Friedreich's Ataxia Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

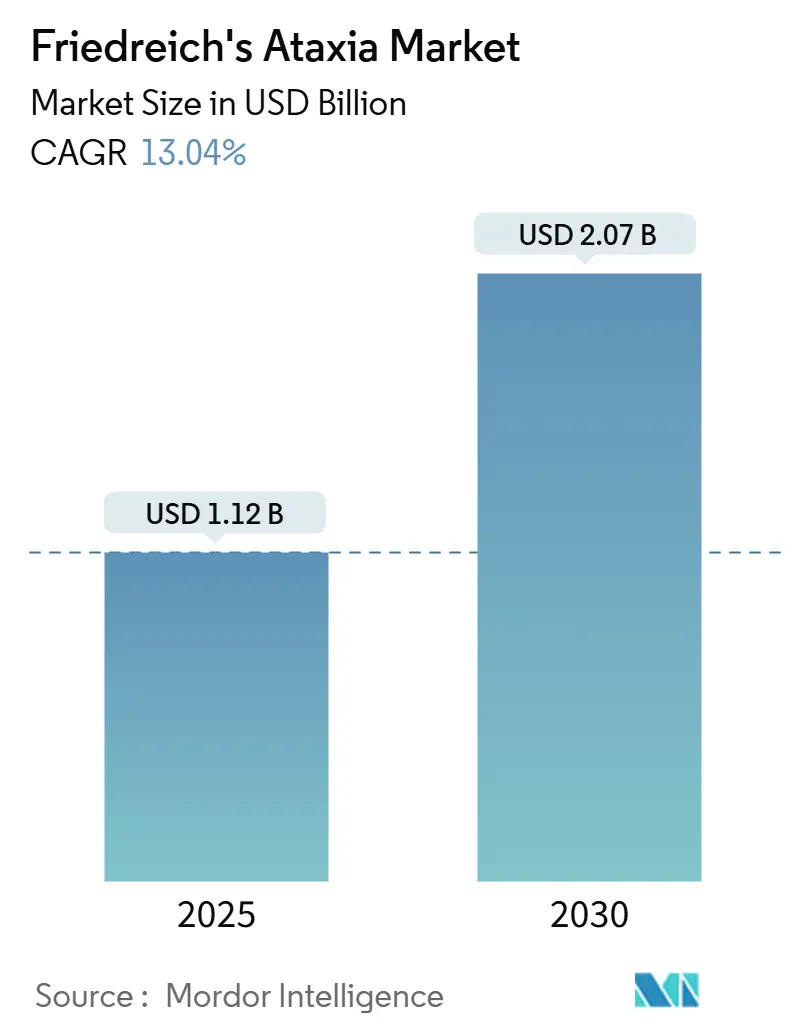

| Market Size (2025) | USD 1.12 Billion |

| Market Size (2030) | USD 2.07 Billion |

| Growth Rate (2025 - 2030) | 13.04% CAGR |

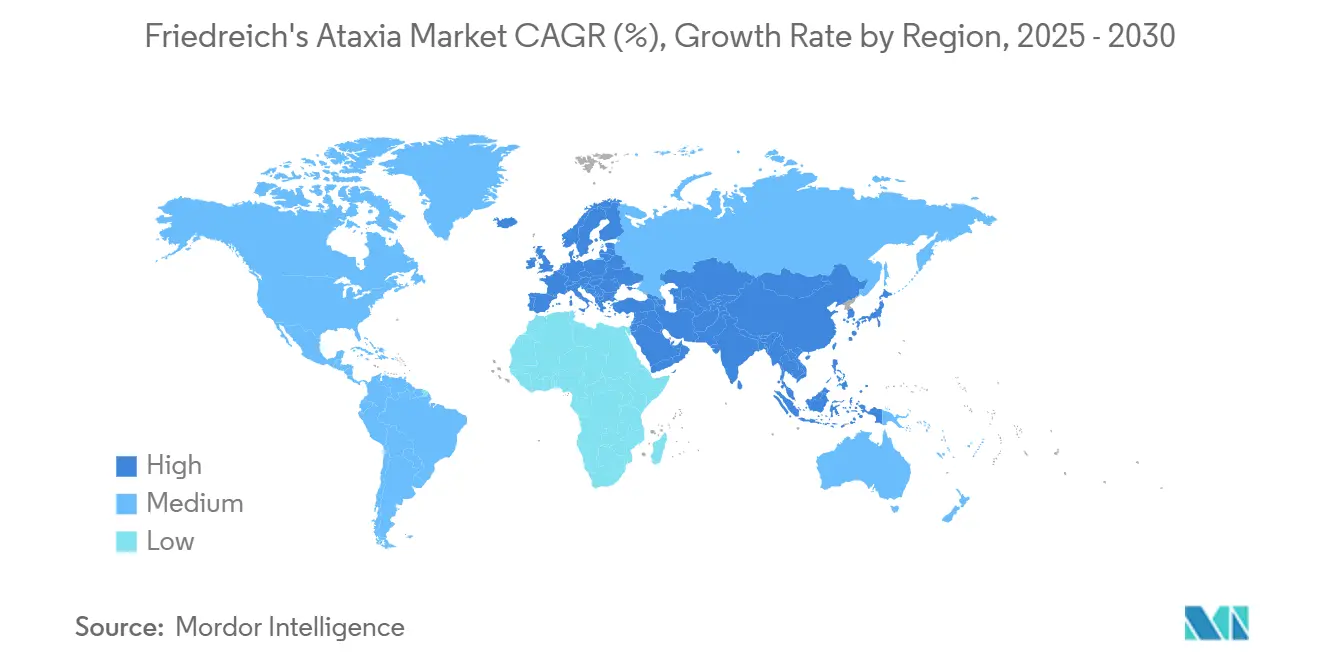

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

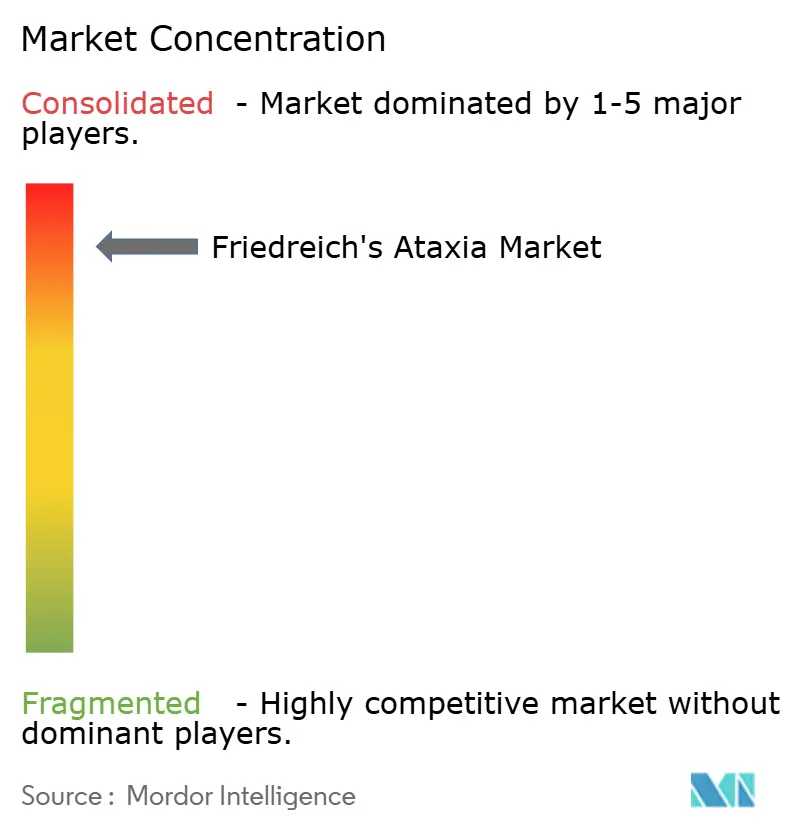

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Friedreich's Ataxia Market Analysis by Mordor Intelligence

The Friedreich's ataxia market size stood at USD 1.12 billion in 2025 and is on track to reach USD 2.07 billion by 2030, reflecting a robust 13.04% CAGR. Momentum stems from the first-in-class approval of omaveloxolone, fast-rising gene-therapy pipelines, and broader newborn screening that identifies patients earlier. Capital inflows accelerate as manufacturers race to expand adeno-associated virus (AAV) capacity, while specialty-pharmacy networks refine logistics for ultra-rare treatments. Investors see durable pricing power, yet long-term growth still hinges on resolving viral-vector bottlenecks and generating cost-effectiveness data acceptable to payers. Competitive intensity remains moderate because technical barriers in vector production and clinical development restrict new entrants.

Key Report Takeaways

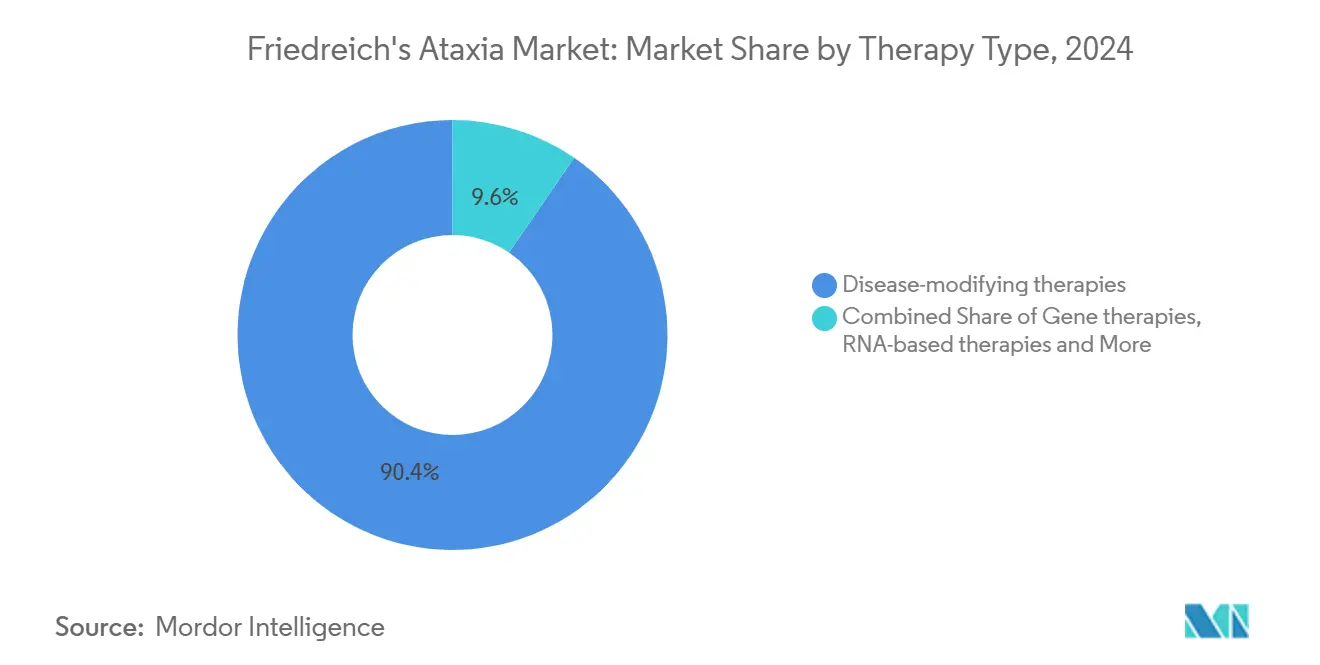

- By therapy type, disease-modifying drugs held 90.43% Friedreich's ataxia market share in 2024; gene therapies are set to climb at an 11.23% CAGR to 2030.

- By drug class, antioxidant/Nrf2 activators commanded 88.56% of the Friedreich's ataxia market size in 2024, whereas mitochondrial stabilizers are expanding at a 10.52% CAGR through 2030.

- By route, oral products accounted for a 89.37% share in 2024; intrathecal delivery is advancing at a 9.01% CAGR as next-generation vectors move into late-stage trials.

- By age group, adults (18–40 years) represented 61.22% of revenue in 2024; pediatric use is rising fastest at a 9.64% CAGR, driven by vataquinone’s priority review.

- By distribution channel, specialty pharmacies captured 68.62% share in 2024, while hospital pharmacies are growing at 11.89% CAGR as gene-therapy infusions shift care to tertiary centers.

- By geography, North America controlled 52.34% revenue in 2024; Asia-Pacific is projected to register a 9.47% CAGR to 2030 supported by expanding rare-disease registries.

Global Friedreich's Ataxia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| First disease-modifying approval (omaveloxolone) | +3.2% | North America, Europe | Short term (≤ 2 years) |

| Gene-therapy R&D ramp-up | +2.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Broader patient registries | +2.1% | Global, with APAC acceleration | Medium term (2-4 years) |

| Newborn-screen panel expansion | +1.9% | North America, Europe, selective APAC | Long term (≥ 4 years) |

| AI-enabled drug repurposing | +1.6% | Global research hubs | Long term (≥ 4 years) |

| Orphan-drug tax incentives | +1.4% | Primarily North America, growing in EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

First disease-modifying approval (omaveloxolone)

Regulators cleared omaveloxolone in 2023, and the product quickly demonstrated measurable gains on the modified Friedreich’s Ataxia Rating Scale, reversing a prior paradigm that focused only on symptom relief.[1]U.S. Food and Drug Administration, “FDA Approves First Treatment for Friedreich’s Ataxia,” fda.gov European authorization in 2024 broadened access to 27 member states and ignited price negotiations that shape global launch strategies. Long-term data show a 55% slowdown in functional decline, forcing pipeline competitors to prove either greater durability or single-dose convenience. Validation of the Nrf2 pathway has unlocked investment in next-gen antioxidants, and modified rating-scale endpoints have become acceptable surrogates, streamlining trial design. Payers still scrutinize lifetime value, yet early clinical gains provide the Friedreich's ataxia market with clear proof that a disease trajectory can be shifted.

Gene-therapy R&D ramp-up

Companies now target frataxin restoration at its genetic origin. Lexeo’s LX2006 cut left-ventricular mass index by 11.4% at 12 months in cardiomyopathy patients.[2]Lexeo Therapeutics, “Positive Interim Phase 1/2 Data of LX2006,” lexeotx.comVoyager, in collaboration with Neurocrine, has selected a candidate that combines novel capsids with robust spine tropism and plans to initiate first-in-human dosing in 2025. Capacity gaps compel construction of purpose-built plants such as Novartis’s Colorado facility and Roche’s EUR 90 million German center, yet vector shortages still postpone some trials. Capital is flowing toward in-house manufacturing to control quality and scale. The surge boosts innovation but also magnifies raw-material constraints that may temper near-term Friedreich's ataxia market growth.

Broader patient registries & earlier diagnosis

Cross-border data networks refine natural-history curves, letting sponsors power trials with fewer subjects and shorter timelines. The U.S. FA Identified program funds no-cost genetic testing for individuals over 16 years, raising confirmed diagnoses.[3]PreventionGenetics, “Biogen FA Identified Program,” preventiongenetics.com Triple-quadrupole mass spectrometry now pinpoints compound heterozygotes that legacy assays miss, increasing carrier detection. Grants from the U.S. Department of Defense enable genomic studies that reveal milder phenotypes associated with shorter GAA expansions, offering future opportunities for stratified medicine. High-resolution MRI and DTI biomarkers detect disease progression within one year, providing sensitive endpoints for early-stage programs. Together, these tools expand the treatable population, underpinning steady growth in the Friedreich's ataxia market.

Newborn-screen panel expansion

States such as California and New York are reviewing proposals to add frataxin gene testing to routine screens, inspired by successes with spinal muscular atrophy. Earlier identification could shift the treatment window to infancy, where neuronal plasticity is at its highest, potentially cementing lifelong benefits. Implementation costs remain an obstacle, yet public-health models show that early gene-therapy intervention may avert downstream social-care spending. Pilot studies in Italy and Japan report positive parental acceptance and minimal false-positive rates. Rollout pace hinges on reimbursement for confirmatory genetic workups and post-diagnosis counseling. If adoption widens, the Friedreich's ataxia market could add hundreds of newly diagnosed patients annually.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Small patient pool limiting ROI | –2.9% | Global, more acute in emerging markets | Long term (≥ 4 years) |

| High therapy cost & reimbursement hurdles | –2.3% | Global, variable by payer system | Medium term (2-4 years) |

| Mitochondrial-toxicity concerns | –1.8% | Regions with strict safety regulators | Short term (≤ 2 years) |

| Limited viral-vector capacity | –1.6% | Worldwide, with APAC bottlenecks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Small patient pool limiting ROI

Only around 25,000 people live with Friedreich’s ataxia worldwide, equating to a prevalence of 1 in 20,000 to 1 in 50,000 among Caucasian populations. Ultra-rare economics push list prices beyond USD 300,000 per year, triggering payer pushback even in high-income countries. Recruitment can stretch multiple years because patients are dispersed across continents and must meet strict genotype criteria. Multinational trials inflate costs through duplicative regulatory submissions. Variable disease severity, tied to GAA repeat length, requires larger sample sizes, further eroding return prospects.

High therapy cost & reimbursement hurdles

Omaveloxolone’s retail price approaches USD 370,000 annually and usually requires prior authorization. Gene-therapy candidates anticipate launch prices that could exceed USD 1 million per dose, straining health technology assessment models. Europe’s decentralized reimbursement means time-to-revenue varies from months in Germany to years in Spain. In the United States, the Inflation Reduction Act still casts uncertainty over long-term pricing, although orphan-drug carve-outs ease near-term pressure. Emerging markets struggle to fund ultra-rare treatments, limiting global Friedreich's ataxia market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Disease-Modifying Treatments Underpin Growth

Disease-modifying therapies accounted for 90.43% of 2024 revenue, driven by the adoption of SKYCLARYS across the United States and Europe. The Friedreich's ataxia market size for gene therapies is expected to surge at 11.23% CAGR, reflecting the advancement of programs such as LX2006 and Voyager’s candidate. Demand momentum signals a paradigm shift from symptomatic relief to interventions that slow or halt progression. Gene-therapy uptake depends on vector supply, surgical expertise for intrathecal dosing, and long-term durability data. Protein replacement and RNA-based strategies remain active but face competition for trial participants.

The Friedreich's ataxia market benefits from regulatory precedent, yet commercial risk clusters around manufacturing scale-up and payer negotiations. Sponsors weigh single-dose pricing models against the potential need for retreatment. Combination regimens may emerge, pairing antioxidants with genetic or protein restoration to address both upstream and downstream pathology. Investor focus is turning toward assets with differentiated delivery or tissue targeting that can bypass vector immunity and extend patient eligibility.

By Drug Class: Antioxidants Retain Lead, Stabilizers Accelerate

Antioxidant/Nrf2 activators held 88.56% Friedreich's ataxia market share in 2024 thanks to omaveloxolone’s launch success. The class enjoys oral convenience, scalable small-molecule manufacturing, and well-characterized safety. Nonetheless, mitochondrial stabilizers post a 10.52% CAGR, buoyed by Phase 2 data from nomlabofusp that showed dose-dependent increases in frataxin levels. Drug-class diversification hedges against single-mechanism failure and paves the way for the development of combination therapies.

Pipeline programs are exploring PPAR agonists, frataxin gene vectors, and novel redox modulators. Each mechanism has differing regulatory paths and cost structures, which influence investment strategies. Sponsors with robust CMC platforms can shorten timelines, giving antioxidants a time-to-market edge, while gene vectors promise transformative efficacy once manufacturing matures.

By Route of Administration: Oral Dominance Faces Targeted Delivery Needs

Oral products accounted for 89.37% of revenue in 2024, securing adherence and facilitating broad community and clinic prescribing. Intrathecal delivery grows at the fastest rate, with a 9.01% CAGR, as gene therapies require direct access to the cerebellum or spinal cord. Intravenous routes serve protein replacement regimens and systemic gene-therapy approaches, yet call for infusion centers and cold-chain logistics.

High-touch delivery models push hospitals to outfit neurology suites with specialized catheters and imaging guidance. Oral regimens will maintain market presence due to their ease of use and payer familiarity, but targeted approaches are essential for achieving central nervous system frataxin restoration. Over time, route diversification strengthens the Friedreich's ataxia market by matching therapy modality to disease biology.

By Age Group: Adult Care Shifts Toward Pediatric Intervention

Adults aged 18-40 generated 61.22% of 2024 sales as current labels focus on onset after adolescence. The segment is mature, with established diagnostic pathways and treatment centers. Pediatric uptake is projected to grow at a 9.64% CAGR through 2030, as vatiquinone seeks FDA approval for children, and BRAVE, a global Phase 3 study, evaluates omaveloxolone in patients as young as 2 years.

Earlier intervention could delay irreversible neuron loss, boosting lifetime quality-adjusted life years. Pediatric programs struggle with age-appropriate endpoints, weight-based dosing, and long-term follow-up; however, success would expand the Friedreich's ataxia market size and shift the revenue mix toward younger cohorts. Late-onset patients remain a niche yet medically necessary segment that may need adjusted dosing due to comorbidities.

By Distribution Channel: Specialty Pharmacies Hold Sway, Hospitals Gain Ground

Specialty pharmacies accounted for 68.62% of 2024 sales, as they handle prior authorization, financial counseling, and cold-chain coordination for high-cost, rare-disease drugs. Hospital pharmacies, however, are growing at an 11.89% CAGR in lockstep with gene-therapy infusions that must be administered in controlled settings.

Health systems develop integrated care pathways that link neurology, cardiology, and rehabilitation. Specialty channels remain critical for ongoing refill management and adherence monitoring. Over time, a hybrid model may dominate, with hospitals leading induction dosing and specialty networks overseeing maintenance. Strategic channel optimization expands reach, keeps costs in check, and sustains growth in the Friedreich's ataxia market.

Geography Analysis

North America accounted for 52.34% of 2024 revenue, driven by early FDA clearance, robust orphan-drug incentives, and mature specialty pharmacy ecosystems. U.S. academic hubs offer trial infrastructure and patient registry depth, which reduces development risk. Canada offers public reimbursement through special-access programs, albeit at a slower rate, while Mexico increases volume through private clinics serving cross-border patients. Manufacturing clusters in Massachusetts, North Carolina, and Colorado give the region supply resilience that underpins the Friedreich's ataxia market.

Europe follows with rapid but heterogeneous adoption. EMA approval grants centralized marketing, yet national health-technology-assessment deadlines vary, creating complexity in the launch sequence. Germany’s early-access environment accelerates revenue ramp, whereas Spain and Italy proceed more slowly. Investments in Belgian and German vector plants shorten supply chains, but capacity remains constrained. Patient-advocacy groups secure research funding and influence reimbursement debates, maintaining a favorable policy climate.

Asia-Pacific is the fastest-growing region at 9.47% CAGR to 2030 thanks to policy shifts in China, Japan, and Australia that boost rare-disease visibility. China’s national rare-disease list supports accelerated approval and tax rebates, though reimbursement remains piecemeal. Japan’s Sakigake pathway rewards innovation with priority review. Limited vector capacity forces reliance on imports, so any Western production glitch ripples across APAC. Countries are expanding newborn-screen pilots and patient registries, which will unlock incremental Friedreich's ataxia market demand as diagnostic rates improve.

Competitive Landscape

The Friedreich's ataxia market is moderately concentrated. Biogen solidified its leadership after acquiring Reata for USD 7.3 billion in 2024, gaining SKYCLARYS and its established prescriber base. Lexeo and Voyager advance gene-replacement strategies that seek functional cures rather than chronic management. Larimar pursues protein-replacement therapy that may complement upstream genetic fixes.

Strategic differentiation revolves around vector engineering, tissue tropism, and manufacturing yield. Companies invest in in-house AAV plants to sidestep contract-development backlogs. CRISPR-based players secure non-dilutive grants to explore one-time edits, although regulatory pathways are still in formation. Alliance models proliferate, such as Neurocrine co-developing Voyager’s asset to share cost and technical risk. Overall, the competitive arena favors firms with integrated R&D, process development, and commercial capabilities that can navigate the unique barriers of the Friedreich's ataxia therapeutics industry.

Friedreich's Ataxia Industry Leaders

-

Biogen

-

Lexeo Therapeutics

-

Minoryx Therapeutics

-

PTC Therapeutics

-

Retrotope

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Biogen initiated the BRAVE Phase 3 pediatric study evaluating omaveloxolone in children aged 2-<16 years, with a 52-week randomized period followed by an open-label extension.

- June 2025: The U.K. Medicines and Healthcare products Regulatory Agency approved omaveloxolone for patients aged 16 and older.

- February 2024: Larimar Therapeutics announced positive top-line Phase 2 data for nomlabofusp and plans a confirmatory trial ahead of a 2025 BLA submission.

Global Friedreich's Ataxia Market Report Scope

According to the scope of the report, Friedreich's ataxia is a hereditary neurodegenerative disorder characterized by progressive damage to the nervous system, leading to impaired coordination, muscle weakness, and difficulty walking. It is caused by mutations in the FXN gene, which results in reduced production of frataxin, a protein essential for mitochondrial function. Symptoms typically begin in childhood or adolescence and may include gait instability, speech problems, and cardiovascular issues. Currently, treatment mainly focuses on managing symptoms and improving quality of life.

The Friedreich's ataxia market is segmented by therapy type, which includes disease-modifying therapies, gene therapies, protein-replacement therapies, RNA-based therapies, and symptomatic therapies. Additionally, the market is segmented by drug class into antioxidant/Nrf2 activators, PPAR agonists, frataxin-gene vectors (AAV, lentiviral), mitochondrial stabilizers, and others. Furthermore, the segmentation by route of administration includes oral, intravenous, intrathecal, and subcutaneous routes of administration. The market is also segmented by age group into pediatric (<18 years), adult (18–40 years), and late-onset (>40 years). The segmentation by distribution channel includes hospital pharmacies, specialty pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Disease-modifying Therapies |

| Gene therapies |

| Protein-replacement Therapies |

| RNA-based Therapies |

| Symptomatic Therapies |

| Antioxidant/Nrf2 Activators |

| PPAR Agonists |

| Frataxin-gene Vectors (AAV, lentiviral) |

| Mitochondrial Stabilizers |

| Others |

| Oral |

| Intravenous |

| Intrathecal |

| Subcutaneous |

| Pediatric (<18 yrs) |

| Adult (18–40 yrs) |

| Late-onset (>40 yrs) |

| Hospital Pharmacies |

| Specialty Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Disease-modifying Therapies | |

| Gene therapies | ||

| Protein-replacement Therapies | ||

| RNA-based Therapies | ||

| Symptomatic Therapies | ||

| By Drug Class | Antioxidant/Nrf2 Activators | |

| PPAR Agonists | ||

| Frataxin-gene Vectors (AAV, lentiviral) | ||

| Mitochondrial Stabilizers | ||

| Others | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Intrathecal | ||

| Subcutaneous | ||

| By Age Group | Pediatric (<18 yrs) | |

| Adult (18–40 yrs) | ||

| Late-onset (>40 yrs) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Friedreich's ataxia market in 2030?

The market is forecast to reach USD 2.07 billion by 2030.

Which therapy segment is expanding fastest?

Gene therapies are expected to post an 11.23% CAGR between 2025 and 2030.

How dominant are antioxidant/Nrf2 activators today?

They held 88.56% of 2024 revenue, driven by omaveloxolone’s launch.

Why is Asia-Pacific the fastest-growing region?

Expanding patient registries, newborn screening, and rare-disease policies in China and Japan drive a 9.47% CAGR.

What challenges limit near-term gene-therapy supply?

Global shortages of viral-vector manufacturing capacity and raw materials constrain output.

Page last updated on: