GCC Compound Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.2 Billion |

| Market Size (2026) | USD 14.94 Billion |

| Market Size (2031) | USD 19.31 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

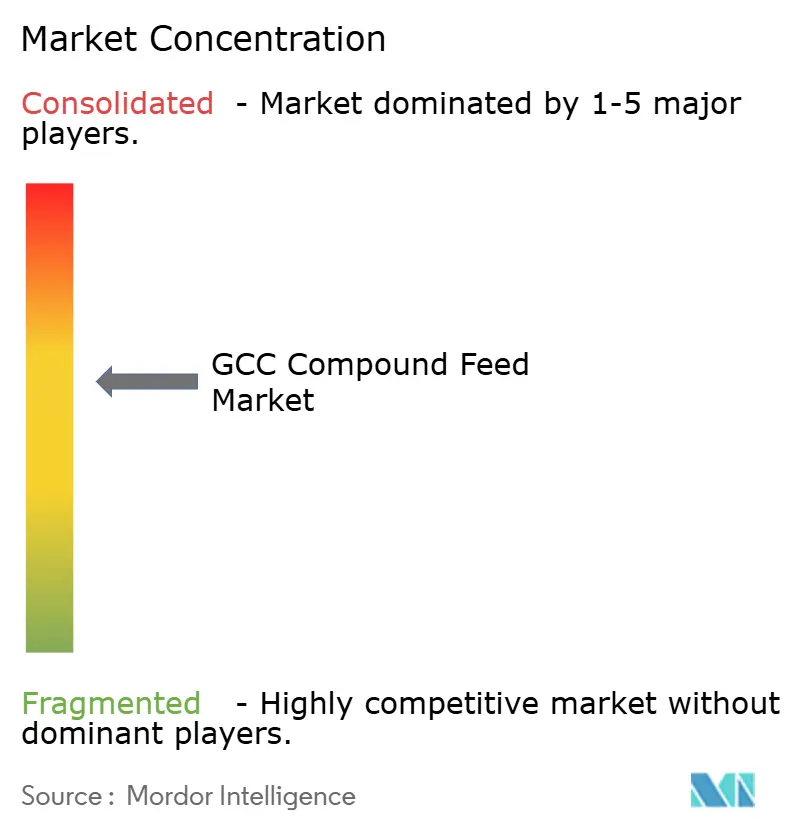

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Compound Feed Market Analysis by Mordor Intelligence

The GCC compound feed market size was valued at USD 14.2 billion in 2025 and estimated to grow from USD 14.94 billion in 2026 to reach USD 19.31 billion by 2031, at a CAGR of 5.24% during the forecast period (2026-2031). Ongoing food-security programs under Vision 2030, sizable livestock expansions, and investments in precision nutrition continue to underpin robust demand. Saudi Arabia’s scale advantage, the UAE’s subsidy regime, and Oman’s aquaculture push are reshaping regional feed formulations toward higher-value cereals, supplements, and extruded products. Volatile grain import costs and stricter antibiotic rules remain headwinds, but region-wide modernization of mills and storage infrastructure provides buffers and efficiency gains. Competitive dynamics favor vertically integrated leaders while niche entrants leverage technology to serve high-margin aquafeed and medicated additive segments.

Key Report Takeaways

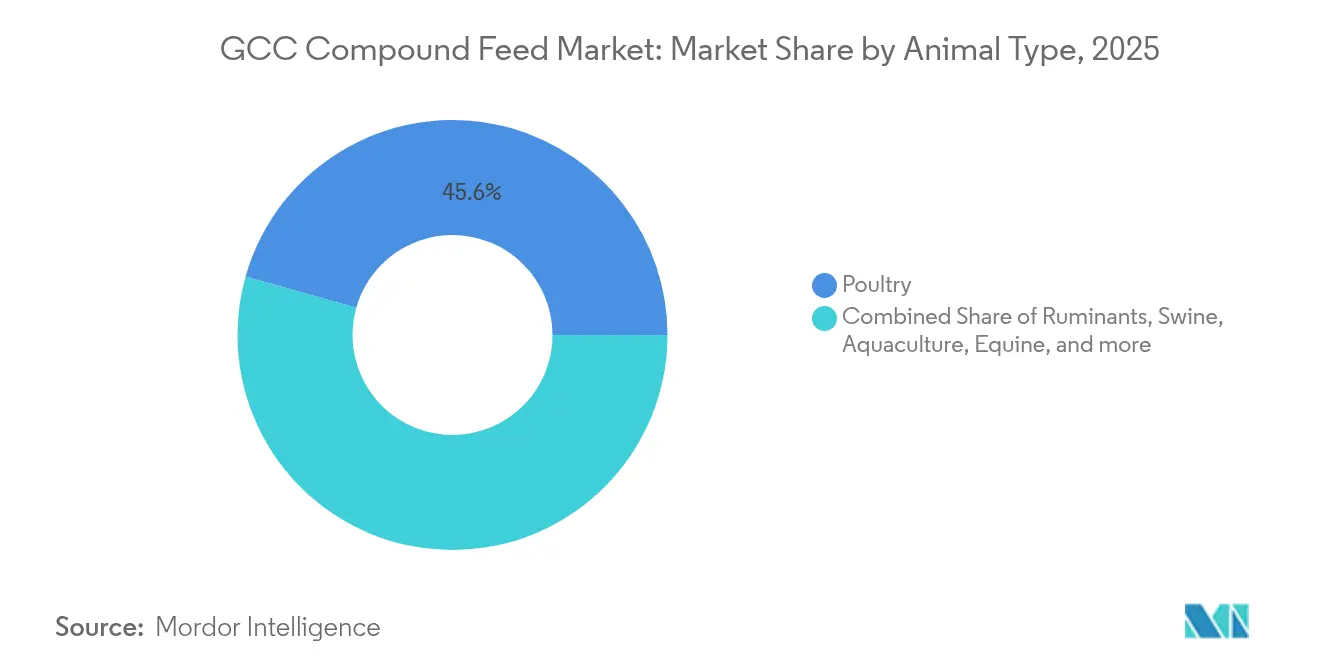

- By animal type, poultry led with 45.62% GCC compound feed market share in 2025, while aquaculture is projected to expand at an 8.72% CAGR through 2031.

- By ingredient, cereals accounted for 53.44% of the GCC compound feed market size in 2025; supplements are poised for 9.51% CAGR growth to 2031.

- By feed form, pellets held 60.35% revenue share in 2025, whereas extruded feeds are tracking the fastest 10.12% CAGR to 2031.

- By geography, Saudi Arabia controlled 56.48% of the GCC compound feed market in 2025; Oman is set to register the highest 7.66% CAGR to 2031.

- Al Ghurair Foods, ARASCO, and three other majors captured a major share in the GCC compound feed market in 2024, indicating a moderately concentrated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of GCC Compound Feed Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry meat consumption per capita | +1.2% | Saudi Arabia and the UAE, with spillover to Kuwait and Bahrain | Medium term (2-4 years) |

| Government food-security policies backing local mills | +1.0% | GCC-wide, strongest in Saudi Arabia and the UAE | Long term (≥4 years) |

| Precision nutrition and mill automation | +0.8% | UAE and Saudi Arabia, a gradual rollout in Qatar and Oman | Medium term (2-4 years) |

| Heightened livestock-health focus | +0.7% | All GCC, regulation-driven in Saudi Arabia and the UAE | Short term (≤2 years) |

| Mega desert dairy projects using TMR feeds | +0.6% | Primarily Saudi Arabia, secondary the UAE | Long term (≥4 years) |

| Port-based aquafeed extrusion plants | +0.5% | Oman and UAE coasts, and selective Qatar marine zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Poultry Meat Consumption Per-Capita

Broiler self-sufficiency programs continue to accelerate feed uptake, with Saudi Arabia alone targeting 80% domestic chicken supply through expanded integrated farms. Balady Company’s SAR 1.14 billion (USD 304 million) facility confirms investor confidence, while feed represents 60%–70% of poultry production costs[1]Source: U.S. Department of Agriculture Foreign Agricultural Service, “Saudi Arabia Livestock and Products Annual,” fas.usda.gov. Demographic growth and tourism inflows create additional institutional food-service demand, encouraging mills to optimize corn-heavy formulations that underpin stable cereal purchases. Pellet producers benefit most because automated feeders favor pelletized diets that lift feed-conversion ratios. Regional hatcheries are also upgrading genetics, reinforcing demand for nutrient-dense starter feeds that shorten grow-out cycles.

Government Food-Security Policies Supporting Local Feed Mills

UAE’s 25% feed subsidies and Saudi wheat procurement mandates of 1.5 million metric tons per year tilt economics in favor of domestic mills. Subsidies shield margins from grain swings, while preferential purchasing secures captive demand for local output. Larger integrated players deepen government ties to lock in multi-year contracts; smaller firms pivot toward organic or specialty lines to stay competitive within rigorous quality frameworks. Capital grants for silo construction further lower entry barriers for modernization, raising sector-wide efficiency. These programs collectively raise utilization rates and inject confidence for green-field and brown-field expansions across the bloc.

Advances in Precision Nutrition and Mill Automation

Near-infrared spectroscopy, cloud-based formulation tools, and automated batching together cut feed-conversion ratios by up to 8%. Early adopters gain cost leadership and brand differentiation, especially in aquaculture and dairy, where precise nutrient delivery commands premiums. Integration of real-time livestock-performance data allows mills to tweak formulations within hours, enhancing customer loyalty. Robotics in bagging and palletizing reduces labor costs and workplace injuries, while predictive maintenance powered by IoT sensors minimizes unplanned downtime. Partnerships with global tech vendors accelerate knowledge transfer and local manufacturing of advanced diets, creating a virtuous cycle of innovation.

Heightened Livestock-Health Focus Spurring Medicated Additives

Disease outbreaks have heightened demand for functional additives such as probiotics, prebiotics, and immune boosters. Producers adopt medicated feeds that comply with stricter antibiotic rules, creating an opportunity for mills with segregated lines and robust traceability protocols. Additive inclusion rates are rising in starter rations and transition diets, driving double-digit growth for premix suppliers. Regulatory agencies favor preventive nutrition, allowing mills to position higher-margin specialty blends as a cost-effective biosecurity measure. Joint ventures with veterinary pharmaceutical companies expedite product registration and broaden distribution reach. As livestock densities climb, on-farm trials demonstrating morbidity reductions further reinforce uptake.

Restraints Impact Analysis of GCC Compound Feed Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile global grain prices | −1.1% | All GCC, the highest pressure in Bahrain and Kuwait | Short term (≤2 years) |

| Water-scarcity crop bans raising import reliance | −0.5% | Core in Saudi Arabia and the UAE, with spillover to neighbors | Long term (≥4 years) |

| Consumer pivot toward plant-based diets | −0.4% | UAE and Qatar urban centers with gradual regional adoption | Long term (≥4 years) |

| Tighter antibiotic growth-promoter regulations | −0.3% | Regulation-led in Saudi Arabia and the UAE with GCC harmonization | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Global Grain Prices

Corn and soybean meal comprise more than 70% of raw-material cost, exposing mills to commodity swings. Saudi soybean meal use hit 1.54 million metric tons in 2024, and currency moves amplify price shocks. Larger groups deploy hedging and storage strategies, whereas smaller producers absorb margin hits or adjust recipes with alternative proteins. Extended payment terms with livestock integrators stretch working capital during price spikes. Currency hedges and forward contracts mitigate some risk, yet sustained high prices can squeeze feed-mill margins by up to 4 percentage points.

Water-Scarcity Crop Bans Raising Import Dependence

Saudi Arabia’s ban on fodder-crop irrigation and the UAE’s phase-out of Rhodes grass shift demand toward imported hay and higher-energy compound feeds. Mills respond by boosting cereal inclusion, raising exposure to global price swings and inland freight costs. Longer supply chains stretch working-capital cycles and require larger silo buffers to prevent production gaps. Government soft-loan schemes help finance storage, but smaller firms lack collateral. Resulting cost pressure can lift finished-feed prices by up to 6% in drought years, prompting farmers to adopt precision feeding and high-moisture storage systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

GCC Compound Feed Market Segment Analysis

By Animal Type:

Aquaculture Drives Premium GrowthAquaculture commanded the fastest 8.72% CAGR outlook, propelled by Oman’s USD 1.2 billion development fund and coastal cage investments that generate steady call-off orders for extruded floating feeds. Poultry retained leadership with 45.62% GCC compound feed market share in 2025, underwritten by expanding broiler capacities linked to food-security mandates.

Regional diversification into finfish and shrimp lowers reliance on traditional livestock while enabling export sales to East Asian buyers. Feed manufacturers able to deliver species-specific amino-acid profiles and lipid ratios secure pricing power. In contrast, ruminant diets revolve around TMR blends tied to mega dairies, providing high-volume yet lower-margin outlets. Swine and equine formulations remain niche, serving cultural or high-end recreational segments that still value premium nutrition and traceability.

By Ingredient:

Supplements Capture Innovation PremiumCereals constituted 53.44% of the GCC compound feed market size in 2025, cementing corn, wheat, and barley as bulk energy carriers. Supplements, however, are projected to rise at a 9.51% CAGR, reflecting intensified focus on gut health and production efficiency.

Higher inclusion of vitamins, enzymes, and functional botanicals supports antibiotic-free targets and boosts feed-conversion metrics. Cakes and meals, especially soybean meal, underpin essential amino acids, while by-products such as wheat bran deliver cost-effective fiber and protein. Ingredient innovation, therefore, migrates value away from commodity grains toward differentiated micronutrient packages that suppliers leverage for margin uplift and customer lock-in.

By Feed Form:

Extruded Technology Commands GrowthPellets captured 60.35% GCC compound feed market share in 2025, favored for low dust, ease of handling, and reliable feed conversion in automated barns. Extruded feeds, though smaller today, are forecast to register a 10.12% CAGR as marine farming and premium livestock producers demand superior digestibility and thermal stability.

Extrusion’s ability to embed oil coatings and create slow-sinking pellets suits offshore cages combating feed loss. Upfront capital demands limit entry, allowing early movers to command pricing premiums. Mash and crumble formats persist for younger stock and cost-sensitive segments but face gradual substitution where pellet or extruded advantages outweigh cost differentials.

Geography Analysis

Saudi Arabia Compound Feed Market

Saudi Arabia retained 56.48% of the GCC compound feed market in 2025 on the back of SAR 9 billion (USD 2.4 billion) livestock-city investments and integrated broiler capacity that now produces 80% of national chicken needs. Corn imports reaching 4.74 million metric tons certify sustained demand for energy-dense formulations. Vertically integrated majors such as ARASCO align sourcing, crushing, and distribution to ensure a stable supply within expansive desert production clusters.

United Arab Emirates Compound Feed Market

The UAE followed with well-capitalized mills anchored in Dubai and Abu Dhabi industrial zones, supported by 25% feed subsidies that preserve competitiveness against importers. Port proximity allows quick turnover of bulk grain arrivals, while companies like Agthia leverage advanced process automation to supply both domestic barns and neighboring markets. Camel, goat, and specialty dairy segments add product diversity, prompting new camel-feed lines under the Agrivita brand.

GCC Compound Feed Market

Oman is proposed to deliver the region’s fastest 7.66% CAGR, attributable to marine aquaculture rollouts and government co-financing of coastal feed-mill infrastructure. Over 428,000 live animals entered the sultanate in 2024, reinforcing ruminant feed volumes even as marine diets scale rapidly. Qatar, Kuwait, and Bahrain round out the bloc with specialty equine and small-ruminant niches that demand consistent premium formulations and traceable supply chains.

Regulatory Landscape

Regulation of compound feed across the GCC is increasingly framed through national feed-safety frameworks, facility licensing, and product registration requirements that influence plant design, documentation, and market access. In Saudi Arabia, the Saudi Food and Drug Authority (SFDA) administers the Feed Law (Royal Decree No. M/60, 2014, with implementing governance via SFDA Board Decision No. 2-16-1439, 2017), covering feed safety, labeling, quality, and oversight of imported and locally produced feed.

Compliance requirements are also tightening at the establishment level, supported by the SFDA technical requirements for feed factories and warehouses updated in April 2025. These updates emphasize Good Production Practices and specification control in factories and storage sites. In the UAE, the Ministry of Climate Change and Environment (MOCCAE) manages registration and renewal of manufactured animal feed for import, with registrations typically issued for multi-year validity (five years). The process is supported by public electronic lists of registered products and materials (including additives and supplements) and registered establishments, reinforcing traceability and standardization for feed and premix suppliers operating across borders.

Competitive Landscape

The GCC compound feed market is moderately concentrated: the top five firms secured significant revenue share in 2024, leaving space for agile specialists. Al Ghurair Foods led is one of the most promient players, followed by ARASCO[3]Source: U.S. Department of Agriculture Foreign Agricultural Service, “Saudi Arabia Livestock and Products Annual,” fas.usda.gov. Both leverage vertically integrated models spanning grain procurement to last-mile delivery, enabling scale efficiencies and bargaining power with bulk shippers.

Mid-tier players pursue geographic or product specialization, such as port-centric aquafeed extrusion or organic livestock lines. Capacity additions in Yanbu, Jeddah, and Sohar feature high-speed pelletizers and cloud-controlled batching that lift throughput while reducing energy intensity. Technology alliances with international equipment suppliers fast-track the adoption of moisture-controlled coolers, NIR sensors, and single-pellet durability testers.

Start-ups harness data analytics to custom-tune rations, while multinational protein companies establish captive feed arms to secure inputs for integrated poultry and dairy complexes. Competitive intensity will likely rise as subsidies align with output quality metrics, pushing efficiency benchmarks higher and rewarding innovators who fuse digital tools with stringent quality systems and resilient sourcing networks.

GCC Compound Feed Industry Leaders

Al Ghurair Foods LLC

Arabian Agricultural Services Company – ARASCO

Agthia Group PJSC (Abu Dhabi Developmental Holding Company PJSC – ADQ)

IFFCO Group (Allana International Ltd)

Trouw Nutrition Middle East (Nutreco N.V.)

- *Disclaimer: Major Players sorted in no particular order

GCC Compound Feed Market Companies Covered in this Report

- Al Ghurair Foods LLC

- Arabian Agricultural Services Company (ARASCO)

- Agthia Group PJSC

- IFFCO Group

- Trouw Nutrition Middle East

- Oman Flour Mills Company SAOG

- Fujairah Feed Factory LLC

- National Feed and Flour Production and Marketing Co. LLC

- Al Watania Agriculture Co.

- Bahra Advanced Food Industries Ltd.

Market Opportunities and Future Outlook

Capacity additions and processing modernization in Saudi Arabia and the UAE are creating near-term demand for cereals, premixes, and specialty additives that can match higher-throughput mill requirements and tighter quality systems. Modern Mills Companys SAR 150 million (USD 40 million) new feed mill project at Al-Jumum (annual capacity 422,000 metric tons, completion target Q4 2026) and Balady Poultry Company commissioning a new Saudi feed mill (three lines totaling 60 tonnes per hour) both increase the need for consistent raw-material supply, formulation services, and QA-ready additive inclusion.

A second opportunity cluster is tied to equipment-led upgrades and the shift toward higher-value formulations, where automation and extrusion can improve performance and reduce wastage. Arabian Mills for Food Products Co. has an expansion pipeline across Riyadh and Hail, and it signed SAR 71.2 million (USD 19 million) contracts with Buhler AG for equipment and design services. This indicates continued investment in upgraded lines aimed at premium pellets and extruded diets, while regulatory tightening in Saudi Arabia (SFDA) and the UAE (MOCCAE) is also increasing the value of compliant, documented feed additives and medicated or functional nutrition products, favoring manufacturers with batch-level traceability, segregated production capabilities, and established product-registration pathways.

Recent Industry Developments in GCC Compound Feed Market

- March 2026: Balady Poultry Company commissioned a new feed mill in Saudi Arabia with three production lines totaling 60 tonnes per hour. The project focuses on higher internal feed self-sufficiency and tighter control over broiler diet quality, reinforcing demand for premium poultry formulations and consistent cereal and supplement inputs.

- February 2025: ARASCO signed an MoU with Buhler to improve feed production efficiency in Saudi Arabia. The collaboration centers on process optimization and technology support, accelerating modernization of milling operations and strengthening the ability to manufacture higher-spec compound feed under stricter quality frameworks.

- December 2024: The Yanbu Grain Terminal began operations with 3 million metric tons of capacity in Saudi Arabia. Expanded grain handling and logistics capacity supports lower inbound friction for western-region feed mills and improves resilience against import supply disruptions that can affect formulation continuity.

GCC Compound Feed Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the GCC compound feed market covers factory-made feed mixes sold for livestock and aquaculture in GCC member countries, measured in value terms. It includes complete feed and complementary formulations where multiple ingredients are blended to meet animal nutrition needs.

Scope exclusions: It excludes on-farm mixing done for self-consumption and standalone feed additives sold separately from compound feed.

Segments Covered in This Report

- By Animal Type

- Ruminants

- Poultry

- Swine

- Aquaculture

- Equine

- Other Animal Types

- By Ingredient

- Cereals

- Cakes and Meals

- By-products

- Supplements

- By Feed Form

- Mash

- Pellets

- Crumbles

- Extruded

- Other Forms

- By Geography

- United Arab Emirates

- Saudi Arabia

- Oman

- Bahrain

- Kuwait

- Qatar

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure for demand, supply, and pricing across GCC feed categories, and to align definitions across countries. We referred to public datasets and references such as FAOSTAT for livestock numbers and feed-use context, UN Comtrade for feed ingredient trade flows, national statistics portals and agriculture ministries for production and food security programs, and central bank or official FX releases for currency timing.

It was also used to sanity-check feed output and raw material exposure using documents such as customs bulletins, trade association releases, and company annual reports and investor presentations for capacity and expansion commentary. Where available, a paid subscription for company financials and an import or export shipment-level database were used to verify key players, plant footprint signals, and ingredient movement patterns. The sources listed here are illustrative, and many other public references were also reviewed for data capture, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and short surveys were run with feed mill managers, procurement teams, nutritionists, distributors, and large farm operators across the GCC so assumptions could be stress-tested. These conversations helped pin down feed form mix (for example, pellets versus mash), animal-type demand shifts, typical formulation changes during price swings, and realistic price pass-through timing across countries.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | |

| Mid tier: 54% | Functional/Unit leaders: 38% | |

| Smaller Players: 18% | Managers: 49% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs compound feed demand from country-level livestock and aquaculture output signals, then converts those signals into feed requirements using practical feed-intensity benchmarks. The totals were corroborated with selective bottom-up approximations, such as sample ASP multiplied by volume checks by animal type, channel conversations on throughput, and supplier roll-ups where coverage was adequate.

Key inputs used in the model included livestock and poultry headcounts, aquaculture output direction, feed form preference shifts (pellets versus mash), import dependence for major feed ingredients, and average pricing by feed category adjusted for observable raw material cycles. When specific segment splits were unclear, we used a conservative allocation approach anchored on interview ranges, then rechecked the implied per-animal feed usage so outliers could be corrected.

For forecasting, scenario analysis was used because growth is sensitive to policy moves affecting local production, farm expansion pacing, and ingredient price volatility. In practice, the scenarios were guided by expert expectations on herd growth, farm consolidation, and substitution behavior in formulations, and then the final path was selected based on the most repeated operating assumptions from primary respondents.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final number stays connected to real market signals. We compared country totals against independent indicators such as livestock production direction, feed milling activity discussions, and ingredient import trends, and then investigated any large mismatches before sign-off.

A second analyst review was applied to the assumptions, conversions, and country roll-ups, followed by a final pass to confirm units, FX timing, and rounding logic. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity additions, policy changes, or sharp commodity price swings. Before delivery, the full model is re-opened so clients receive the latest updated view.

Mordor Intelligence's Gcc Compound Feed Market Size Compared With Other Published Estimates

Published market sizes for GCC compound feed can differ even when they sound like they measure the same thing, because the boundaries and pricing logic often vary. Differences usually show up in what is counted as compound feed versus adjacent feed products, which country coverage rules are applied, and how price changes are carried into the base year.

Import and export movement of key feed ingredients, along with feed-form and animal-type mix checks from field interviews, are the evidence points that keep Mordor Intelligence tied to a realistic demand pool rather than a broad animal feed bundle. Gaps also come from whether a study includes only livestock and poultry, whether aquaculture is fully counted, whether nominal prices are used without consistent FX timing, and how quickly the model is refreshed after commodity swings.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.2 B (2025) | |

| Industry Publisher A | USD 9.6 B (2025) | Often presented with a narrower counted basket that leans toward livestock and poultry feed, which can understate totals when aquaculture and full feed-form coverage are included. The valuation can also rely on simpler price carry-forward assumptions during raw material volatility. |

| Trade Data Platform B | USD 13.8 B (2024) | This style of estimate is commonly reconstructed from trade and producer revenue logic for a broader animal feed definition, which may not match compound feed-only boundaries. It can also reflect nominal wholesale pricing conventions and a different base year and FX timing, which shifts value comparisons. |

The spread across the three figures is mainly explained by category boundaries and the year and price conventions used to value feed. By keeping the counted product set consistent with compound feed and by cross-checking the implied demand using animal output and ingredient movement signals, the final number stays traceable to clear, repeatable inputs.

Key Questions Answered in the Report

How large is the GCC compound feed market today?

The GCC compound feed market size stands at USD 14.94 billion in 2026 and is projected to reach USD 19.31 billion by 2031.

Which country dominates feed demand across the Gulf?

Saudi Arabia leads with 56.48% market share thanks to its large poultry and dairy sectors and supportive food-security policies.

What is the fastest-growing livestock segment for feed suppliers?

Aquaculture feed registers the quickest 8.72% CAGR, driven by Omani and Emirati investments in marine farming infrastructure.

Which feed form is gaining momentum beyond pellets?

Extruded feeds are forecast to expand at a 10.12% CAGR as aquaculture and premium livestock producers seek improved digestibility.

How are subsidies affecting regional feed production?

UAE's 25% feed subsidies and Saudi wheat procurement programs boost domestic mill competitiveness and reduce import dependence.

What is the biggest risk to feed-mill profitability?

Exposure to volatile global grain prices poses the largest margin threat, especially to smaller mills lacking hedging strategies.

Page last updated on: