Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

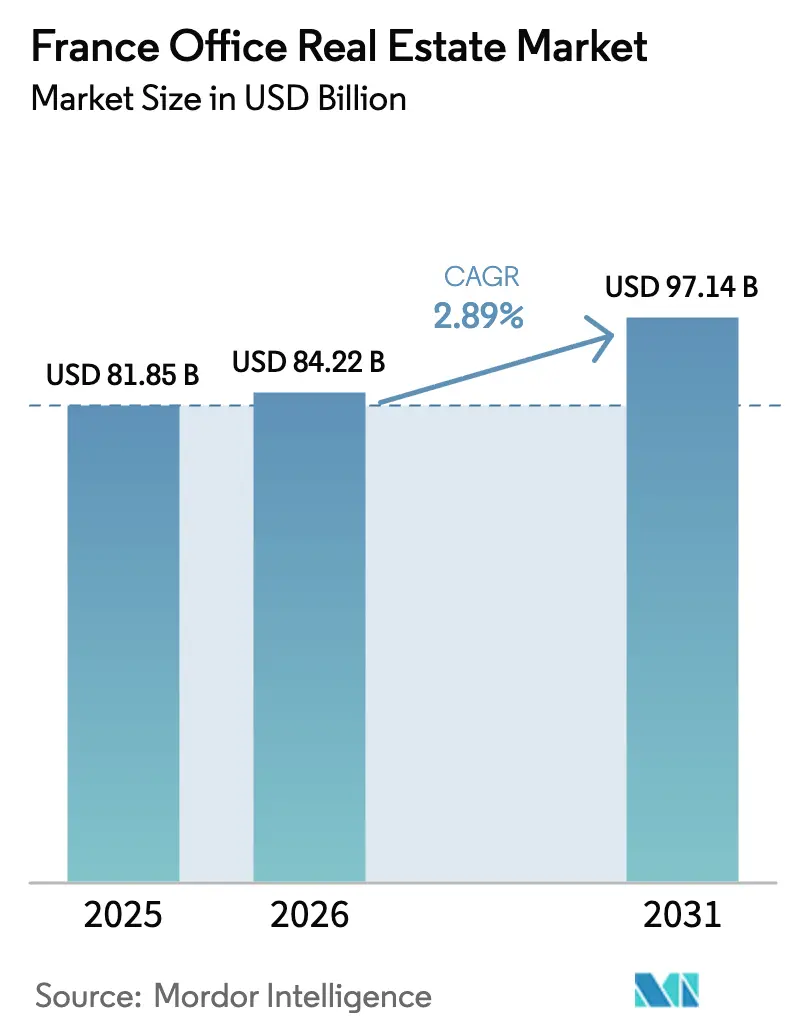

| Base Year Market Size (2025) | USD 81.85 Billion |

| Market Size (2026) | USD 84.22 Billion |

| Market Size (2031) | USD 97.14 Billion |

| Growth Rate (2026 - 2031) | 2.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Office Real Estate Market Analysis by Mordor Intelligence

France office real estate market size in 2026 is estimated at USD 84.22 billion, growing from 2025 value of USD 81.85 billion with 2031 projections showing USD 97.14 billion, growing at 2.89% CAGR over 2026-2031. The measured pace shows how landlords and investors are recalibrating portfolios for hybrid work, tighter energy-performance rules and a widening gap between prime and secondary assets. Flexible work patterns, the Paris 2024 legacy infrastructure spend of USD 550 million and rising capital allocations toward ESG-certified buildings are anchoring demand in core sub-markets. Institutional investors injected USD 3.74 billion in Q1 2025 alone as compressed yields in the Paris CBD fueled renewed confidence. A 50% surge in construction costs since 2019 supports rental growth for in-place Grade A stock but restricts new supply, while AI-powered space-optimization tools are reshaping tenant requirements and elevating retrofit economics. Leasing remains dominant, yet faster growth in direct acquisitions signals an ownership pivot toward buildings that already satisfy EU taxonomy thresholds.

Key Report Takeaways

- By building grade, Grade A offices captured 50.68% of the France office real estate market share in 2025; Grade B/C combined is forecast to grow at a 3.31% CAGR through 2031.

- By transaction type, rental agreements held 74.66% of 2025 activity, while sales transactions are projected to advance at a 3.39% CAGR to 2031.

- By end use, the Information Technology segment commanded 26.74% share of the France office real estate market size in 2025 and is projected to expand at 3.58% CAGR through 2031.

- By city, Paris retained 73.65% share of the France office real estate market size in 2025; Lyon is the fastest-growing locality at a 3.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible and hybrid workspace demand | +0.8% | Nationwide; highest in Paris, Lyon, Marseille | Medium term (2-4 years) |

| Corporate ESG and green-leasing mandates | +0.6% | Strongest in Île-de-France and business districts | Long term (≥ 4 years) |

| Paris 2024 Olympic legacy refurbishments | +0.4% | Île-de-France with spillover to connected metro areas | Short term (≤ 2 years) |

| AI-enabled space-optimization analytics | +0.3% | Major tech hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Flexible & Hybrid Workspace Demand

Hybrid work is firmly embedded across corporate France as 87% of employers now require partial in-office attendance, with employees clocking 3.5 days per week on-site.[1]Institut National de la Statistique et des Études Économiques (INSEE), “Télétravail et présentiel : le travail hybride, une pratique désormais ancrée dans les entreprises,” insee.fr The preference for collaborative, technology-ready environments has already driven 42% of total floor space refurbishments toward flexible layouts. Prime CBD buildings therefore record declining vacancy even as peripheral stock exceeds 10%. Lease renegotiations favor shorter terms and built-in expansion clauses that match fluid staffing levels. Portfolio consolidation is accelerating, funneling capital expenditure into fewer yet higher-quality assets. The resulting bifurcation underscores why the France office real estate market continues to polarize around energy-efficient Grade A towers located near multimodal transport.

Heightened Corporate ESG & Green-Leasing Mandates

The EU taxonomy and France’s Décret Tertiaire require a 40% energy-consumption cut by 2030, pressuring landlords to decarbonize assets or accept a “brown discount”. Certified buildings already command rent premiums and enjoy lower vacancy, while lenders increasingly restrict financing for non-compliant stock. Fifty-seven percent of occupiers target net-zero footprints by 2030, channeling capex toward photovoltaic retrofits and smart-metering solutions. The regulatory push has created a refurbishment boom, with specialized contractors and PropTech vendors capitalizing on demand. Early-mover owners that attain green labels are locking in blue-chip tenants at higher headline rents, reinforcing a “flight to green” dynamic inside the France office real estate market.

Paris 2024 Olympic Legacy Boosting Grade-A Refurbishments

The Games acted as a catalyst for USD 550 million of transport and urban upgrades.[2]Choose Paris Region, “Redefining the Future, the Paris 2024 Legacy,” chooseparisregion.org The Grand Paris Express has added new stations that extend the CBD footprint into Seine-Saint-Denis, prompting landlords to reposition older buildings as Grade A inventory. Reduced commute times broaden tenant catchments, while global visibility from the Olympics pulled fresh foreign capital into French real assets. Development pipelines that were paused during the pandemic have resumed, targeting delivery dates aligned with new metro line openings. Short-term momentum continues to benefit refurbishment specialists able to pivot assets quickly toward prime sustainability ratings.

AI-Enabled Space-Optimization & Utilization Analytics

Nine in ten large companies plan to embed AI tools for workplace management within five years. Investments range from real-time desk-occupancy sensors to predictive maintenance engines that lower operating costs. France’s PropTech ecosystem attracted sizable funding in 2024, with firms such as Accenta delivering decarbonization platforms that integrate IAQ monitoring and energy controls. Early adopters report measurable operating-expense savings, justifying rent premiums while supporting tenants’ ESG disclosures. Data-security and interoperability concerns remain, yet pilot successes are convincing more institutional owners to deploy building-operating systems across portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remote-work headcount dilution | -0.7% | Nationwide; deepest in peripheral sub-markets | Long term (≥ 4 years) |

| Elevated construction and financing costs | -0.5% | Nationwide; severe for speculative projects | Medium term (2-4 years) |

| Stricter capital-allocation hurdles | -0.3% | Legacy stock in all regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prolonged Remote-Work Headcount Dilution

Telework participation stabilizes at 22% of the French workforce and averages 1.9 days at home weekly. Peripheral sub-markets therefore register rising vacancy as occupiers downsize legacy footprints. Finance and ICT sectors post telework penetration of 75% and 60% respectively, amplifying space surrender in La Défense and western suburbs. Landlords are reassessing conversion prospects—turning obsolete floorplates into residential or mixed-use schemes—to mitigate unleased inventory. Over the long term, the France office real estate market must reconcile lower per-employee area ratios with persistent preference for prime, well-amenitized hubs.

Elevated Construction & Financing Costs Amid Inflation

The construction industry continues to face significant challenges as inflationary pressures persist. Input prices jumped 50% from 2019, while the Construction PMI sat at 43.8 in March 2025, signalling contraction Savills Construction Briefing. Higher interest rates drive lenders to demand greater pre-leasing, elongating project timelines and raising required returns. Speculative ground-up projects outside Paris CBD struggle to pencil out, reinforcing scarcity of Grade A supply. Developers with strong balance sheets and ESG-ready pipelines retain bargaining power with both tenants and financiers, but smaller players face exit or recapitalization. As the market evolves, stakeholders must adapt to these shifting dynamics to navigate the road ahead successfully.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Assets Drive Market Polarization

Grade A premises held 50.68% France office real estate market share in 2025. Tenants value energy efficiency and wellness features that facilitate hybrid protocols, supporting a 3.05% CAGR for this cohort through 2031. Grade B and Grade C face accelerated depreciation unless refurbished; many owners evaluate conversions to residential or life-science laboratories where zoning allows. Paris CBD Grade A asking rents hit USD 1,320 per square meter in 2024, up 12% year-on-year, whereas suburban Grade C stock sees double-digit vacancy. Leasing spreads illustrate the growing bifurcation inside the France office real estate market.

Hybrid work magnifies this divide because firms require fewer desks yet demand richer amenities—from acoustically treated collaboration zones to smart-building dashboards that track carbon emissions. Developers of new towers integrate photovoltaic façades, low-carbon concrete and AI-driven HVAC, surpassing Décret Tertiaire thresholds years ahead of schedule. Retrofits also accelerate: Gecina earmarked USD 915 million for deep-energy upgrades, betting on the incoming “green premium.” The trend implies ongoing capital flows into Grade A pipelines even as secondary stock flirts with obsolescence, reinforcing quality polarization throughout the France office real estate market.

By Transaction Type: Sales Growth Outpaces Rental Dominance

Rental contracts accounted for 74.66% of 2025 activity, reflecting occupiers’ desire for operational flexibility. Nevertheless, sales deals are forecast to climb 3.39% annually, faster than the overall France office real estate market. The USD 1.07 billion purchase of the Majunga Tower by Unibail-Rodamco-Westfield typifies renewed appetite for trophy assets, Batinfo. Prime yields compressed from 4.5% to 4.0% in Paris CBD during 2024-2025, enticing pension funds and sovereign entities.

Leases themselves evolve: average term now sits at 6.4 years versus 9 years pre-pandemic, with frequent break options. Portfolio-sale structures allow investors to absorb inventory requiring phased retrofits, capturing upside once energy targets are met. Meanwhile, cross-border investors from North America tripled allocations to France in 2024, and many are scouting JV structures to navigate local regulations. The France office real estate market, therefore, observes a dual mechanism: leasing remains volume leader, yet equity inflows tilt toward direct ownership of green assets with solid rent reversion potential.

By End Use: Technology Sector Leadership Drives Innovation Adoption

Information Technology firms held 26.74% France office real estate market share in 2025 and topped the growth league at 3.58% CAGR to 2031. AI start-ups and cloud providers favor flexible floorplates wired with 5G and a redundant fiber backbone, often clustered around Paris Station F or Lyon Part-Dieu. Banks follow, yet they rationalize branch networks, shifting headquarters into fewer, high-spec floors to reinforce employer branding. Consulting and professional services occupy premium CBD suites to maintain client proximity; their footprint stabilizes as hybrid staffing optimizes desk ratios.

Tech occupiers integrate IoT sensors that track energy and occupancy, feeding corporate ESG dashboards. J.P. Morgan’s lease of CBRE IM’s Marché Saint-Honoré underscores demand for brand-defining addresses in the capital’s historic core. Life-science corporates in Marseille’s Euroméditerranée district need floor-loading and lab ventilation, nudging landlords to re-engineer existing assets. Across categories, the unifying theme is digital enablement: any building lacking robust connectivity risks prolonged vacancy, highlighting why technology leadership propels overall absorption in the France office real estate market.

Geography Analysis

Paris continues to command 73.65% of the 2025 transaction value, backed by its concentration of global headquarters and government agencies. Take-up in Central Paris reached 388,000 square meters in Q1 2025, even though total deals slipped 6% year on year; CBD sub-markets alone saw a 13% bounce, proving the appeal of core micro-locations. Supply is constrained by landmark preservation and lengthy permitting, which upholds rent inflation yet limits headline volume growth. Prime net effective rents have outpaced wage inflation, sparking corporate interest in alternative hubs.

Lyon records the quickest growth trajectory at 3.76% CAGR to 2031. Annual office take-up is forecast to surpass 320,000 square meters as companies capitalize on lower occupancy costs and a vibrant innovation ecosystem clustered in the Part-Dieu and Confluence districts. Vacancy at 5.6% signals balanced conditions, and municipal authorities incentivize green refurbishments via tax rebates, strengthening the investment thesis for value-add strategies.

Marseille, together with smaller regional cities, forms an emerging set of opportunities aligned with government decentralization policy. Programs under Provence Promotion highlight improved international schools and digital hubs that appeal to expatriate staff. France Stratégie observes that telework increases demand for well-amenitized urban nodes, implying steady if modest office absorption in secondary municipalities.Investors, however, assess each locale for transport connectivity and sector specialization before committing capital.

Competitive Landscape

The France office real estate market is moderately concentrated. Competition centers on a cluster of dominant REITs that control most CBD towers, while new foreign entrants chase ESG-qualified assets. Gecina’s USD 19.14 billion portfolio is 87% Paris-centric and 97% green-certified, delivering a 5.4-year average lease maturity. Covivio allocates USD 26.4 billion across Europe, yet channels two-thirds of new capex into Paris offices, where it booked 176,200 square meters of leasing in 2024. Icade concentrates on future-proofing Seine-Saint-Denis inventory, recently re-letting the 29,000 square-meter Pulse building to the Departmental Council.

International capital is intensifying the rivalry. North American investors raised allocations to USD 3.4 billion in 2024, lured by Eurozone stability and green-premium upside. Joint-venture structures such as PGIM Real Estate with Pithos Capital target alternative niches like self-storage, signaling diversification beyond offices. PropTech disruptors provide data-driven leasing platforms and net-zero retrofitting solutions, creating service partnerships with incumbent landlords rather than outright displacement.

Strategic moves increasingly focus on refurbishment excellence rather than land-bank accumulation. Covivio’s USD 1.1 billion annual investment pipeline is skewed to deep-energy retrofits, while Gecina rotates out of mature residential units to fund student-housing and co-living projects that enhance overall portfolio agility. Asset managers embed AI-enabled building-management systems to quantify carbon savings and pass these metrics through to occupiers’ reporting obligations. Competitive advantage thus hinges on the ability to blend technology, sustainability, and tenant-experience services efficiently within the France office real estate market.

France Office Real Estate Industry Leaders

Jones Lang LaSalle IP, Inc.

Knight Frank

CBRE

BNP Paribas Real Estate

Cushman & Wakefield

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CBRE Investment Management completed the leasing of the iconic Marché Saint-Honoré office building in Paris to J.P. Morgan, underscoring appetite for prestige CBD addresses.

- April 2025: Icade recorded USD 358.6 million in Q1 revenue, signing or renewing nearly 50,000 square meters of leases and fully re-letting the Pulse building to the Seine-Saint-Denis Departmental Council.

- March 2025: European Commission approved EUR 700 million aid scheme for Spain to enhance large-scale electricity storage, supporting integration of renewable energy and potentially adding 2.5 to 3.5 gigawatts of new storage capacity by 2029.

- February 2025: Covivio announced a 10% rise in recurring earnings for 2024 after investing USD 1.21 billion, with Paris CBD rents reaching USD 1,320 per square meter.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts the entire stock of purpose-built office buildings throughout metropolitan France whose primary use is the leasing or sale of workspace to corporate and institutional occupiers, whether in single-tenant towers or multi-tenant blocks. Values are expressed in constant 2024 US dollars and reflect the aggregated capital worth of stabilized assets, not the flow of yearly investment.

Scope exclusion: serviced coworking centers housed inside retail or hospitality premises and facility-management revenues are kept outside the sizing base.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifesciences, Energy, Legal)

- By City

- Paris

- Lyon

- Marseille

- Rest of France

Detailed Research Methodology and Data Validation

Primary Research

We interviewed brokers, asset managers, financing banks, large occupiers in tech and BFSI, as well as municipal permitting officials across Ile-de-France, Auvergne-Rhone-Alpes, and PACA. Their inputs refined vacancy thresholds, effective rents, and post-COVID space utilization ratios, allowing us to tighten model assumptions that were only partly visible in desk research.

Desk Research

Our analysts began with national data repositories such as INSEE's building completions archive, Banque de France's real-estate financing dashboards, and DGFiP's notarized transactions file. Sector context was enriched through Issue Papers from the French Institute of Real Estate Management, green-lease guidelines released by ADEME, and quarterly vacancy maps published by ImmoStat. Company filings and investor decks from listed landlords supplied rent rolls and disposal prices, while paid access to D&B Hoovers contributed firm-level asset book values. These structured datasets let us sketch supply pipelines, capital flows, and replacement costs across Paris, Lyon, Marseille, and secondary cities.

Press releases, planning approvals, and tender logs (via Tenders Info) then helped validate pipeline timing and refurbishment scale. The sources named are illustrative; many additional public and subscription materials were consulted for cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down build began with INSEE's inventory of existing office floor area, multiplied by typical transaction values to reconstruct the 2024 capital stock, which is then trended with new deliveries, demolitions, and price movement indices. Bottom-up signals, sampled landlord portfolios, channel checks on Grade-A asking rents, and average deal sizes served as guardrails to adjust regional totals. Key levers include GDP growth, prime yield compression, net absorption, refurbishment share, remote-work adoption rates, and ESG retrofit premiums. Five-year projections employ a multivariate regression that links capital values to GDP, employment in services, and vacancy swings, before scenario analysis overlays account for interest-rate paths. Where landlord roll-ups were incomplete, we imputed values using median EUR / m2 benchmarks from tax data.

Data Validation & Update Cycle

Outputs pass through variance screens versus ImmoStat vacancy, MSCI capital-value indices, and BNP Paribas rent trackers; anomalies trigger model reruns and senior-analyst sign-off. The France study refreshes annually, with interim revisions when macro shocks or major policy shifts occur, and every fresh copy is quality-checked again just prior to client delivery.

Why Mordor's France Office Real Estate Baseline Commands Confidence

Published numbers often diverge because some firms report yearly investment flow, others price only Grade-A CBD floorspace, and refresh cadences differ.

Key gap drivers include differing inclusion of owner-occupied stock, use of euro-area yield assumptions versus France-specific yields, and whether refurbishments are treated as new supply.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 81.85 B (2025) | Mordor Intelligence | - |

| USD 28 B (2024) | Regional Consultancy A | counts leased stock only, omits owner-occupied and provincial assets |

| EUR 4.9 B (2024) | Trade Journal B | reports annual investment volume, not total capital stock |

The comparison shows that when scope and valuation basis differ, estimates swing widely. By anchoring on the full asset base, documenting each adjustment, and refreshing every year, Mordor Intelligence gives decision-makers a transparent, repeatable baseline they can benchmark with confidence.

Key Questions Answered in the Report

What is the current size of the France office real estate market?

The France office real estate market size reached USD 84.22 billion in 2026 and is projected to climb to USD 97.14 billion by 2031.

How fast will the market grow between 2026 and 2031?

It is expected to expand at a 2.89% compound annual growth rate, driven by hybrid-work adaptation and ESG retrofits.

Which building grade captures the largest share?

Grade A properties hold 50.68% of 2025 value and are favored for their energy performance and central locations.

Why is Lyon considered the fastest-growing city for offices?

Lyon benefits from 25-30% lower occupancy costs than Paris, robust infrastructure upgrades and a forecast 3.76% CAGR through 2031.

How are ESG regulations impacting asset values?

EU taxonomy and Décret Tertiaire rules create a “green premium” for compliant buildings and a “brown discount” for inefficient stock, reshaping capital allocation.

What risks could dampen future growth?

Prolonged remote-work trends, 50% construction-cost inflation since 2019 and tight financing conditions may restrain new supply and transaction velocity within the France office real estate market.

Page last updated on: