Hydrophobic Interaction Chromatography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 513.41 Million |

| Market Size (2031) | USD 721.09 Million |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

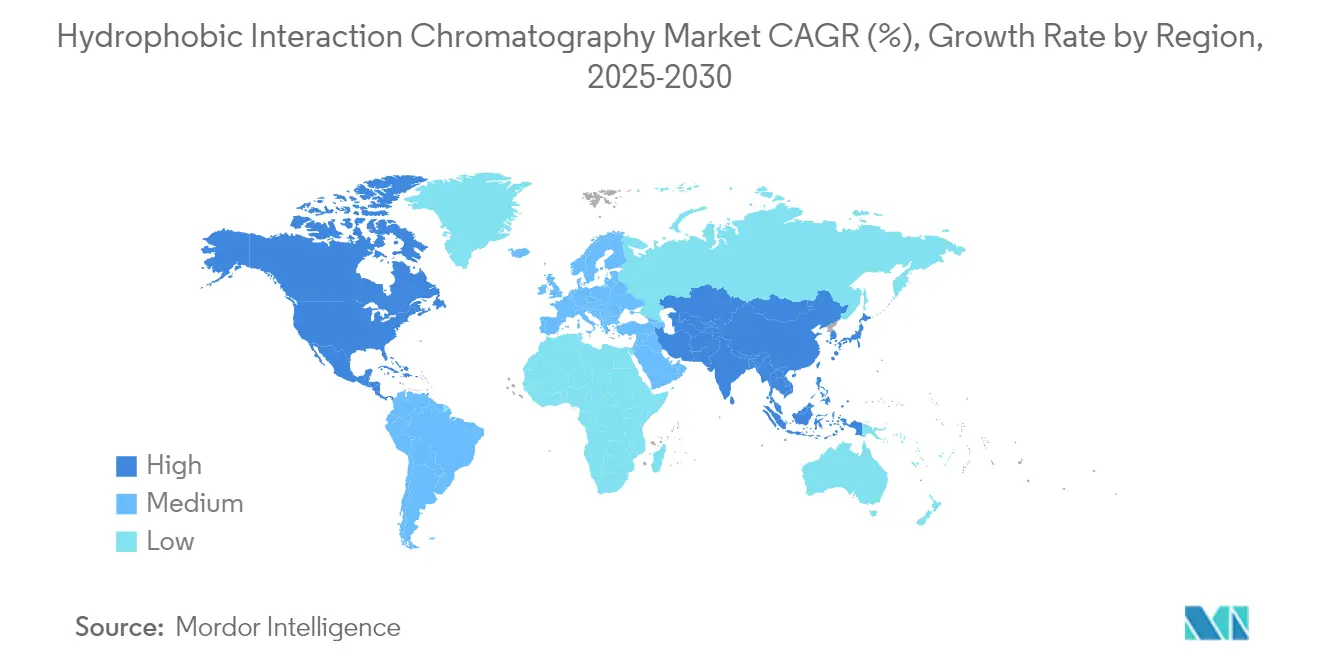

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

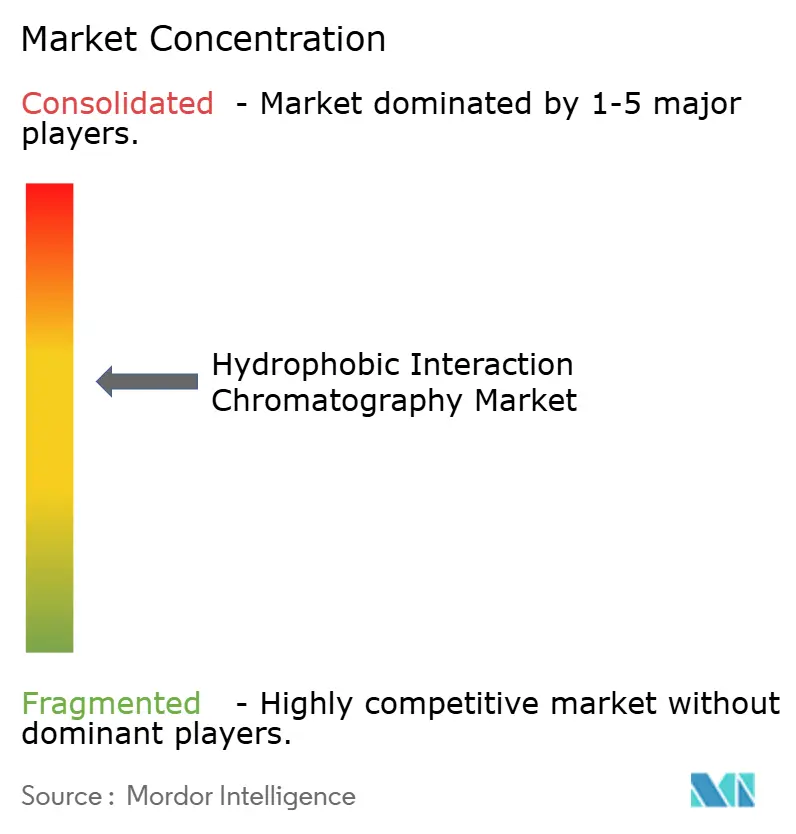

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydrophobic Interaction Chromatography Market Analysis by Mordor Intelligence

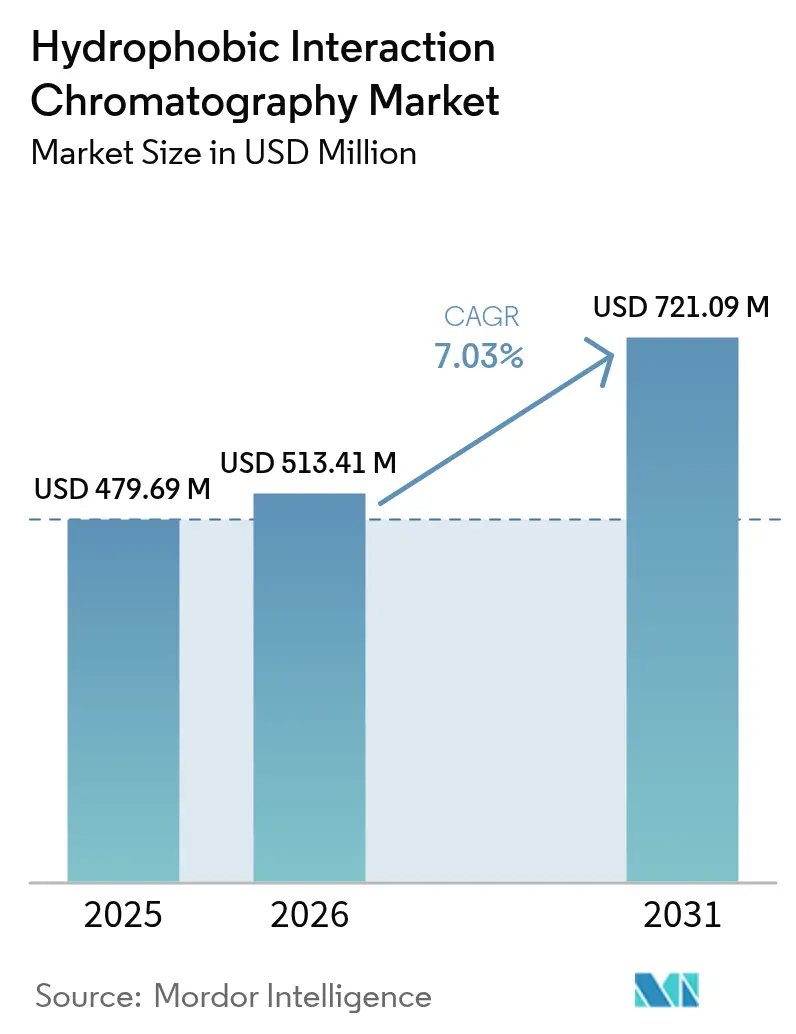

The hydrophobic interaction chromatography market size is expected to grow from USD 479.69 million in 2025 to USD 513.41 million in 2026 and is forecast to reach USD 721.09 million by 2031 at 7.03% CAGR over 2026-2031. Strong demand for downstream polishing of monoclonal antibodies, antibody–drug conjugates, and other complex biologics underpins this advance, as manufacturers seek robust, high-selectivity workflows that guarantee host-cell protein levels below informal 100 ppm thresholds. Capacity additions such as Danaher’s USD 1.5 billion resin expansion program and Samsung Biologics’ USD 1.46 billion plant upgrade raise global production headroom while amplifying purification bottlenecks, thereby reinforcing the economic case for hydrophobic interaction chromatography market solutions. Technology progress in mixed-mode resins and electrospun membranes shortens process trains, reduces solvent consumption, and keeps cost-of-goods competitive despite higher upstream titers. Regional regulatory frameworks that emphasize low-salt eluates, especially in the United States and European Union, further accelerate uptake by clarifying submission pathways and mitigating scale-up risk.[1]Federal Register, “Guidance for Continuous Manufacturing of Drug Substances,” U.S. Federal Register, federalregister.gov

Key Report Takeaways

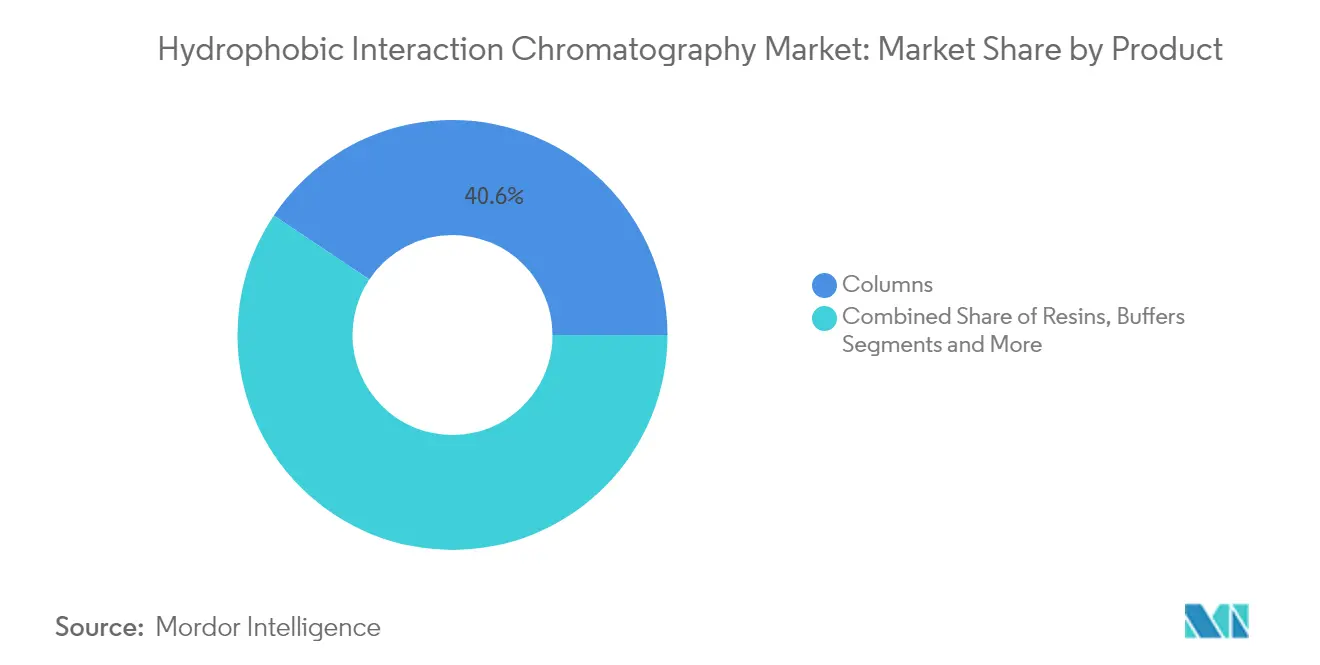

- By product, columns captured 40.62% of the hydrophobic interaction chromatography market share in 2025, while resins are projected to advance at a 9.52% CAGR through 2031.

- By sample type, monoclonal antibodies held 51.84% of the hydrophobic interaction chromatography market size in 2025; antibody-drug conjugates are on track for a 12.28% CAGR to 2031.

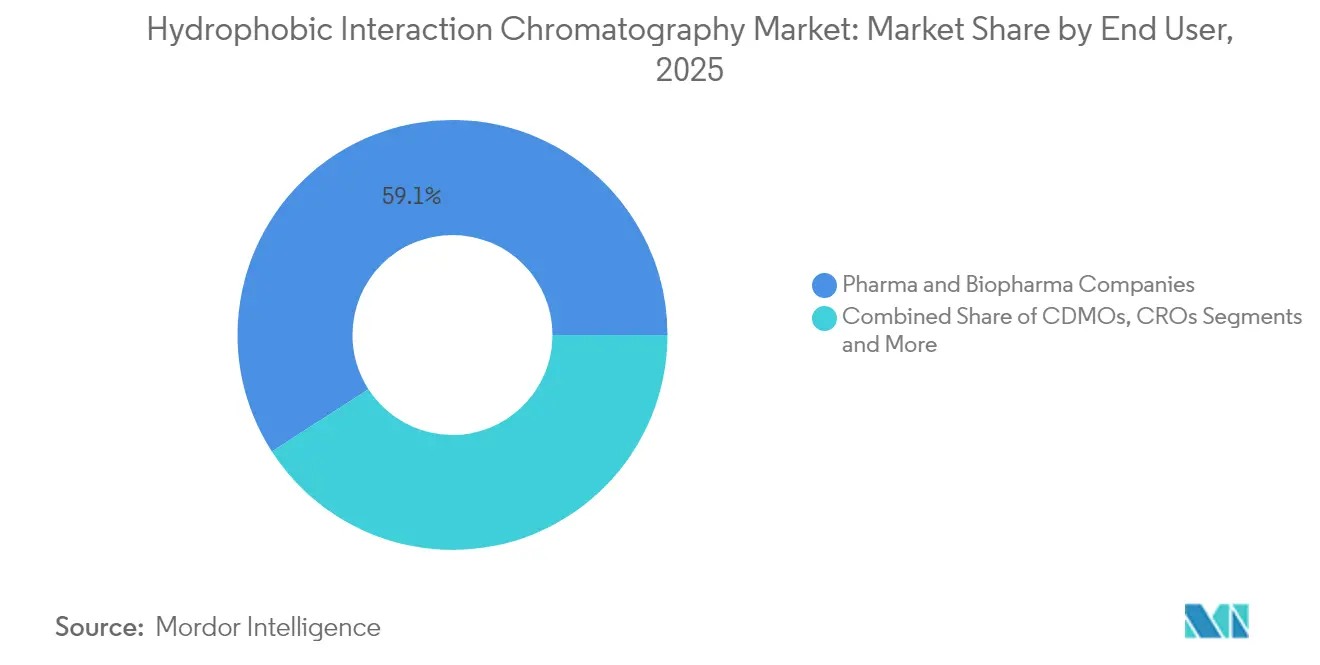

- By end-user, pharma and biopharma companies controlled 59.12% of the hydrophobic interaction chromatography market share in 2025, whereas CDMOs are poised to grow at a 10.15% CAGR.

- By geography, North America accounted for 37.12% of the hydrophobic interaction chromatography market size in 2025; Asia-Pacific is set to expand fastest at an 10.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrophobic Interaction Chromatography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For Monoclonal Antibodies | +1.80% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Surge In Global Biopharma Manufacturing Capacity | +1.50% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Advances In High-Throughput HIC Resins & Columns | +1.20% | Global | Short term (≤ 2 years) |

| Rising R&D Spending On Antibody-Drug Conjugates | +1.00% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Continuous-Processing Adoption Needs HIC Membranes | +0.80% | North America & EU | Long term (≥ 4 years) |

| Regulatory Push For Low-Salt Purification Workflows | +0.70% | Global, led by FDA and EMA regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Monoclonal Antibodies

Rising antibody titers have moved average commercial bioreactor campaigns above 5 g/L, which intensifies downstream bottlenecks that only hydrophobic interaction chromatography market workflows currently address with proven robustness. Manufacturing economics reveal that purification at times consumes 80% of the total cost of goods, sharpening management focus on fewer, higher capacity HIC steps that retain product quality. Fujifilm’s USD 1.2 billion North Carolina expansion alone adds 160,000 L dedicated to antibodies and immediately lifts regional demand for HIC resins and columns. Host-cell protein specifications trending below 100 ppm make the polishing power of HIC indispensable for late-stage process qualification.[2]Biotechnology Progress Editorial Team, “Labor Costs and Economics in Downstream Purification,” Biotechnology Progress, asmedigitalcollection.asme.org The knock-on effect is steady double-digit revenue visibility for hydrophobic interaction chromatography market suppliers through mid-term planning cycles.

Surge in Global Biopharma Manufacturing Capacity

Asia-Pacific governments are pouring incentives into GMP plants, and the region’s stainless-steel volume is rising faster than anywhere else, opening a persistent gap for purification infrastructure.[3]ISPE Authors, “GMP Roadmap for Emerging Biomanufacturing Hubs,” Pharmaceutical Engineering, pharmeng.orgSamsung Biologics and Lotte Biologics together earmark more than USD 4.8 billion for large-scale facilities, each engineered around state-of-the-art downstream halls that feature sizable HIC suites. Harmonized standards under the Pharmaceutical Inspection Co-operation Scheme are eliminating specification ambiguity, so buyers are free to select higher-performance hydrophobic chromatography market equipment rather than the lowest-cost legacy gear. Local production of columns and resins, such as Cytiva’s new plant in Incheon, reduces lead times and foreign-exchange exposure, prompting multinationals to re-balance sourcing toward the region. As a result, capacity increments translate directly to resin pull-through, strengthening the hydrophobic interaction chromatography industry revenue base.

Advances in High-Throughput HIC Resins & Columns

Mixed-mode agarose resins now exceed 90 g/L dynamic binding capacity for antibodies, effectively doubling productivity inside identical skid footprints. Hydrophobic-charge induction chromatography has entered mainstream adoption, offering milder elution pH and superior selectivity for difficult-to-purify conjugates. Electrospun membranes reach static capacities near 25 mg/mL and shorten cycle times because diffusive limitations vanish, which cuts buffer volumes and reduces energy consumption in line with sustainability mandates. Single-step virus polishing on new calcium hydroxyapatite media routinely recovers more than 75% of viral particles while trimming contaminating protein content by 90% or more. These step-change gains ensure that the hydrophobic interaction chromatography market retains relevance even as affinity capture and multi-modal options proliferate.

Rising R&D Spending on Antibody-Drug Conjugates

More than 500 late-preclinical and clinical ADC programs require purification methods that separate conjugated from unconjugated antibody with single-resin precision, a task for which HIC remains the gold standard. The hydrophobic payload makes conjugates cling to resin ligands, enabling sharp resolution of drug-to-antibody ratio species without extreme salt conditions. Novel non-toxic linker–payload surrogates allow high-throughput DAR optimization on HIC platforms, accelerating process development and compressing time to IND filings. Cyclodextrin-enhanced buffer formulations stabilize highly hydrophobic conjugates during purification, pushing aggregate levels below 1% and thereby complying with draft FDA expectations for ADC quality profiles. Regulatory scrutiny, particularly around residual host-cell proteins in conjugates, elevates analytical HIC to a mission-critical QC tool and fuels sustained capital replacement cycles across the hydrophobic interaction chromatography market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Skilled Downstream Processing Talent | -1.20% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Availability Of Alternative Chromatography Modes | -0.80% | Global | Medium term (2-4 years) |

| High Cost Of Premium HIC Equipment & Consumables | -0.60% | Developing markets, price-sensitive segments | Long term (≥ 4 years) |

| Shift Toward Single-Use Affinity Membranes Bypassing HIC | -0.40% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Downstream Processing Talent

Industry 4.0 initiatives mandate data-science competencies that remain scarce, driving wage inflation and project delays when firms roll out continuous HIC trains. Programming languages such as Python and R are now basic requirements for chromatography data handling, yet only a fraction of process engineers possess such skills, lengthening validation timelines. Labor costs outstrip raw-material spending by an order of magnitude at pilot scale, so unfilled roles directly dent operating margins and slow new hydrophobic interaction chromatography market installations. Vendor-hosted academies partially close gaps, but emerging-market buildouts still outpace talent development, which could temper near-term uptake. Until curricula evolve, the skills deficit will be an immediate drag on the hydrophobic interaction chromatography market momentum.

Availability of Alternative Chromatography Modes

Continuous high-capacity protein A resins achieve 90 g/L with >95% recoveries, allowing direct flow-through polishing and reducing reliance on HIC in some antibody platforms. Membrane-based affinity captures cut cycle times by half and runs at lower back pressure, which appeals to facilities struggling with utility constraints or green targets. Economic models demonstrate that membrane-only trains can trim downstream operating expenses by 23%, intensifying procurement scrutiny of every HIC column in new plants. Mixed-mode ligands delivering high selectivity at neutral pH lessen the need for follow-on HIC steps to remove aggregates. While HIC retains irreplaceable strengths for specific conjugates and viral vectors, these innovations carve away share growth potential and dampen hydrophobic interaction chromatography market expansion in mature antibody workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Columns Drive Market Leadership

Columns dominate with 40.62% 2025 revenue because end-users favor equipment that pairs well with validated automation scripts and meets agency filings without amendments. Large axial configurations still headline high-volume installations, though radial designs gain popularity where throughput pressure drop trade-offs tilt economics. End-users lean on robust pack integrity testing and proven cleaning protocols, choosing established column brands even when alternate devices advertise higher capacity, thus anchoring the hydrophobic interaction chromatography market around legacy footprints. Columns also benefit from a wide network of third-party skid integrators, simplifying procurement and validation across multi-plant networks. In turn, scale stability and familiar control interfaces lessen operator training burdens, a decisive factor amid acute workforce shortages. Though membrane modules nibble at small-lot processes, columns remain the default when batch sizes exceed 2,000 L because resin reuse amortizes capital outlays over longer campaigns. Resin internal diffusion constraints continue to set flowrate ceilings, but suppliers are now optimizing bead architecture to double volumetric productivity without altering system hydraulics. As regulatory bodies stay cautious about wholesale hardware swaps, columns will remain centre-stage in the hydrophobic interaction chromatography market even as adjacent formats proliferate.

Resins underpin the highest growth trajectory at 9.52% CAGR due to rapid adoption of mixed-mode ligands pursuing better selectivity at lower salt. Agarose matrices command premium share on biocompatibility, while polymeric beads claim ground where alkaline cleaning or high pressure demands apply. Manufacturers channel heavy investment into ligand chemistry that uses shorter synthesis paths, cutting lead times and reducing carbon intensity in keeping with ESG reporting duties. Purolite’s USD 150 million Pennsylvania site for agarose resin greatly enlarges North America’s local supply, trims geopolitical risk, and elevates service levels through regional warehousing. Buyers reward such resilience with multi-year dual-sourcing agreements that lock volume and price, stabilizing the hydrophobic interaction chromatography market size for consumables sourcing teams. As upstream densities keep trending higher, dynamic capacity becomes the procurement scorecard; hence resin innovation remains the decisive variable that shapes the total addressable hydrophobic interaction chromatography market.

By Technology: Classical HIC Maintains Dominance

With decades of process characterization data and copious regulatory precedents. Process transfer risk remains low, and that reliability convinces quality leadership teams to stay with familiar salt-gradient workflows. Validation documentation from older biologics portfolios doubles as a template for new products, which compresses development calendars and curbs consulting spend. The hydrophobic interaction chromatography market, therefore, leans on established ligands like phenyl and butyl, whose robustness is thoroughly understood under multi-cycle cleaning regimens. Switching costs extend beyond consumables, touching every line in electronic batch records, so finance teams often prefer incremental process bolstering instead of full re-engineering. Even within continuous designs, classical packed beds nest comfortably inside switching valve matrices, further protecting their installed base.

Hydrophobic-charge induction chromatography is the fastest climber because it marries hydrophobic and electrostatic interactions, letting developers elute sensitive payloads at near-neutral pH. Its growing dossier of regulatory filings for viral vector and ADC products elevates confidence among quality functions that guard against late-stage surprises. Protein scientists appreciate HCIC for resolving subtle glycoform differences without extreme salt or pH, which avoids product degradation and preserves potency. Vendors now supply predictive simulation tools that shorten resin screening to weeks, not months, expanding the hydrophobic interaction chromatography market use case in strained development timelines. As more biopharmas pivot toward highly modified antibody scaffolds, HCIC’s differentiated selectivity secures repeating orders and paves the way for platform adoption.

By Sample Type: Monoclonal Antibodies Lead Applications

Monoclonal antibodies occupy 51.84% of 2025 revenue because they stand as the biopharma workhorse, forming the backbone of commercial launch calendars worldwide. Their purification flowsheets rely on protein A capture followed by ion exchange and an HIC polish that removes aggregates and variants to sub-1% levels. With each new 20,000 L reactor that comes online, three to five fresh columns of HIC capacity are usually specified, tying global capacity expansion directly to hydrophobic interaction chromatography market sales. The predictable physicochemical nature of IgG molecules simplifies method bridging across molecules, giving CDMOs a plug-and-play template that lowers tech-transfer costs and cements HIC demand even when product mixes change. Regulatory confidence is equally deep: hundreds of biologics license applications cite classical HIC steps, so reviewers seldom raise new questions, accelerating market adoption among late entrants.

Antibody–drug conjugates post the fastest 12.28% CAGR because their hydrophobic payload escalates purification complexity, which magnifies HIC’s advantage. Separating DAR 0, DAR 2, and DAR 4 species by minor shifts in ligand affinity ensures precise dosage control, an FDA hot-button area that commands strict acceptance criteria. Mock payload surrogates enable developers to experiment on bench-scale HIC screens without toxic compound handling, thus speeding knowledge capture and design freezes. The hydrophobic interaction chromatography market size attached to ADC campaigns multiplies quickly because each product run needs dedicated resin or well-validated cleaning protocols to prevent cross contamination. As sponsor pipelines fill with site-specific conjugation chemistries, the probability of unique HIC steps per molecule climbs, projecting sustained growth into the next decade.

By End-User: Pharma Companies Dominate Utilization

Pharma and biopharma firms command a 59.12% 2025 share, reflecting their control of commercial licenses and late-stage manufacturing decisions that directly specify purification kits. Large integrated players often sign multi-year framework agreements with resin suppliers, aligning price indexes with purchase volume and shielding budgets from raw-material swings. They also hold the most extensive installed base of automated skid hardware, so incremental HIC capacity can be bolted on without new validation of control software, protecting timelines for product launches. Cross-functional governance boards within these firms convert corporate sustainability goals into procurement criteria, and HIC suppliers are able to document solvent savings and gain preferred-vendor status. The hydrophobic interaction chromatography market thus grows in tandem with each blockbuster’s scale-up cycle.

Contract development and manufacturing organizations grow fastest at 10.15% CAGR because biotech innovators want to de-risk capital commitments amid macro uncertainty. CDMOs differentiate through broad technology menus; therefore, they purchase diverse HIC media types to satisfy heterogeneous client molecules. Lonza’s USD 1.2 billion site acquisition and Samsung Biologics’ multi-plant complex underscore the scale of outsourced capacity coming online, and each suite requires fresh columns, skids, and resins. CDMOs negotiate volume-rebate tiers yet remain open to novel membrane formats that promise rapid turnover, feeding a healthy competitive tension inside the hydrophobic interaction chromatography market. Their global footprint also democratizes access in emerging markets, amplifying downstream demand where local innovators ramp biosimilar pipelines.

Geography Analysis

North America commands 37.12% of 2025 revenue and holds a deep bench of innovators, contract manufacturers, and tool suppliers whose proximity shortens supply chains and speeds service response. The Food and Drug Administration endorses continuous manufacturing. It publishes guidance that clarifies expectations for in-line monitoring, thereby emboldening adopters of membrane-based continuous HIC in pilot and commercial settings. United States federal incentives, including recent tax credits for biologics infrastructure, lower effective capital cost, and underpin orders for high-throughput column skids. Canada pursues complementary investments in antibody facilities, while Mexico advances regional fill-finish hubs that create incremental resin demand. As these networks interlink, cross-border logistics keeps lead times short and deepens the hydrophobic interaction chromatography market footprint.

Europe remains a powerhouse driven by the European Medicines Agency’s harmonized framework, which facilitates quick mutual recognition of new purification technologies. Germany’s concentration of biotech clusters, coupled with carbon-reduction targets, pushes suppliers to design low-solvent HIC workflows suited for ISO 14064 reporting. The United Kingdom safeguards its post-Brexit life-sciences status by fast-tracking advanced therapy applications, many requiring viral vector purification where HIC plays a central role. Southern European states leverage EU recovery funds to modernize biologics plants, inserting automated HIC steps to meet export quality tiers. Environmental, social, and governance (ESG) rules also force manufacturers to adopt resins with lower chemical footprints, further shaping the regional hydrophobic interaction chromatography industry narrative.

Asia-Pacific delivers the fastest 10.85% CAGR as China, India, and South Korea race to secure biopharma self-sufficiency and capture contract manufacturing flows. Massive campus-style projects, typified by Samsung Biologics and Lotte Biologics, integrate upstream, downstream, and fill-finish units in a single site, locking in long-term resin and column demand. Governments extend tax holidays and accelerated depreciation to shorten payback periods, while local regulators endorse Pharmaceutical Inspection Co-operation Scheme alignment, smoothing export clearance. Japanese innovators inject process-development rigor and collaborate with global suppliers to pilot membrane HIC solutions, seeding technology spill-overs region-wide. Southeast Asian nations add smaller multiproduct plants, thereby broadening customer bases for hydrophobic interaction chromatography market suppliers that offer modular, quick-turnaround packages.

Competitive Landscape

The market displays moderate concentration as giant conglomerates pursue acquisitions to assemble full-line bioprocess portfolios. Thermo Fisher Scientific paid USD 4.1 billion for Solventum’s purification assets, giving it deeper column and membrane breadth and locking in cross-selling opportunities across cell-culture and analytical divisions. Danaher fused Cytiva and Pall into a USD 7.5 billion entity and earmarked USD 600 million for HIC resin expansion, signalling a willingness to invest at scale to defend its share. Such moves intensify price competition for commodity ligands but raise switching barriers because buyers favor integrated supply chains that guarantee delivery.

Innovation remains a battlefield where smaller technology specialists survive by focusing on niche ligands tailored for antibody-drug conjugates, viral vectors, or difficult-to-express enzymes. Electrospun membrane suppliers tout 25% media-cost reductions and 40% shorter cycles, courting CDMOs eager to balance facility throughput against capital budgets. Digital twins and artificial-intelligence-driven method optimisation packages, sometimes bundled free with resin purchases, differentiate premium brands that can fund software teams. In parallel, sustainability metrics enter tender documents, so vendors that publish lifecycle assessments of resin manufacturing win new inclusion lists, edging out slower incumbent producers.

Emerging-market manufacturers of foundational agarose resins gain ground by matching performance specs at lower landed cost, prompting Western leaders to seed local manufacturing to preserve lead times. Joint ventures in India and China shorten order fulfilment and bolster after-sales support, upgrading customer loyalty in those high-growth geographies. Collectively, these strategic responses maintain a dynamic equilibrium in the hydrophobic interaction chromatography market, where scale consolidation coexists with fast-moving technology frontiers.

Hydrophobic Interaction Chromatography Industry Leaders

Bio-Rad Laboratories, Inc.

Thermo Fisher Scientific

Sartorius AG

Tosoh Bioscience GmbH

General Electric (GE Healthcare)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thermo Fisher Scientific announced a USD 2 billion United States manufacturing expansion, allocating USD 1.5 billion to equipment and consumables capacity increases that include hydrophobic interaction chromatography market resins.

- February 2025: Thermo Fisher Scientific acquired Solventum’s Purification & Filtration division for USD 4.1 billion, widening its downstream toolkit with HIC columns, membranes, and filtration skids.

- November 2024: Sartorius Stedim Biotech opened a Center for Bioprocess Innovation in Massachusetts and plans to build GMP suites in 2025 that will showcase advanced HIC skids.

- October 2024: Agilent Technologies launched the Infinity III LC Series with automated method assist features relevant for HIC process analytics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the hydrophobic interaction chromatography (HIC) market as the annual sales value of consumables, resins, pre-packed or empty columns, buffers, and related kits designed to separate biomolecules by hydrophobic retention in aqueous high-salt environments, spanning discovery labs to commercial bioprocessing plants. We, the analysts at Mordor Intelligence, include classical HIC and hydrophobic-charge-induction variants used during capture, intermediate, or polishing steps for recombinant proteins and viral vectors.

Scope Exclusion: Instruments that lack a hydrophobic retention phase, such as pure ion-exchange or size-exclusion hardware, are outside our measured universe.

Segmentation Overview

- By Product

- Columns

- Axial flow columns

- Radial flow columns

- Resins

- Agarose-based resins

- Polymer-based resins

- Silica-based resins

- Buffers

- Kosmotropic salts

- Additives & modifiers

- Columns

- By Technology

- Classical HIC

- Hydrophobic-Charge Induction Chromatography (HCIC)

- Mixed-mode HIC resins

- By Sample Type

- Monoclonal antibodies

- Antibody-drug conjugates

- Vaccines

- Viral vectors & gene-therapy products

- Other recombinant proteins

- By End-User

- Pharma & Biopharma Companies

- Contract Development & Manufacturing Orgs (CDMOs)

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We complemented desk findings with structured talks to process development scientists, procurement heads at CDMOs, and regional consumable distributors across North America, Europe, and Asia. These dialogues clarified resin replacement cycles, average selling prices, and adoption barriers that documents alone seldom reveal.

Desk Research

Our desk work began by mapping biologics batch volumes drawn from FDA Biological License Application data, EMA dossiers, and Japan PMDA approvals, which hint at downstream purification needs. Trade values from UN Comtrade, resin import tariffs, and BioPhorum capacity trackers were aligned with patent trends gathered through Questel, highlighting shifts toward salt-tolerant media. Company 10-Ks, investor decks, and technical notes enriched these open sources, while proprietary revenue splits from D&B Hoovers and news feeds on Dow Jones Factiva let us triangulate supplier exposure. The sources named are illustrative; many additional references supported data capture, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction of global purification spend, built from recombinant protein output, typical HIC step prevalence, and median resin usage per harvest generated the baseline, which we then cross-checked through selective bottom-up tests such as supplier roll-ups and channel ASP × volume probes. Key variables fed into the model include approved biologic pipeline size, average mAb titers, single-use system penetration, salt-tolerant resin uptake, and regional manufacturing expansions. Multivariate regression blended with scenario analysis extends forecasts to 2030, and gaps in granular inputs are bridged through nearest neighbor proxies.

Data Validation & Update Cycle

Outputs run through variance checks against customs statistics and quarterly earnings calls before senior review. We refresh figures annually and trigger interim updates for price shocks, regulatory shifts, or major M&A, ensuring clients always receive our latest view.

Why Mordor's Hydrophobic Interaction Chromatography Baseline Commands Reliability

Published estimates often diverge because providers apply different product baskets, price decks, and refresh cadences. Our disciplined scope selection, variable transparency, and yearly update rhythm make our baseline the dependable choice for planning.

Key gap drivers include some publishers bundling hardware with consumables, others freezing 2019 ASPs, and a few anchoring growth on conservative mAb scenarios no longer aligned with current late-stage pipelines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 479.69 M (2025) | Mordor Intelligence | - |

| USD 418.2 M (2023) | Global Consultancy A | Excludes HCIC consumables and keeps pre-COVID tariffs |

| USD 320.3 M (2021) | Industry Journal B | Uses constant 2019 ASPs with no currency conversion |

| USD 688.89 M (2022) | Regional Consultancy C | Bundles HIC instruments with consumables |

Taken together, these contrasts show that Mordor's balanced blend of spend mapping and supplier reality checks yields a transparent, repeatable baseline that decision makers can trust.

Key Questions Answered in the Report

What is the current value of the hydrophobic interaction chromatography market?

The market is valued at USD 513.41 million in 2026 and is projected to grow at a 7.03% CAGR through 2031.

Why are monoclonal antibodies so crucial for hydrophobic interaction chromatography adoption?

They account for 51.84% of 2025 revenue, and their purification trains universally include an HIC polish to meet tight aggregate specifications.

Which geography is growing fastest in hydrophobic interaction chromatography?

Asia Pacific is estimated to grow at the highest CAGR 10.85% over the forecast period (2026-2031).

Which region has the biggest share in Global Hydrophobic Interaction Chromatography Market?

In 2025, the North America accounts for the largest market share in Global Hydrophobic Interaction Chromatography Market.

What years does this Global Hydrophobic Interaction Chromatography Market cover?

The report covers the Global Hydrophobic Interaction Chromatography Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Hydrophobic Interaction Chromatography Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: