Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

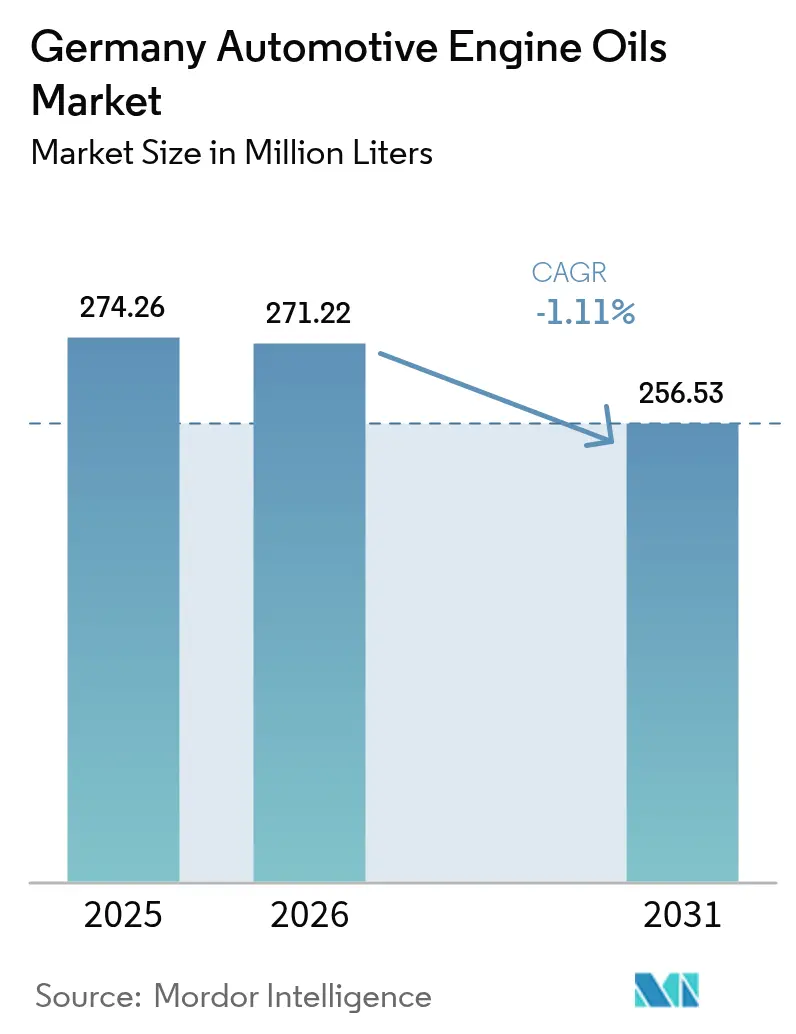

| Base Year Market Size (2025) | 274.26 Million liters |

| Market Volume (2026) | 271.22 Million liters |

| Market Volume (2031) | 256.53 Million liters |

| Growth Rate (2026 - 2031) | -1.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Automotive Engine Oils Market Analysis by Mordor Intelligence

The Germany Automotive Engine Oils Market size was valued at 274.26 Million liters in 2025 and estimated to decline from 271.22 Million liters in 2026 to reach 256.53 Million liters by 2031, at a CAGR of -1.11% during the forecast period (2026-2031). The German automotive engine oil market continues to face headwinds from rapid electrification, tighter Euro-7 emission rules, and a service-network shake-up that together curb lubricant consumption in mass-volume grades. However, hybrid powertrains, long-drain OEM approvals, and sustainability mandates are redirecting value toward premium low-viscosity synthetics and bio-based blends, which trade at noticeably higher margins even as aggregate volumes fall. Competitive positioning increasingly hinges on technical validation, a secure Group III base-oil supply, and the ability to deliver verified Scope 3 carbon savings that align with Germany’s climate policy. Domestic champions capitalize on “Made in Germany” trust, while multinational majors deploy vertical integration and refinery upgrades to defend their share in the German automotive engine oils market.

Key Report Takeaways

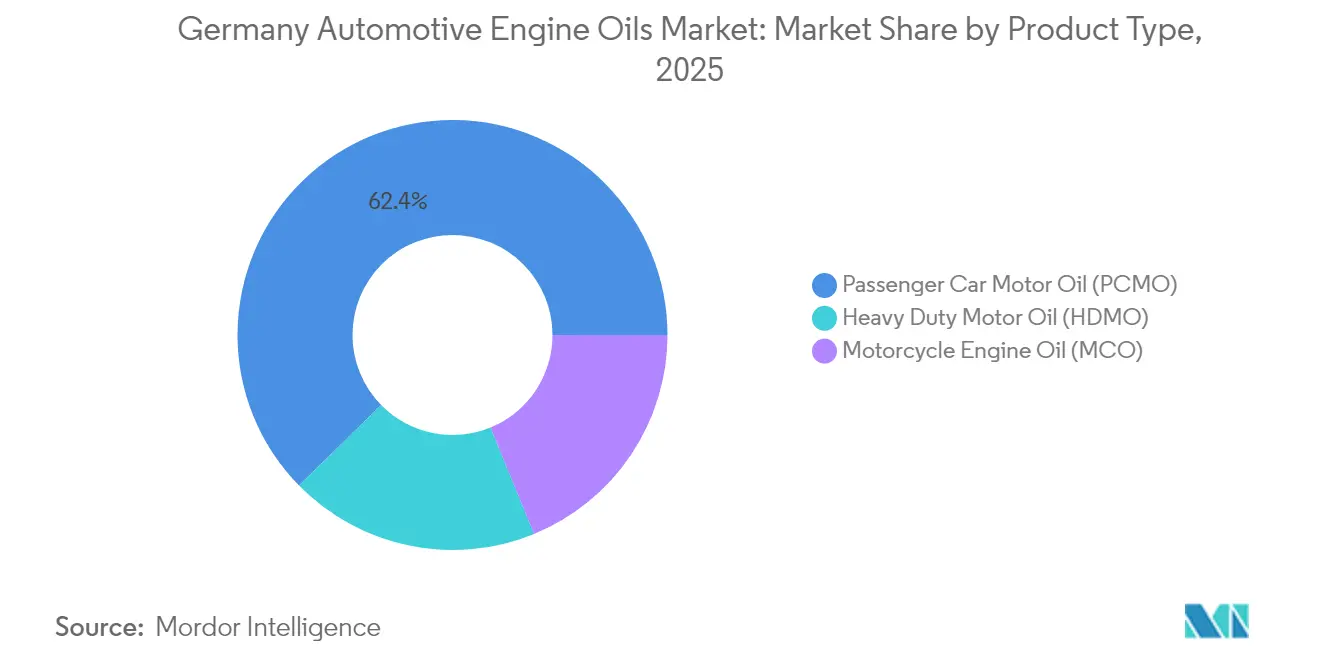

- By product type, Passenger Car Motor Oil led with a 62.35% share of the German automotive engine oils market in 2025, whereas Motorcycle Engine Oil showed the mildest retreat at a -0.95% CAGR through 2031.

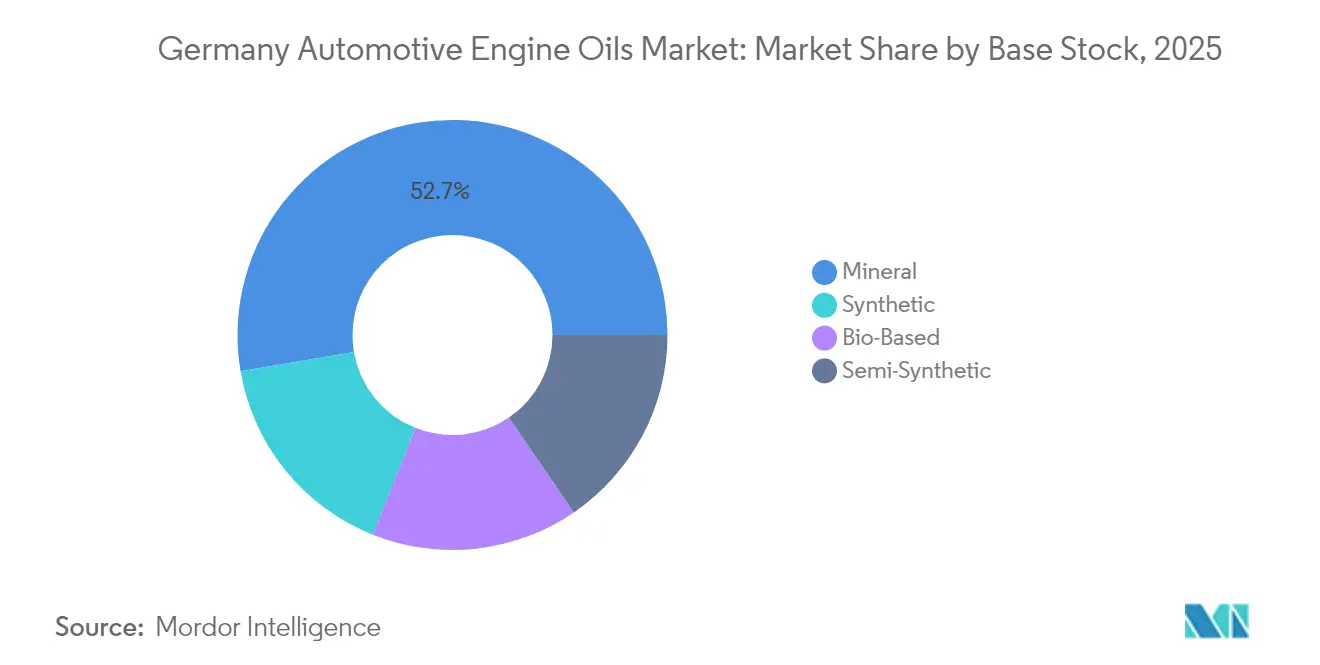

- By base stock, mineral grades captured 52.70% of the German automotive engine oil market size in 2025, while full synthetics are forecast to narrow the gap by declining at a rate of -0.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Euro-7 fuel-economy push accelerates low-viscosity synthetic adoption | +0.3% | Germany, EU core markets | Medium term (2-4 years) |

| Ageing German car parc lifts maintenance and top-up demand | +0.2% | Germany national | Long term (≥4 years) |

| OEM long-drain approvals stimulate premium oil upgrades | +0.2% | Germany, spillover to EU | Medium term (2-4 years) |

| Bio-based and re-refined oils gain traction post-VerpackG 2025 amendment | +0.1% | Germany national | Long term (≥4 years) |

| B2B2C e-commerce platforms reshape workshop procurement | +0.1% | Germany, EU expansion | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Euro-7 Fuel-Economy Push Accelerates Low-Viscosity Synthetic Adoption

Euro-7 tailpipe standards reduce particulate and NOx emissions, prompting OEMs to prescribe 0W-20 and even 0W-16 lubricants that minimize internal friction and meet on-road emissions verification requirements[1]“Euro-7 Emission Standards,” European Commission, ec.europa.eu. New ACEA sequences aligned with these limits ensure that the German automotive engine oil market remains anchored to synthetic chemistries, despite a decline in unit volume. Mercedes-Benz MB 229.71 and BMW Longlife-22FE++ are now mandatory for post-2025 hybrid gasoline models, each requiring ultra-stable low-SAPS formulations. Lubricant blenders that already hold these approvals can charge a premium because replicating the testing protocol costs several million euros and takes 18 months. Euro-7 thus converts regulation into a margin growth lever inside the Germany automotive engine oils market, reinforcing a shift from selling liters to selling lifecycle performance credentials. The upside is most visible in dealership channels, where OEM-specific oils already account for more than two-thirds of synthetic PCMO throughput.

Ageing German Car Parc Lifts Maintenance and Top-Up Demand

Germany’s average light-vehicle age reached 9.5 years in 2025, a full year higher than in 2020, lengthening ownership cycles and expanding aftermarket opportunities[2]“DAT Report 2025,” Deutsche Automobil Treuhand, dat.de . Older engines typically experience higher blow-by and gasket seepage, which raises mid-interval top-up requirements and necessitates the use of viscosity grades such as 5W-30, which are suited to legacy Euro-5 fleets. Workshops report that cars older than eight years require an additional 0.4 liters of make-up oil between scheduled services, which partially compensates for the volume dip induced by the uptake of battery-electric vehicles. Commercial vans and rigid trucks exhibit a similar pattern, with fleet managers extending replacement timelines to hedge against uncertainty in residual value. This demography underpins steady demand in the German automotive engine oils market for high-mileage formulations featuring seal conditioners and detergency boosters. Suppliers with bundled filter-and-oil service kits have leveraged the trend, raising per-visit revenue even as visit frequency stabilizes.

OEM Long-Drain Approvals Stimulate Premium Oil Upgrades

Volkswagen’s VW 508 00/509 00 (Longlife IV) and Porsche C20 approvals extend service windows to 30,000 km or two years, reducing waste streams while increasing the per-liter value captured by suppliers. Long-drain compliance requires Group III + base oils blended with advanced antioxidants, which elevates additive treat rates. For blenders in the German automotive engine oils market, these specifications have doubled gross margin per liter relative to legacy 10W-40 mineral oils. FUCHS secured exclusive first-fill status for several Mercedes-Benz hybrid drivetrains in 2024, underscoring how technical co-development locks in aftermarket pull-through. Competitive barriers are high because each failed engine-test run incurs additional costs, discouraging late entrants. Long-drain programs, therefore, pivot the German automotive engine oils market toward a value-over-volume configuration that rewards research and development depth and OEM intimacy.

Bio-Based and Re-Refined Oils Gain Traction Post-VerpackG 2025 Amendment

Germany’s amended Packaging Act requires lubricant marketers to increase the recycled content in containers and disclose product carbon footprints, sparking interest in re-refined and bio-based base stocks. TotalEnergies amplified the signal by acquiring Tecoil’s 50,000 t/y re-refinery in 2024, adding forward-integrated feedstock to support German customers. End-user surveys indicate that fleet managers are willing to pay a premium for verified low-carbon PCMO, particularly when corporate ESG targets are linked to supplier selection. The integration of digital product passports, which will be mandatory from 2030, further differentiates compliant brands within the German automotive engine oils market and underwrites resilient pricing for circular formulations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU refinery rationalisation swings base-oil availability and price | –0.4% | Germany, broader EU | Short term (≤2 years) |

| 2025 German Chemicals Tax lifts additive costs | –0.2% | Germany national | Short term (≤2 years) |

| Counterfeit oils on online marketplaces erode brand trust | –0.1% | Germany, EU spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Refinery Rationalisation Swings Base-Oil Availability and Price

Shell will repurpose its Wesseling site to focus on Group III production from late 2025, trimming Group I and tightening short-chain supply. BP is reducing Gelsenkirchen crude runs to lower carbon intensity, thereby shrinking local vacuum gas-oil streams that feed base-oil hydrotreaters. Spot Group III prices dipped in early 2025; however, smaller blenders report difficulty in locking multi-year contracts, thereby elevating supply-chain risk. Import reliance has risen to of German base-oil demand, exposing buyers to freight volatility through ARA hubs. Large integrated majors preserve margins by using internal transfer pricing, while independent lubricators face a cost pass-through lag that compresses EBITDA. Capacity shifts, therefore, act as a structural drag on the German automotive engine oils market during the forecast horizon.

Counterfeit Oils on Online Marketplaces Erode Brand Trust

Fake 5W-30 drums often mimic OEM approval codes but fail density and viscosity checks, resulting in knock-on engine wear and warranty disputes. Brand owners must now deploy serialized QR seals and blockchain registries, which add to packaging costs. Persistent counterfeiting risk deters some garages from trading up to premium synthetics, thereby slowing value-mix improvement in the German automotive engine oils market, particularly in price-sensitive rural areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Faces Electrification Pressure

Passenger Car Motor Oil accounted for 62.35% of the German automotive engine oil market in 2025, reflecting Germany’s historic car-centric mobility infrastructure and well-developed dealership maintenance network. EV uptake, led by premium brands, is starting to erode aggregate PCMO demand; yet, the sub-segment still secures a share of the German automotive engine oils market, particularly for high-temperature, turbocharged gasoline engines that require low-SAPS 0W-20 formulations. Motorcycle Engine Oil, though much smaller in volume, will post the mildest volume decline at a –0.95% CAGR because leisure riding culture, particularly in Bavaria and Baden-Württemberg, sustains ICE two-wheelers well into the 2030s. Heavy-duty motor oil demand remains linked to freight-corridor activity on Germany’s Autobahn network, where fleet telematics favor extended-drain 10W-30 CK-4 formulations with mild HTHS retention for Euro VI diesel engines. The German automotive engine oil market, therefore, exhibits a two-speed profile: conventional PCMO grades in older sedans contract sharply, while OEM-specific synthetics for luxury hybrids capture a resilient wallet share.

Fleet managers prioritize fuel economy and downtime reduction, prompting HDMO suppliers to adopt FA-4 5W-30 blends that deliver fuel savings in long-haul operations. Meanwhile, MCO marketers utilize extended shelf-life monoesters to increase average selling prices at retail. OEM-filled hybrid models, such as the Mercedes-Benz GLC 400e, require dual-purpose formulations that control LSPI and maintain catalyzer protection, giving German integrators early-mover leverage. Across every product bracket, the German automotive engine oils market rewards chemistry capable of meeting both Euro-7 after-treatment durability and customer perception of premium brand value.

By Base Stock: Synthetic Grades Outperform in Declining Market

Mineral oils still accounted for 52.70% of the German automotive engine oil market in 2025, yet their volume declined faster than the overall trend as OEMs reinforced 0W and 5W indices that cannot be met with Group I stocks alone. Full synthetics, in contrast, shrink by only –0.83% CAGR because Euro-7 and OEM long-drain mandates require higher oxidative stability, which pushes average treat-rate costs up but also boosts the margin pool as price differentials widen. Semi-synthetic hybrids lose strategic relevance, caught between low-cost mineral loyalty and true high-performance synthetics that secure dealership recommendation.

Shell’s Wesseling expansion to 300 kt/y Group III output offers domestic blenders a proximity advantage, mitigating logistics risk once Russian base-oil imports ceased during the 2024 geopolitical realignments. Suppliers differentiate themselves through pour-point depressant technology, with ester-enriched 0W-16 meeting the cold-start demands of plug-in hybrid duty cycles. The German automotive engine oils market, therefore, migrates toward a barbell structure: low-income users cling to low-additive 15W-40, while fleet and premium-car owners adopt high-end synthetics enlivened by renewable content claims. This polarization shapes research and development pipelines, guiding capital expenditures toward hydrocracker upgrades rather than traditional solvent refining.

Geography Analysis

Regional demand remains concentrated in North Rhine-Westphalia, Baden-Württemberg, and Bavaria, thanks to high vehicle registrations and thriving industrial fleets. Urban electrification initiatives in Berlin and Hamburg are beginning to reduce PCMO throughput in dealership quick-lube bays, yet suburban commuter belts still favor ICE vehicles for their range flexibility, thereby preserving lubricant demand diversity. Southern federal states exhibit the highest motorcycle penetration, which cushions the MCO decline and supports a vibrant aftermarket for performance esters and specialty two-stroke injector cleaners.

Eastern regions such as Saxony and Thuringia offer cost-competitive warehouse space, attracting e-commerce-driven lubricant distribution hubs that shorten lead times to Poland and the Czech Republic. Despite electrification, the Munich–Stuttgart premium car corridor sustains per-vehicle oil consumption because OEM specifications dictate dealership loyalty. Conversely, rural Schleswig-Holstein exhibits a notable shift toward private-label 10W-40 purchased through discount retailers, illustrating divergent price elasticities within a single national boundary.

Upcoming EU TEN-T corridor extensions will increase long-haul freight volume through Rhineland logistics hubs, indirectly supporting HDMO sales even when passenger-car lubricants become less competitive. Concurrently, planned low-emission zones restrict older diesel vehicles from operating inside city centers, prompting fleet operators to modernize, which temporarily reduces the first-fill volume. These offsetting currents confirm that local policy heterogeneity is a vital layer of due diligence when mapping channel strategy inside the Germany automotive engine oils market.

Competitive Landscape

The German automotive engine oil market features a moderately consolidated competitive landscape. FUCHS, headquartered in Mannheim, continued to deepen OEM alignment, securing factory-fill status for Mercedes hybrid drivelines and rolling out an in-house e-fluids suite for gearboxes and thermal-management loops. Competitive intensity is sharpening as aggregate liters fall. Majors invest in lab capabilities that shorten homologation cycles, a move that independents cannot easily replicate. Digital subscription platforms that pair lubricant analytics with telematics data now differentiate service models, shifting emphasis from product sales to uptime assurance. Innovation gravity tilts toward circular economy offerings. Medium-sized German blenders respond by co-investing in regional re-refineries to backstop feedstock and hedge volatility in virgin Group III prices. Advances in free-standing detergent booster packs enable on-site customization, allowing distributors to carry fewer finished SKUs.

Germany Automotive Engine Oils Industry Leaders

Shell plc

LIQUI MOLY

BP Plc

FUCHS

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP Plc initiated a review of its Castrol lubricants unit, valued at up to USD 10 billion, as part of a wider divestment program running through 2027. The outcome will impact Castrol’s German footprint, where the brand holds a notable share in the premium PCMO market.

- September 2024: Chevron appointed Finke Mineralölwerk as the exclusive German distributor for Texaco-branded lubricants, leveraging 70 regional sales offices to extend reach across independent workshop channels.

Germany Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How much engine oil volume will Germany consume by 2031?

Demand is projected to slip to 256.53 million liters, reflecting a -1.11% CAGR from 2026.

Which lubricant category still claims the largest share in German vehicles?

Passenger Car Motor Oil leads with 62.35% of national consumption in 2025.

What keeps synthetic formulations more resilient than mineral grades?

Euro-7 emission rules and OEM long-drain approvals require low-viscosity Group III blends, limiting their decline to –0.83% CAGR.

How does Euro-7 influence the specifications workshops must stock?

The standard drives adoption of 0W-20 and 0W-16 oils that meet tighter particulate and NOx limits and carry OEM approvals such as VW 508 00/509 00.

Page last updated on: