France Electric Commercial Vehicle Battery Pack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

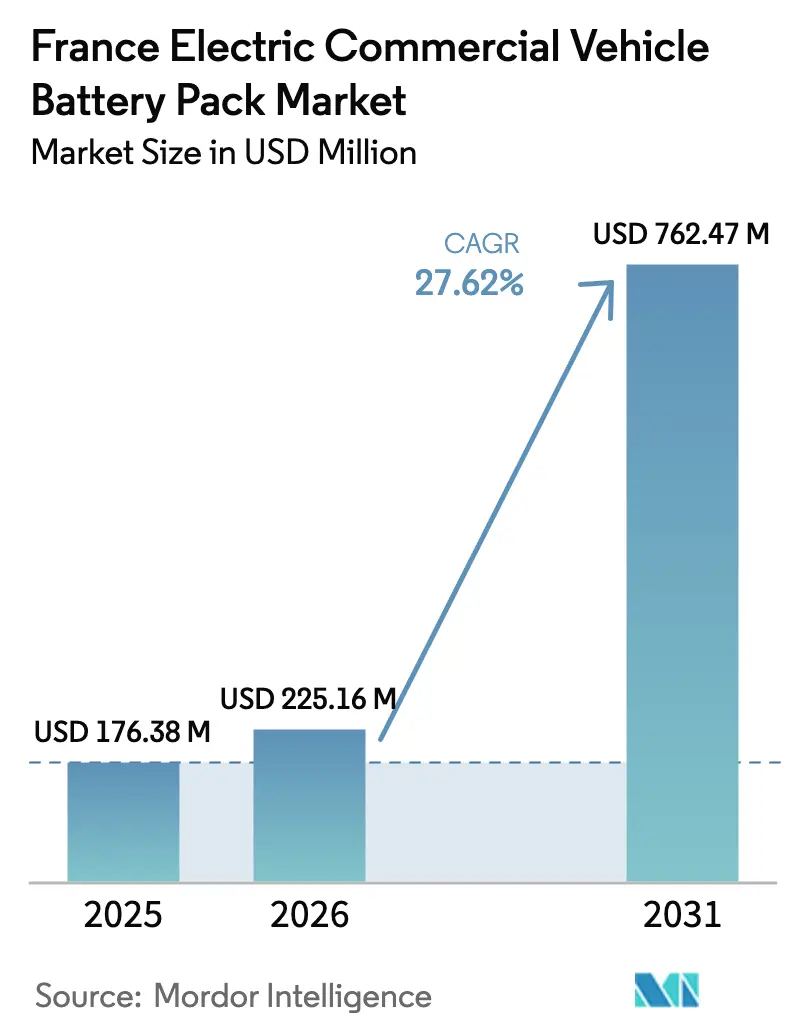

| Base Year Market Size (2025) | USD 176.38 Million |

| Market Size (2026) | USD 225.16 Million |

| Market Size (2031) | USD 762.47 Million |

| Growth Rate (2026 - 2031) | 27.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Electric Commercial Vehicle Battery Pack Market Analysis by Mordor Intelligence

The French electric commercial vehicle battery pack market size is expected to grow from USD 176.38 million in 2025 to USD 225.16 million in 2026 and is forecast to reach USD 762.47 million by 2031 at 27.62% CAGR over 2026-2031. Strict fleet electrification regulations under national climate legislation accelerate the shift to zero-emission transport in cities. These rules expedite vehicle purchases and clarify demand forecasts, helping suppliers stabilize production planning and reduce automotive volume volatility.

In Europe, emissions standards for heavy-duty vehicles are driving long-haul fleet operators to place orders earlier to meet targets. Falling battery costs make electric commercial cars more competitive, with total ownership costs nearing parity with diesel options. Regulatory allowances for higher weight limits in electric trucks eliminate payload disadvantages and enable larger battery packs. Utility-backed leasing programs are improving residual values and reducing financial risks, easing the transition for fleet operators.

Key Report Takeaways

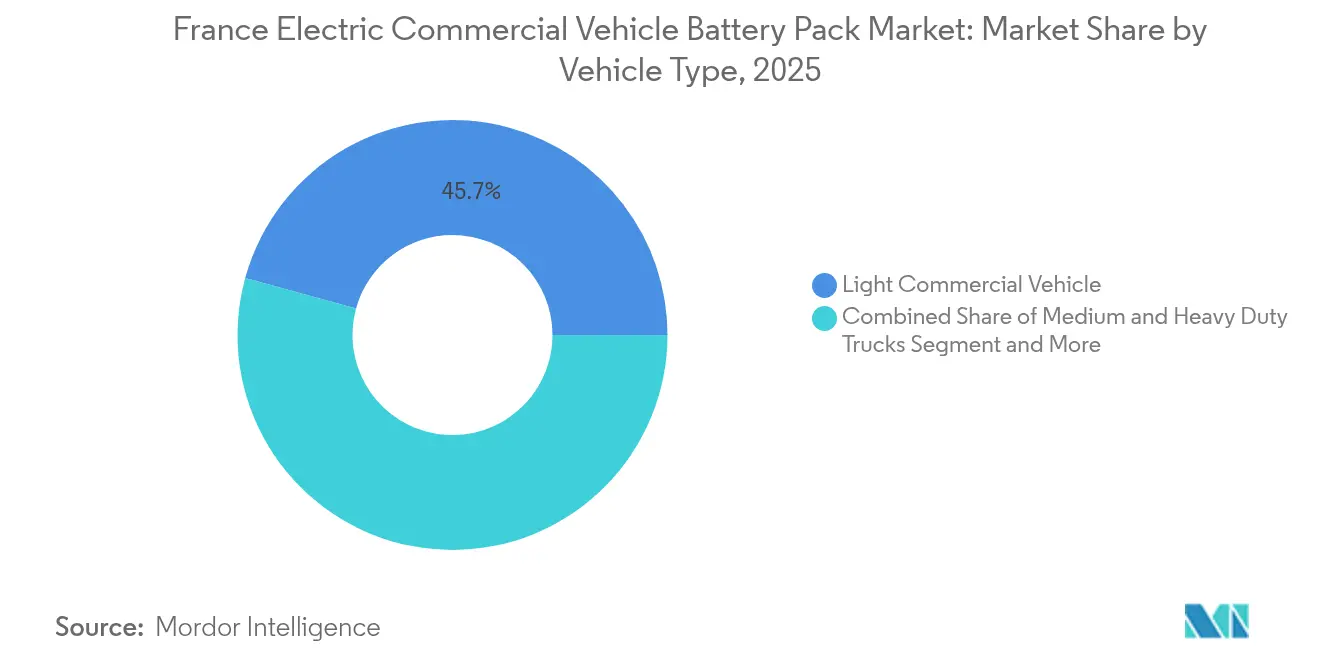

- By vehicle type, light commercial vehicles held 45.73% of the French electric commercial vehicle battery pack market share in 2025; medium and heavy-duty trucks are projected to advance at a 28.26% CAGR through 2031.

- By propulsion type, battery electric models captured 76.64% of the French electric commercial vehicle battery pack market share in 2025, and are projected to grow at a 27.96% CAGR to 2031.

- By chemistry, lithium iron phosphate accounted for a 40.98% share of the French electric commercial vehicle battery pack market size in 2025, while lithium manganese iron phosphate is set to expand at a 27.92% CAGR.

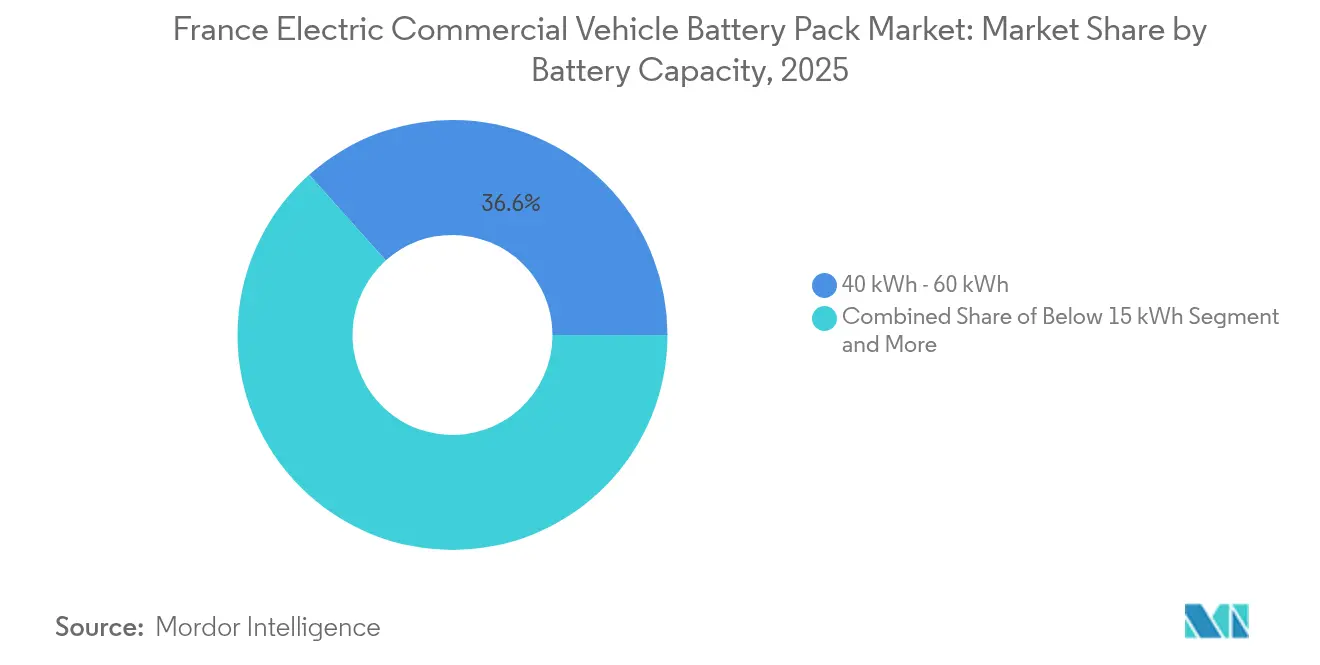

- By capacity, 40–60 kWh packs commanded 36.62% of the French electric commercial vehicle battery pack market size in 2025; 100–150 kWh packs led growth at 27.65% CAGR.

- By battery form, prismatic designs accounted for 48.62% of the French electric commercial vehicle battery pack market size in 2025 and are expected to continue rising at a 28.21% CAGR.

- By voltage class, 400–600 V systems controlled 56.54% of the French electric commercial vehicle battery pack market size in 2025, whereas 600–800 V platforms show a 28.37% CAGR.

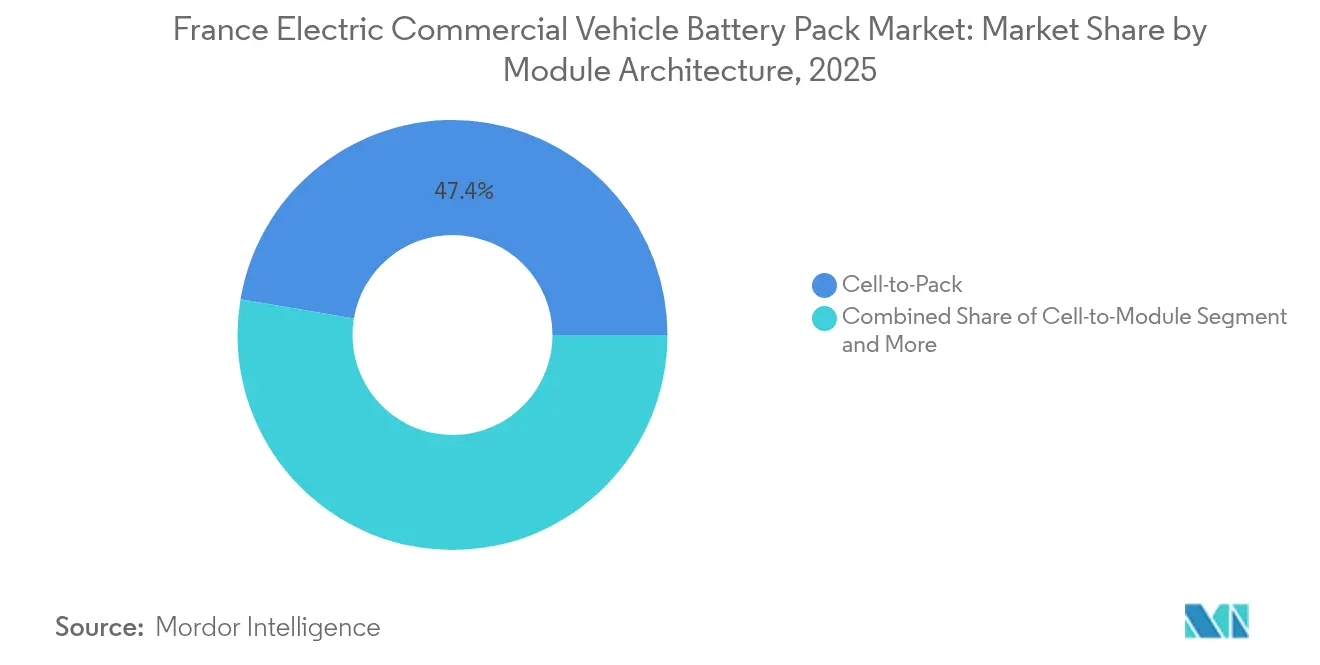

- By module architecture, cell-to-pack solutions held 47.35% of the French electric commercial vehicle battery pack market size in 2025, and recorded the highest 27.74% CAGR through 2031.

- By component, cathode held 37.58% of the French electric commercial vehicle battery pack market size in 2025, however separator recorded the highest 27.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Electric Commercial Vehicle Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet EV Targets (Climate Law) | +6.2% | National, concentrated in 43 ZFE cities | Short term (≤ 2 years) |

| Battery Cost Drop (Scale and Imports) | +4.8% | National with EU supply chain integration | Medium term (2-4 years) |

| ZEV Zones in Cities | +3.1% | Urban centers: Paris, Lyon, Marseille, Toulouse | Short term (≤ 2 years) |

| E-Truck TCO Shift (Weight Exemptions) | +2.9% | National freight corridors | Medium term (2-4 years) |

| Lithium Manganese Iron Phosphate for Bus Safety | +1.7% | Public transport networks nationwide | Medium term (2-4 years) |

| 2nd-Life Leasing (Utilities) | +1.4% | National grid integration points | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Fleet-Electrification Targets Drive Unprecedented Demand

France’s Climate and Resilience Law bans diesel commercial vehicles by 2025, forcing fleet operators to place immediate high-volume battery orders despite unproven long-term economics[1]“Zones à Faibles Émissions-Mobilité,”, Ministère de la Transition Écologique, ecologie.gouv.fr. Enforcement through automatic fines compresses procurement cycles from 3–5 years to roughly 12–18 months, which overwhelms supplier planning and creates temporary allocation bottlenecks. Euro 7 durability rules that impose 75% capacity retention on N1 vans further steer buyers toward premium chemistries with proven cycle life.

Declining Battery Costs Accelerate Commercial Viability

Battery pack costs have steadily declined in recent years due to increased production capacity and strategic industrial collaborations. Large-scale manufacturing initiatives in Europe are unlocking economies of scale, further reducing costs. Meanwhile, China's low-cost lithium iron phosphate batteries are intensifying competition, pushing domestic manufacturers to improve efficiency or risk losing market share.

These cost shifts are transforming urban transportation. In France, electric delivery fleets are nearing cost parity with diesel vehicles, signaling a likely transition to electric mobility in urban logistics within the next few years.

Zero-Emission Zones Create Geographic Demand Concentration

The jump from 11 to 43 ZFEs within one year funnels 60% of commercial registrations into Paris, Lyon, and Marseille, creating urban hotspots that test charging capacity and after-sales service density [2]“Observatoire des Zones à Faibles Émissions,”, ADEME, ademe.fr. Automatic plate-recognition enforcement removes compliance loopholes, so operators frontload electrification in dense cities and push demand troughs into suburban regions.

Weight Exemptions Transform E-Truck Economics

European regulators have set higher weight limits for electric trucks, a move not extended to diesel vehicles. This change addresses the added weight of batteries in electric trucks, allowing them to match the payload capacities of their diesel counterparts.

Moreover, updated tolling policies within the Eurovignette framework provide monetary incentives for greener transport choices. These toll reductions notably lower the operational expenses for electric trucks, hastening the journey towards achieving cost parity with diesel in long-haul freight [3]“Proposal for a Regulation Setting CO₂ Standards for Heavy-Duty Vehicles,”, European Commission, europa.eu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SME Fleet Cost Barrier | -2.3% | National, concentrated in rural/suburban areas | Short term (≤ 2 years) |

| Cell Supply Gap (Pre-2026) | -1.8% | National manufacturing capacity constraints | Medium term (2-4 years) |

| Battery Passport Burden | -1.4% | EU-wide regulatory compliance | Medium term (2-4 years) |

| Grid Delays for MW Charging | -0.9% | Major freight corridors and industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SME Fleet Cost Barriers Persist Despite Incentives

Despite the availability of substantial government grants aimed at facilitating the transition, electric vans continue to require a notably higher initial investment than their diesel counterparts. This financial burden poses a significant challenge, especially for small fleet operators with often limited budgets.

Compounding the issue, traditional leasing companies are still wary of fully adopting electric commercial vehicles. Their reservations arise from uncertainties regarding the long-term value of battery packs in high-mileage scenarios, a concern heightened by the lack of comprehensive real-world testing.

Domestic Production Capacity Lags Demand Growth

France's battery cell production lags behind market demand, and this gap is set to continue for several years. Although significant industrial ramp-ups are in the pipeline, they won't be fully functional for some time, forcing manufacturers to lean on imports.

Dependence on overseas suppliers, especially from Asia, is extending lead times and bolstering the pricing power of these external entities. Consequently, the European electric vehicle sector grapples with supply chain challenges and mounting cost pressures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Light Commercial Dominance With Heavy-Truck Upside

Light commercial vehicles captured 45.73% of the French electric commercial vehicle battery pack market share in 2025, reflecting their fit with urban delivery patterns mandated by zero-emission zones (ZFEs). Their standardized 40–60 kWh packs match daily mileage limits and enable high production scale, which lowers per-kilowatt-hour costs for fleet buyers. ZFE enforcement through automatic plate recognition removes compliance loopholes and locks in demand from courier, postal, and service fleets concentrated in Paris, Lyon, and Marseille. Weight-exemption rules add up to 2 tonnes of allowable mass, so payload losses that once deterred e-van adoption no longer threaten revenue on dense urban routes.

Medium and heavy-duty trucks register the fastest 28.26% CAGR through 2031 as 100–150 kWh packs pair with 600–800 V drivetrains to chase long-haul electrification targets. Payload-neutral operations made possible by the exemption accelerate substitution on key freight corridors, especially where megawatt chargers cut dwell times to under 45 minutes. Municipal bus fleets remain the smallest volume slice yet set the pace for technology adoption because fire-safe LMFP chemistries satisfy strict depot insurance requirements. Taken together, vehicle-type diversification balances supplier exposure between quick-cycle urban demand and longer-term heavy-truck ramps that follow infrastructure build-out.

By Propulsion Type: Battery Electric Vehicles Cement Lead

Battery electric models held 76.64% of 2025 segment shipments as fleet operators prioritize mechanical simplicity and lower service costs over plug-in hybrid flexibility. Regenerative braking improves energy recapture during stop-and-go duty cycles, extending real-world range without adding pack mass. Higher purchase incentives for pure EVs versus PHEVs further tilt total cost of ownership equations in favor of all-electric drivetrains.

Plug-in hybrids preserve a niche among regional haulers who need diesel backup while charging coverage matures. Yet, their share continues to slide as 600–800 V architectures deliver rapid top-up capabilities for battery electrics. Fleet data show that once daily mileage regularly exceeds 150–200 km inside ZFEs, BEVs outperform hybrids on fuel, maintenance, and compliance penalties. As French corridors add high-power chargers, operators increasingly retire PHEVs at lease end rather than renew them, cementing BEVs as the propulsion standard for commercial use cases.

By Battery Chemistry: Cost-Centric LFP Faces Safety-Driven LMFP Surge

Lithium iron phosphate secured a 40.98% share in 2025 because its favorable EUR/kWh profile aligns with parcel-van and regional freight budgets. The chemistry’s inherent thermal stability also suits urban depots that lack elaborate fire-suppression systems.

Lithium manganese iron phosphate is the fastest-growing chemistry, with a 27.92% CAGR, driven by municipal bus tenders that now specify enhanced thermal-runaway thresholds following several high-profile fires. Lithium manganese iron phosphate’s 160–180 Wh/kg density helps buses meet range targets without using pricier nickel-rich NMC (Nickel-Manganese-Cobalt-Oxide) blends. Traditional NMC variants continue to appeal to payload-sensitive heavy trucks, while NCA (Lithium Nickel Cobalt Aluminum Oxide) and LTO (Lithium Titanium Oxide) serve niche, high-performance, or extreme-cycle-life applications. Suppliers, therefore, tailor portfolios across cost, safety, and energy-density vectors rather than betting on a single chemistry roadmap.

By Capacity: Mid-Range Packs Dominate, High-Capacity Units Accelerate

The French electric commercial vehicle battery pack market size, attributable to 40–60 kWh packs, captured 36.62% in 2025 because this window covers 90% of urban delivery missions under ZFE restrictions. Standardization allows OEMs to spread tooling cost across multiple van platforms while ensuring sub-60-minute recharge at existing 150 kW urban chargers.

High-capacity 100–150 kWh batteries post the highest 27.65% CAGR as long-haul fleets pivot to electric rigs that exploit weight exemptions on 40-tonne combinations. Operators prefer a single large pack over dual-pack architectures to cut maintenance complexity and streamline end-of-lease residual calculations. Sub-15 kWh and 15–40 kWh units remain confined to plug-in hybrids and specialty lift platforms, whereas packs above 150 kWh await broader megawatt charging coverage before scaling in volume.

By Battery Form: Prismatic Cells Optimize Commercial Interiors

Prismatic formats accounted for 48.62% of shipments in 2025 and continue to post a 28.21% CAGR because their rectangular geometry maximizes floor-pan volume and simplifies liquid-cooling plate integration. The stable housing also aids field service, enabling faster module swaps during tight delivery windows.

Cost-sensitive applications often favor cylindrical cells, thanks to their widespread availability and competitive pricing. Yet, in space-constrained environments like panel vans, where maximizing chassis volume is paramount, the round shape of these cells can prove inefficient. Pouch cells, frequently utilized in lightweight fleet equipment, offer design flexibility. However, they come with the caveat of needing extra mechanical protection, complicating packaging and driving up costs. On the other hand, prismatic cells are becoming the go-to choice for fleet operators. Their rectangular shape not only simplifies assembly but also trims down the overall vehicle weight, making them a standout option in commercial layouts.

By Voltage Class: Mainstream 400–600 V Balances Cost and Performance

Systems rated 400–600 V maintained a 56.54% share last year, hitting the sweet spot where off-the-shelf inverters, contactors, and safety components meet cost and regulatory constraints. This class charges up to 250 kW without exotic insulation requirements, fitting daily depot cycles for most vans and medium trucks.

The 600–800 V tier records a 28.37% CAGR thanks to megawatt charging pilots that trim long-haul dwell times below mandated driver rest periods. Fleets weighing upgrade costs against productivity gains typically adopt higher voltage when daily mileage exceeds 500 km or when vehicle utilization tops 20 hours per day. Sub-400 V architectures persist in hybrid and micro-utility vehicles, while >800 V experimental systems remain on test tracks until safety standards mature.

By Module Architecture: Cell-to-Pack Takes Weight Out, Keeps Uptime High

Cell-to-pack platforms captured 47.35% of 2025 volume and expanded at a 27.74% CAGR because eliminating intermediate modules removes 10–15% weight and slices roughly 5% off material cost. Every kilogram saved translates into added payload or range for urban vans capped by gross vehicle weight limits.

Early concerns over field reparability fade as suppliers launch mobile service rigs capable of on-site partial cell replacement within four hours, minimizing downtime penalties that once favored modular systems. Cell-to-module remains popular in heavy trucks where operators value quick swap-outs on multi-shift duty cycles. Module-to-pack architectures persist mainly to amortize legacy tooling but lose share each year as new chassis launch directly with integrated designs.

By Component: Cathode Materials Anchor Value, Separators Race Ahead

Cathode powders represented 37.58% of the bill-of-materials value in 2025 because nickel, manganese, and phosphate proportions decide energy density and thermal profile. Price swings for lithium carbonate feedstock directly influence pack quotations and thus procurement calendars for large fleets.

Separator films show the fastest 27.95% CAGR as next-generation ceramic-coated variants raise shutdown temperatures above 150 °C to meet Euro 7 durability rules for N1 vans. Anodes edge toward silicon-enhanced blends at 25% of value to lift capacity without breaching cost ceilings, while electrolyte suppliers refine flame-retardant additives tailored to heavy-duty thermal loads. Localization efforts steer component contracts toward French or wider-EU producers to secure Battery-Passport compliance and de-risk geopolitical supply shocks.

Geography Analysis

Île-de-France has taken the lead in France's electric commercial vehicle battery market. The region's dominance stems from a dense network of zero-emission zones and parcel distribution hubs, all centered around Paris. Early investments in high-powered public charging infrastructure, coupled with proactive municipal incentives, have spurred the adoption of electric vans, with new registrations significantly outpacing the national average.

Île-de-France's proximity to a major battery cell manufacturing facility offers local vehicle manufacturers reduced logistics costs and quicker turnaround times for service parts. Planned upgrades to the electrical grid near key freight hubs promise to boost connection capacity, setting the stage for high-powered charging corridors vital for heavy-duty electric trucks. These infrastructure and supply chain advantages are driving robust growth in regional battery demand.

Southern France, with cities like Lyon, Marseille, and Toulouse, is witnessing a swift rise in electric vehicle battery adoption. This surge is largely attributed to the push for zero-emission compliance in tourism logistics and port operations. Initiatives like discounted port fees for electric drayage trucks have spurred logistics firms to embrace battery packs that align with fast-charging infrastructure on major transport routes.

Local governments are bolstering this shift by co-financing depot upgrades that incorporate solar energy and second-life battery storage. Such initiatives not only cut electricity costs during peak hours but also enhance the economics of electric truck ownership, allowing for quicker recovery of initial investments.

Western and Northern industrial zones, situated outside major metropolitan areas, represent the remaining share of national battery demand. Yet, their progress is hampered by limited charging infrastructure. As a result, many rural transport cooperatives still depend on diesel vehicles, awaiting the completion of planned grid upgrades that will facilitate high-capacity charging depots.

Competitive Landscape

A mix of domestic and international players shapes France’s electric vehicle battery supply landscape. Local manufacturers have secured a significant portion of the market, with notable contributions from firms focused on scaling production and tailoring solutions for commercial fleets. One leading domestic supplier has secured considerable financing to expand its production capacity, aiming to meet a substantial share of national demand and reduce reliance on imports from Asia.

Another French company has achieved financial stability by offering modular battery solutions designed for last-mile delivery vans, which require quick and efficient servicing—an attractive feature for courier fleets operating under tight schedules.

In response to growing pressure for localization, Asian battery leaders are forming joint ventures and licensing technologies to maintain their presence in the French market. One such partnership involves a large-scale plant supplying batteries for light commercial vehicles. At the same time, another collaboration focuses on developing advanced battery systems that reduce structural weight and meet stringent durability standards—key factors for medium-sized vans competing on payload efficiency. Some Asian firms are also expanding their footprint through direct vehicle sales bundled with charging infrastructure, bypassing traditional battery integrators and capturing additional revenue from energy services.

As the market matures, competitive focus is shifting away from pure energy density toward comprehensive lifecycle support and regulatory compliance. Companies with integrated recycling programs and second-life battery solutions are gaining an edge in tenders prioritizing environmental stewardship. Service reliability is also becoming a key differentiator, with some suppliers offering rapid on-site repairs to meet fleet uptime targets. Overall, the ability to scale production, localize operations, and provide end-to-end solutions is the most critical factor for gaining market share, surpassing chemistry innovation as the primary driver of competitive advantage.

France Electric Commercial Vehicle Battery Pack Industry Leaders

Contemporary Amperex Technology Co. Ltd. (CATL)

LG Energy Solution Ltd.

Forsee Power

Automotive Cells Company (ACC)

Akasol AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Renault Group revealed plans for its Sandouville site to manufacture a groundbreaking lineup of electric light commercial vehicles (LCVs). These vehicles are destined for Flexis SAS, a newly formed joint venture by Renault Group, Volvo Group, and CMA CGM. The initiative aims to strengthen the collaboration between these industry leaders, leveraging their combined expertise to drive innovation in the electric LCV market.

- February 2024: ACC has successfully closed a EUR 4.4 billion debt raising, significantly enhancing its funding for constructing three gigafactories dedicated to lithium-ion battery cell production across France, Germany, and Italy. This funding will also support the company's research and development initiatives, further strengthening its position in the market.

France Electric Commercial Vehicle Battery Pack Market Report Scope

The French Electric Commercial Vehicle Battery Pack Market Report is Segmented by Vehicle Type (Light Commercial Vehicle, and More), Propulsion Type (BEV, and More), Battery Chemistry (LFP, and More), Capacity (Below 15 KWh, and More), Battery Form (Cylindrical, and More), Voltage Class (Below 400 V, and More), Module Architecture (CTM, and More), Component (Anode, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Light Commercial Vehicle |

| Medium and Heavy Duty Trucks |

| Bus |

| Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) |

| NMC (Nickel Manganese Cobalt Oxide) |

| NCA (Nickel Cobalt Aluminum Oxide) |

| LTO (Lithium Titanium Oxide) |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) |

| Below 15 kWh |

| 15 - 40 kWh |

| 40 - 60 kWh |

| 60 - 80 kWh |

| 80 - 100 kWh |

| 100 - 150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Below 400 V (48 - 350 V) |

| 400 - 600 V |

| 600 - 800 V |

| Above 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| By Vehicle Type | Light Commercial Vehicle |

| Medium and Heavy Duty Trucks | |

| Bus | |

| By Propulsion Type | Baterry Electric Vehicle |

| Plug-in Hybrid Electric Vehicle | |

| By Battery Chemistry | LFP (Lithium Iron Phosphate) |

| LMFP (Lithium Manganese Iron Phosphate) | |

| NMC (Nickel Manganese Cobalt Oxide) | |

| NCA (Nickel Cobalt Aluminum Oxide) | |

| LTO (Lithium Titanium Oxide) | |

| Others (LCO, LMO, NMX, Emerging Battery Technologies, etc.) | |

| By Capacity | Below 15 kWh |

| 15 - 40 kWh | |

| 40 - 60 kWh | |

| 60 - 80 kWh | |

| 80 - 100 kWh | |

| 100 - 150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Below 400 V (48 - 350 V) |

| 400 - 600 V | |

| 600 - 800 V | |

| Above 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 2

- Vehicle Type - Vehicle type considered under this segment include commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms