Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 30.01 Billion |

| Market Size (2026) | USD 31.4 Billion |

| Market Size (2031) | USD 39.39 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Last Mile Delivery Market Analysis by Mordor Intelligence

The Germany last mile delivery market size was valued at USD 30.01 billion in 2025 and estimated to grow from USD 31.4 billion in 2026 to reach USD 39.39 billion by 2031, at a CAGR of 4.64% during the forecast period (2026-2031). Stable economic growth, the nation’s position as Europe’s largest e-commerce arena, and infrastructure spending mandated under the German Postal Law 2024 combine to underpin sustained parcel demand and network densification. Competitive intensity heightens as incumbents and new alliances race to expand open-access parcel-locker footprints, roll out electric fleets, and embed AI route engines that curb rising wage and fuel bills. Regulatory measures that tighten emissions limits spur accelerated fleet electrification, while consumer preference for convenient PUDO options pushes carriers to re-engineer the urban stop footprint. The Germany last mile delivery market is thus set for methodical, technology-led growth with consolidation favoring operators that can balance service quality, cost discipline, and sustainability milestones.

Key Report Takeaways

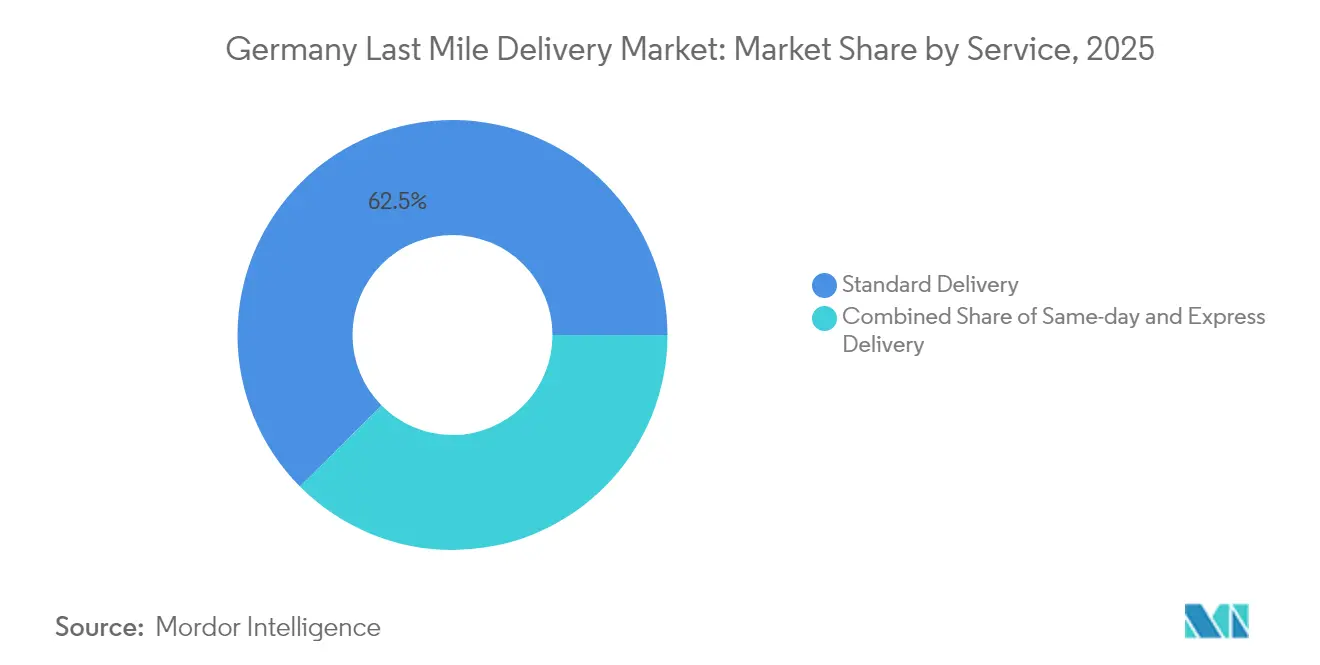

- By service, standard delivery held 62.45% of the Germany last mile delivery market share in 2025; same-day delivery is projected to record a 3.62% CAGR through 2031.

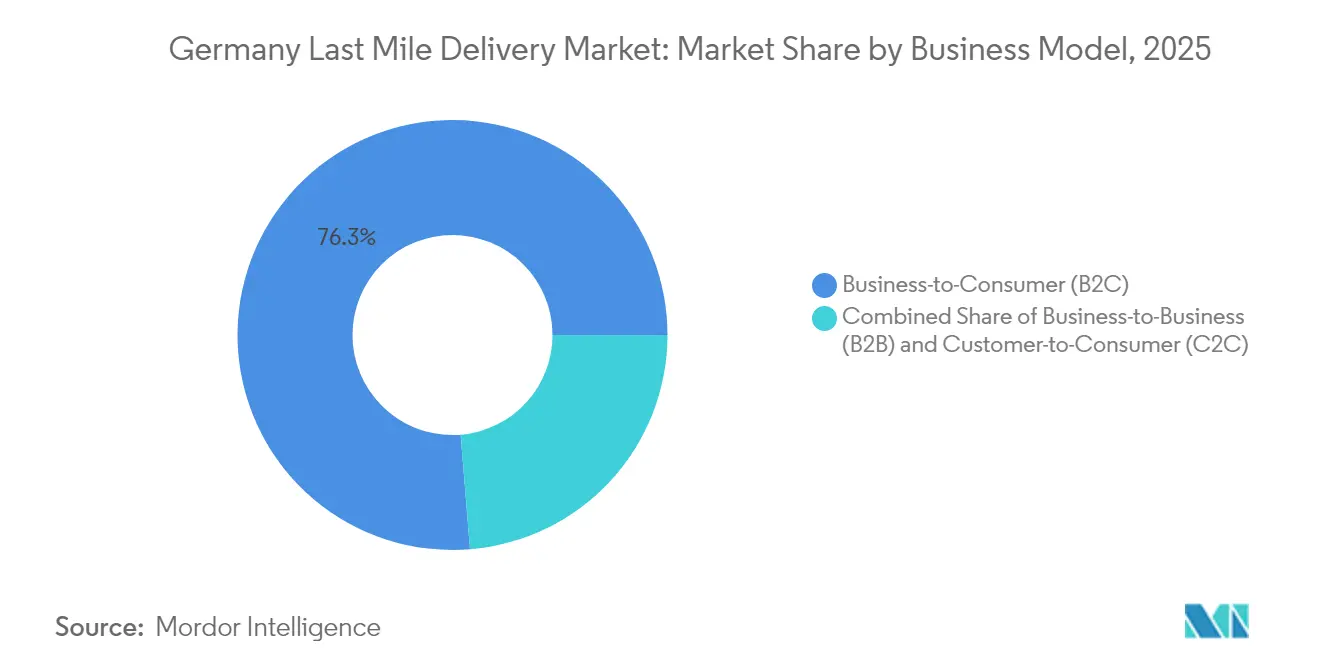

- By business model, B2C accounted for 76.30% of the Germany last mile delivery market size in 2025, while C2C is forecast to expand at a 3.98% CAGR to 2031.

- By end-user industry, e-commerce retail commanded a 36.60% share of the Germany last mile delivery market size in 2025, and healthcare delivery is advancing at a 4.25% CAGR through 2031.

- By federal state, North Rhine-Westphalia led with 20.90% share in 2025, whereas Berlin is clocking the fastest trajectory at a 4.69% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Last Mile Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in domestic e-commerce parcel volumes | +1.2% | National, with concentration in NRW, Bavaria, Berlin | Medium term (2-4 years) |

| Expansion of parcel-locker & PUDO networks | +0.8% | Urban centers nationwide, led by DHL, DPD-GLS networks | Short term (≤ 2 years) |

| Sustainability regulations driving EV fleets | +0.9% | Major metropolitan areas, Hamburg, Berlin, Munich | Long term (≥ 4 years) |

| Micro-hub reuse of vacant retail & parking assets | +0.7% | Dense urban areas, Berlin, Hamburg, Frankfurt | Medium term (2-4 years) |

| AI-enabled zonal logistics & route optimization | +1.1% | National deployment by major carriers | Short term (≤ 2 years) |

| German Postal Law 2024 boosting infrastructure spend | +0.4% | National infrastructure, rural area focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Domestic E-commerce Parcel Volumes

Domestic B2C parcel flows continue to rise as German consumers deepen online shopping penetration, sending annual shipment counts to record highs[1].Federal Network Agency, “Postal Market Data,” Bundesnetzagentur, bundesnetzagentur.de Cross-border platforms such as Temu and Shein import sizeable parcel quantities, amplifying inbound volumes and stretching urban sorting hubs. Consumer surveys reveal higher expectations for predictable delivery windows, consolidating demand around carriers with dense stop coverage and automated sortation. The fashion-led Zalando–About You tie-up, signed in 2025, further amplifies parcel density by pooling fulfillment under unified logistics leadership. Larger operators gain scale economies that shield margins, whereas newcomers shoulder a higher cost-per-stop in sparsely served corridors.

Expansion of Parcel-Locker & PUDO Networks

The October 2024 DPD-GLS alliance created Germany’s largest open locker system, enabling parcel hand-off interoperability across thousands of automated boxes[2]Reuters Staff, “DPD-GLS Partnership Germany,” Reuters, reuters.com. Deutsche Post DHL is on track to install a Packstation within walking distance for most urban residents by 2030. Building-integrated lockers launched through the 2025 myflexbox–DPD cooperation improve first-attempt success and shrink delivery dwell time. Retail checkout APIs now surface locker locations in real time, encouraging click-and-collect and cutting failed delivery costs. High up-front locker investment favors scale players able to underwrite multi-year site leases.

Sustainability Regulations Driving EV Fleets

Germany’s Clean Air Act and EU zero-emission zone mandates compel carriers to electrify fleets ahead of the 2030 deadline, accelerating battery van procurement and charging-dock buildouts[3]Federal Environment Agency, “Sustainable Mobility,” Umweltbundesamt, umweltbundesamt.de. Deutsche Post DHL deployed thousands of StreetScooter vans and built on-site chargers in every major sorting node by end-2024. Hermes runs fully emission-free city routes in Hamburg employing cargo bikes and compact e-vans, showcasing operational viability at lower lifecycle cost per kilometer than diesel units. Government purchase incentives remain in place through 2026, helping carriers phase out internal-combustion vans ahead of the regulatory cliff.

AI-Enabled Zonal Logistics & Route Optimization

Deutsche Post DHL’s in-house AI platform processes millions of historical stops each night to rewrite next-day zone boundaries and loading sequences, reducing empty kilometers and lifting stop productivity. Predictive algorithms factor in weather, traffic, and customer time-of-day availability to minimize failed attempts. Mid-tier carriers adopting similar cloud-native engines report double-digit fuel savings, shrinking exposure to diesel volatility. GDPR compliance requires data-minimization protocols, but successful pilots confirm that customer location analytics can be anonymized while retaining optimization value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labor & fuel costs | -0.6% | National, acute in high-wage regions | Short term (≤ 2 years) |

| Package theft/damage & failed first-attempts | -0.4% | Urban areas, apartment-dense neighborhoods | Medium term (2-4 years) |

| Wage-inflation from collective bargaining rounds | -0.5% | National, ver.di union coverage areas | Short term (≤ 2 years) |

| Scarce inner-city logistics real-estate | -0.3% | Metropolitan areas, Berlin, Munich, Hamburg | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Labor & Fuel Costs

Collective bargaining rounds in 2024 granted postal and parcel employees meaningful wage increases, lifting the cost base for carriers that already spend more than half of their operating expenses on personnel. Driver shortages remain chronic, forcing firms to raise entry pay and sign-on bonuses. Fuel outlays also climbed during 2024 amid energy-price volatility and higher highway tolls, compressing margins where contractual rate-adjustment clauses lag input inflation[4]Federal Statistical Office, “Consumer Price Index Categories,” Destatis, destasis.de. Automation in sort centers and partial fleet electrification offset some pressure but require multiyear capital commitments.

Scarce Inner-city Logistics Real Estate

Prime warehouse vacancies across German metros hover in low single digits, driving rents in Berlin and Munich to record highs. Zoning restrictions push last-mile operators toward brownfield conversions and mixed-use permits that can take years to secure. Carriers increasingly partner with parking-garage owners or retrofit retail basements into micro-hubs, strategies that preserve proximity yet demand creative layout and access solutions. The scarcity elevates capital intensity and favors incumbents with existing footprints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Standard Delivery Holds Its Lead as Same-day Gains Momentum

Standard delivery services captured 62.45% of the Germany last mile delivery market share in 2025, sustained by consumer sensitivity to shipping fees and the breadth of rural destinations served. Same-day options, though niche, is expected to log the strongest forward pace at a 3.62% CAGR (2026-2031) as urban shoppers increasingly value immediacy for time-critical purchases.

The Germany last mile delivery market size for same-day services is expected to rise steadily, helped by retailer partnerships that pool order cut-off times and micro-hub staging. Carriers employ AI sorting to feed evening rounds that deliver before midnight, maintaining service differentiation without eroding unit margins. Standard delivery profitability remains tied to high stop density and consolidated line-haul, while express-service demand stabilizes in B2B verticals needing guaranteed transit.

By Business Model: B2C Dominance Faces C2C Upswing

B2C parcels anchored 76.30% of 2025 revenue, reflecting mature e-commerce penetration and entrenched carrier-retailer integrations. C2C traffic, fueled by Vinted and similar resale marketplaces, is predicted to grow at a 3.98% CAGR (2026-2031), injecting fragmented shipment flows that require flexible pickup slots and convenient drop-off points.

The Germany last mile delivery market size linked to C2C exchanges benefits from cross-border activity between Germany, France, and Italy, with carriers leveraging open locker networks to streamline handovers. B2B flows, although smaller, maintain relevance in industrial supply chains where documentation and time-definite needs justify premium pricing. Platform APIs that auto-generate labels and customs data simplify C2C adoption and reinforce growth momentum.

By End-user Industry: E-commerce Leads, Healthcare Accelerates

E-commerce retail retained a 36.60% grip on value in 2025, helped by fashion, consumer electronics, and home goods that produce high return ratios and repeat deliveries. Healthcare parcels, encompassing prescription drugs and temperature-sensitive biologics, are tracking a 4.25% CAGR through 2031 as telemedicine uptake and demographic aging amplify doorstep demand.

Healthcare’s ascent propels investment in GDP-compliant vans and cold-chain packaging that meet stringent thermal integrity rules. UPS’s 2024 acquisition of Frigo-Trans expanded access to validated, temperature-controlled routes that can serve hospitals and pharmacies nationwide. Subscription-based beauty and wellness boxes supplement base volume, while bulky furniture and white-goods deliveries require two-person crews and scheduled time slots, complicating network planning.

Geography Analysis

North Rhine-Westphalia (NRW) contributed 20.90% of the value in 2025, leveraging extensive autobahn links and proximity to Benelux markets that enable cross-border fulfillment synergies. Cologne and Düsseldorf host high-capacity sort centers, and the state’s industrial base supplies steady B2B parcel flows that balance residential peaks.

Berlin exhibits the fastest growth trajectory at 4.69% CAGR through 2031, propelled by a thriving startup ecosystem, rising disposable income, and city-backed smart-mobility programs that fast-track micro-depot permits. Elevated real-estate costs push carriers toward underground parking-hub conversions and cargo-bike routes that comply with low-emission zone rules.

Competitive Landscape

Deutsche Post DHL sustains leadership through unmatched network scale, proprietary locker assets, and vertically integrated air and road line-haul. Yet rivalry tightened after the DPD-GLS alliance pooled locker infrastructure, giving customers carrier-agnostic drop-off freedom. UPS expanded healthcare breadth by taking over Frigo-Trans, while FedEx upgraded Karlsruhe capacity to shorten cut-offs in southwest corridors.

Investment focus spans AI route engines, electrification, and micro-hub buildouts that alleviate inner-city congestion. Smaller couriers partner with retail chains to embed PUDO counters, carving niches in specialized or regional segments. Sustainability credentials emerge as tender prerequisites for municipal and enterprise contracts, advantaging early adopters of battery vans and cargo bikes.

White-space opportunities lie in cold-chain healthcare, C2C resale, and rural service gaps where German Postal Law investment subsidies lower entry barriers. Consolidation is expected as capital intensity climbs, with locker-network sharing and joint purchasing groups echoing recent tie-ups. Overall market concentration is moderate, and leadership is likely to depend on technology depth, fulfillment flexibility, and regulatory compliance speed.

Germany Last Mile Delivery Industry Leaders

Deutsche Post DHL Group

Hermes

UPS

DPD

GLS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Jun 2025: UPS Germany launched UPS SmartEnergy Solutions, a shipping service that removes emissions at source by leveraging renewable energy procurement and route electrification.

- May 2025: DPD Germany began building a sustainable sorting center in Kaiserslautern, targeting advanced automation and energy efficiency standards.

- May 2025: GLS Germany commenced construction of a Bremen distribution hub designed to process 35,000 parcels daily and open in late 2026.

- February 2024: FedEx Express opened an expanded Karlsruhe facility, enlarging parcel handling zones and improving pickup-and-delivery times in southwest Germany.

Germany Last Mile Delivery Market Report Scope

The transit of goods from a transportation hub to the last delivery destination is known as last-mile delivery. Last-mile delivery focuses on getting things to the final user as quickly as possible. A complete assessment of Germany's Last Mile Delivery Market includes an overview of the economy market, market size estimation for key segments, and emerging trends in the market segments in the report. The report sheds light on the market trends like growth factors, restraints, and opportunities in this sector. The competitive landscape of Germany's Last Mile Delivery Market is depicted through the profiles of active key players. The report also covers the impact of COVID–19 on the market and future projections.

The Germany Last-Mile Delivery Market report is segmented by Service (B2B (Business-to-Business), B2C (Business-to-Consumer), and C2C (Customer-to-Customer)). The report offers the market size in value terms in USD for all the abovementioned segments.

By Service

| Standard Delivery |

| Same-day |

| Express Delivery |

By Business Model

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

By End-user Industry

| E-commerce Retail |

| Fashion & Lifestyle |

| Beauty, Wellness & Personal Care |

| Home & Furniture |

| Consumer Electronics & Appliances |

| Healthcare & Medical Supplies |

| Others |

By German Federal State

| Baden-Wurttemberg |

| Berlin |

| Bavaria |

| North Rhine-Westphalia |

| Rest of German Federal State |

| By Service | Standard Delivery |

| Same-day | |

| Express Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End-user Industry | E-commerce Retail |

| Fashion & Lifestyle | |

| Beauty, Wellness & Personal Care | |

| Home & Furniture | |

| Consumer Electronics & Appliances | |

| Healthcare & Medical Supplies | |

| Others | |

| By German Federal State | Baden-Wurttemberg |

| Berlin | |

| Bavaria | |

| North Rhine-Westphalia | |

| Rest of German Federal State |

Key Questions Answered in the Report

How large is Germany’s last-mile delivery value pool in 2026?

The segment is worth USD 31.4 billion in 2026 and is projected to continue rising through 2031.

What compound annual growth rate is forecast for German last-mile logistics to 2031?

A 4.64% CAGR is projected between 2026 and 2031.

Which service format currently captures the greatest share of parcel revenue?

Standard delivery commands 62.45% of 2025 value, reflecting consumer price sensitivity and nationwide coverage.

Why is same-day fulfillment showing the quickest momentum?

Dense urban demand, retailer differentiation, and micro-hub rollouts are pushing same-day volume along a 3.62% CAGR trajectory through 2031.

How are emissions rules influencing city-center delivery tactics?

Clean-air legislation is accelerating electric van adoption, cargo-bike routes, and charging-infrastructure build-outs to secure zero-emission compliance before 2030.

Which German state is expanding parcel volume the fastest?

Berlin leads with a projected 4.69% CAGR to 2031, buoyed by its digital-first consumer base and supportive urban-logistics policies.

Page last updated on: