Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

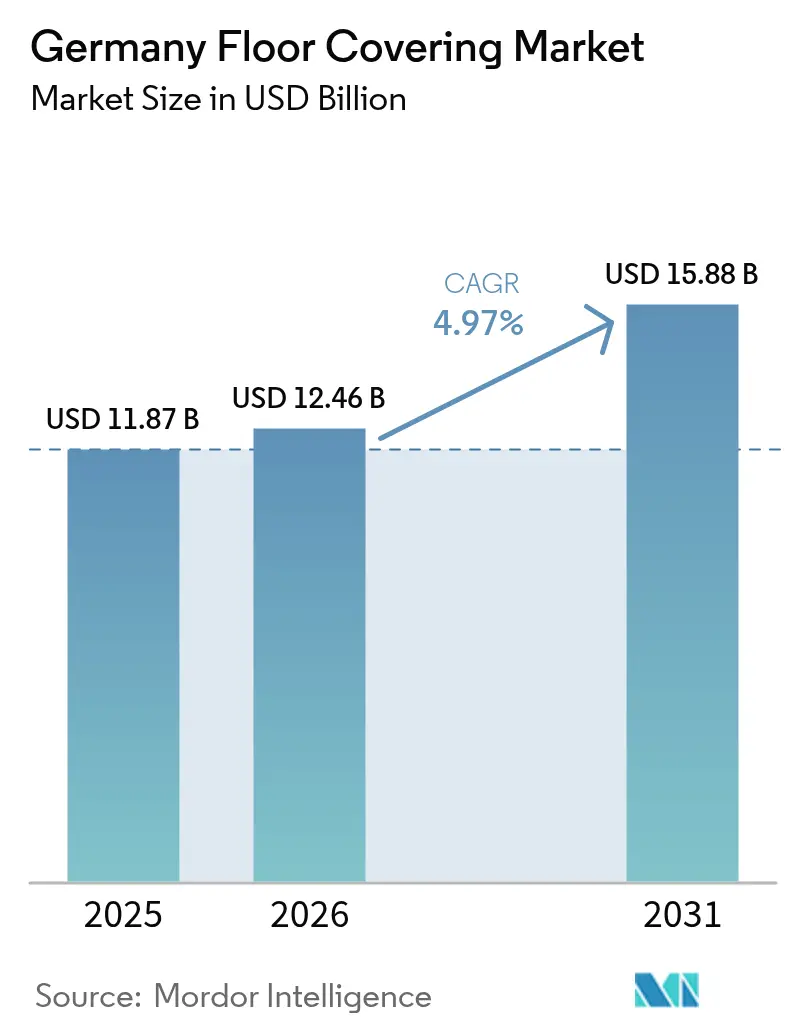

| Base Year Market Size (2025) | USD 11.87 Billion |

| Market Size (2026) | USD 12.46 Billion |

| Market Size (2031) | USD 15.88 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Floor Covering Market Analysis by Mordor Intelligence

The Germany floor covering market size was valued at USD 11.87 billion in 2025 and estimated to grow from USD 12.46 billion in 2026 to reach USD 15.88 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031). Government-backed renovation subsidies, shifting consumer priorities toward indoor air quality, and accelerating e-commerce adoption combine to offset the drag from Germany’s broader construction slowdown. Subsidized efficiency refurbishments are funneling discretionary budgets into flooring categories certified for low emissions and underfloor-heating compatibility, while premium wood and high-performance vinyl products win share on aesthetics and lifecycle value [1]Bundesministerium für Wohnen, Stadtentwicklung und Bauwesen, “Gebäudeenergiegesetz (GEG),” bmwsb.bund.de. . Competitive intensity stays moderate, with the top five vendors controlling roughly 45% of turnover yet leaving ample room for mid-sized sustainability specialists to capture niche demand. Geographically, the Germany floor covering market benefits from South Germany’s premium renovation appetite and East Germany’s rapid Tier-2-city uplift, creating a two-speed expansion pattern that suppliers must navigate. Online channels are reshaping the path to purchase as Amazon and omnichannel DIY chains refine virtual visualization tools and same-day click-and-collect models. Meanwhile, installer shortages and hardwood input volatility act as near-term brakes yet also spur innovation in click-lock formats and engineered alternatives that conserve material while easing labor bottlenecks.

Key Report Takeaways

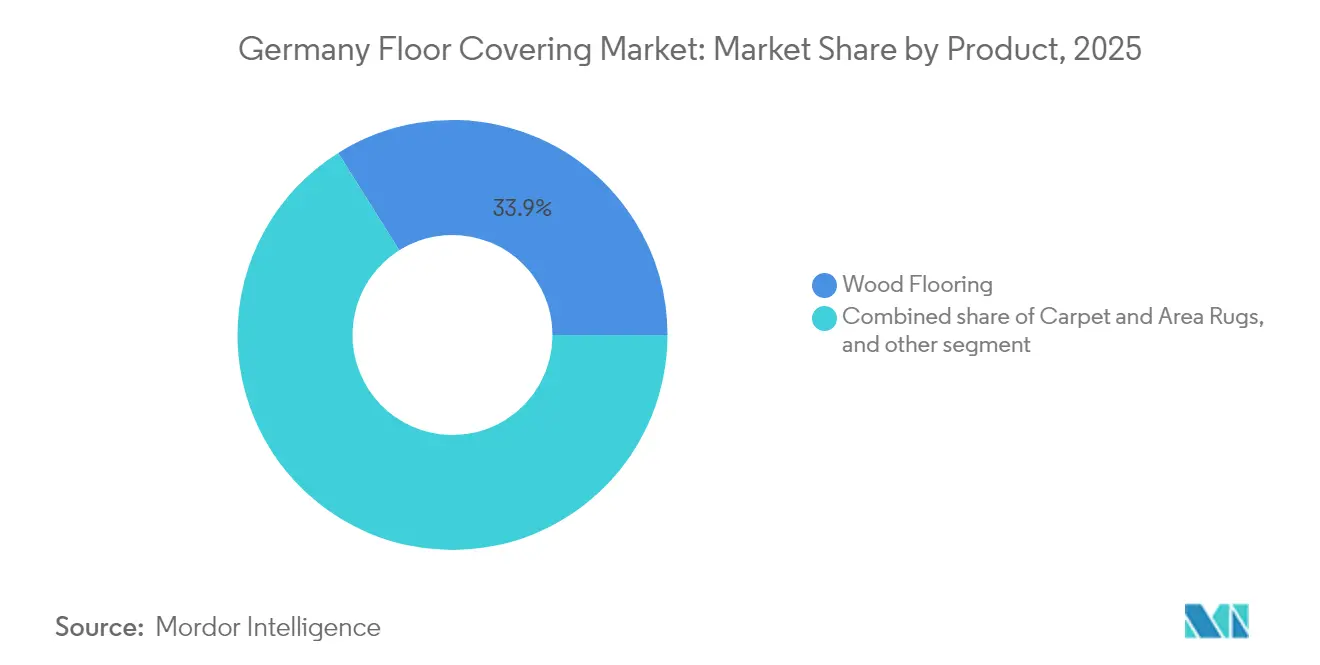

- By product, wood flooring led with 33.92% Germany floor covering market share in 2025, while vinyl/SPC-LVT is projected to expand at a 7.75% CAGR through 2031.

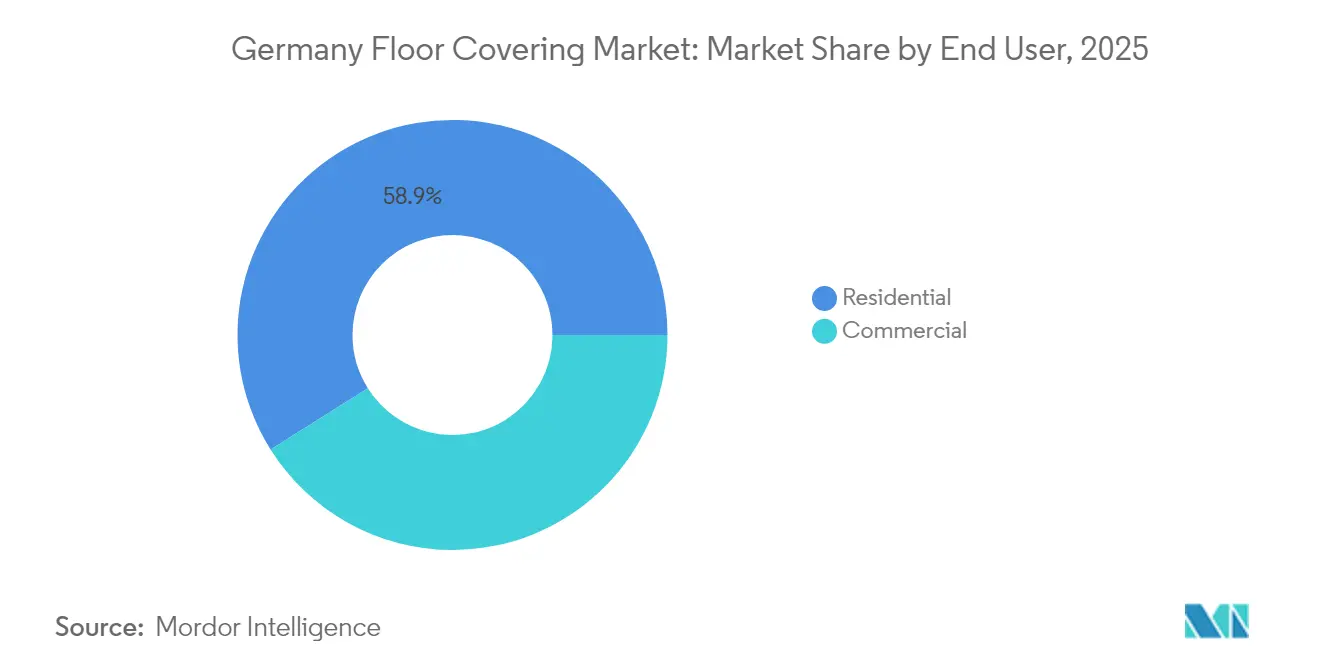

- By end user, the residential segment accounted for 58.94% of the Germany floor covering market size in 2025, whereas commercial applications are tracking a 5.66% CAGR to 2031.

- By distribution channel, home centers held 36.84% of the Germany floor covering market size in 2025, and online stores post the quickest growth at 10.73% CAGR through 2031.

- By region, South Germany captured 30.86% of the Germany floor covering market share in 2025, whereas East Germany is set for a 7.64% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Re-urbanisation-led renovation wave | +1.2% | East & Central Germany (Leipzig, Dresden, Erfurt) | Medium term (2-4 years) |

| Subsidized energy-efficient refurbishments | +1.8% | National, higher in residential | Short term (≤ 2 years) |

| Low-VOC and recyclable flooring demand | +0.9% | National, premium clusters in South & West | Long term (≥ 4 years) |

| Underfloor heating compatibility preference | +0.7% | National, skewed to new builds and major renovations | Medium term (2-4 years) |

| Post-COVID DIY boom boosting home-centre traffic (mainstream) | +0.6% | National, especially suburban areas with high homeownership | Short term (≤ 2 years) |

| Spread of hybrid work is shrinking new-office demand (mainstream) | –0.5% | Urban centres with slowing commercial real estate activity | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Re-urbanisation-led renovation wave in Tier-2 cities

Smaller German cities are experiencing a pronounced refurbishment upswing as young households migrate from rural districts, stimulating elevated replacement cycles in the Germany floor covering market [2]Postbank, “Wo Eigentumswohnungen im Bestand noch wertvoller werden,” postbank.de. . Property investors in Leipzig and Dresden prioritize fast-install LVT and laminate to shorten vacancy periods and meet the design expectations of digitally native tenants. The East German economy, although contracting 0.1% in 2024, shows flooring resilience because renovation outlays are less cyclical than new construction starts. Lower labor rates in these regions further improve project ROI, nudging landlords to upgrade surfaces sooner than depreciation schedules dictate. Manufacturers attuned to mid-market pricing and click-lock formats, therefore, gain a volume tailwind. The trend also diversifies geographic revenue streams, reducing suppliers’ dependence on the mature South-West cluster.

Subsidized energy-efficient refurbishments under BEG program

The BEG framework grants 15-20% rebates on envelope upgrades, injecting fresh capital into flooring budgets and uplifting premium segments of the Germany floor covering market. Homeowners aiming for maximum subsidy increasingly specify materials compatible with underfloor heating, pushing engineered wood and high-density vinyl with certified thermal conductivity. Complementary tax deductions—20% of renovation spend spread across three years—further amplify payback for efficiency-oriented materials. Certification requirements elevate the role of branded suppliers, able to document emission levels and lifecycle performance. The program’s short-term horizon concentrates demand into a two-year burst, allowing capable producers to lock in share gains ahead of eventual subsidy tapering. Installers, meanwhile, favor floating floors that speed project completion within tight grant deadlines.

Growing demand for low-VOC and recyclable flooring

Consumers now rank indoor air safety alongside visual appeal, inducing a measurable shift toward products meeting the EU’s 0.062 mg/m³ formaldehyde cap effective August 2026 [3]Fraunhofer WKI, “EU-wide regulation of formaldehyde limits from 2026,” wki.fraunhofer.de. . Suppliers such as Forbo, whose portfolio averages 37% recycled content, convert sustainability into pricing power and specification wins on certified green buildings. Circular-economy take-back schemes like Tarkett’s ReStart, already recycling 750 tons annually, resonate with corporate ESG targets in the Germany floor covering industry. Rating systems, including LEED and BREEAM, increase materials-related weightings, encouraging architects to embed low-VOC floors early in design. The premium paid for environmentally advanced surfaces narrows as scale economies and recycled feedstock uptake reduce cost differentials. Long-term momentum, therefore, remains highly positive, with impact spread across residential and commercial refurbishments.

Germany’s Gebäudeenergiegesetz stipulates 65% renewable content for heating systems in new builds, accelerating the adoption of underfloor heating that demands thermally conductive floor layers. Engineered wood, ceramic tile, and LVT products engineered for stability under temperature cycles gain incremental share in the Germany floor covering market. Traditional carpet and thick solid wood lose relevance except where decoupling mats solve conductivity gaps. Floating installation formats proliferate because they accommodate expansion while lowering labor inputs amid installer shortages. Retailers capitalize by bundling heating panels and floor coverings into turnkey packages, reinforcing the compatibility theme. Over the medium term, value propositions hinge on certified R-values and moisture-barrier technologies that balance energy savings with acoustic comfort.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe installer labor shortage | -1.4% | National, most acute in sanitary, heating & roofing trades | Short term (≤ 2 years) |

| Soaring hardwood input prices | -0.8% | National, premium wood segments | Medium term (2-4 years) |

| Sluggish residential permits after 2023 interest-rate hikes | -1.0% | National, more pronounced in new-build housing markets | Short to medium term (1–3 years) |

| Stringent EHS compliance costs for PVC flooring makers | -0.6% | National, impacting mid-tier and budget PVC product lines | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Severe installer labor shortage

The Germany floor covering market contends with more than 15,000 vacancies across floor-related trades, lengthening project lead times and inflating labor costs by 7.9% in 2024 [4]Institut der deutschen Wirtschaft, “Fachkräftereport März 2025,” iwkoeln.de.. Developers routinely wait six to eight weeks for certified crews, encouraging end users to gravitate toward DIY-friendly click-lock planks. Manufacturers exploit the gap through pre-finished surfaces and integrated underlays that compress installation windows. Training initiatives from trade associations are ramping up, but will take time to ease shortages. Consequently, volume upside in premium segments that demand expert fitting remains capped in the near term. Retailers mitigate disruption by curating vendor-certified installers and digital scheduling platforms to streamline workforce allocation.

Soaring hardwood input prices

Global supply swings pushed hardwood import volumes down 32% and revenue down 15% in 2023, squeezing German producers’ margins. Oak, accounting for 85% of hardwood sales, sees acute pressure as rival industries compete for limited timber. Engineered substrates and decorative laminates emerge as substitutes, with Egger’s Decorative Collection 24+ offering 300 designs that mimic premium species at a lower cost. Price volatility nudges retailers to diversify assortments into rigid vinyl and laminate lines that deliver wood visuals without raw-material risk. Consumer willingness to pay for genuine hardwood narrows, shifting market share toward resilient surfaces. Over the medium term, sustainable forestry certifications and longer procurement contracts may stabilize supply, yet elasticity will continue favoring engineered alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wood Dominance Faces Vinyl Innovation

Wood flooring held 33.92% of the Germany floor covering market share in 2025, reflecting the material’s perceived authenticity and lasting value in renovation projects. Vinyl/SPC-LVT, however, exhibits the strongest momentum with a 7.75% CAGR, underpinned by waterproof cores and rapid-click formats that appeal to both professionals and DIY consumers. The Germany floor covering market size allocated to ceramic tiles remains sizable in commercial realms, where durability and maintenance override softness. Laminate segments stabilize as digital print advancements close the realism gap with hardwood, while carpet retracts amid allergy concerns and cleaning effort. Manufacturers such as Windmöller push PVC-free bio-vinyl to reconcile performance with recycling mandates, and Tarkett’s linoleum revival adds a natural, carbon-neutral alternative. Cross-category innovation centers on acoustic upgrades and integrated vapor barriers that broaden application scope.

Demand elasticity skews toward mid-priced engineered wood lines that minimize waste of premium timber and meet underfloor heating criteria. Vinyl developers focus on rigid, dent-resistant cores suited to high-traffic commercial environments yet visually aligned with residential aesthetics. Laminate producers invest in high-pressure overlay technologies that lift impact resistance and water tolerance, positioning the category against entry-level LVT. Stone and porcelain tile maintain niche appeal in luxury builds and public facilities, demanding high thermal mass for energy regulation. The product landscape, therefore, continues to fragment, giving multi-category vendors cross-selling advantages while allowing specialists to differentiate via sustainability credentials and advanced installation systems.

By End User: Residential Renovation Drives Commercial Growth

Residential spending accounted for 58.94% of the Germany floor covering market size in 2025 as homeowners tapped subsidies to upgrade outdated surfaces. Renovation cycles shorten further as energy-audit triggers align floor replacement with insulation and heating overhauls. Commercial demand, though smaller today, is forecast to expand at a 5.66% CAGR through 2031, propelled by flexible office retrofits and health-care facility upgrades that prioritize hygienic, low-VOC surfaces. Hybrid work reshuffles square-footage needs yet bolsters sales of high-spec home-office floors with acoustic damping and ergonomic warmth. Hospitality and retail segments seek resilient designs offering rapid turnover and brand-specific aesthetics, with LVT and carpet tiles allowing phased replacement without full closure.

Builders and facility managers in commercial settings increasingly specify cradle-to-grave-certified materials to satisfy tenant ESG requirements. Residential buyers value visual continuity across open-plan spaces, pushing wider plank formats and matte finishes that integrate with Scandinavian-inspired interiors. The end-user split, therefore, guides channel strategy: DIY-friendly retailers capture residential impulse upgrades, while contract dealers and project distributors cultivate specification influence in commercial schemes. Training programs for installers gain urgency across both domains to maintain artistry quality amid labor scarcity.

By Distribution Channel: Digital Transformation Accelerates

Home centers captured 36.84% of the Germany floor covering market size in 2025, leveraging showroom experience and add-on installation services. Online stores, though smaller, post a 10.73% CAGR as virtual reality estimators and free sample logistics reduce tactile barriers. Amazon’s USD 1.3 billion gross DIY turnover underscores how platform economics can cannibalize legacy volumes, especially for commodity laminates and adhesive accessories. Specialty retailers defend share by curating premium assortments and in-store design consultation, while flagship stores operate as brand theaters to reinforce product narratives.

Omnichannel pioneers integrate inventory systems to enable online reservation with same-day pickup, limiting delivery wait times that frustrate renovation schedules. Digital configurators offering instant bill-of-materials facilitate upselling of underlays, trims, and maintenance kits. Manufacturers experiment with direct-to-consumer microsites featuring subscription-based floor-care consumables, extending lifetime revenue per square meter. The distribution mix continues shifting toward a hybrid model where physical touchpoints anchor complex purchases and online platforms handle replenishment and standard SKUs.

Geography Analysis

South Germany generated 30.86% of Germany floor covering market share in 2025 owing to Bavaria and Baden-Württemberg’s affluent households and diversified industry base. Premium wood, natural stone, and designer tiles resonate with regionally popular Alpine and Mediterranean interior themes. East Germany, while only mid-teens in current size, records the fastest 7.64% CAGR, powered by Leipzig’s 1.9% annual property appreciation and subsidy-fuelled urban renewal. West Germany’s mature markets in North Rhine-Westphalia and Hesse exhibit steadier growth anchored by ongoing retrofit programs in large housing associations. North Germany, centered on Hamburg and Bremen, gains from maritime logistics expansion and offshore wind infrastructure, yet colder climate tilts preferences toward high-insulation laminates and carpet tiles.

Public infrastructure outlays of USD 545 billion equivalent over 2025-2030 funnel indirect demand into commercial floor upgrades, particularly in transport hubs and education facilities. Building permit issuance down 16.8% in 2024 points to prolonged new-build softness, keeping renovation at the forefront across all regions. Regional cost differentials influence product mix: East German buyers favor value-engineered laminates and LVT, whereas South German consumers opt for multi-layer oak engineered planks with brushed finishes. Supplier localization strategies, such as Egger’s Heiligengrabe laminate plant in Brandenburg, improve lead times and resonate with regional employment priorities.

Competitive Landscape

The Germany floor covering market remains moderately concentrated, with Tarkett holding the leading position, followed by Forbo, Mohawk’s Quick-Step, Parador, and Egger. These top five players collectively account for a significant portion of the market, reflecting strong brand presence and established distribution networks. Tarkett’s ReStart recycling initiative exemplifies circular-economy positioning and helps secure large corporate tenders seeking closed-loop material streams. Forbo’s 70% carbon-intensity reduction per square meter since 2004 shapes its appeal to public sector refurbishments subject to life-cycle-cost scoring. Quick-Step continues to push water-resistant laminate via patented hydroseal technology, targeting entry-level apartment turnovers. Parador leverages made-in-Germany branding, while Egger’s Decorative Collection 24+ ties digital planning tools to specifier workflows and boosts design-to-order velocity.

Strategic moves in 2025 center on consolidation and brand integration: Tarkett seeks to go private at EUR 20 per share to streamline decision cycles, and Kährs folds Upofloor into its master brand to pool R&D on PVC-free solutions. Distribution alliances intensify as Transom Capital merges Virginia Tile with Galleher to extend specialty reach into Central Europe, challenging domestic wholesalers that rely on regional warehouses. Digital engagement accelerates across the field: Egger’s VR room visualizer and Forbo’s carbon footprint calculators differentiate buying journeys and feed data to architects’ BIM platforms, reinforcing pull-through on multiyear project pipelines.

An emerging white space involves smart-floor sensors embedded in luxury vinyl for usage analytics in commercial buildings, with German prop-tech startups piloting solutions in corporate campuses. Suppliers also race to develop bio-based polyurethane wear layers that satisfy looming microplastic regulations. Overall, market leadership increasingly hinges on circular value chains, digital services, and rapid design refresh cycles rather than pure capacity scale.

Germany Floor Covering Industry Leaders

Tarkett S.A.

Forbo Holding AG

Mohawk Industries (Quick-Step)

Parador GmbH

Egger Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tarkett Group issued a draft offer to buy remaining shares at EUR 20 (USD 24), aiming to take the company private and accelerate strategic pivots.

- June 2024: Transom Capital acquired Virginia Tile and merged it with Galleher, forging a cross-border distributor focused on professional channels.

- February 2024: Egger rolled out its Decorative Collection 24+ with 68 new designs and biennial update cadence.

Germany Floor Covering Market Report Scope

The report provides a detailed study, with the underlying factors for the variations in the floor covering market growth trends. The report also provides a competitive landscape, covering company market shares, with detailed profiling for major revenue-contributing companies.

By Product

| Carpet and Area Rugs |

| Wood Flooring |

| Ceramic Tiles Flooring |

| Laminate Flooring |

| Vinyl Flooring |

| Stone Flooring |

| Other Products |

By End User

| Commercial |

| Residential |

By Distribution Channel

| Home Centers |

| Flagship Stores |

| Specialty Stores |

| Online Stores |

| Other Distribution Channels |

By Region Germany

| North Germany |

| West Germany |

| South Germany |

| East Germany |

| By Product | Carpet and Area Rugs |

| Wood Flooring | |

| Ceramic Tiles Flooring | |

| Laminate Flooring | |

| Vinyl Flooring | |

| Stone Flooring | |

| Other Products | |

| By End User | Commercial |

| Residential | |

| By Distribution Channel | Home Centers |

| Flagship Stores | |

| Specialty Stores | |

| Online Stores | |

| Other Distribution Channels | |

| By Region Germany | North Germany |

| West Germany | |

| South Germany | |

| East Germany |

Key Questions Answered in the Report

How big is the Germany floor covering market in 2026?

It is valued at USD 12.46 billion and is projected to reach USD 15.88 billion by 2031, reflecting a 4.97% CAGR.

Which product commands the largest share of German demand?

Wood flooring leads with 33.92% share, although vinyl/SPC-LVT is the fastest-growing category at 7.75% CAGR.

Why is East Germany growing faster than other regions?

Tier-2-city re-urbanization and subsidy-supported renovations drive a 7.64% CAGR in East Germany despite overall economic stagnation.

What role do online channels play in flooring sales?

Online stores grow at 10.73% CAGR as virtual visualization tools reduce purchase barriers, even though home centers remain the largest channel.

Which regulatory change most affects product specifications?

The EU-wide formaldehyde limit of 0.062 mg/m³ effective August 2026 intensifies demand for low-VOC and recyclable flooring.

How severe is the installer shortage?

Germany faces over 15,000 open flooring-related trade positions, adding six-to-eight-week delays and pushing adoption of DIY-friendly products.

Page last updated on: