FRP Vessels Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

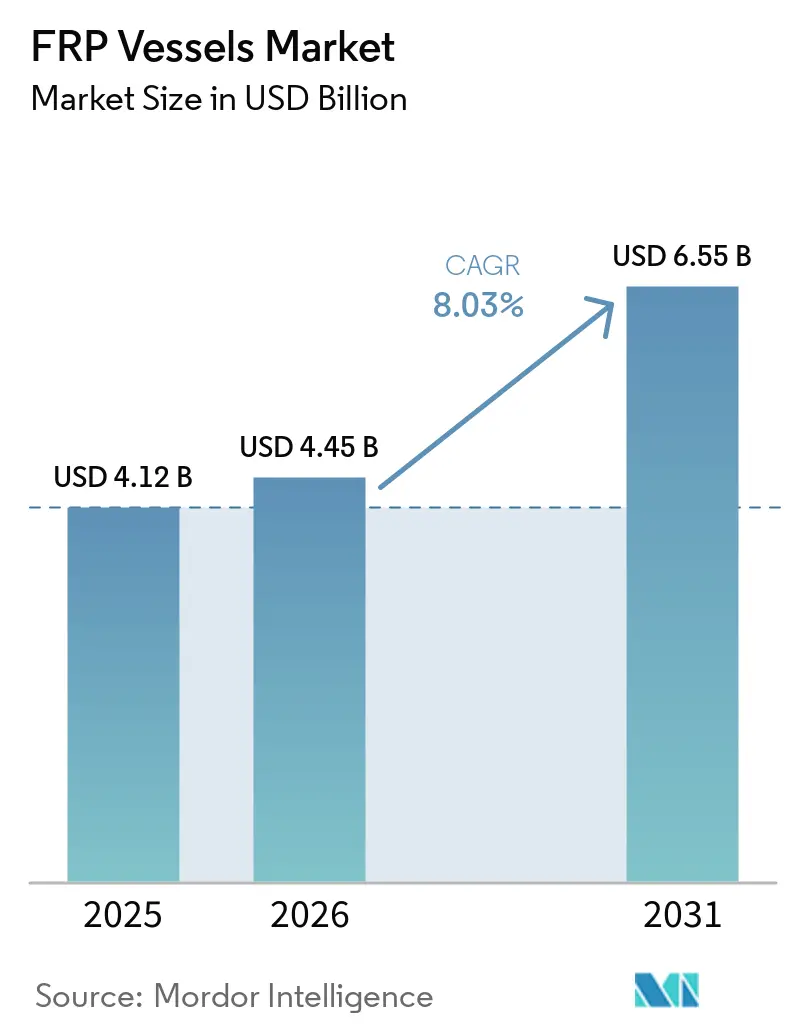

| Market Size (2026) | USD 4.45 Billion |

| Market Size (2031) | USD 6.55 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

FRP Vessels Market Analysis by Mordor Intelligence

The FRP Vessels Market size is projected to be USD 4.12 billion in 2025, USD 4.45 billion in 2026, and reach USD 6.55 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031. Growth stems from an industry pivot away from corrosion-prone steel toward lightweight composites that align with green-hydrogen mandates, large-scale desalination rollouts, and the global backlog of municipal water upgrades. Medium pressure designs dominate near-term demand, but high pressure cylinders for mobility are scaling faster as automotive fuel-cell platforms migrate to 700-bar systems. Glass fiber remains the revenue mainstay, yet carbon fiber’s share is widening in high-performance hydrogen and offshore duties. Asia-Pacific sets the pace through aggressive vessel capacity scale-ups in China and infrastructure renewal across India, while North America and Europe benefit from hydrogen incentives and tightening water regulations. Competitive activity is steady rather than tumultuous, with filament-winding specialists deepening automation and hydrogen-tank integrators expanding geographic footprints.

Key Report Takeaways

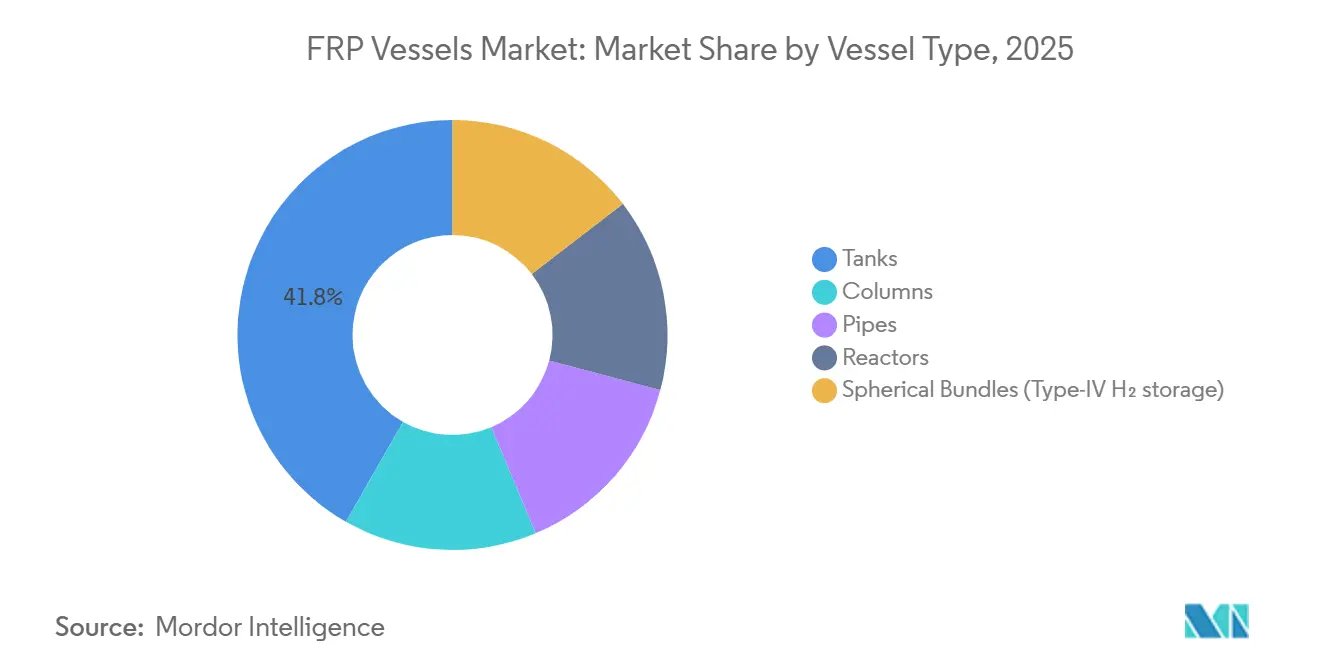

- By vessel type, tanks led with 41.76% of the FRP vessels market share in 2025, while reactors will post the fastest 8.69% CAGR through 2031.

- By pressure classification, medium pressure (10–250 bar) commanded 46.01% the FRP vessels market share in 2025, whereas high pressure (≥250 bar) is advancing at an 8.92% CAGR through 2031.

- By fiber type, glass fiber captured 64.83% of the FRP vessels market share in 2025, whereas carbon fiber is projected to expand at an 8.55% CAGR through 2031.

- By application, water and wastewater treatment held 34.93% of the FRP vessels market share in 2025, while hydrogen and alternative-fuels storage are forecast to surge at a 9.05% CAGR through 2031.

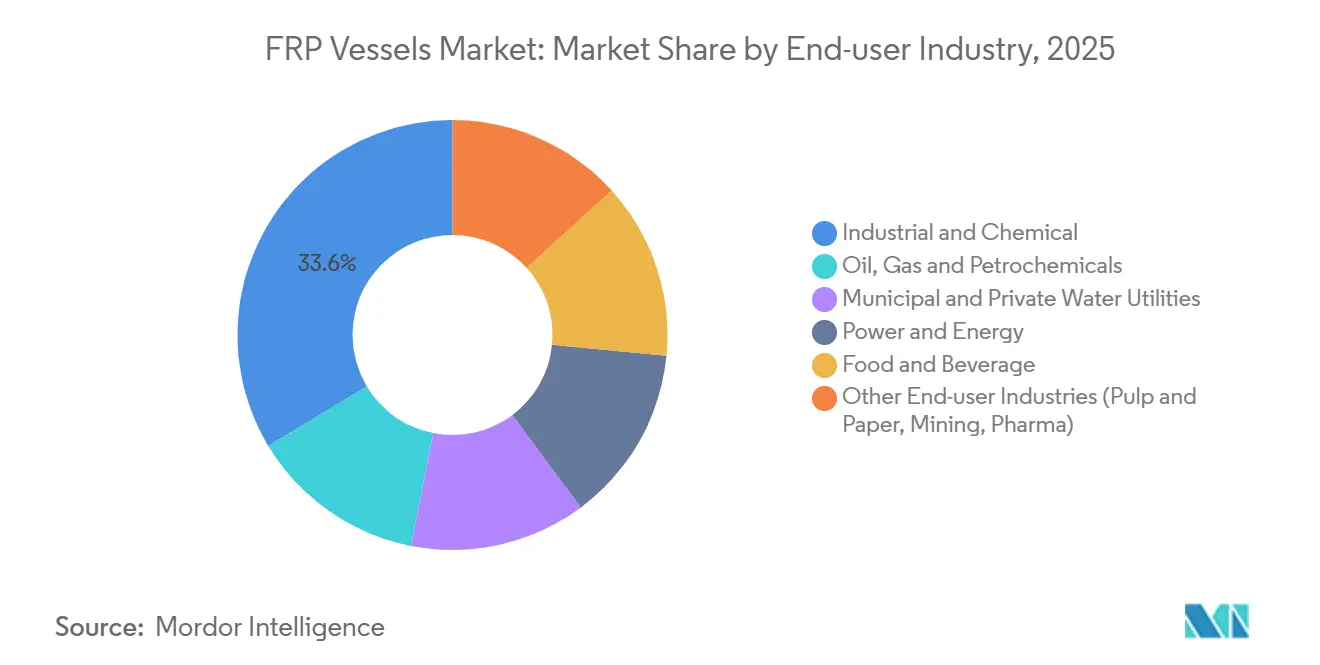

- By end-user industry, industrial and chemical accounted for 33.63% of the FRP vessels market share in 2025, yet power and energy will grow fastest at 9.29% CAGR through 2031.

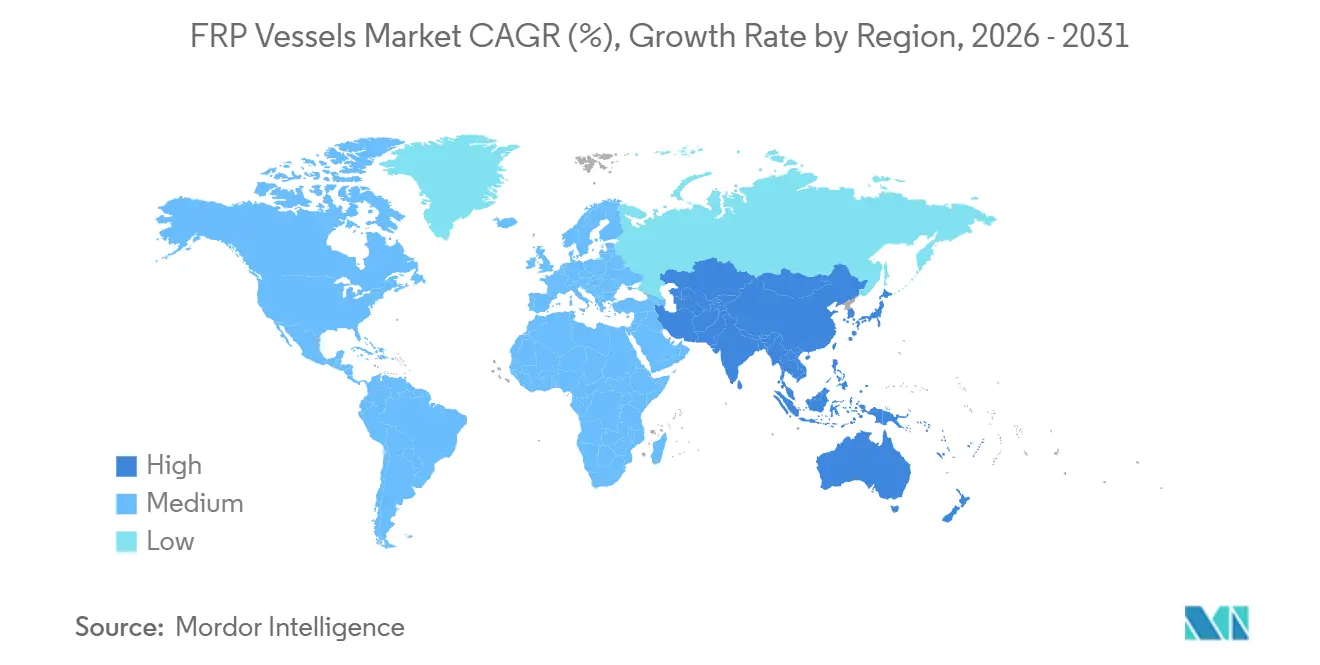

- By geography, Asia-Pacific captured 44.89% of the FRP vessels market share in 2025 and will rise at a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global FRP Vessels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of lightweight, corrosion-resistant materials | +1.8% | Global, with concentration in coastal and chemical zones | Medium term (2–4 years) |

| Rising demand from water and wastewater utilities | +1.6% | Asia-Pacific, North America, Middle-East | Short term (≤ 2 years) |

| Expansion of chemical and petrochemical processing capacity | +1.3% | Asia-Pacific core, spill-over to Middle-East | Medium term (2–4 years) |

| Growth in renewable-energy and desalination projects | +1.2% | Middle-East, Southern Europe, North Africa | Medium term (2–4 years) |

| Rapid hydrogen storage roll-out for fuel-cell mobility | +1.4% | North America, EU, Japan, South Korea, China | Long term (≥ 4 years) |

| National green-hydrogen mandates unlocking long-run captive demand | +0.9% | EU, United States, China, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of Lightweight, Corrosion-Resistant Materials

FRP vessels reduce weight by approximately 70% compared to steel, easing transport and lowering foundation loads in retrofits. Offshore platforms and marine desalination sites prefer composites to eliminate galvanic corrosion, extending service life beyond 30 years without coatings. Chemical plants integrate dual-laminate designs for acids and alkalis, avoiding liner delamination seen in steel. Encore Arabia supplied such tanks to the Saudi Water Conversion Corporation in 2025, reinforcing FRP’s viability in high-temperature seawater service[1]Future Pipe Industries, “Encore Arabia Dual-Laminate Solutions,” futurepipe.com. The lifetime-cost advantage outweighs higher upfront prices in harsh operating environments.

Rising Demand from Water and Wastewater Utilities

North American municipalities accelerated steel-to-FRP replacements in 2024-2025 after corrosion failures, with the Zone 7 Water Agency and the Florida Governmental Utility Authority citing lower maintenance and NSF/ANSI 61 compliance. First Line’s 3,019-unit order for Qinghai lithium projects shows cross-sector pull between industrial water and mining. India’s prefabricated sewage systems increasingly specify FRP for chloride-rich waste streams, leveraging modular moving-bed biofilm designs for rapid installation. Deferred maintenance backlogs now fuel a multiyear procurement wave.

Expansion of Chemical and Petrochemical Processing Capacity

Asia-Pacific refinery and petrochemical build-outs favor FRP for produced water, crude, and chemical intermediates because the material resists hydrogen sulfide and organic acids. PetroChina Dushanzi’s April 2025 reactor order underscores China’s localization drive. Middle-East complexes specify FRP reactors and columns for chlor-alkali and fertilizer duty, with Future Pipe Industries partnering with Saudi Aramco to deepen in-kingdom composites supply. Larger single-train plants demand vessels beyond 4 m diameter, pushing filament-winding machinery to new limits.

Growth in Renewable Energy and Desalination Projects

Gulf desalination expansions rely on FRP housings for reverse-osmosis membranes, brine storage, and dosing units. Al Johi built a 500 m³ monolithic tank for Saudi Arabia’s Ministry of Water, proving field-joint elimination benefits. Renewable integration requires composite tanks for thermal fluids in concentrated solar power and hydrogen buffers at wind farms. The EU-funded HYGHER project allocates EUR 5 million to high pressure hydrogen value chains, including composite storage. Factory-fabricated vessels cut onsite labor and sidestep the skilled-welder shortage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial CAPEX and installation costs | -1.1% | Global, acute in price-sensitive municipal tenders | Short term (≤ 2 years) |

| Limited recyclability and end-of-life pathways | -0.7% | EU, North America (circular-economy mandates) | Medium term (2–4 years) |

| Skilled-labor shortages in large-diameter filament winding | -0.9% | North America, Europe, emerging Asia-Pacific | Medium term (2–4 years) |

| Inconsistent global codes and standards for FRP pressure vessels | -0.6% | Global, fragmentation across UN, ASME, ISO, TPED | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX and Installation Costs

Composite vessels cost 1.5-to-2.5× steel alternatives, deterring budget-constrained utilities despite lower lifecycle totals. Large-diameter winders exceed USD 500,000, and specialized lifting gear adds another 10-15% to the delivered price. Retrofit sites may need foundation upgrades due to altered load paths, inflating civil budgets. Familiarity bias also steers buyers toward steel even after corrosion failures shorten tank life.

Limited Recyclability and End-of-Life Pathways

Thermoset resins resist remelting, leaving only mechanical grinding, pyrolysis, or solvolysis. Mechanical routes consume 0.27-2.03 MJ/kg and recover fibers with 50-70% of virgin strength. Global carbon-fiber recovery capacity is near 6,120 tons per year, far below installed composite stock, and glass-fiber recycling is largely absent. EU circular-economy directives will impose take-back obligations by 2028, pressuring margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vessel Type: Tanks Dominate, Reactors Accelerate

Tanks accounted for 41.76% of the 2025 revenue, maintaining their dominance in the FRP vessels market due to their extensive use in water treatment and chemical storage. Reactors are projected to grow at a CAGR of 8.69% through 2031, driven by their reliability in handling chemical and thermal stress in process industries. Hybrid tank-reactor designs, incorporating mixers and jackets, are redefining traditional categories, while sanitary fermenters for food and biotech applications contribute to additional market demand.

Process plants increasingly specify ASME RTP-1 or BPE-compliant reactors to avoid pitting issues associated with stainless steel. Pharmaceutical manufacturers are adopting 1,000-20,000 L filament-wound vessels for their smooth inner surfaces, which facilitate CIP operations. Food processors are utilizing FRP fermenters for products like soy sauce and vinegar, while hydrogen mobility is driving the adoption of spherical cylinder bundles in fleet depots. The FRP vessels market continues to emphasize application-specific engineering over standardized solutions.

By Pressure Classification: Medium Pressure Leads, High Pressure Surges

Medium pressure vessels (10–250 bar) contributed 46.01% of the 2025 revenue, dominating the FRP vessels market across industrial gases and municipal networks. High pressure vessels (≥250 bar) are expected to grow at a CAGR of 8.92% through 2031, driven by demand for 350-bar logistics and 700-bar mobility cylinders.

The ASME RTP-1:2023 standard governs sub-1 bar vessels, while UN R134, TPED, and ISO 14692 regulate high pressure hydrogen applications, leading to increased testing costs. The Welding Research Council’s 2025 Bulletin 601 provides guidance for in-service inspections, addressing owner concerns. While code convergence remains a challenge, progress is being made through collaborative working groups.

By Fiber Type: Glass Fiber Prevails, Carbon Fiber Gains

Glass fiber accounted for 64.83% of the 2025 market value, driven by its cost-effectiveness for water and chemical tanks. Carbon fiber is projected to grow at a CAGR of 8.55% through 2031, supported by its high tensile strength (6 GPa) and increasing demand in mobility and offshore sectors. The market for carbon fiber-based FRP vessels is expected to expand significantly, particularly in hydrogen transport applications.

Towpreg wet winding enhances dimensional accuracy to ±0.5 mm but incurs a 20-30% material cost premium. Process modeling indicates that winding tensions of 2-50 lbf achieve fiber volume fractions of 52-65%, impacting burst strength and mandrel release. Hybrid glass-carbon lay-ups are gaining traction in applications requiring intermediate performance at lower costs.

By Application: Water and Wastewater Treatment Anchors, Hydrogen and Alternative-Fuels Storage Accelerates

Water and wastewater treatment accounted for 34.93% of the 2025 revenue, driven by municipal replacements in the U.S. and Asia. Hydrogen and alternative-fuels storage is projected to grow at a CAGR of 9.05% through 2031, emerging as the most dynamic segment within the FRP vessels market. Power and desalination plants are incorporating FRP housings in thermal loops, while petrochemical facilities are deploying corrosion-resistant columns.

California utilities have reported 30-year lifespan projections for new FRP tanks, eliminating the need for cathodic protection. Hexagon Composites’ USD 11.7 million order in Mexico for 2026 highlights Latin America’s growing hydrogen infrastructure. Diverging performance requirements are segmenting supply chains into low pressure, glass fiber solutions and high pressure, carbon fiber cylinders.

By End-user Industry: Industrial and Chemical, Power and Energy Surges

The industrial and chemical industry accounted for 33.63% of the 2025 revenue, maintaining its leadership in the FRP vessels market through applications in specialty acids, fertilizers, and pharmaceuticals. The power and energy industry is projected to grow at a CAGR of 9.29% through 2031, driven by desalination and renewable energy integration projects, particularly in arid regions. Municipal utilities are replacing aging steel tanks to achieve lifecycle savings, while food processors demand sanitary interiors resistant to biofilm formation.

Future Pipe Industries’ contracts in Saudi Arabia secure volumes for petrochemical applications, while Shalin Composites exports Indian-made units to Gulf water projects. Purchase decisions vary by industry: chemical orders prioritize process compatibility, power projects focus on speed and modularity, and food applications emphasize compliance with health standards.

Geography Analysis

Asia-Pacific captured 44.89% of the 2025 revenue and is projected to grow at a CAGR of 9.18% through 2031, supported by China’s 600-unit-per-day RO vessel production facility and India’s water renewal programs. South Korea’s goal of deploying 6.2 million fuel-cell vehicles by 2040 sustains demand for high pressure cylinders, while ASEAN countries adopt FRP for palm-oil and aquaculture facilities. Government subsidies and local fiber supply chains help maintain low production costs, reinforcing the region’s dominance.

North America benefits from steel infrastructure replacements and shale-gas water handling. Zone 7 and Florida authorities installed FRP potable-water tanks in 2025, reporting reduced maintenance costs. Hexagon Purus increased its Maryland production capacity to 10,000 cylinders annually[2]Hexagon Composites, “Cylinder Capacity Expansion in Maryland,” hexagoncomposites.com, while Canada’s oil sands adopted FRP for tailings water management. The U.S. Inflation Reduction Act’s hydrogen credits are supporting the establishment of new high pressure vessel plants.

Europe blends strict circular-economy regulations with hydrogen development initiatives. The EU Clean Hydrogen Partnership funds R&D, and German facilities produce 40,000 cylinders annually. Southern Europe and North Africa are opting for FRP housings in desalination pipelines to prevent seawater corrosion. The Middle-East relies on composites for large-scale desalination and petrochemical projects, with Saudi Aramco partnering with Future Pipe Industries to localize supply. Latin America is showing early momentum with Mexico’s hydrogen-cylinder order and Brazil’s chemical expansions, though its capacity lags behind Asia-Pacific.

Competitive Landscape

The FRP vessels market is low concentrated. Future Pipe Industries, Hexagon Composites, and Worthington dominate the high pressure hydrogen storage segment, while regional players like Shalin Composites and EPP Composites focus on water and chemical applications. Hexagon’s acquisition of Worthington’s Sustainable Energy Solutions in July 2025 eliminated a direct competitor in the CNG segment and consolidated Type-IV capacity. Future Pipe Industries’ November 2025 agreement with Saudi Aramco secures contracts for petrochemical and utility projects with local content alignment.

First Line’s 20,000 m² facility in China, operational since March 2025, produces 600 RO vessels daily, leveraging cost efficiencies to penetrate export markets. Roth Composite Machinery and Mikrosam are advancing automation with fiber-change modules and offline programming, reducing labor costs by up to 30%. Innovation clusters include self-sensing vessels under the ISIMON project and Fraunhofer IPT’s smartVessel, which integrates fiber-optic sensors for health monitoring. Market participants are increasingly divided into high-volume automated producers and low-volume custom fabricators.

FRP Vessels Industry Leaders

Future Pipe Industries

Hexagon Composites ASA

NOV

Plasticon

Worthington Enterprises

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Future Pipe Industries received the Make it in the Emirates (MIITE) and In-Country Value (ICV) certifications in the United Arab Emirates (UAE). These certifications highlighted the company's contribution to the FRP vessels market by supporting local manufacturing and aligning with the UAE's sustainability objectives.

- July 2025: Hexagon Composites ASA expanded its presence in the clean fuel business by acquiring full ownership of Sustainable Energy Solutions (SES) from Worthington Enterprises. This acquisition is expected to strengthen Hexagon's position in the FRP vessels market, as SES specializes in manufacturing high pressure gas cylinders used for hydrogen storage, LPG, and CNG.

Global FRP Vessels Market Report Scope

FRP (Fiberglass Reinforced Plastic) vessels are durable, corrosion-resistant tanks used for water treatment, filtration, and chemical storage. They serve as a lightweight and cost-effective alternative to stainless steel and are commonly utilized in RO plants, residential water softeners, and industrial processing.

The FRP Vessels Market is segmented into vessel type, pressure classification, fiber type, application, end-user industry, and geography. By vessel type, the market is segmented into tanks, columns, pipes, reactors, and spherical bundles (type-IV H₂ storage). By pressure classification, the market is segmented into low pressure (≤10 bar), medium pressure (10–250 bar), and high pressure (≥250 bar). By fiber type, the market is segmented into glass fiber, carbon fiber, aramid fiber, and hybrid fiber (glass-carbon/glass-basalt). By application, the market is segmented into water and wastewater treatment, chemical processing and storage, oil, gas, and petrochemical upstream, food and beverage processing, power generation and desalination, hydrogen and alternative-fuels storage, and pharmaceutical and biotech fluids. By end-user industry, the market is segmented into industrial and chemical, oil, gas, and petrochemicals, municipal and private water utilities, power and energy, food and beverage, and other end-user industries (pulp and paper, mining, pharma). The report also covers the market size and forecasts for FRP vessels in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Tanks |

| Columns |

| Pipes |

| Reactors |

| Spherical Bundles (Type-IV H₂ storage) |

| Low Pressure (≤10 bar) |

| Medium Pressure (10–250 bar) |

| High Pressure (≥250 bar) |

| Glass Fiber |

| Carbon Fiber |

| Aramid Fiber |

| Hybrid Fiber (Glass-Carbon/Glass-Basalt) |

| Water and Wastewater Treatment |

| Chemical Processing and Storage |

| Oil, Gas and Petrochemical Upstream |

| Food and Beverage Processing |

| Power Generation and Desalination |

| Hydrogen and Alternative-Fuels Storage |

| Pharmaceutical and Biotech Fluids |

| Industrial and Chemical |

| Oil, Gas and Petrochemicals |

| Municipal and Private Water Utilities |

| Power and Energy |

| Food and Beverage |

| Other End-user Industries (Pulp and Paper, Mining, Pharma) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Vessel Type | Tanks | |

| Columns | ||

| Pipes | ||

| Reactors | ||

| Spherical Bundles (Type-IV H₂ storage) | ||

| By Pressure Classification | Low Pressure (≤10 bar) | |

| Medium Pressure (10–250 bar) | ||

| High Pressure (≥250 bar) | ||

| By Fiber Type | Glass Fiber | |

| Carbon Fiber | ||

| Aramid Fiber | ||

| Hybrid Fiber (Glass-Carbon/Glass-Basalt) | ||

| By Application | Water and Wastewater Treatment | |

| Chemical Processing and Storage | ||

| Oil, Gas and Petrochemical Upstream | ||

| Food and Beverage Processing | ||

| Power Generation and Desalination | ||

| Hydrogen and Alternative-Fuels Storage | ||

| Pharmaceutical and Biotech Fluids | ||

| By End-user Industry | Industrial and Chemical | |

| Oil, Gas and Petrochemicals | ||

| Municipal and Private Water Utilities | ||

| Power and Energy | ||

| Food and Beverage | ||

| Other End-user Industries (Pulp and Paper, Mining, Pharma) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the FRP vessels market?

The FRP vessels market stands at USD 4.45 billion in 2026 and is projected to reach USD 6.55 billion by 2031.

Which vessel type will grow fastest through 2031?

Reactors are expected to register the highest 8.69% CAGR through 2031.

How quickly will high pressure FRP vessels expand through 2031?

The high pressure segment is forecast to grow at an 8.92% CAGR between 2026 and 2031.

Why is carbon fiber growing fastest through 2031?

Mobility and offshore applications demand higher tensile strength, pushing carbon fiber adoption at an 8.55% CAGR through 2031.

Page last updated on: