Germany Electric Vehicle Charging Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

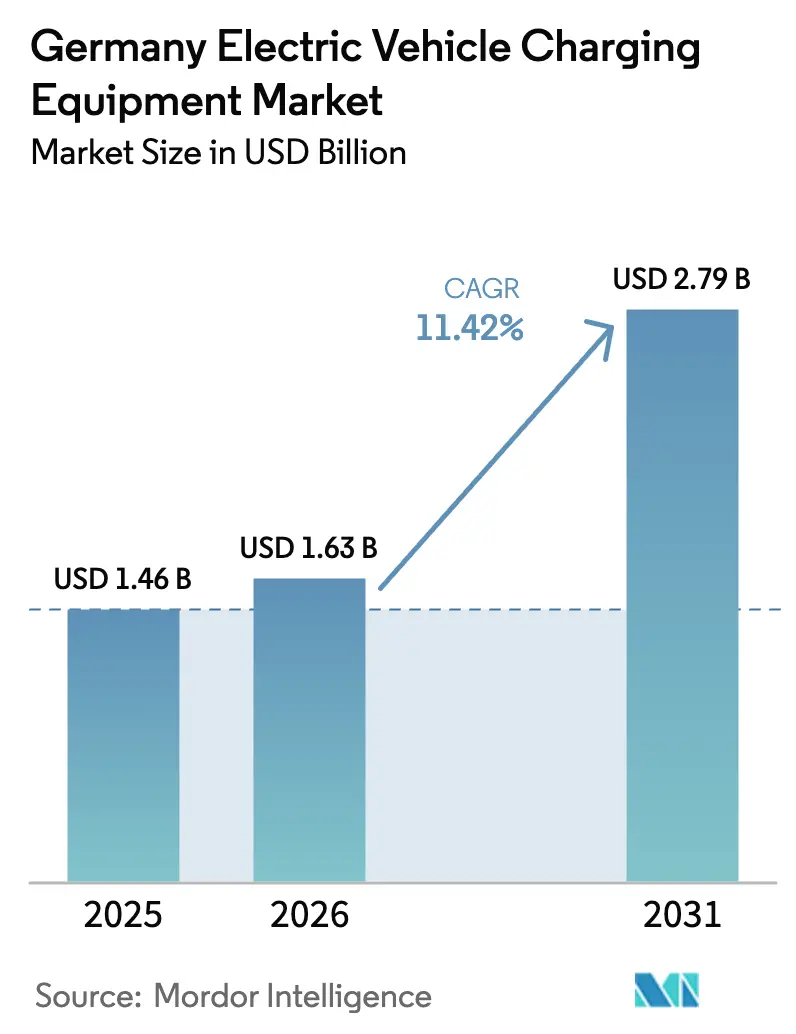

| Base Year Market Size (2025) | USD 1.46 Billion |

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 2.79 Billion |

| Growth Rate (2026 - 2031) | 11.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Electric Vehicle Charging Equipment Market Analysis by Mordor Intelligence

The Germany Electric Vehicle Charging Equipment Market size is expected to grow from USD 1.46 billion in 2025 to USD 1.63 billion in 2026 and is forecast to reach USD 2.79 billion by 2031 at 11.42% CAGR over 2026-2031.

This growth outlook reflects Berlin’s decision to pivot from vehicle purchase incentives to federally mandated infrastructure deployment under the Deutschlandnetz fast-charging program. Contracted revenue streams, grid-integrated hardware requirements, and OEM co-investment obligations now shape a business environment in which predictable cash flows matter more than short-term demand swings. Equipment makers are responding by scaling local service networks, optimizing liquid-cooled power electronics, and bundling long-term maintenance with software upgrades. Meanwhile, utilities and energy retailers have begun offering vertically integrated packages that combine charging hardware, renewable-electricity contracts, and dynamic tariffs, compressing margins for standalone operators yet widening market opportunities for suppliers that can deliver turnkey solutions.

This reformatted policy landscape reshapes capital allocation. Federal commitments of EUR 1.9 billion to install more than 900 fast-charging sites by late 2025 convert speculative site selection into contracted revenue that supports debt financing for equipment purchases. The removal of direct vehicle subsidies in December 2023 channels public money toward grid expansions, transformer upgrades, and liquid-cooled dispensers, fundamentally improving visibility for investors funding the German electric vehicle charging equipment market. Automakers, no longer supported by consumer incentives, are forming joint ventures with oil majors and utilities to guarantee brand-aligned charging experiences and safeguard long-haul travel convenience. For suppliers, the result is clear: the German electric vehicle charging equipment market rewards those who can combine hardware reliability, software flexibility, and grid-service compatibility without compromising speed of deployment.

Key Report Takeaways

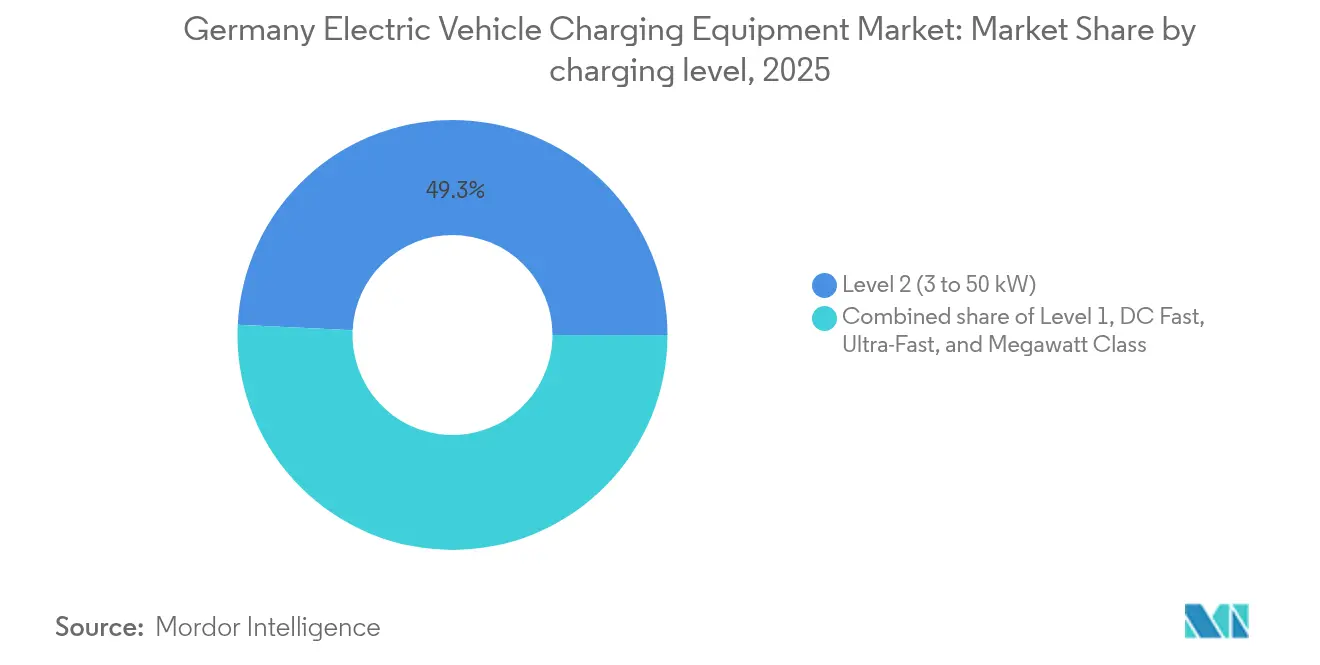

- By charging level, Level 2 systems captured 49.25% of the German electric vehicle charging equipment market share in 2025, while Megawatt Class chargers are forecast to expand at a 30.6% CAGR through 2031.

- By installation site, residential settings held 61.60% of the German electric vehicle charging equipment market share in 2025, whereas transportation hubs are projected to grow at a 27.9% CAGR to 2031.

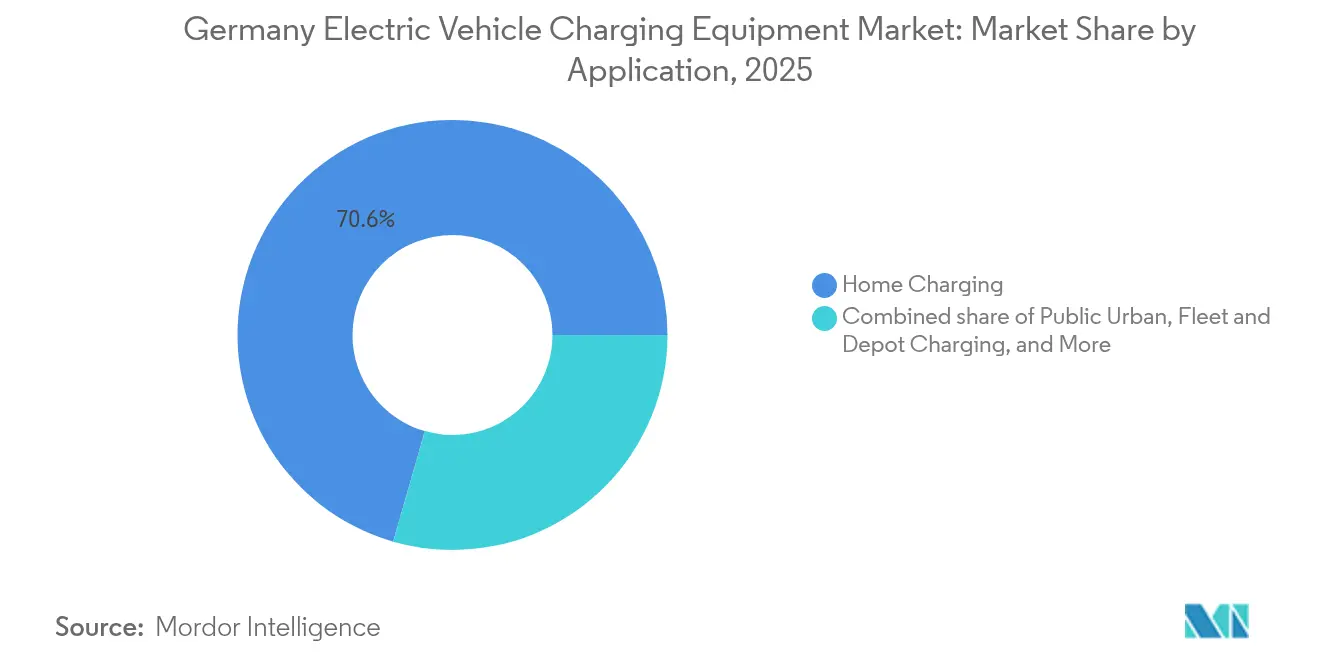

- By application, home charging accounted for a 70.55% share of the German electric vehicle charging equipment market size in 2025, and fleet-depot installations are projected to advance at a 34.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with Germany contributing to the overall trajectory. The outlook on worldwide electric vehicle charging equipment market reflects how these are expected to evolve collectively.

Germany Electric Vehicle Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust federal subsidies and Deutschlandnetz tenders | +2.80% | National focus on North Rhine-Westphalia, Bavaria, Baden-Württemberg | Short term (≤ 2 years) |

| OEM-backed HPC corridor roll-out (IONITY, Mercedes-BP) | +3.20% | Autobahn corridors and major cities | Medium term (2-4 years) |

| Dynamic-tariff revenues for smart residential chargers | +2.10% | Urban centers with high EV density | Medium term (2-4 years) |

| Building Code mandate for EV-ready parking (GEG 2023) | +1.90% | Nationwide, early enforcement in large cities | Short term (≤ 2 years) |

| Fleet electrification surge in urban logistics | +1.50% | Metropolitan logistics hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Federal Subsidies & Deutschlandnetz Tenders

The Deutschlandnetz program directs EUR 1.9 billion toward more than 900 publicly accessible fast-charging locations that must deliver 99% uptime and full roaming compatibility. Contracts awarded in September 2024 cover rural corridors within 10 km of autobahn exits, converting uncertain traffic volumes into fixed revenue guarantees that de-risk capex for operators. Local content rules favor suppliers with German service crews, positioning Alpitronic and Compleo to capture substantial orders. The Master Plan Charging Infrastructure II targets 1 million public charge points by 2030, up from 100,000 in 2024, and effectively sets the installation tempo that underpins demand in the German electric vehicle charging equipment market.

OEM-Backed HPC Corridor Roll-Out (IONITY, Mercedes-BP)

Automakers now view branded charging as a post-sale loyalty tool. IONITY expanded to 100 German sites by mid-2024 and plans 200 by 2026, installing 350 kW dispensers that reduce highway dwell times to 15 minutes. Mercedes-Benz and bp will deploy 300 high-power stations across Germany by 2026, integrating car-based payment through the Mercedes me platform. These moves threaten independent charge-point operators yet open volume opportunities for white-label equipment providers that can tailor branding and payment integration quickly.

Dynamic-Tariff Revenues for Smart Residential Chargers

GEIG amendments that take effect in January 2025 require bidirectional capability for new home units above 11 kW, effectively turning household chargers into grid assets.(1)Federal Ministry for Economic Affairs and Climate Action, “Building Energy Act Amendments,” bmwk.de Pilot projects in Hamburg and Munich generated EUR 30–50 in monthly grid-service income per vehicle during 2024, shortening payback periods on higher-capacity wallboxes. Suppliers such as Wallbox and Webasto rolled out firmware upgrades to retrofit ISO 15118-20 features across existing installed bases, monetizing software while locking in service subscriptions.

Building Code Mandate for EV-Ready Parking (GEG 2023)

The Gebäudeenergiegesetz revision obliges residential buildings with more than five spaces to include EV-ready conduit and capacity, with financial penalties for non-compliance. Commercial buildings must equip 20% of parking spaces with active chargers. Municipal enforcement in Berlin and Frankfurt resulted in occupancy permit delays throughout 2024, forcing developers to pre-order hardware and lifting near-term demand in the German electric vehicle charging equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High grid-connection and transformer upgrade costs | -1.80% | National, acute in rural areas | Short term (≤ 2 years) |

| Volatile subsidy outlook post-2025 | -1.40% | Nationwide, with state-level variation | Medium term (2-4 years) |

| Distribution-grid permitting bottlenecks | -1.20% | Municipalities with understaffed DSOs | Short term (≤ 2 years) |

| Tariff and roaming complexity lowering public-charger utilization | -0.90% | Urban locations with multiple roaming schemes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Grid-Connection & Transformer Upgrade Costs

Medium-voltage extensions can add EUR 50,000–150,000 to a site while transformer upgrades cost another EUR 30,000–80,000, undermining standalone operator economics, especially outside large cities. To contain investment, Alpitronic and Compleo introduced buffer-battery chargers that shave peak demand by 30-40%, but only become cost-effective when grid upgrades exceed EUR 100,000 per location.

Volatile Subsidy Outlook Post-2025

Direct hardware grants will sunset after 2025, leaving many public charging projects without the 40–60% capex co-funding that spurred the 2022–2024 build-out. Operators must pivot to dynamic pricing, grid-service revenues, and advertising partnerships. The funding gap raises the risk that charger deployment trails EV registrations from 2026 onward.

Distribution-Grid Permitting Bottlenecks

DSO approvals can delay commissioning by up to 12 months, jeopardizing Deutschlandnetz contract deadlines. The Federal Network Agency published streamlined timelines in 2024, yet enforcement remains patchy across 900 distribution grids.(2)Federal Network Agency, “Guideline on Grid Connection for Charging Points,” bundesnetzagentur.de Vertically integrated utilities such as EnBW and E.ON exploit internal grid-operator ties to accelerate projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Level: Megawatt Class Redefines Truck Logistics

Level 2 systems retained 49.25% of the German electric vehicle charging equipment market share in 2025, supplying residential and workplace sites where 7–22 kW meets overnight needs. Megawatt-class units above 350 kW will grow at a 30.6% CAGR through 2031, driven by EU truck CO₂ penalties that begin in 2025. The German electric vehicle charging equipment market size for Megawatt Class products is projected to rise from USD 165 million in 2026 to USD 625 million by 2031, indicating high-power systems are set to narrow the gap with legacy Level 2 volumes. ChargePoint and Kempower supply modular cabinets that scale from 1 MW to 3 MW, lowering entry capex and letting depot operators match capacity with fleet-growth milestones.

Competitive intensity in direct-current fast charging spans 50 kW to 350 kW dispensers. IONITY and Shell Recharge continue 150 kW-plus rollouts to guarantee 50-km spacing on key autobahn routes, while urban retailers install 50–150 kW units to capture dwell-time charging. Level 1 chargers below 3 kW remain a legacy niche. Hardware manufacturers that deliver liquid-cooled cables, grid-stabilizing inverter controls, and ISO 15118-20 software expect higher service revenues as fleets demand uptime guarantees above 98%.

By Installation Site: Transportation Hubs Capture Fleet Transition

Residential driveways and garages secured 61.60% of Germany's electric vehicle charging equipment market share in 2025, yet transportation hubs will outpace every other site category with a 27.9% CAGR. The German electric vehicle charging equipment market size attributed to airports and ports will jump from USD 205 million in 2026 to USD 702 million by 2031 as clean-air regulations electrify ground support and taxi fleets. Frankfurt Airport earmarked EUR 15 million for 500 charging points by 2026, offering suppliers opportunities for high-duty-cycle uptime contracts.

Commercial lots, supermarkets, and retail chains maintain steady volume as property owners chase footfall loyalty with mid-speed charging. Public curbside installations expand more slowly because permitting procedures stretch timelines and create high ground-rent costs. GEG 2023 obligations now extend EV-ready infrastructure to new office buildings and logistics warehouses, smoothing demand for pre-fabricated clusters that compress on-site labor costs.

By Application: Fleet Depot Charging Outpaces Consumer Segments

Home charging accounted for 70.55% of Germany's electric vehicle charging equipment market share in 2025, supported by household off-peak tariffs. Fleet and depot projects will post a 34.1% CAGR to 2031, beating every other application. The German electric vehicle charging equipment market size for depot systems is forecast to climb from USD 375 million in 2026 to USD 1.63 billion by 2031. DHL's and DB Schenker's electrification roadmaps rely on megawatt-scale architectures with dynamic load balancing to avoid grid upgrades that would otherwise derail project returns. Equipment vendors that couple hardware, energy-management software, and long-term financing gain an edge because fleet managers value total cost of ownership over sticker price.

Workplace charging preserves a niche as employers use free or discounted power as a hiring perk. Public urban chargers face utilization hurdles below 30% due to roaming complexity and inconsistent pricing. Highway corridor chargers enjoy predictable revenue from Deutschlandnetz contracts, though maintenance penalties linked to 99% uptime will challenge operators with under-resourced service teams.

Geography Analysis

Germany’s policy uniformity masks regional deployment gaps shaped by grid readiness and administrative efficiency. North Rhine-Westphalia and Bavaria secured the largest Deutschlandnetz allotments in 2024, leveraging strong highway density and automotive supply chains that spur corporate fleet demand. Berlin and Hamburg lead urban charger density thanks to municipal grants that layer on top of federal mandates, while Brandenburg and Mecklenburg-Vorpommern trail because low population density weakens business-case economics, and grid upgrades exceed EUR 100,000 per fast-charge site. Rural electrification grants launched in 2024 aim to bridge the divide by 2027.

The Master Plan Charging Infrastructure II targets 1 million public points by 2030, requiring a tenfold rise in annual installations versus 2024. EnBW and E.ON committed EUR 500 million to roll out 10,000 fast chargers by 2027, bundling renewable power to cut end-user tariffs by 15-20%.Bidirectional charging mandates make Germany a proving ground for vehicle-to-grid services. Early Hamburg pilots show households capturing EUR 30–50 per month in grid-balancing fees, though battery-warranty negotiations with carmakers remain incomplete. Suppliers offering ISO 15118-20-ready wallboxes position themselves for this revenue layer.

Municipal DSOs retain veto power through connection approvals. New federal guidelines cap preliminary assessments at four weeks, but enforcement varies across 900 operators, prolonging uncertainty for independent developers. Regional partnerships with utilities, therefore, become indispensable for equipment vendors seeking to cut lead times.

Analysis of the electric vehicle charging equipment market by Mordor Intelligence spans multiple other regional evaluations across Europe, North America, and South America, supported by country-level insights for Netherlands, Belgium, Spain, Italy, Sweden, and Norway, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The top five suppliers, ABB, Siemens, Alpitronic, Compleo, and Bosch, controlled roughly 40-45% of unit shipments in 2024, pointing to moderate concentration. Industrial conglomerates exploit decades-long utility relationships to secure municipal concessions, while pure-play specialists win tenders by pivoting faster on liquid-cooling, modular design, and software upgrades. Utilities, including EnBW, E.ON, Shell Recharge, and bp pulse, extend vertically into hardware to stabilize load profiles and package renewable-electricity contracts.(5)Siemens AG, “Sicharge Pro Launch,” siemens.com

White-space opportunities lie in megawatt-class depot charging, bidirectional residential hardware, and transportation hubs that demand ruggedized equipment. Kempower and ChargePoint target depots with satellite architectures that spread 1 MW across a dozen dispensers, yielding 30% lower per-vehicle costs. Alpitronic differentiates on 99% uptime guarantees critical to Deutschlandnetz penalties, whereas Wallbox and Webasto chase bidirectional-charging premium segments. For all players, software now delivers stickier revenue than metal: energy-management platforms, predictive maintenance, and grid-service integration top buyer wish lists.

Germany Electric Vehicle Charging Equipment Industry Leaders

ABB Ltd

Siemens AG

Tesla Inc.

ChargePoint Inc

Delta Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Wallbox released over-the-air upgrades enabling ISO 15118-20 bidirectional charging on the Pulsar Plus line, covering 50,000 units.

- October 2024: Mercedes-Benz AG and bp plc announced a joint venture to deploy 1,000 high-power charging points across Europe by 2026, with Germany receiving 300 units concentrated in urban retail locations and mixed-use developments.

- September 2024: The German Federal Ministry for Digital and Transport awarded the first 200 Deutschlandnetz fast-charging contracts, committing EUR 1.9 billion to deploy 900-plus sites by late 2025. Alpitronic GmbH and Compleo Charging Solutions AG secured 35% of initial awards, leveraging their focus on 99% uptime guarantees and liquid-cooled cable technology that supports 350 kW dispensing without thermal throttling.

- August 2024: EnBW AG announced a EUR 300 million investment to expand its HyperNetz fast-charging network to 2,000 locations by 2027, prioritizing urban centers and autobahn corridors.

Germany Electric Vehicle Charging Equipment Market Report Scope

Electric vehicle (EV) charging equipment refers to the infrastructure used to charge electric vehicles. The EV charging equipment plays a crucial role in the widespread adoption of electric vehicles. The availability of robust EV charging infrastructure is essential for overcoming range anxiety, a primary concern for potential EV buyers. It helps in reducing carbon emissions and improving air quality.

The German electric vehicle charging equipment market is segmented by charging level, installation site, and application. By charging level, the market is segmented into level 1, level 2, DC fast, ultra-fast, and megawatt-class. By installation site, the market is segmented by residential, commercial and retail, public municipal, and transportation hubs. By application, the market is segmented into home, workplace, public urban, highway corridor, fleet, and depot charging. For each segment, the market sizing and forecasts have been provided based on value (USD).

| Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) |

| DC Fast (50 to 150 kW) |

| Ultra-Fast (150 to 350 kW) |

| Megawatt Class (Above 350 kW) |

| Residential |

| Commercial and Retail |

| Public Municipal |

| Transportation Hubs (Airports, Ports) |

| Home Charging |

| Workplace Charging |

| Public Urban Charging |

| Highway Corridor/En-Route Fast Charging |

| Fleet and Depot Charging |

| By Charging Level | Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) | |

| DC Fast (50 to 150 kW) | |

| Ultra-Fast (150 to 350 kW) | |

| Megawatt Class (Above 350 kW) | |

| By Installation Site | Residential |

| Commercial and Retail | |

| Public Municipal | |

| Transportation Hubs (Airports, Ports) | |

| By Application | Home Charging |

| Workplace Charging | |

| Public Urban Charging | |

| Highway Corridor/En-Route Fast Charging | |

| Fleet and Depot Charging |

Key Questions Answered in the Report

How large will Germany’s charging-equipment opportunity be by 2031?

The Germany electric vehicle charging equipment market is projected to reach USD 2.79 billion by 2031, up from USD 1.63 billion in 2026.

Which charging-level segment will grow fastest this decade?

Megawatt Class systems above 350 kW will expand at a 30.6% CAGR to 2031 as truck fleets electrify.

What share of installations will remain residential by the end of the forecast?

Residential sites held 61.60% share in 2025, but their portion will decrease as transportation hubs and depots accelerate build-outs.

How will subsidy changes affect project economics after 2025?

The sunset of direct hardware grants raises capital costs, forcing operators to rely on dynamic tariffs, grid-service income, and vertically integrated energy packages.

Which companies currently lead on unit shipments?

ABB, Siemens, Alpitronic, Compleo, and Bosch together delivered roughly 40–45% of charging dispensers to the German market in 2024.

Page last updated on: