Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

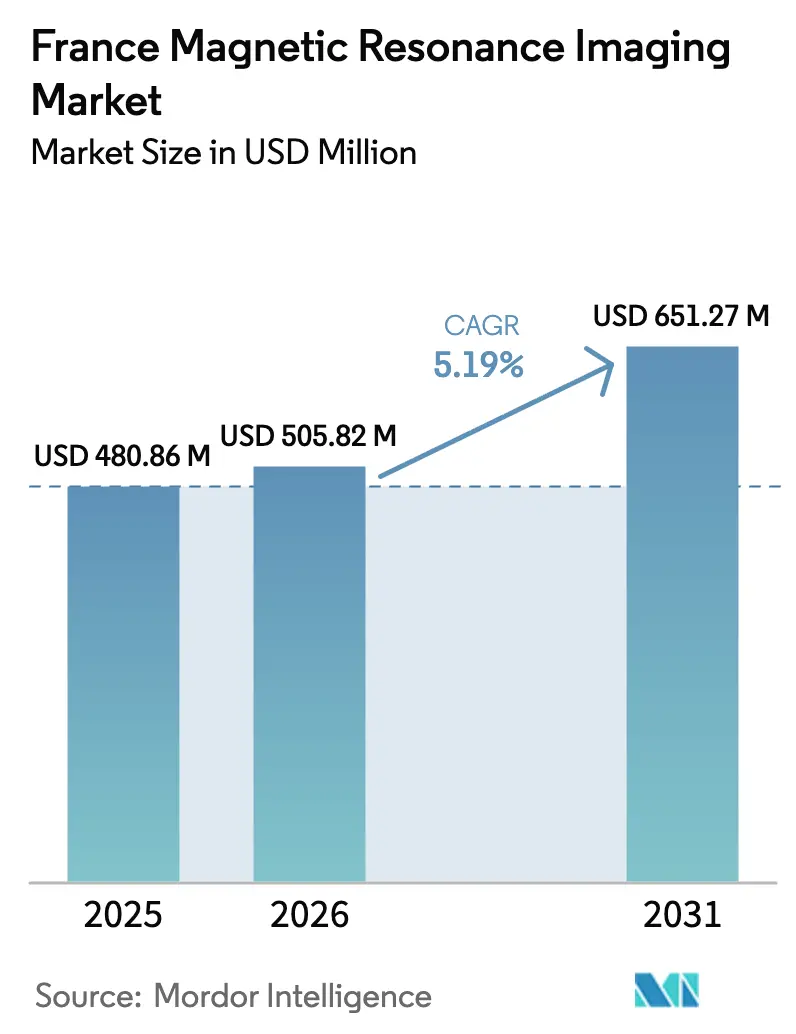

| Base Year Market Size (2025) | USD 480.86 Million |

| Market Size (2026) | USD 505.82 Million |

| Market Size (2031) | USD 651.27 Million |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

The France magnetic resonance imaging market size is expected to grow from USD 480.86 million in 2025 to USD 505.82 million in 2026 and is forecast to reach USD 651.27 million by 2031 at 5.19% CAGR over 2026-2031. This sustained rise reflects the country’s national commitment to upgrade its installed base of 1,312 scanners, leverage EUR 95 million (USD 104.5 million) in France 2030 imaging funding, and accelerate AI integration in clinical workflows. Rapid deployment of virtually helium-free systems, local production of MRI units at GE’s Buc site, and reforms that mandate outpatient capacity are reshaping procurement cycles and service delivery models. Vendor financing programs, private-equity consolidation of radiology groups, and a robust pipeline of ultra-high-field research platforms further reinforce the growth trajectory of the France magnetic resonance imaging market. Replacement demand is accelerating because France is one of only four European nations now meeting COCIR’s golden-rule age profile, which specifies that at least 60% of scanners be under five years old.

Key Report Takeaways

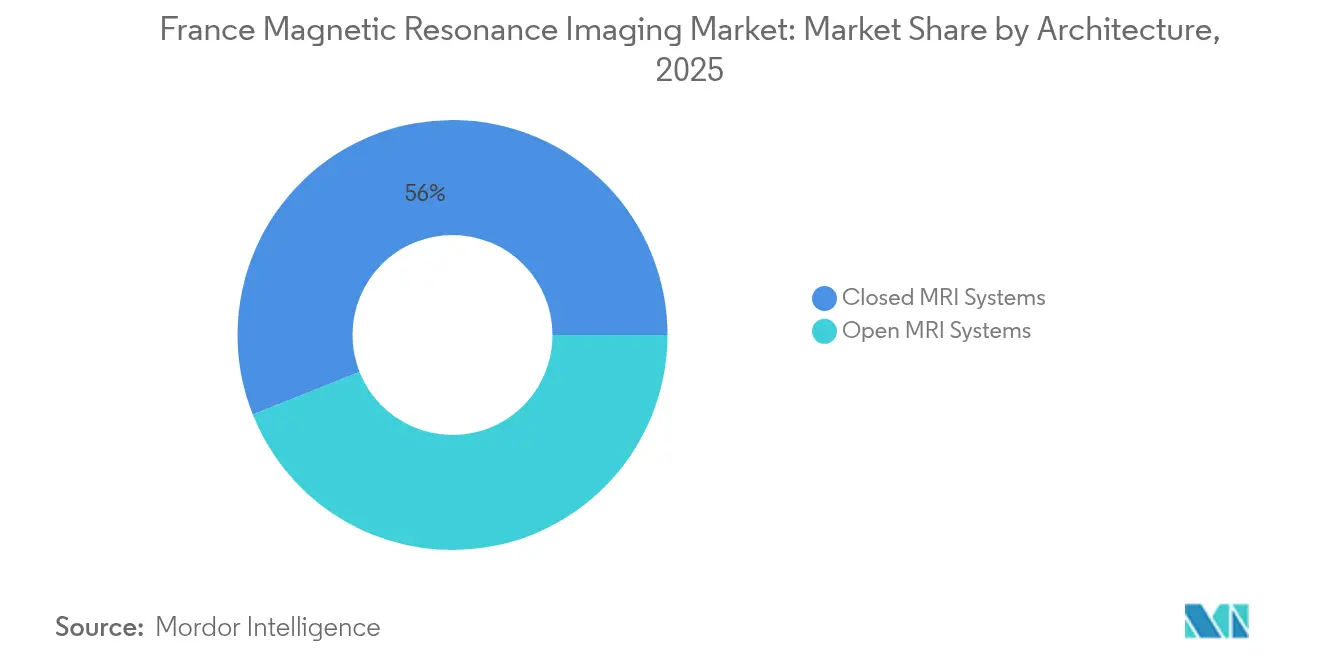

- By architecture, closed systems led with 56.03% France magnetic resonance imaging market share in 2025. Open systems are projected to record the fastest 7.39% CAGR through 2031.

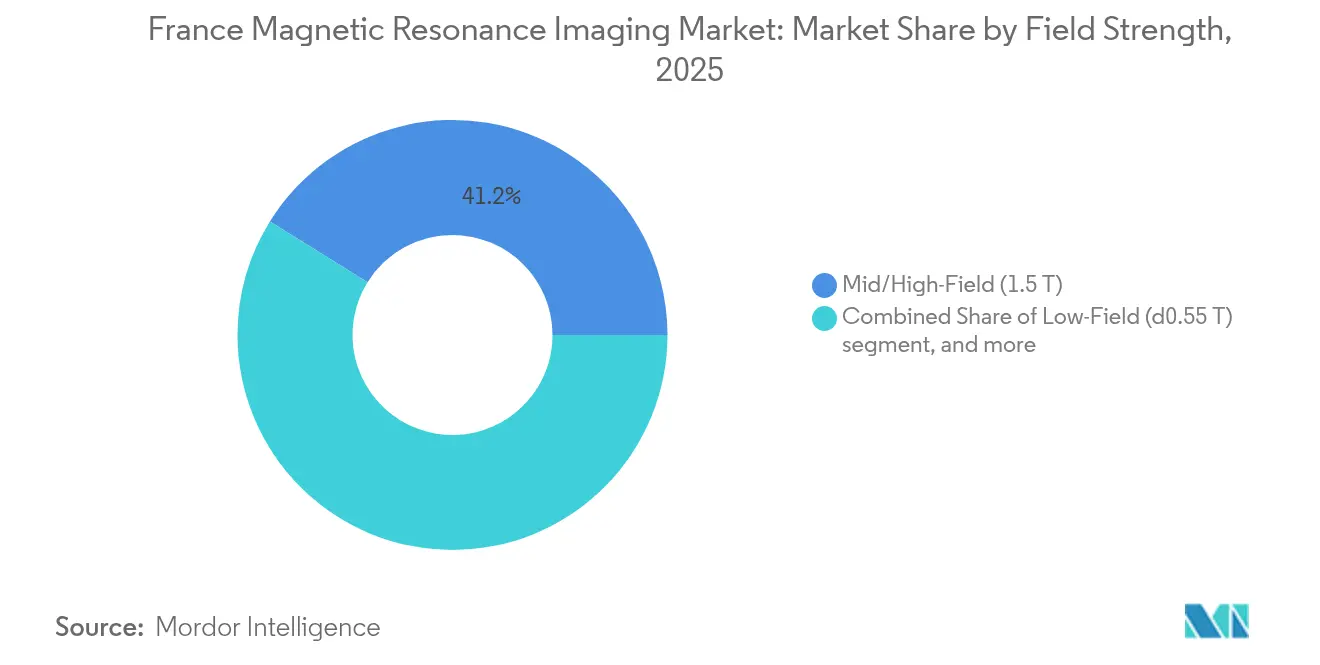

- By field strength, mid/high-field 1.5 T units accounted for 41.15% of the France magnetic resonance imaging market size in 2025. Low-field systems (≤0.55 T) are forecast to advance at a 6.69% CAGR between 2026-2031.

- By application, neurology captured 30.29% of the France magnetic resonance imaging market in 2025. Cardiology is poised for the highest 6.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Magnetic Resonance Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in cancer & neuro-degenerative disease burden | +1.2% | Nationwide, aging regions | Long term (≥ 4 years) |

| Growing adoption of 3 T scanners in French university hospitals | +0.8% | CHU networks, major metros | Medium term (2-4 years) |

| National AI-for-imaging strategy under “France 2030” funding | +1.0% | Île-de-France & Rhône-Alpes R&D hubs | Medium term (2-4 years) |

| Expansion of outpatient MRI capacity via 2024 social-security reforms | +0.9% | Underserved territories | Short term (≤ 2 years) |

| Vendor financing programs for private clinics | +0.7% | Regional private sector | Short term (≤ 2 years) |

| Aging installed base reaching end-of-life triggers replacement wave | +1.1% | Nationwide, scanners > 10 years | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Cancer & Neuro-Degenerative Burden

France’s aging population is escalating clinical demand for high-resolution neurological and oncological imaging. Expanded national screening protocols now rely on MRI for early tumor detection and disease staging. The Iseult 11.7 T platform at CEA produced first-in-human brain scans in 2024, demonstrating sub-millimeter resolution that improves hippocampal atrophy measurement and iron mapping for Parkinson’s diagnostics[1]DSIH, “Iseult 11.7 T delivers first human brain images,” dsih.fr. University hospitals are therefore scaling MRI slots dedicated to neuro-oncology pathways, integrating diffusion and perfusion sequences that shorten diagnostic timelines. Steady gains in five-year cancer survival rates further elevate longitudinal monitoring volumes. Together, these demographic and clinical pressures intensify scanner utilization and accelerate replacement demand across the France magnetic resonance imaging market.

Growing Adoption of 3 T Scanners in University Hospitals

Academic centers including CHU Reims and CHU Nancy are moving from 1.5 T to 3 T platforms to unlock advanced research protocols. Higher field strength improves signal-to-noise ratios, enabling functional MRI, diffusion tensor imaging, and proton spectroscopy that previously required referral to national research facilities[2]CHU Nancy, “Installation du nouvel IRM 3 T,” chu-nancy.fr. France 2030 funds earmark capital for this upgrade cycle, while vendor value partnerships bundle equipment, training, and life-cycle servicing to offset upfront costs. Early adopters report sharper vascular delineation in stroke work-ups and reduced slice thickness in musculoskeletal exams, reinforcing the clinical case for 3 T migration. The resulting rise in high-complexity exams widens reimbursement differentials between university hospitals and private clinics, adding momentum to the France magnetic resonance imaging market expansion.

National AI-for-Imaging Strategy Under France 2030 Funding

Public grants are fueling French AI start-ups that automate image reconstruction, lesion detection, and workflow triage. The ImaSpiiR-X consortium secured EUR 18.2 million (USD 20.0 million) to commercialize spectral MRI advances, while Gleamer’s 2025 acquisition of Pixyl and Caerus Medical brings CE-marked neuroinflammatory and lumbar spine algorithms into clinical practice. Philips’ SmartSpeed software, compatible with 97% of sequences, delivers up to 3× faster scans and 65% higher spatial resolution on existing scanners, expanding throughput without new hardware. These innovations speed reporting, cut repeat exams, and free scarce radiologist capacity, directly influencing capital planning at hospital and clinic level.

Expansion of Outpatient MRI Capacity Via 2024 Reforms

Social-security legislation effective January 2024 prescribes new authorizations for ambulatory imaging sites to curb hospital backlog. Streamlined approvals reduced median licensing time from 12 to 6 months according to the Ministry of Health, triggering bids for mobile trailers and modular suites serving medical deserts in the North and Center-West. Networks such as IMADIS Groupe operate 24/7 teleradiology hubs that interpret scans from 300 partner establishments, reinforcing rural deployment feasibility. Accelerated outpatient penetration spreads scan volumes, sustaining the France magnetic resonance imaging market even as procedure tariffs undergo annual downward pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capped public-hospital budgets & DRG-linked tariffs | −0.8% | Nationwide public sector | Long term (≥ 4 years) |

| Lengthy ANSM approval cycle for novel field strengths | −0.4% | National, innovation hubs | Medium term (2-4 years) |

| Persistent shortage of MRI technologists in regional France | −0.5% | Regional & rural areas | Short term (≤ 2 years) |

| High procurement cost vs. CT & ultrasound alternatives | −0.6% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capped Public-Hospital Budgets & DRG-Linked Tariffs

Public facilities spend only 5% of operating income on capital investment, down from 10% in 2009, limiting MRI fleet renewal. The EUR 1.3 billion technical forfait allotted to MRI exams faces annual cost-containment reviews by Assurance Maladie, squeezing per-scan reimbursement. Hospital CFOs therefore delay purchases or pivot to vendor-financed value partnerships, lengthening procurement cycles. Competitive tension rises because private clinics can recover costs faster under fee-for-service models, siphoning complex cases. These structural funding barriers dampen large volume orders, tempering the France magnetic resonance imaging market CAGR despite robust clinical demand.

Lengthy ANSM Approval Cycle for Novel Field Strengths

Ultra-high-field MRI systems undergo 18-month safety dossiers at ANSM before first-in-patient use. The Iseult 11.7 T project required staged volunteer protocols and granular electromagnetic modeling to satisfy regulator thresholds[3]DSIH, “ANSM validation process for ultra-high-field MRI,” dsih.fr. Vendors must produce additional biocompatibility data, elevating launch costs and pushing break-even horizons. AI-driven image-post-processing apps also navigate a Class IIb MDR pathway, stretching go-to-market timetables. These prolonged approvals defer revenue from novel platforms and moderate the pace of technology turnover within the France magnetic resonance imaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Diagnostic Precision Sustains Closed-System Leadership

Closed scanners anchored 56.03% of the France magnetic resonance imaging market in 2025 thanks to superior homogeneity and high channel coils that satisfy neurology, oncology, and musculoskeletal protocols. Closed units now incorporate BlueSeal and DryCool helium-free designs, which reduce energy consumption and help mitigate global helium shortages. These sustainability gains influence hospital tenders, which score equipment based on carbon criteria. Open platforms remain niche but gather momentum with a 7.39% CAGR because patient comfort improves completion rates among claustrophobic and pediatric cohorts. Outpatient centers in Provence and Brittany advertise panoramic 0.4 T systems as a differentiator, capturing referrals from general practitioners. The France magnetic resonance imaging market size for open architecture will therefore expand while coexistence persists, reflecting complementary—not substitutive—clinical use-cases.

Second-generation open units deploy AI-based reconstruction that compensates for lower field strength, closing the quality gap with closed systems. Portable intraoperative models further extend open design into hybrid operating rooms, adding functional values rather than siphoning demand from mainstream diagnostic suites. Closed scanners, however, retain the premium tier of France magnetic resonance imaging market share because they support 3 T upgrades, spectroscopy adjuncts, and parallel transmit coils essential for clinical research trials.

By Field Strength: Mid-Field Dominance Meets Low-Field Innovation

Mid/high-field 1.5 T platforms command 41.15% France magnetic resonance imaging market share, offering a balance of cost, throughput, and reimbursements aligned with routine neurology and abdominal imaging. Investment priority remains on refurbishing these workhorses with AI acceleration packages and dual-energy coils, extending asset life and lowering per-exam consumables. Very-high-field 3 T adoption pushes ahead in 15 university hospitals, supporting advanced connectome mapping and tractography studies tied to EU Horizon grants.

Low-field technology is the fastest riser, clocking a 6.69% CAGR, because 0.55 T mobile trailers and hyper-portable 0.05 T bedside units enter emergency workflows. Proof-of-concept deployments in rural Normandy enable stroke triage without patient transfer, meeting reform targets for distance imaging access. Service contracts guarantee remote calibration, mitigating historical maintenance hesitancy among small clinics. Over the forecast horizon, low-field share growth widens the overall France magnetic resonance imaging market size by unlocking new service sites rather than cannibalizing hospital volumes.

By Application: neurology retains lead while cardiology accelerates

Neurology held 30.29% of examinations in 2025, benefiting from structured Alzheimer’s screening pathways that reimburse volumetric hippocampal assessment. High adoption of diffusion tensor and multi-band functional protocols drives repeat scanning and research partnerships with AI start-ups that label white-matter lesions. Oncology remains second, but mix shifts toward whole-body diffusion imaging for metastatic surveillance, shortening CT dependency in treatment cycles. Musculoskeletal exams ride the wave of sports medicine demand, especially in the lead-up to the 2026 Winter Olympics bid, which bolsters private imaging-center footfall.

Cardiology grows fastest at 6.34% CAGR because compressed-sense sequences reduce breath-hold requirements, making MRI accessible for heart-failure patients previously sent to CT. French academic societies now endorse MRI as first-line for arrhythmogenic right ventricular cardiomyopathy, spurring scan referrals. Hepatology units adopt liver-fat quantification protocols, showcasing MRI’s expanding abdominal footprint. Collectively, this diversified application suite sustains rising throughput and strengthens the revenue base of the France magnetic resonance imaging market.

Competitive Landscape

Global manufacturers establish their market presence through integrated offerings that combine hardware, AI, and financing. Siemens Healthineers leads through long-horizon value partnerships, securing life-cycle services that ensure uptime and facilitate research collaboration. GE HealthCare’s Buc manufacturing line, inaugurated in 2024, yields an 84% lower delivery carbon footprint to EU buyers and supports agile configuration for site-specific shielding constraints. Koninklijke Philips N.V. scales BlueSeal helium-free magnets and SmartSpeed AI, positioning sustainability and speed as procurement differentiators. Collectively, these three suppliers captured approximately 64% of the French magnetic resonance imaging market share in 2024.

Tier-two vendors pursue niche strategies. Canon Medical advances rapid-sequence cardiac protocols on 1.5T Vantage Orian units, appealing to private clinics seeking cardiology growth. Esaote promotes open 0.4 T systems for veterinary and extremity imaging, tapping non-hospital budgets. Start-ups such as Hyperfine eye CE approval for 0.064 T portable systems, yet long ANSM review cycles defer revenue realization.

AI firms shape competitive parameters. Gleamer’s acquisitions assemble an MRI-centric toolbox that bundles neuro and spine triage algorithms into a single SaaS license. French firm Incepto curates a marketplace of FDA-cleared apps, embedding these in PACS workflows and sharing subscription income with radiology groups. Service differentiators therefore pivot from pure magnet specifications to total-cost-of-ownership propositions, reinforcing integrated model dominance.

France Magnetic Resonance Imaging Industry Leaders

GE Healthcare

Koninklijke Philips NV

Esaote SpA

Canon (Canon Medical Systems Corporation)

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ImaSpiiR-X consortium awarded EUR 18.2 million France 2030 grant for planar spectral MRI technology

- December 2024: AP-HP signed its first Siemens-Healthineers framework accord to co-develop systemic imaging solutions for chronic diseases.

- October 2024: Siemens Healthineers and CHU Nantes agreed a EUR 55 million, 12-year Value Partnership for six helium-free scanners and research staff.

France Magnetic Resonance Imaging Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique that is used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body. The France magnetic resonance imaging market is segmented by architecture (closed MRI systems and open MRI systems), field strength (low-field MRI systems, high-field MRI systems, very high-field MRI systems, and ultra-high MRI systems), application (oncology, neurology, cardiology, gastroenterology, musculoskeletal, and other applications). The report offers the value (in USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) |

| Very-High-Field (3 T) |

| Ultra-High-Field (7 T +) |

By Application

| Neurology |

| Oncology |

| Musculoskeletal |

| Cardiology |

| Gastroenterology |

| Other Applications |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) | |

| Very-High-Field (3 T) | |

| Ultra-High-Field (7 T +) | |

| By Application | Neurology |

| Oncology | |

| Musculoskeletal | |

| Cardiology | |

| Gastroenterology | |

| Other Applications |

Key Questions Answered in the Report

How large is the French MRI sector in 2026?

It is valued at USD 505.82 million and is forecast to climb to USD 651.27 million by 2031.

What growth rate is expected for MRI equipment demand in France through 2031?

The segment is projected to expand at a 5.19% CAGR over the 2026-2031 period.

Which clinical use accounts for the highest number of MRI scans in France?

Neurology leads with 30.29% of examinations, driven by nationwide neuro-degenerative screening programs.

Why are low-field portable MRI systems gaining traction across France?

²0.55 T units enable point-of-care imaging in rural areas, meeting reform goals to reduce geographic access gaps while lowering installation costs.

How do 2024 social-security reforms affect outpatient MRI capacity?

Streamlined licensing and funding incentives are fueling new ambulatory imaging centers, easing hospital backlogs and improving appointment times.

Which suppliers hold the largest share of French MRI equipment sales?

Siemens Healthineers, GE HealthCare, and Philips together account for roughly 64% of national scanner installations.

Page last updated on: