Germany Electric Bus Battery Pack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

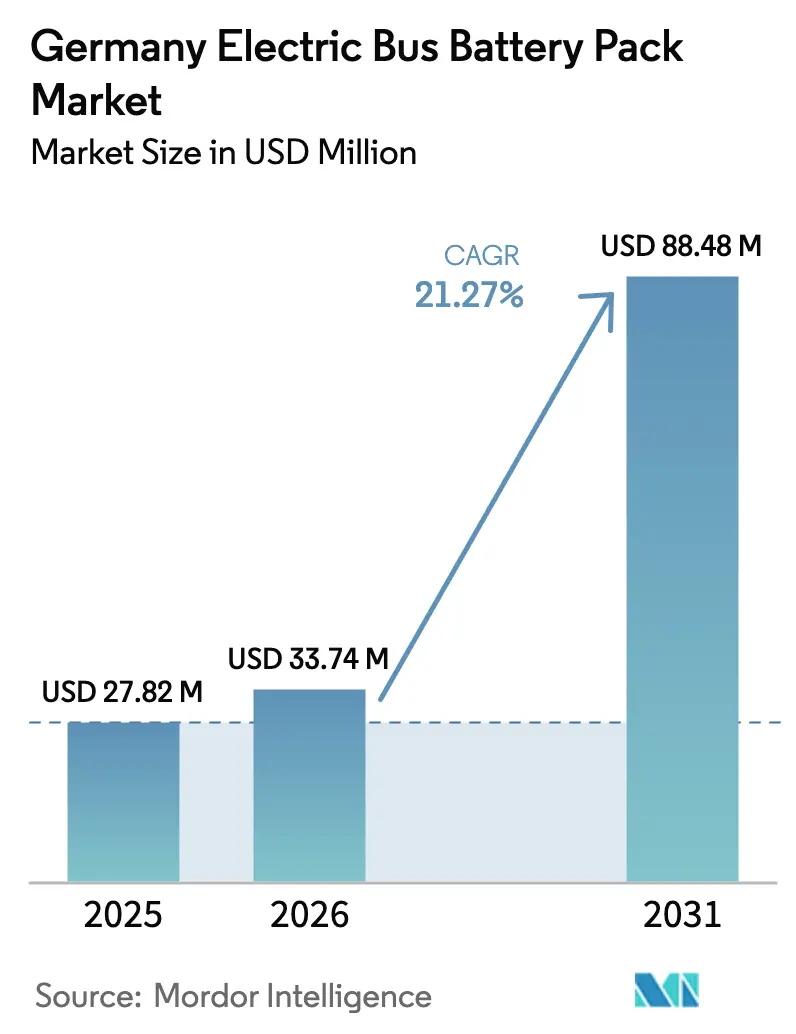

| Base Year Market Size (2025) | USD 27.82 Million |

| Market Size (2026) | USD 33.74 Million |

| Market Size (2031) | USD 88.48 Million |

| Growth Rate (2026 - 2031) | 21.27% CAGR |

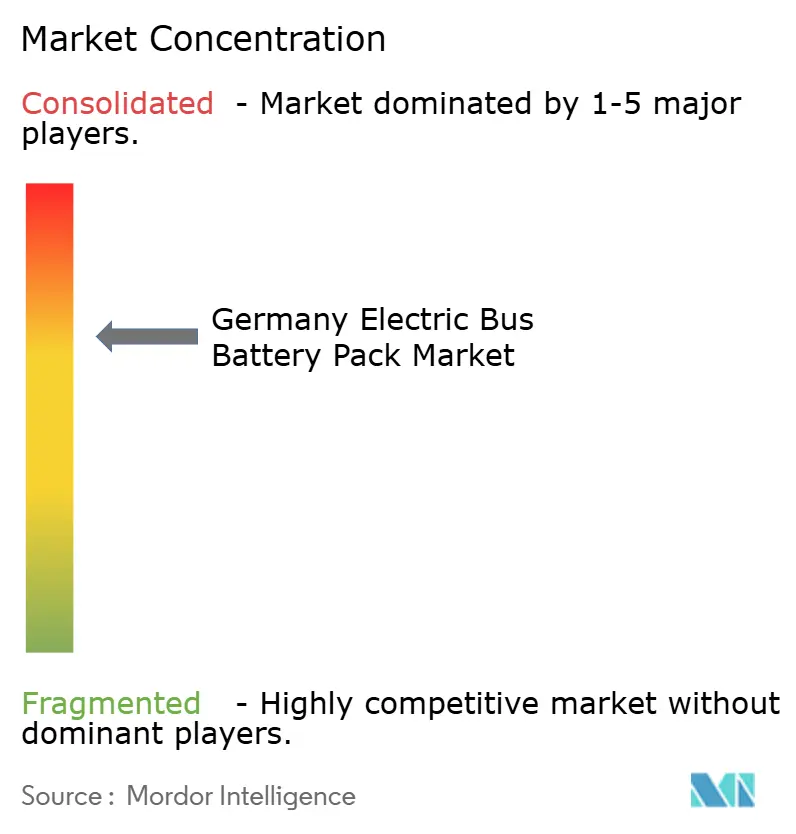

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Electric Bus Battery Pack Market Analysis by Mordor Intelligence

The German electric bus battery pack market size was valued at USD 27.82 million in 2025 and estimated to grow from USD 33.74 million in 2026 to reach USD 88.48 million by 2031, at a CAGR of 21.27% during the forecast period (2026-2031). The projection confirms rapid momentum fueled by stringent EU zero-emission procurement quotas, falling lithium-ion pack prices, and a wave of domestic gigafactory investments. Battery electric propulsion already dominates city fleets, and the lithium iron phosphate (LFP) chemistry has achieved cost parity with traditional alternatives, helping operators close the total-cost-of-ownership gap with diesel buses. Rising adoption of 800 V modular architectures further accelerates charging-time reductions, while depot-level energy storage integration opens ancillary revenue streams for transit agencies. Supply-chain localization led by Northvolt and CATL is trimming logistics costs and strengthening the security of supply. At the same time, critical-mineral price volatility and a temporary freeze in federal e-bus subsidies remain near-term hurdles.

Key Report Takeaways

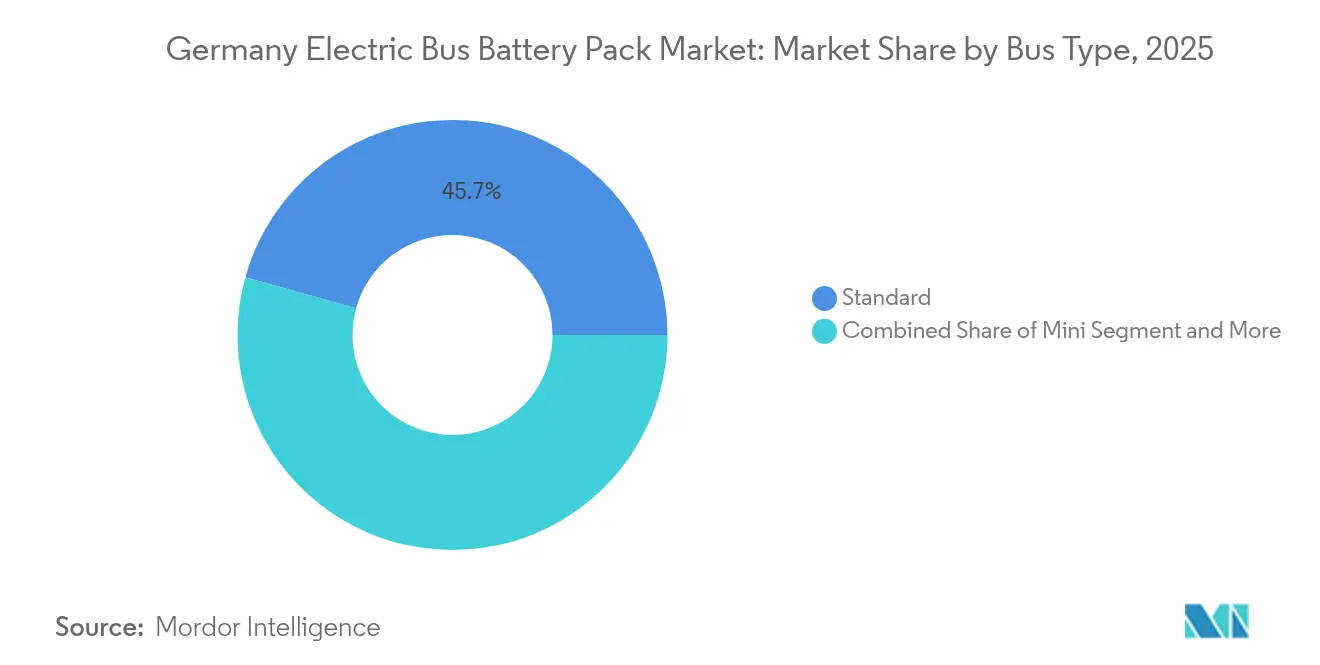

- By bus type, standard 12-meter models led with 45.68% revenue share in 2025; articulated 18-meter variants are projected to expand at a 21.79% CAGR to 2031.

- By propulsion, battery electric vehicles captured 85.62% of the German electric bus battery pack market share in 2025; they are also forecast to grow at a 22.54% CAGR through 2031.

- By battery chemistry, lithium iron phosphate held 41.58% share of the German electric bus battery pack market size in 2025, while lithium manganese iron phosphate is advancing at a 22.05% CAGR to 2031.

- By battery form, prismatic formats commanded a 50.36% share of the German electric bus battery pack market in 2025; pouch cells posted the highest 22.37% CAGR through 2031.

- By voltage class, the 600-800 V range accounted for 41.86% of the German electric bus battery pack market share in 2025; above-800 V systems show a 21.88% CAGR through 2031.

- By module architecture, cell-to-module designs held a 47.78% share of the German electric bus battery pack market in 2025; cell-to-pack configurations will grow at a 21.74% CAGR to 2031.

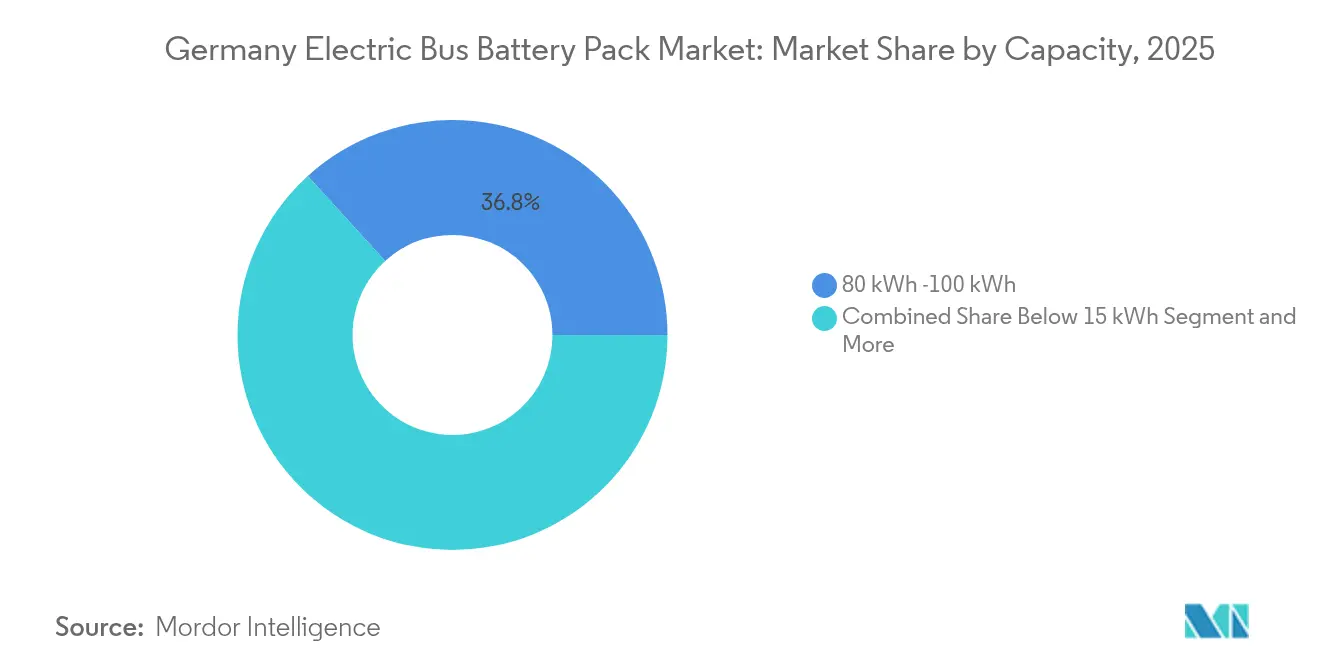

- By capacity, the 80-100 kWh bracket led with 36.75% of the German electric bus battery pack market share in 2025; packs above 150 kWh expand at a 21.99% CAGR through 2031.

- By component, cathode materials captured a 40.12% share of the German electric bus battery pack market in 2025; separators represent the fastest-growing component segment, with a 21.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Electric Bus Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Europe Zero-Emission Building (ZEB) Mandates | +5.2% | Germany, broader EU compliance | Medium term (2-4 years) |

| Standard 800V Modules | +4.1% | Germany, early adoption in premium bus segments | Medium term (2-4 years) |

| Fast Lithium Iron Phosphate/ Nickel Manganese Cobalt Oxide Cost Drop | +3.8% | Global, with German manufacturing benefits | Short term (≤ 2 years) |

| City Low Emission Zones and Diesel Bans | +3.1% | Germany, major metropolitan areas | Short term (≤ 2 years) |

| Domestic Gigafactory Growth | +2.9% | Germany, with spillover to neighboring EU states | Long term (≥ 4 years) |

| Depot Energy Storage | +2.7% | Germany, urban transit authorities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Standardized 800 V Modular Architectures

Next-generation electric vehicle systems are rapidly evolving, with new architectures facilitating much quicker charging. These innovations significantly reduce the time vehicles spend at depots, boosting operational efficiency for fleet operators. Standardized connector compatibility across the industry eases infrastructure upgrades, allowing depots to adopt high-powered charging solutions seamlessly. A leading manufacturer's decision to introduce advanced platforms across its electric bus range underscores the technology's maturity and readiness for broad adoption.

Battery pack designs are advancing, too, featuring scalable modules that simplify maintenance. This is a vital benefit for operators overseeing a mix of fleet ages and usage patterns. Together, these strides bolster a more resilient and serviceable electric vehicle ecosystem, particularly in commercial settings.

Rapid USD/kWh Decline of High-Capacity LFP and NMC Packs

Advancements in manufacturing and design have driven a steady decline in battery pack prices in recent years. As a result, high-capacity systems are becoming more affordable. This trend allows vehicle manufacturers to opt for larger battery configurations without facing significant cost hikes, especially in the bus segment.

Take, for instance, a leading electric coach model. It showcases how enhanced energy density can achieve a more extended driving range while maintaining competitive pricing. The industry is also gravitating towards more integrated battery designs, hinting at even greater cost savings in the future. Such innovations amplify the economic disparity between battery-electric and diesel vehicles, making the former increasingly appealing when considering the total cost of ownership.

Expansion of Domestic Gigafactories and Supply-Chain Localization

Northvolt’s EUR 4.5 billion (USD 4.96 billion) Schleswig-Holstein plant targets 60 GWh annual output by 2029, while MAN’s Nuremberg pack facility adds 50,000-100,000 units annually from 2025 [1]“E-bus orders surge ahead of EU quota,” Electrive, electrive.com. These projects shorten lead times, cut logistics emissions, and support custom pack configurations tuned to German duty cycles. Localization extends upstream to cathode refining and separator production, lowering import dependency and shielding operators from geopolitical supply risks. Integrated recycling lines within new factories help close the materials loop, a prerequisite for meeting future EU end-of-life regulations.

Depot-Level Energy-Storage Integration

Innovative transit agencies now deploy parked buses as grid assets, earning EUR 2,000 - 4,000 (USD 2,300 - 4,600) per vehicle annually through frequency-response markets[2]“Germany’s Renewable Energy Act and storage tariffs,” Clean Energy Wire, cleanenergywire.org. Hamburg’s Hochbahn leads with vehicle-to-grid pilots supported by favorable tariffs under Germany’s Renewable Energy Act. Sophisticated energy-management software balances fleet readiness with grid commitments, transforming battery packs into revenue generators that shrink payback periods and accelerate procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Bus Subsidy Freeze (KTF Ruling) | -2.1% | Germany, federal funding programs | Short term (≤ 2 years) |

| Mineral Price Volatility | -1.8% | Global, affecting German supply chains | Medium term (2-4 years) |

| Weak 2nd-Life Value Chain | -1.4% | Germany, EU recycling infrastructure | Long term (≥ 4 years) |

| Battery Welder Shortage | -1.2% | Germany, specialized manufacturing workforce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Federal E-Bus Subsidy Freeze (KTF Ruling)

The Constitutional Court's recent ruling has suspended a significant climate funding initiative, leading to delays in numerous electric vehicle orders. The verdict also eliminated subsidies that had previously offset many vehicle purchase costs. This development poses a particular challenge for smaller municipalities, which often lack alternative financing avenues and now risk lagging behind larger cities in their efforts to electrify fleets.

Although research funding is still accessible, incentives for procurement have been halted, resulting in a brief hiatus in public tenders. While political discussions are underway to address the matter, fleet operators must seek alternative financing methods, such as leasing or municipal borrowing, to advance their shift towards cleaner transportation.

Critical-Mineral Price Volatility

In recent years, the battery materials market has grappled with pronounced volatility. Key inputs, including lithium, cobalt, and nickel, have faced sharp price swings and supply disruptions. These challenges have notably influenced battery chemistries, especially in premium electric vehicles and intercity buses, where raw materials constitute a significant portion of overall pack costs[3]Henry Sanderson, “Mineral price volatility hits EV supply chains,” Financial Times, ft.com.

In response to this uncertainty, manufacturers and fleet operators are pivoting towards more stable chemistries and exploring financial hedging. Yet, budgeting remains a challenge amidst these unpredictable conditions. While domestic recycling is a promising solution to mitigate global supply risks, commercial-scale operations are still years away. In the interim, the sector continues to navigate a maze of fluctuating costs and tight supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bus Type: Standard Models Anchor Demand

Standard 12-meter buses generated 45.68% of the German electric bus battery pack market in 2025, underpinning the baseline volume that suppliers rely on. These vehicles balance 80-120 passenger capacity with maneuverability essential for Germany’s dense city centers. Their typical 200-350 kWh battery requirement aligns with mass-produced LFP packs, securing cost efficiencies critical for municipal budgets. Growth in this category remains healthy but steady as most large cities have already standardized on 12-meter fleets for core routes.

Articulated 18-meter buses display a 21.79% CAGR through 2031, reflecting route consolidation in Berlin, Munich, and Hamburg. Operators choose larger buses to maximize driver utilization and reduce congestion. Battery packs in the 400-600 kWh range dominate, creating opportunities for high-capacity suppliers and favoring cell-to-pack layouts that optimize energy density. Smaller categories such as mini and microbuses retain niche roles for rural and paratransit services, while midi buses fill mid-volume needs in secondary cities. Technology spillovers from standard and articulated formats accelerate performance enhancements across all sub-segments, keeping the German electric bus battery pack market on an innovation trajectory.

By Propulsion Type: Battery Electric Supremacy

Battery electric buses held 85.62% share in 2025 and will sustain a 22.54% CAGR to 2031, reinforcing Germany’s commitment to fully zero-tailpipe fleets. Operators appreciate up to 90% well-to-wheel efficiency and simplified maintenance compared with hybrid systems. The German electric bus battery pack market size for fully electric models benefits from EU quotas that effectively eliminate combustion components in city environments.

Plug-in hybrids linger primarily as a hedge against charging infrastructure gaps or for extended regional routes. Still, their market relevance dwindles as winter-range concerns ease and depot charging networks expand. Diesel price volatility and the proliferation of low-emission zones speed hybrid retirements. In response, suppliers shift R&D budgets almost entirely to full-battery architectures, accelerating pack-level energy-density gains that make hybrids increasingly redundant.

By Battery Chemistry: LFP Dominance, LMFP Momentum

LFP (Lithium Iron Phosphate) chemistry captured a 41.58% share in 2025, thanks to its proven safety and long cycle life, which are vital for high-occupancy vehicles where thermal stability is paramount. German OEMs value the chemistry’s benign failure mode and compatibility with stringent fire-safety regulations. Cost advantages over nickel-rich variants further solidify LFP's position in the German electric bus battery pack market.

LMFP (Lithium Manganese Iron Phosphate) is expected to record the fastest 22.05% CAGR through 2031, adding manganese to increase energy density by 15-20% without compromising safety. This makes LMFP attractive for articulated and intercity routes needing additional range. NMC (Nickel Manganese Cobalt Oxide) chemistries continue serving premium segments, yet face competitive pressure as successive LFP iterations narrow performance gaps. Lithium titanate remains in the niche for ultra-fast charging use cases, while NCA (Nickel Cobalt Aluminum Oxide) chemistry’s cobalt content limits adoption due to ESG scrutiny.

By Capacity: Upsizing for All-Day Operation

Packs in the 80-100 kWh bracket led with 36.75% share in 2025, tightly matching standard city buses' daily 150-200 km duty cycles. This capacity sweet spot minimizes both pack cost and charging infrastructure requirements. However, segments above 150 kWh post a 21.99% CAGR as articulated buses and route optimization projects demand all-day range without opportunity charging.

Larger capacities allow operators to dispense with costly in-route chargers and simplify depot layouts. Hamburg’s decision to standardize on 350 kWh packs underscores the operational appeal. Smaller capacity segments remain relevant for airport shuttles or downtown circulators, while mid-range sizes offer flexibility for cities transitioning to full electrification.

By Battery Form: Prismatic Strength, Pouch Agility

Prismatic cells had a 50.36% share in 2025, owing to rugged construction and mature supply chains. Their rectangular geometry simplifies module assembly and thermal management, attributes prized in heavy-duty applications.

Pouch cells grow 22.37% annually, motivated by superior gravimetric energy density and lighter housing. Daimler’s next-generation eCitaro leverages pouch formats to shave weight and extend range. Cylindrical cells linger for specialty modular packs but cannot match prismatics for volumetric efficiency at commercial-vehicle scale. The result is a balanced market where form-factor choice hinges on OEM design philosophy and specific operating constraints.

By Voltage Class: 600-800 V Standard, High-Voltage Horizon

The 600-800 V class owned 41.86% of the German electric bus battery pack market in 2025, delivering 150-250 kW charging speeds that align with today’s depot infrastructure. Safety protocols and technician training are already entrenched at this voltage level, lowering adoption hurdles.

Yet above-800 V systems exhibit a 21.88% CAGR as operators chase under-one-hour turnarounds and future-proof depot investments through 2031. These ultra-high-voltage packs promise reduced cable weights and higher inverter efficiency, but demand advanced insulation and stricter service procedures. Sub-400 V architectures will gradually phase out except in budget-constrained rural fleets.

By Module Architecture: CTM Reliability, CTP Efficiency

Cell-to-module (CTM) designs retained 47.78% share in 2025, favored for ease of field service because defective modules can be swapped without pulling entire packs. German operators prioritize maintainability to maximize fleet uptime, underpinning CTM’s resilience.

Cell-to-pack (CTP) grows 21.74% yearly, leveraging fewer parts and 13% higher volumetric energy density thanks to the elimination of module housings. CATL’s Qilin platform catalyzes OEM interest by demonstrating faster assembly and enhanced thermal uniformity. Module-to-pack options fill an interim niche but will cede ground as manufacturing moves toward full integration.

By Component: Cathode Cost Center, Separator Surge

Cathodes represented 40.12% of the component value in 2025, reflecting their significant role in performance and raw material economics. LFP (Lithium Iron Phosphate), LMFP (Lithium Manganese Iron Phosphate), and NMC (Lithium Nickel Manganese Cobalt Oxide) variants dominate the bill of materials, and advances in high-manganese formulations aim to curb nickel and cobalt dependency.

Separators enjoy a 21.52% CAGR as ceramic-coated films enable higher voltage operation and bolster safety through 2031. Domestic separator production capacity is ramping to align with gigafactory rollouts, reinforcing supply security. Anode, electrolyte, and current-collector innovations also contribute, but breakthroughs in cathode and separator technology most directly influence cost and safety, key purchasing criteria for German transit agencies.

Geography Analysis

Germany anchors the German electric bus battery pack market through aggressive city-level electrification commitments backed by EU procurement law. Berlin, Munich, Hamburg, and Cologne plan over 8,000 e-bus acquisitions by 2027, securing predictable demand for local pack assemblers. Municipal operators in northern Germany favor large overnight-charged packs that maximize energy throughput in extended daily schedules, whereas southern states prioritize mid-range capacities for intercity services.

Domestic manufacturing advantages proliferate as Northvolt’s Schleswig-Holstein cell plant and MAN’s Nuremberg pack facility reach scale, lowering transport costs and aligning production with German labor standards. Supply-chain proximity allows rapid design iterations tailored to winter performance and local regulatory nuances, giving German suppliers an edge over Asian imports. Cross-border spillover extends to Austria and Denmark, where German-built packs equip regional bus contracts seeking established technology.

Eastern European modernization funds create a secondary market that German producers can tap with proven LFP technology and service expertise. EU regulatory harmonization ensures technical interoperability, positioning Germany as a central hub for continental battery-electric bus solutions. Overall, geographic clustering around northern production centers reinforces Germany’s role as the largest consumer and primary exporter within Europe’s commercial-EV battery ecosystem.

Competitive Landscape

Asian incumbents remain influential, yet localization tilts bargaining power toward European alliances. CATL leverages partnerships with Mercedes-Benz and MAN to embed its LFP and LMFP chemistries in flagship German models, securing early design wins and economies of scale. Northvolt counters a gigafactory committed to commercial-vehicle cells, offering OEMs a low-carbon European supply alternative. The German electric bus battery pack market thus reflects moderate concentration, with a handful of global suppliers covering most city tenders.

Strategic playbooks emphasize vertical integration. BYD bundles battery supply with complete bus platforms, challenging legacy OEMs to secure independent pack sources or co-invest in internal lines. European bus makers increasingly lock in long-term cell contracts, while component firms develop advanced thermal-management and vehicle-to-grid modules that differentiate beyond commodity cells.

Competitive vectors now pivot around total cost of ownership, depot-integration services, and life-cycle management rather than raw energy density. Suppliers can combine 800 V architectures with grid-services software to obtain defensible margins. Intellectual property in safety algorithms and real-time diagnostics becomes a key moat amid otherwise converging chemistry choices. Market entrants face high capital barriers but can carve niches in second-life repurposing, rural microbus packs, or specialty separators.

Germany Electric Bus Battery Pack Industry Leaders

BYD Company Ltd.

Contemporary Amperex Technology Co. Ltd. (CATL)

Samsung SDI Co. Ltd.

LG Energy Solution Ltd.

Northvolt AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: At its EUR 100 million (USD 115.2 million) plant in Nuremberg, MAN has commenced production of battery packs, targeting an annual output of 100,000 units. The facility also includes on-site recycling capabilities, emphasizing sustainability in its operations.

- November 2024: Germany's largest single e-bus procurement sees Hamburg's Hochbahn ordering 350 eCitaro buses, each equipped with 400 kWh battery packs and upgraded for depot charging. This significant order highlights the city's commitment to sustainable public transportation and reducing carbon emissions.

Germany Electric Bus Battery Pack Market Report Scope

The Germany Electric Bus Battery Pack Market Report is Segmented by Bus Type (Mini/Microbus, and More), Propulsion Type (Battery Electric, and More), Battery Chemistry (LFP, and More), Capacity (Below 15 kWh, and More), Battery Form (Cylindrical, and More), Voltage Class (Below 400V, and More), Module Architecture (CTM, and More), Component (Anode, and More). Market Forecasts are Provided in Terms of Value (USD).

| Mini / Microbus (<8 meter) |

| Midi (8 - 10.5 meter) |

| Standard / 12-meter |

| Articulated (18 meter) |

| Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) |

| NMC (Nickel Manganese Cobalt Oxide) |

| NCA (Nickel Cobalt Aluminum Oxide) |

| LTO (Lithium Titanium Oxide) |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) |

| Below 15 kWh |

| 15 - 40 kWh |

| 40 - 60 kWh |

| 60 - 80 kWh |

| 80 - 100 kWh |

| 100 - 150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Below 400 V (48 - 350 V) |

| 400 - 600 V |

| 600 - 800 V |

| Above 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| By Bus Type | Mini / Microbus (<8 meter) |

| Midi (8 - 10.5 meter) | |

| Standard / 12-meter | |

| Articulated (18 meter) | |

| By Propulsion Type | Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle | |

| By Battery Chemistry | LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) | |

| NMC (Nickel Manganese Cobalt Oxide) | |

| NCA (Nickel Cobalt Aluminum Oxide) | |

| LTO (Lithium Titanium Oxide) | |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) | |

| By Capacity | Below 15 kWh |

| 15 - 40 kWh | |

| 40 - 60 kWh | |

| 60 - 80 kWh | |

| 80 - 100 kWh | |

| 100 - 150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Below 400 V (48 - 350 V) |

| 400 - 600 V | |

| 600 - 800 V | |

| Above 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include is variety of buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 3

- Vehicle Type - Vehicle type considered under this segment include commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms