Bio-alcohols Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

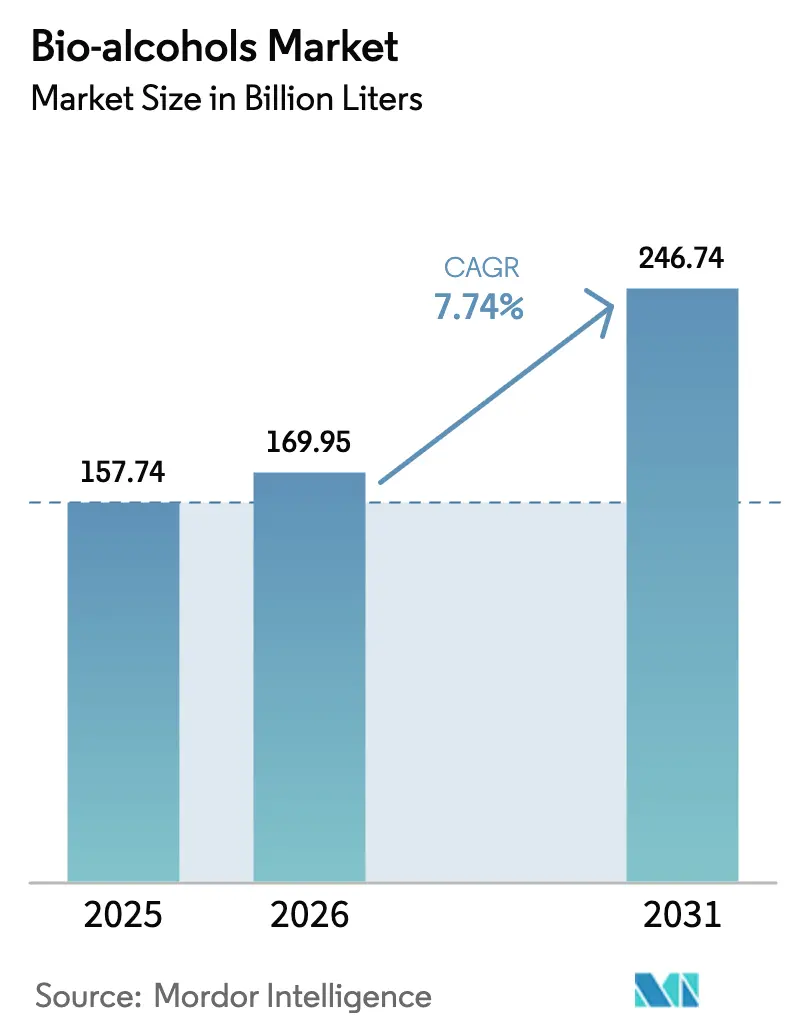

| Market Volume (2026) | 169.95 Billion liters |

| Market Volume (2031) | 246.74 Billion liters |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

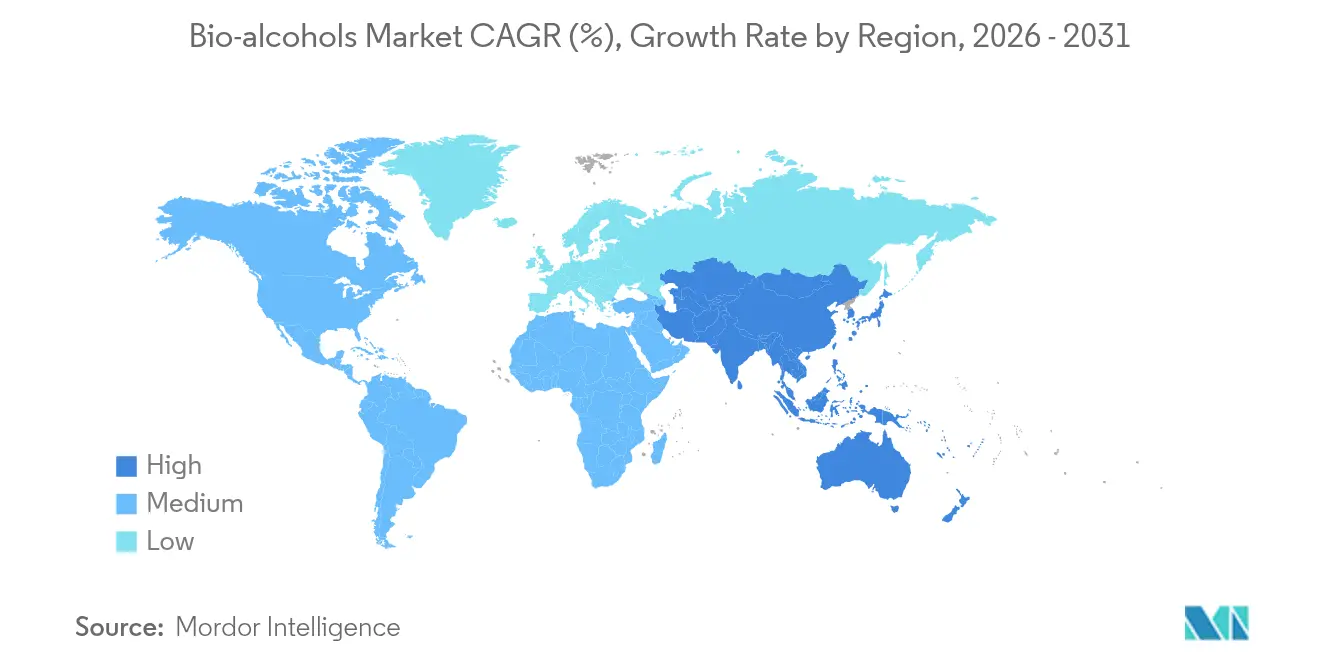

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

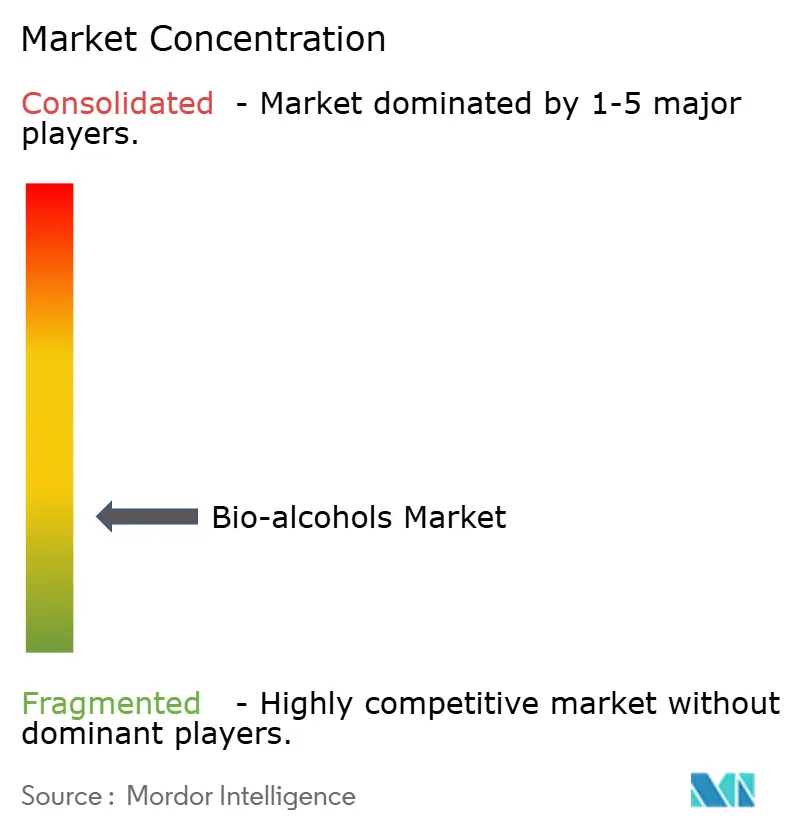

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-alcohols Market Analysis by Mordor Intelligence

Bio-alcohols Market size in 2026 is estimated at 169.95 billion liters, growing from 2025 value of 157.74 billion liters with 2031 projections showing 246.74 billion liters, growing at 7.74% CAGR over 2026-2031. This growth reflects tightening renewable-fuel rules, quick progress in alcohol-to-jet certification, and the arrival of commercial carbon-capture-to-alcohol systems that give refiners fresh revenue while cutting emissions. Demand is also being reshaped by sustainable marine-fuel corridors, premium chemical uses in consumer goods, and stronger investor appetite for low-carbon supply chains. Established North American producers keep scale advantages, yet Asia-Pacific is adding capacity faster thanks to policy tailwinds and cost-optimized technologies. Feedstock innovation, especially with algae and industrial off-gases, is helping moderate margin risks linked to crop price swings, while strategic offtake deals with airlines and shippers give investors cash-flow clarity.

Key Report Takeaways

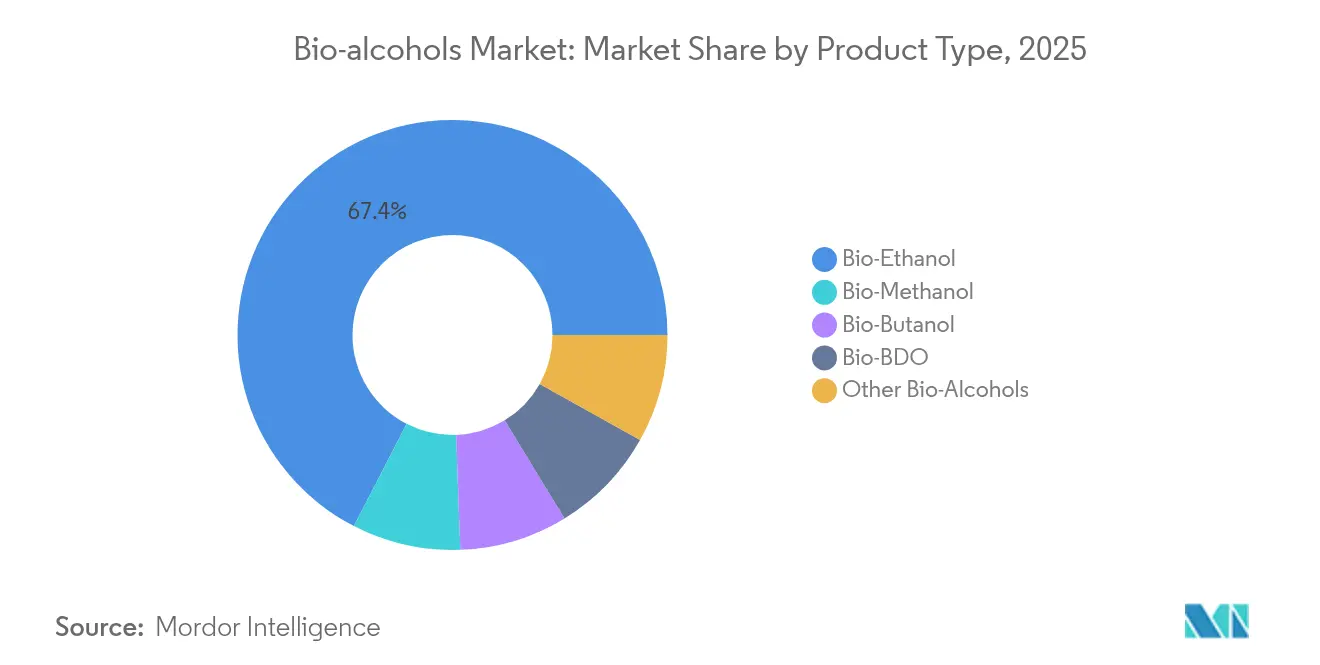

- By product type, bio-ethanol captured 67.42% of revenue in 2025; bio-butanol is projected to grow at a 9.07% CAGR through 2031.

- By feedstock, starch-based routes held 45.21% of 2025 sales, but algal biomass is forecast to climb at an 10.62% CAGR.

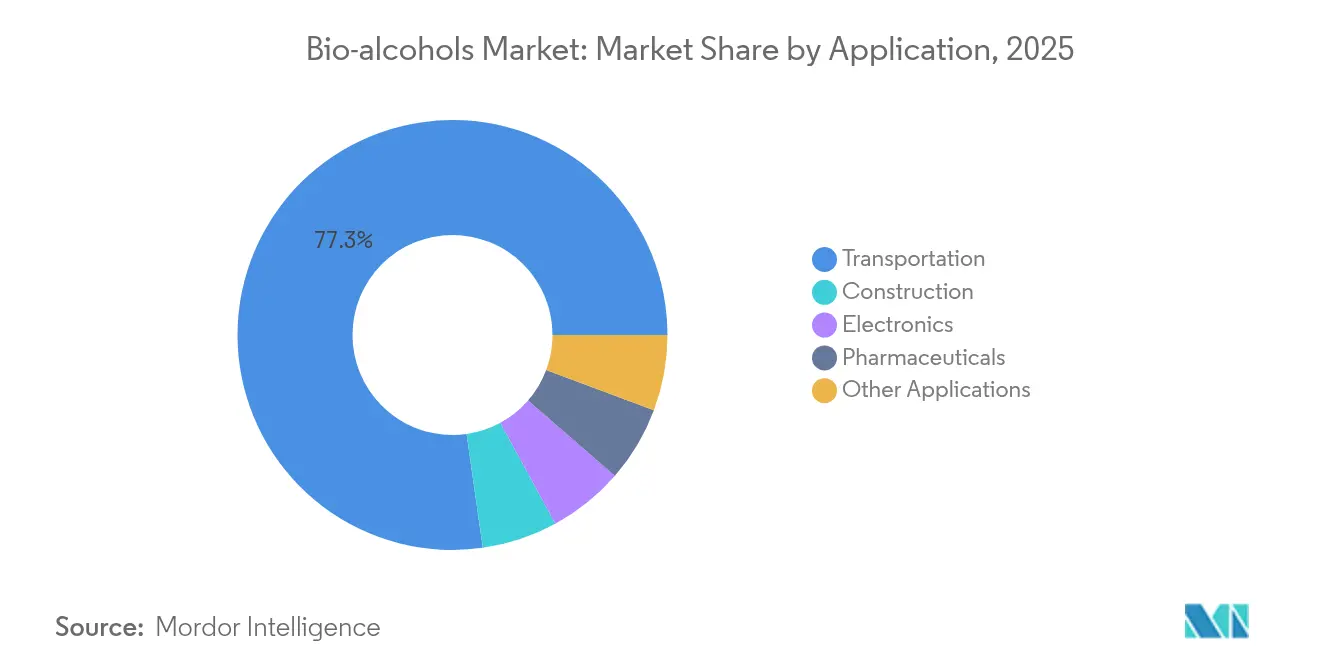

- By application, transportation retained 77.25% of demand in 2025, while other emerging uses are poised for a 10.31% CAGR.

- By region, North America led with 39.02% of the Bio-alcohol market share in 2025, while Asia-Pacific is set to post the fastest 9.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bio-alcohols Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandated ethanol-blend targets | +2.10% | Global, with early gains in India, Brazil, EU | Medium term (2-4 years) |

| Rapid airline SAF certification of Alcohol-to-Jet pathways | +1.80% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Integration of CO₂ to alcohol CCU plants at refineries | +1.60% | North America, EU, emerging in China | Long term (≥ 4 years) |

| Bio-alcohol use as low-carbon chemical feedstock in CPG | +1.40% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Emerging methanol-powered shipping corridors | +0.90% | APAC core, spill-over to Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandated Ethanol-Blend Targets

Blend mandates guarantee demand, reduce investor risk, and speed plant expansions. India’s goal of 30% blending by 2030, having already reached 20%, shows the upside that ambitious policy can unlock. The EU’s ReFuelEU Aviation rule starts with 2% SAF in 2025 and rises to 70% by 2050, offering a clear runway for alcohol-to-jet projects[1]European Commission, “ReFuelEU Aviation,” ec.europa.eu . Brazil’s E27 program remains a template for high blend ratios once logistics barriers ease. Because mandates shield volumes from commodity swings, producers can line up long-term feedstock contracts and lower financing costs.

Rapid Airline SAF Certification of Alcohol-to-Jet Pathways

Aviation’s net-zero push has sharply accelerated testing of alcohol-to-jet routes. LanzaJet’s Freedom Pines Fuels site in Georgia already makes 9 million gallons a year and gives financiers confidence that large plants will run reliably[2]U.S. Department of Energy, “LanzaJet Freedom Pines Fuels,” energy.gov . Axens’ Jetanol projects now top 1 billion gallons per year of planned capacity, underlining the technology’s bankability. SAF often sells at two to three times the price of conventional jet fuel, so bio-ethanol producers enjoy wider margins when they pivot toward aviation customers. Long-term airline offtake deals, such as Southwest’s agreement with USA BioEnergy, further derisk project cash flows.

Integration of CO₂-to-Alcohol CCU Plants at Refineries

Refineries adopting carbon-capture-and-utilization units can recycle exhaust gas into ethanol, creating new product lines while cutting tax exposure. LanzaTech and Eramet will build a Norwegian plant that converts furnace gas into 24 kilotons of ethanol a year. When coupled with sequestration stages, the same hardware delivers dual revenue—saleable alcohol plus carbon credits. Operators can size systems to match local emissions and demand, spreading capital over phased expansions and improving returns.

Bio-Alcohol as Low-Carbon Chemical Feedstock in CPG

Consumer brands want traceable, renewable inputs for everyday products. BASF’s rollout of bio-based ethyl acrylate in Q4 2024 proves that large chemical lines can swap petro-feed with bio-alcohols without re-tooling plants. Braskem’s USD 87 million boost to its green ethylene unit signals growing orders from polymer buyers. Because these specialty chemicals command premiums over fuel blends, producers can diversify earnings and hedge exposure to transport cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility | -1.20% | Global, acute in regions dependent on agricultural commodities | Short term (≤ 2 years) |

| Insufficient pipeline compatibility for high-blend alcohols | -0.80% | North America, EU infrastructure limitations | Medium term (2-4 years) |

| Stagnant global light-vehicle production post-2027 | -0.60% | Global automotive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Insufficient Pipeline Compatibility for High-Blend Alcohols

Most petroleum pipelines cannot handle high alcohol blends due to corrosion and water uptake, forcing reliance on truck or rail. The extra logistics cost erodes delivered-price competitiveness, especially in regions far from blending terminals. Upgrading lines needs cooperation between many owners and warrants high capital that some markets cannot justify yet.

Stagnant Global Light-Vehicle Production Post-2027

Vehicle output is predicted to plateau after 2027 as ownership saturates and electric cars grab share. The IEA sees total oil demand flattening near 105.5 million barrels per day by 2030, signaling limited upside for gasoline and, by extension, ethanol blending[3]International Energy Agency, “Oil 2025,” iea.org . The result is greater urgency for producers to pivot toward aviation, marine, and chemical outlets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Ethanol Dominance Masks Specialty Growth

Bio-ethanol kept a 67.42% 2025 Bio-alcohol market share, underpinned by mature plants, standardized specs, and supportive mandates. Its conversion cost edge and global supply chain reinforce leadership. The Bio-alcohol market size for bio-ethanol is expected to expand steadily in line with nationwide blend limits that increase absolute volume even as gasoline peaks. Yet bio-butanol’s superior energy density and drop-in compatibility are propelling its 9.07% CAGR and a rising slice of premium chemical demand.

Alcohol-to-jet breakthroughs provide a higher-value outlet for ethanol. LanzaJet’s early operating data confirm that low-cost agricultural ethanol can be upgraded into SAF that sells at a 2-3× price multiple. Meanwhile, bio-methanol is carving room in marine fuels and plastics, and bio-BDO caters to pharmaceutical and engineered-material niches. Collectively, specialty alcohols diversify the Bio-alcohol market and lessen sensitivity to road-fuel swings.

By Feedstock: Starch Supremacy Challenged by Algal Innovation

Starch pathways kept 45.21% of 2025 volume thanks to plentiful corn and wheat, integrated milling assets, and co-product credits. That scale advantage helps them anchor pricing, and multi-decade logistics know-how raises barriers for newcomers. Still, the Bio-alcohol market size captured by starch is gradually ced¬ing ground as policy pressure favors non-food inputs.

Algal biomass is the breakout story, clocking an 10.62% CAGR on better photobioreactor yields and DOE grant support. Pilot farms reach cost parity sooner by recycling nutrients and harvesting lipids alongside sugars. Lignocellulosic residues and municipal waste streams are also inching forward, turning disposal liabilities into revenue. This diverse basket improves resilience when bad weather or trade shocks hit grain supplies.

By Application: Transportation Dominance Faces Diversification Pressure

Transportation still wrote 77.25% of demand in 2025, reflecting embedded blend frameworks and robust logistics. The segment’s sheer scale anchors offtake for new projects, letting plants run at high utilization. However, other uses are rising at 10.31% CAGR as electronics, construction, and pharma buyers prize renewable solvents.

Smartphone factories deploy high-purity ethanol for circuit cleaning, while building-material suppliers blend bio-alcohols into low-VOC coatings. Pharma firms need USP-grade alcohol both as an active and an excipient. BASF’s bio-acrylate line anchors this shift, showing that major chemical platforms can switch feedstocks without quality sacrifice. The pivot reduces reliance on vehicle sales cycles and cushions revenue when gasoline demand flattens.

Geography Analysis

North America’s 39.02% 2025 share mirrors its dense corn-to-ethanol corridor, ample rail logistics, and the Renewable Fuel Standard that keeps baseline volumes. Canada’s 2025 Clean Fuel Regulation widens demand for low-carbon blends beyond the United States. Mexico’s new mill investments knit the continent into a self-reinforcing supply chain. Summit Next Gen’s USD 1.6 billion Texas ethanol-to-SAF complex, eligible for JETI subsidies, underlines how local grants align with federal tax credits to lure mega-projects.

Asia-Pacific is the growth engine, tracking a 9.21% CAGR on the back of India’s fast-tracked 30% blend agenda and record rice-feedstock pull. China adds momentum by funding CO₂-to-alcohol pilots that dovetail with its 2060 neutrality plan, while Japan and South Korea channel green-fuel incentives at refineries and airports. ASEAN markets, including the Philippines, are lifting blending rules too, keeping regional demand broad-based. This policy updraft attracts joint ventures that stitch together local feedstock with imported technology, accelerating capacity rollout.

Europe moves with stringent carbon-pricing and SAF mandates that jump-start premium niches. The ReFuelEU rulebook gives investors clarity on future SAF ramp-ups, while Germany and the UK run national subsidies to ensure domestic production. Feedstock flexibility, including sugar beet and waste biomass, helps buffer supply shocks. South America continues leveraging cheap sugarcane and advanced second-generation mills that process bagasse, supporting steady export flows to deficit regions. The Middle East and Africa, though smaller, are piloting projects as part of diversification strategies.

Value Chain Analysis

The bio-alcohols value chain starts with feedstock origination and aggregation, spanning starch and sugar crops, woody biomass, agricultural residues, algal biomass, and industrial off-gases/MSW. Upstream participants include farmers, cooperatives, and industrial emitters, followed by pre-processing (milling, hydrolysis, gas conditioning), conversion (fermentation or gas fermentation), and downstream purification and dehydration to meet fuel, solvent, or chemical-grade specifications. Recent partnerships point to tighter upstream integration to secure low-carbon attributes and supply continuity. Examples include Roquette, Vivescia, and Siplec E.Leclerc aligning French wheat supply chains with retail fuel distribution for low-carbon ethanol, and the Morisora Bio Refinery LLC joint venture (Nippon Paper Industries, Sumitomo Corporation, Green Earth Institute) advancing woody-biomass-to-ethanol development around existing mill infrastructure.

Midstream and downstream logistics are also a differentiator, since alcohol handling, blending, and distribution must address water uptake and compatibility constraints. This often channels volumes to rail, truck, terminals, and dedicated storage rather than multi-product pipelines for higher blends. Commercial routes increasingly link to higher-value demand nodes, including aviation and chemicals, with LanzaJet demonstrating alcohol-to-jet upgrading at commercial scale and Arkema and Catalyxx developing a bio-based acrylic resin value chain where bio-n-butanol (from bioethanol) becomes a key intermediate for downstream formulations. Bottlenecks center on multi-feedstock reliability and cellulosic processing complexity, including equipment wear from solids handling, tailored microbial strains, and the low density of biomass that increases collection, storage, and transport costs, which in turn supports more localized production hubs near feedstock sources and end-use infrastructure.

Competitive Landscape

The Bio-alcohol market is fragmented. ADM, Cargill, and other grain majors lock in feedstock via owned elevators and hedging desks, delivering cost leadership in starch ethanol. BASF and Braskem fold bio-alcohols into chemical value chains, gaining access to higher-margin markets. LanzaTech and Gevo push proprietary conversion routes, forming royalty streams and creating barriers for late entrants.

Scale continues to matter, yet the game is shifting from volume to differentiation. Producers chase vertical integration—growing feedstock, converting, and marketing—in one platform to capture the spread. Horizontal alliances are also rising: airline-producer SAF offtake pacts and chemical-producer licensing deals stabilize demand and finance. Newcomers emphasize low-cost waste feedstocks, CCU loops, and premium compliance credits instead of price wars.

Government backing shapes the field. Gevo’s USD 1.63 billion DOE loan accelerates its Net-Zero 1 plant, demonstrating how federal financing can fast-forward commercialization of novel pathways. Regional grants, joint R&D, and carbon markets complement private capital, letting innovators leapfrog to scale without replicating decades-old fermentation footprints.

Bio-alcohols Industry Leaders

ADM

Cargill Incorporated

POET LLC

Valero Energy Corporation

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity centers on low-carbon compliance and premium end-markets that reward differentiated carbon intensity, particularly where policy clarity and certification pathways translate into capacity actions. In the United States, the EPA finalized the Renewable Fuel Standard Set 2 rule in March 2026, setting 2026 and 2027 volume targets and reallocating 70% of small refinery exemptions granted from 2023 to 2025. This reinforces the role of regulated volumes for conventional and advanced biofuels. On the supply side, POET broke ground in June 2026 on an expansion at its Shelbyville, Indiana bioprocessing facility to increase output, which illustrates how incumbents are adding capacity to serve higher-value demand across fuel and industrial markets.

White space is also emerging through technology upgrades that move commodity ethanol into higher alcohols and specialty chemical intermediates, alongside localized, non-food feedstock supply chains that help limit crop volatility. In Europe, Catalyxx received a EUR 20 million grant in June 2026 from the Clean Hydrogen Partnership (CBE JU) to build an industrial-scale plant for bio-based higher alcohols, with Arkema and Evonik named as partners, connecting bio-alcohol production to downstream materials demand. In South America, new grain-based projects and expansions suggest continued investment momentum in year-round corn ethanol, including Bioenergética Aroeira's announced R$750 million investment in a new plant in Minas Gerais (June 2026) and CerradinhoBio's start-up of a corn ethanol expansion in Chapadão do Céu that raises corn processing capacity from 800,000 to 1.2 million tonnes per year (June 2026). Together, these actions support a broader shift toward multi-feedstock resilience and higher-value outlets such as sustainable aviation fuel and bio-based chemicals, while blending programs continue to anchor demand.

Recent Industry Developments

- June 2026: POET Bioprocessing held a groundbreaking ceremony for an expansion project at its Shelbyville, Indiana facility. The investment adds capacity and strengthens POETs ability to serve fuel-grade and industrial bio-alcohol demand while improving asset utilization across its processing network.

- November 2025: ADM and Tallgrass commenced operations of a bioethanol carbon capture and storage project at ADMs Columbus, Nebraska corn processing complex. Using the Trailblazer pipeline system to move CO2 to a sequestration hub in Wyoming, the project supports lower-carbon ethanol supply and improves access to carbon-intensity-driven markets.

- September 2024: LanzaTech and SEKISUI CHEMICAL CO., LTD. established a master license agreement to commercialize waste-to-ethanol conversion technology. The licensing framework enables facility deployment across Japanese municipalities and expands pathways for feedstock-diversified ethanol production tied to circular waste management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The bio alcohols market is defined as the demand and supply of bio-based alcohols made from biomass and used as fuel blendstocks and as industrial alcohols for chemical, solvent, and related manufacturing use, reported in volume.

Scope exclusions: Beverage alcohol and alcohol production that is purely fossil-derived are not counted in this market sizing.

Segmentation Overview

- By Product Type

- Bio-Methanol

- Bio-Ethanol

- Bio-Butanol

- Bio-BDO

- Other Bio-Alcohols

- By Feedstock

- Starch-based Crops

- Sugar-based Crops

- Lignocellulosic Biomass

- Algal Biomass

- Industrial Off-gases and MSW

- By Application

- Transportation

- Construction

- Electronics

- Pharmaceuticals

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for production, blending, and consumption patterns, and then to anchor regional splits before we finalized totals. We checked public source types such as energy and fuel agencies, agriculture statistics bodies, customs and trade portals, and standards and regulatory publications to understand mandated blending levels, typical blend rates, and compliance timelines. We also reviewed peer-reviewed journals and patent filings to confirm which pathways and feedstocks were scaling in practice versus staying at pilot level.

On the company side, annual reports, investor presentations, and plant announcements were reviewed to map capacity additions, shutdowns, and debottlenecking, which helped us avoid over-counting nameplate capacity. For market context, reputable news coverage and association updates were used to confirm changes in policy, crude price linkages, and demand shocks. Where used, paid subscriptions were limited to company financials and intelligence, patent lookups, and shipment-level import export checks when trade flows were a key driver. These desk research sources are illustrative only, and many additional public and internal reference sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with bio-alcohol producers, distributors, fuel blenders, and downstream industrial buyers, because pricing logic and actual utilization can differ from what capacity figures suggest. We collected input across major demand regions to sanity-check blend-rate assumptions, regional trade dependence, and the pace of higher-alcohol adoption in both fuel and industrial uses. Where desk data was thin, these conversations were also used to set practical ranges for yields, operating rates, and regional price premiums before we finalized the totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 18% | APAC: 42% |

| Mid tier: 47% | Functional/Unit leaders: 27% | EMEA: 36% |

| Smaller Players: 18% | Managers: 55% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using both top-down and bottom-up logic, with the main structure coming from a top-down demand pool that reconstructs bio-alcohol use from fuel consumption, mandated and realized blend rates, and regional industrial alcohol demand indicators. Once regional demand pools were established, we translated them into volumes by applying market-specific conversion factors and typical product mix, then reconciled against production and trade signals.

To keep the model grounded, we tracked practical inputs such as gasoline and diesel consumption trends in major blending countries, annual blend mandates and compliance rates, installed fermentation and upgrading capacity with estimated utilization, import export balances for ethanol and other bio-alcohols, and the relative share shift toward higher alcohol blends where regulations allow. Results were then corroborated with selective bottom-up approximations, including sampled producer shipments, channel checks on distributor volumes, and average selling price ranges where pricing is transparent enough to act as a reasonableness check. When direct observations were missing for smaller countries, gaps were handled through proxying from comparable blend policies, vehicle fuel demand, and trade dependence, followed by primary re-checks.

For forecasting, we used scenario analysis supported by simple time-series methods (exponential smoothing on key demand drivers) so policy shifts and commodity-linked swings could be reflected without overfitting. Assumptions on mandate changes, adoption speed, and utilization were reviewed with industry participants, and we adjusted the final forecast only when multiple signals moved in the same direction.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals, including regional fuel demand totals, announced capacity moves, and net trade direction, and then reviewed for year-to-year jumps that did not match policy or plant events. When variances appeared, we investigated through re-checking unit conversions, blend-rate assumptions, and utilization settings, followed by a second-pass analyst review before sign-off.

The report is refreshed annually, with interim updates when material events occur, such as mandate revisions, major plant outages, or sudden demand shocks. Before delivery, we run a final update pass to ensure the latest policy notes, trade trends, and capacity changes are reflected in the published numbers.

Mordor Intelligence's Bio Alcohols Market Size Measured Against Other Published Estimates

Published estimates for bio alcohols often spread out because the market can be measured in different units, and because some studies mix fuel volumes with broader chemical and energy value pools. Differences also come from how each publisher treats blend compliance versus mandate targets, and whether trade flows and inventory swings are actively reconciled.

The main gap driver is that the reported market size here is explicitly built in liters from realized consumption and blend behavior, while other sources present USD values that can swing based on assumed pricing, inflation treatment, and whether adjacent products are included. When higher alcohols, industrial solvents, or wider biofuel categories are folded into the definition, the total can look much larger even if physical bio-alcohol volumes are similar, which is why the table shows a wide spread against the volume-based sizing used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 169.95 B (2026) | |

| Trade Publisher A | USD 15.40 B (2024) | This figure is value-based and tends to be driven by assumed average pricing across bio-alcohol types, so the total shifts based on price decks, currency timing, and what is counted as industrial use versus fuel use. |

| Global Publisher B | USD 74.75 B (2025) | This estimate appears to cover a broader value pool and a wider definition of bio alcohol applications, which can include more end uses and inflate totals when compared with a liters-based demand build that follows realized blending and consumption. |

Looking at the three lines together, the direction of the gap is consistent with unit choice and scope choice rather than just growth assumptions. By keeping the core model tied to measurable volume drivers like blend realization, fuel demand, and trade balance checks, and using prices only as secondary reasonableness checks, the final output stays transparent and repeatable even when price environments change.

Key Questions Answered in the Report

What is the current Bio-alcohol market size?

The market reached 169.95 billion liters in 2026 and is projected to hit 246.74 billion liters by 2031.

Which region leads the Bio-alcohol market?

North America held 39.02% of Bio-alcohol market share in 2025, backed by established corn-to-ethanol infrastructure.

What segment is growing fastest?

Bio-butanol is forecast to grow at a 9.07% CAGR from 2026-2031 thanks to its higher energy density and chemical versatility.

How are airlines driving demand?

Alcohol-to-jet pathways are certified quickly, and offtake contracts with carriers guarantee volumes at premium prices, lifting producer margins.

Why is algae gaining attention as a feedstock?

Algae avoids food-fuel conflict, offers year-round yields, and has attracted government grants, supporting an 10.62% CAGR outlook for algal routes.

What risks could slow Bio-alcohol market growth?

Feedstock price swings, limited pipeline compatibility for high blends, and flat light-vehicle output after 2027 could dampen the pace unless diversification continues.

Page last updated on: