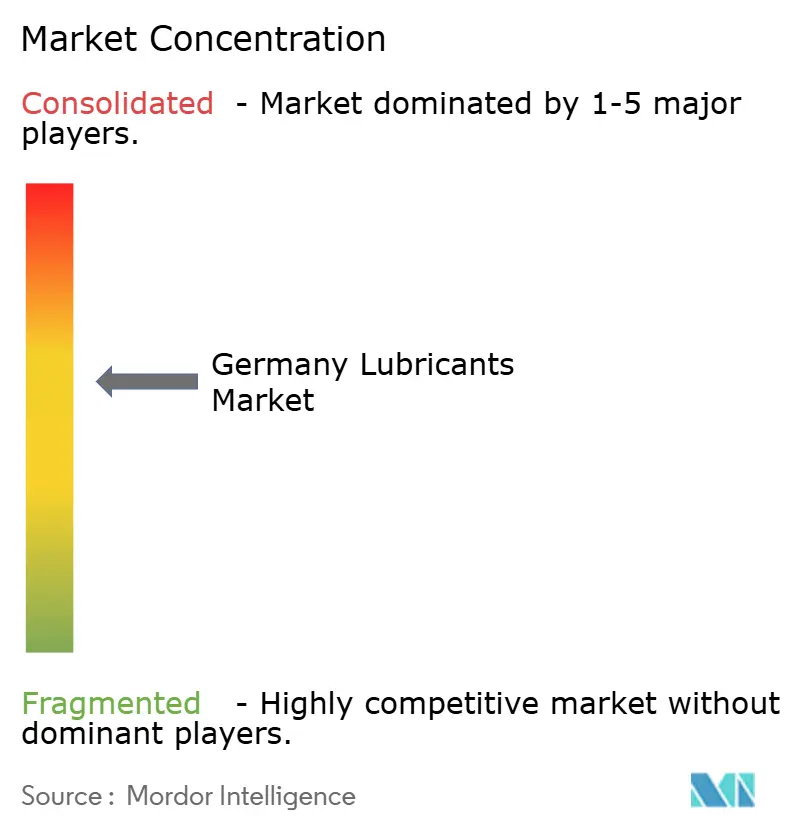

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Lubricants Market Analysis by Mordor Intelligence

The Germany Lubricants Market size is expected to decline from 604.12 million liters in 2025 to 598.92 million liters in 2026 and is forecast to reach 573.61 million liters by 2031 at -0.86% CAGR over 2026-2031. As battery-electric drivetrains phase out traditional engine oils and automakers pivot to low-viscosity synthetics, extending drain intervals, demand is waning. Additionally, with Germany's industrial production declining and volatile factory outputs, the consumption of industrial lubricants has taken a hit. Meanwhile, after a decline in registrations of battery-electric vehicles (BEVs) following subsidy withdrawal, numbers have rebounded. Despite these challenges, there's a silver lining: e-axle lubricants, dielectric battery-cooling fluids, and turbine oils for offshore wind are witnessing significant growth, helping to cushion the blow of volume losses. Heightened regulatory pressures like PFAS phase-outs, Blue Angel biodegradability labels, and CSRD supply-chain audits are hastening the industry's pivot towards re-refined and bio-based formulations. While global giants bolster their market share through integrated supply chains, German specialists are tapping into the burgeoning e-mobility demand via localized co-development initiatives.

Key Report Takeaways

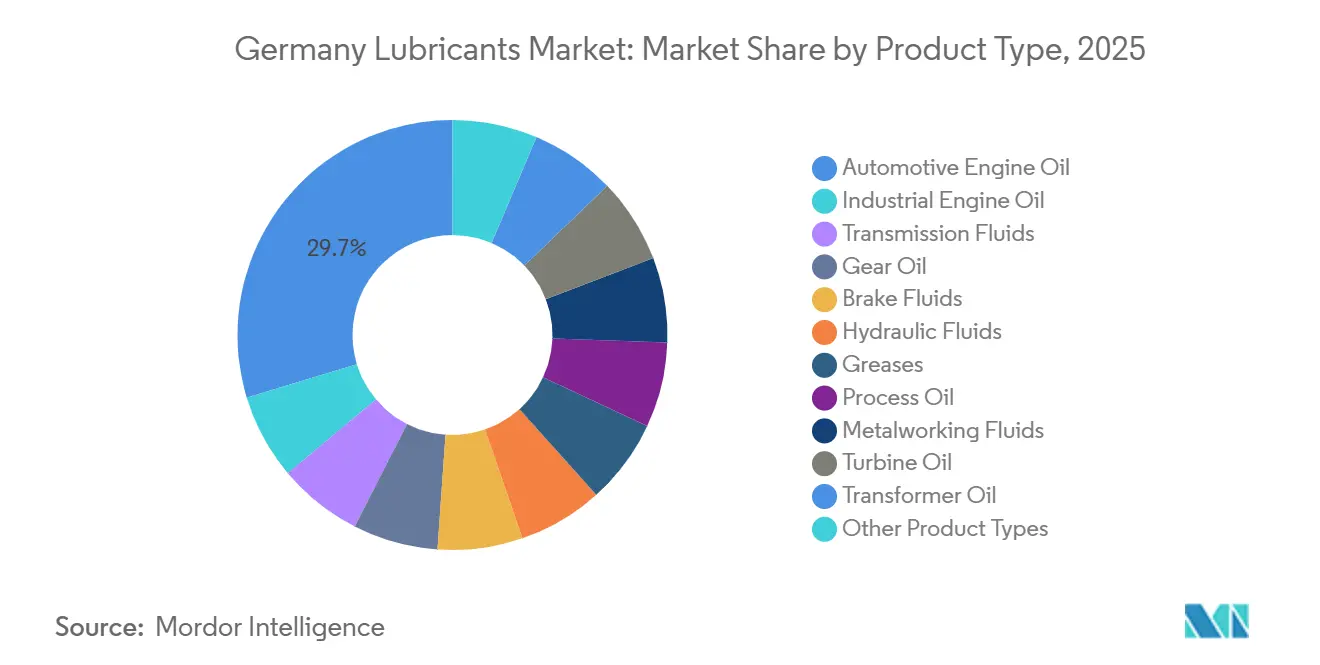

- By product type, automotive engine oil accounted for 29.72% of the market share in 2025. The market size of metalworking fluids is expected to increase with a CAGR of 0.06% during the forecast period (2026-2031).

- By end-user industry, the automotive sector held a 46.22% market share in 2025, and during the forecast period (2026-2031), the industrial sector's share in the market is expected to increase at a CAGR of 0.04%.

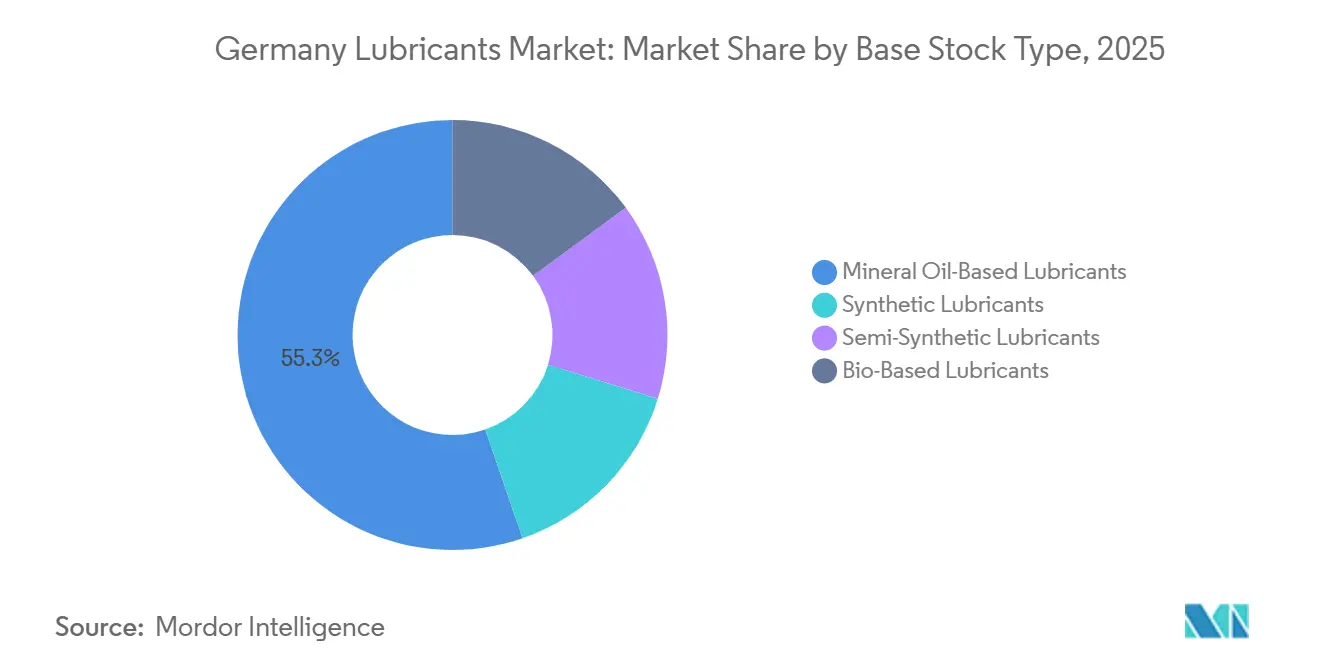

- By base stock type, the market share of the mineral oil-based lubricants was 55.31% in 2025, and the share of bio-based lubricants is expected to increase with a CAGR of 1.96% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Manufacturing-PMI rebound lifting metal-working fluids | +0.3% | Germany, with spillover to Czech Republic, Poland | Medium term (2–4 years) |

| EV-specific e-fluids and thermal-management oils | +0.2% | Germany, EU core markets | Long term (≥ 4 years) |

| Offshore-wind and green-hydrogen turbine-fluid demand | +0.1% | North Sea, Baltic Sea coastal regions | Long term (≥ 4 years) |

| EU Batteries Regulation fostering electrolyte know-how | +0.1% | Germany, EU battery-manufacturing hubs | Medium term (2–4 years) |

| CSRD-driven uptake of re-refined base oils | +0.2% | Germany, EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Manufacturing-PMI Rebound Lifting Metalworking Fluids

In December 2025, Germany's machinery and motor-vehicle plants experienced a significant dip in output before stabilizing. Every uptick in the PMI subsequently bolstered the demand for metal-cutting. Predictive-maintenance emulsions, now integrated with IoT sensors, have successfully extended sump life, leading to a reduction in disposal volumes. Suppliers in Baden-Württemberg have already begun synchronizing coolant replenishment with CNC utilization, achieving a notable reduction in downtime. Meanwhile, a shift from formaldehyde releasers to ester-based semi-synthetics has allowed for easy compliance with ISO 6743-7, ensuring surface finish quality isn't compromised. As production stabilizes, these process enhancements are expected to compound, driving modest volume growth even in a contracting German lubricants market.

EV-Specific E-Fluids and Thermal-Management Oils

By 2026, the Verband der Automobilindustrie forecasts significant growth in battery electric vehicle (BEV) registrations compared to the subdued figures of 2024. Each BEV necessitates dielectric coolants with thermal conductivity greater than 0.15 W/m·K, alongside e-axle oils specifically formulated for electrical insulation and reduced friction. Contracts for factory-fill supplies enhance drivetrain efficiency. Synthetic-ester coolants designed for electric vehicle batteries ensure viscosity stability across a wide temperature range. As automotive fleets transition to electric, these specialized fluids are emerging as the most rapidly expanding segment in Germany's lubricants market.

Offshore-Wind and Green-Hydrogen Turbine-Fluid Demand

Germany, aiming for significant offshore wind capacity by 2030, has been progressing from its operational capacity in 2023, signaling steady annual additions[1]Bundesamt für Seeschifffahrt und Hydrographie, “Offshore Wind Capacity,” BSH.DE. Each megawatt of this capacity utilizes synthetic gear oil and hydraulic fluid. Notably, biodegradable ester formulations have demonstrated the capability to achieve extended service intervals in large turbines. In parallel, with a target for hydrogen electrolyzer roll-outs by 2030, there's a pressing need for compressor and turbine lubricants, specifically tested for high pressures and hydrogen environments. Such developments underscore a sustained demand for high-performance fluids, even as the volumes of conventional engine oils continue to decline.

EU Batteries Regulation Fostering Electrolyte Know-How

Regulation (EU) 2023/1542 mandates strict recycled-content thresholds by 2031, compelling investment in shredders, leach reactors, and smelters that all rely on greases, hydraulics, and heat-transfer oils. Battery-passport QR codes drive traceability, raising the value of lubricants with embedded sensor packages that report viscosity and contamination in real time. Extended producer responsibility targets for collection widen logistics footprints, lifting lubricant demand in forklifts and conveyor bearings.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European refinery closures tightening base-oil supply | -0.5% | Germany, broader EU refining network | Short term (≤ 2 years) |

| Upcoming PFAS ban threatening high-temp greases | -0.3% | Germany, EU-wide | Medium term (2–4 years) |

| EV-subsidy withdrawal distorting specialty-fluid mix | -0.4% | Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

European Refinery Closures Tightening Base-Oil Supply

BP has announced plans to close down its crude capacity at Gelsenkirchen. Meanwhile, Shell repurposed its Wesseling facility into a site capable of producing Group III base oil. In recent years, Germany experienced a significant decline in base-oil sales, which compelled blenders to source premium stocks from the ARA hub. Additionally, smaller formulators, lacking long-term offtake contracts, have been grappling with margin compression, a situation that could hasten industry consolidation.

Upcoming PFAS Ban Threatening High-Temp Greases

ECHA's draft restriction imposes a ceiling on specific PFAS, granting a mere five-year exemption for industrial lubricants[2]European Chemicals Agency, “PFAS Restriction Dossier,” ECHA.EUROPA.EU. Perfluoropolyether greases, essential for bearings operating at temperatures up to 200 degrees Celsius, have no direct substitutes. Furthermore, alternative esters or silicones frequently do not meet load-carrying or oxygen-compatibility standards. This challenge is compounded by reformulation expenses and reduced maintenance intervals, impacting diverse sectors from aerospace actuators to food-contact conveyors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Drain-Interval Extensions Compress Engine-Oil Volumes

Automotive engine oil dominated at 29.72% in 2025. However, ultra-low-viscosity formulations such as 0W-16 and 0W-20 revolutionized the market, allowing for fill volume reductions and extending service intervals significantly. Metalworking fluids show the only positive trend, inching forward at 0.06% CAGR through 2031 as PMI rebounds. Synthetic turbine and transformer oils rode the wave of demand from offshore wind projects and grid upgrades. Meanwhile, brake fluids evolved, with upgrades to DOT 5.1 to better handle the intense heat from regenerative braking. Consequently, the market for engine oils in Germany contracted at a pace outstripping the broader market decline.

In 2025, industrial oil, transmission fluid, and gear oil collectively commanded a significant portion of the market volume, bolstered by long drain intervals favored by commercial fleets. Hydraulic fluids and greases, accounting for a notable share, faced competition from electro-hydraulic actuation substitutes. In a market where basic mineral products waned, specialty blends that leveraged IoT condition monitoring carved out a niche in the German lubricants landscape.

By End-User Industry: Automotive Dominance Masks Structural Decline

Automotive consumed 46.22% of total liters in 2025 share of total oil consumption, even as Germany's vehicle output experienced a year-on-year decline. Industrial applications, projected at a 0.04% CAGR growth through 2031, utilize turbine oils for green-hydrogen facilities and compressor lubricants in battery-recycling operations. Heavy equipment, constituting a notable share of the demand, stands to gain from the climate fund dedicated to rail and road projects, extending through 2027. While the marine and aerospace sectors remain niche, they command high value, necessitating biodegradable cylinder oils and high-temperature greases to meet IMO 2020 standards and support Airbus's production increases.

By Base Stock Type: Synthetics Gain as Mineral Oils Retreat

Mineral oils still held a 55.31% share in 2025, but ceded share yearly to synthetics and semi-synthetics. Bio-based lubricants, growing at a 1.96% CAGR through 2031, win state forestry mandates and CSRD-driven purchasing. Products such as Klüberbio EG 2-68 comply with ISO 12925-1 standards and resist salt-spray corrosion. Semi-synthetics, which combine PAO and Group III minerals, achieve Blue Angel targets without breaking the bank. Meanwhile, advanced PAO and PAG formulations are leading the charge in e-axle oils and hydrogen compressor fluids, driving up synthetic adoption and expanding the premium segment in Germany's lubricants market.

Geography Analysis

In 2025, Germany was a significant contributor to Europe's lubricant demand. However, while Germany struggled with negative growth, neighboring Poland and Czechia, with their cost advantages, experienced a boost in automotive investments. As offshore wind installations increased, the coastal regions of Schleswig-Holstein and Mecklenburg-Vorpommern turned to synthetic turbine oils. North-Rhine-Westphalia, despite being a major hub for the country's metalworking fluid consumption, faced challenges due to soaring gas prices that curtailed usage. While Bavaria and Baden-Württemberg dominated the automotive lubricant market, they dealt with production cuts caused by semiconductor shortages. Eastern regions, relying on oils for agriculture and commercial vehicles, found stability in a niche more insulated from the shift toward passenger car electrification. Given this diverse regional landscape, it is evident that Germany's lubricant market needs to pivot toward specialty high-performance grades to sustain its value amidst declining volumes.

Competitive Landscape

The German lubricants market is moderately consolidated. FUCHS opened an e-mobility fluids center in Mannheim, halving formulation cycles for battery coolants. Quaker Houghton’s sensor-enabled metal-working emulsions lower the total cost of ownership, while Carl Bechem and Zeller+Gmelin target PFAS-free greases for e-motor bearings. IoT analytics, bio-based certifications, and PFAS-free chemistry are the new battlegrounds as players vie for a share in the German lubricants market.

Germany Lubricants Industry Leaders

Shell plc

FUCHS

BP p.l.c.

Exxon Mobil Corporation

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Klüber Lubrication and OKS Spezialschmierstoffe announced their collaboration to establish a strong presence in the specialty lubricants market. The partnership aimed to combine their expertise and resources effectively.

- January 2025: Shell has completed plans to convert its Wesseling refinery to produce 300,000 tonnes of Group III base oils annually. This production will support high-quality lubricants and fulfill 40% of Germany's base oil demand. The initiative highlights Shell's strategic transition from conventional refining to specialty lubricant feedstocks.

Germany Lubricants Market Report Scope

Lubricants are fluids designed to minimize friction between surfaces, thereby preventing wear and tear. Tailored for specific end users, these lubricants are crafted using distinct additives and base oils. Typically, base oils comprise 75% to 90% of a lubricant's formulation, imparting the final product with its essential lubricating properties.

The lubricants market is segmented by product type, end-user industry, and base stock type. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

How fast is Germany’s lubricants demand shrinking?

The German lubricants market size is set to decline at a −0.86% CAGR from 2026 to 2031, contracting from 598.92 million liters in 2026 to 573.61 million liters by 2031.

Which segment will grow fastest despite the overall downturn?

Metalworking fluids are projected to record the highest growth, advancing at a 0.06% CAGR, thanks to the manufacturing-PMI rebound and wider use of IoT-enabled coolants.

What is driving the shift toward bio-based lubricants?

Blue Angel certification, CSRD Scope 3 reporting, and forestry mandates are prompting buyers to adopt bio-based grades growing at a 1.96% CAGR through 2031.

How will refinery closures affect lubricant supply?

Planned crude capacity cuts at Gelsenkirchen and outages at Neustadt have already reduced domestic base-oil availability, tightening feedstock supply and raising import dependence.

Page last updated on: