Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

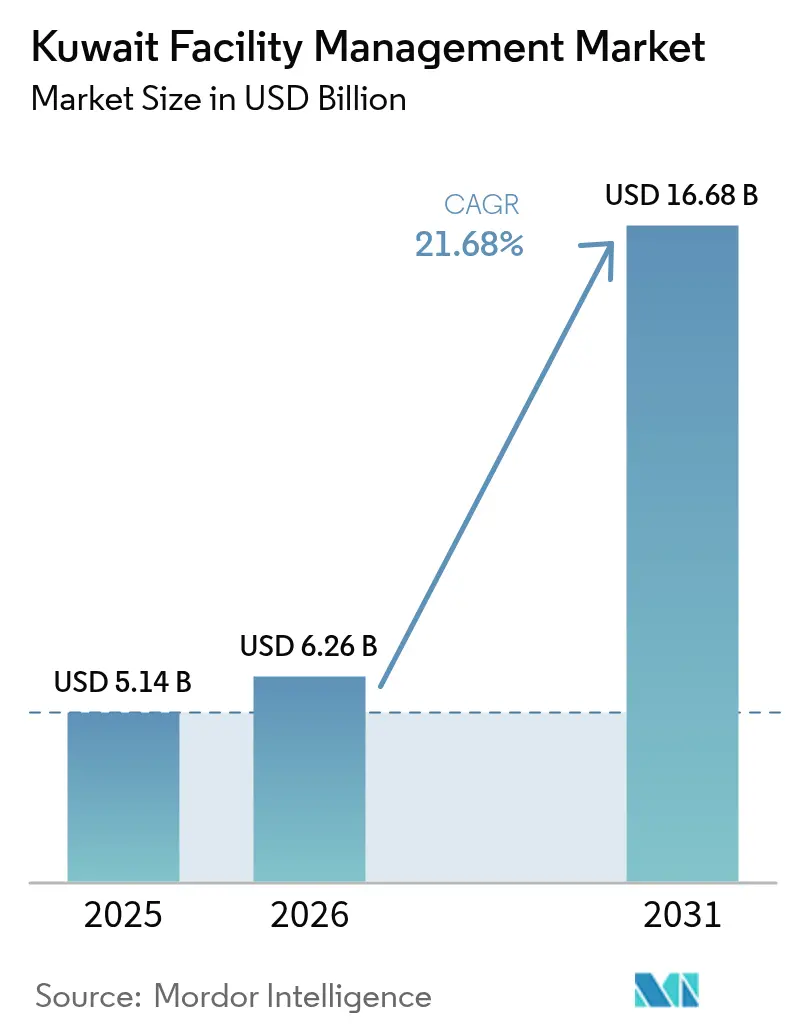

| Base Year Market Size (2025) | USD 5.14 Billion |

| Market Size (2026) | USD 6.26 Billion |

| Market Size (2031) | USD 16.68 Billion |

| Growth Rate (2026 - 2031) | 21.68% CAGR |

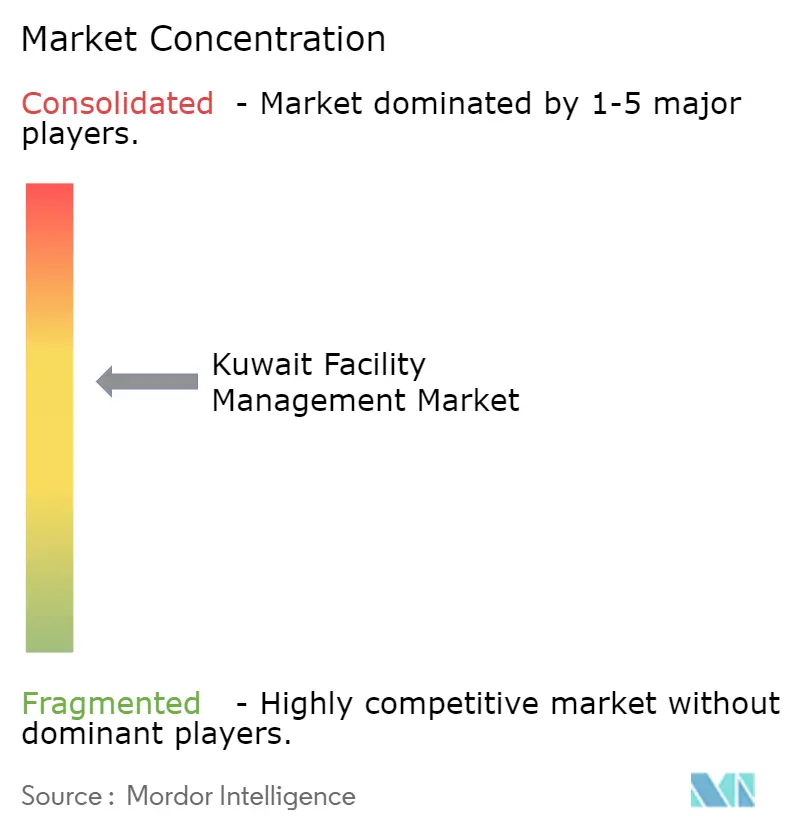

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait Facility Management Market Analysis by Mordor Intelligence

Kuwait facility management market size in 2026 is estimated at USD 6.26 billion, growing from 2025 value of USD 5.14 billion with 2031 projections showing USD 16.68 billion, growing at 21.68% CAGR over 2026-2031. The surge is anchored in Vision 2035, which funnels USD 124 billion into 164 national development programs and demands sophisticated, ESG-aligned facility solutions.[1]U.S. Department of Commerce, “Kuwait – Infrastructure,” TRADE.GOV Massive infrastructure spending, technology-enabled asset management, and stricter energy-efficiency mandates collectively amplify demand for integrated hard and soft services across commercial, industrial, and public assets. Outsourcing contracts linked to public–private partnership (PPP) projects now dominate new awards because they transfer execution risk to specialized firms that combine MEP expertise with Internet-of-Things (IoT) analytics. Kuwait’s harsh climate intensifies focus on predictive HVAC maintenance, while the state’s 2060 net-zero pledge accelerates adoption of green financing and performance-linked service models. Medium-term headwinds arise from Kuwaitization rules that tighten expatriate hiring and from elevated cooling costs that pressure operating budgets, but technology adoption and outcome-based contracts continue to broaden the Kuwait facility management market opportunity set.

Key Report Takeaways

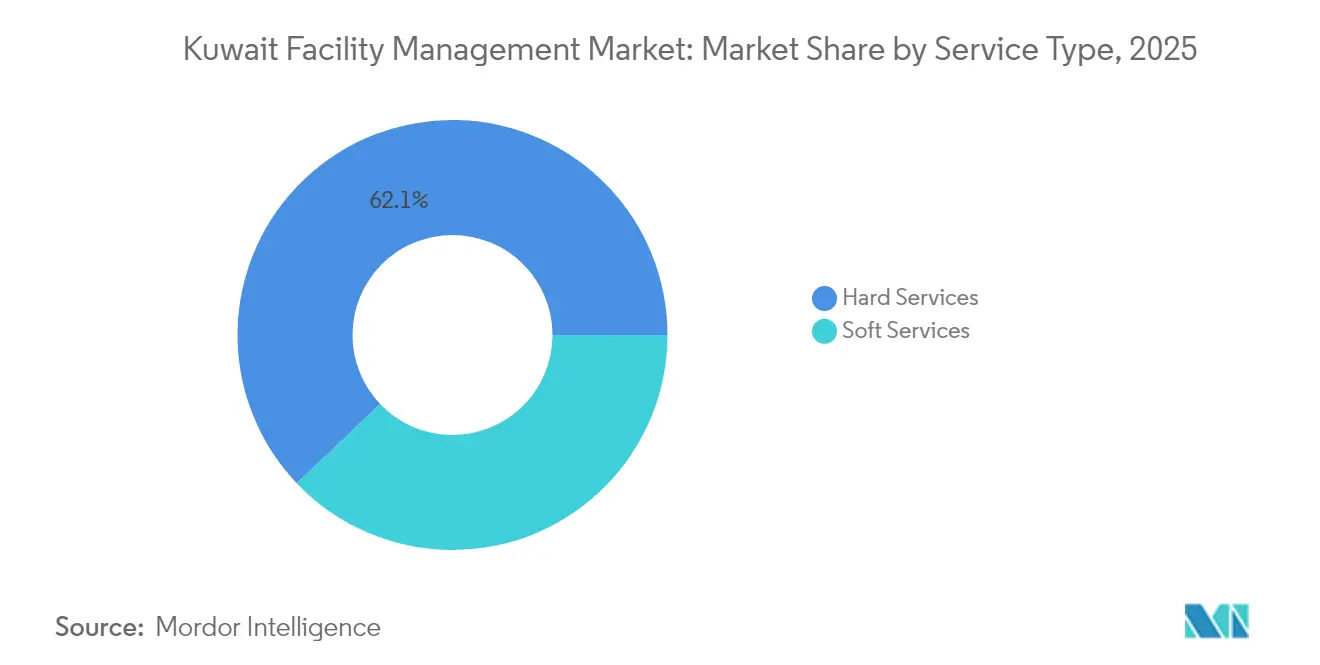

- By service type, hard services held 62.10% of Kuwait facility management market share in 2025, while soft services are advancing at a 23.15% CAGR through 2031.

- By offering type, the outsourced segment accounted for 60.75% of the Kuwait facility management market size in 2025 and is projected to expand at 21.95% CAGR through 2031.

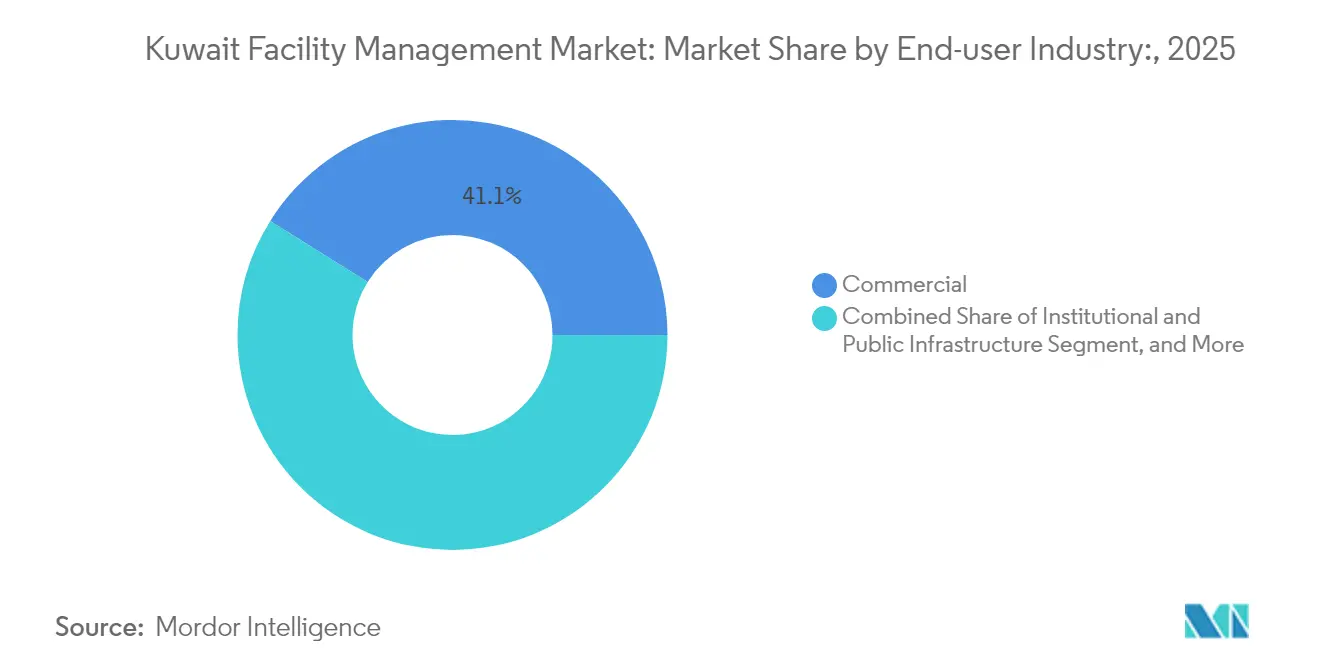

- By end-user industry, commercial facilities commanded 41.10% revenue share in 2025; the industrial and process segment records the fastest growth at 22.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and Population Growth | +4.2% | National (Kuwait City focus) | Medium term (2-4 years) |

| Technology-Led Integrated FM | +3.8% | National (commercial and industrial) | Long term (≥4 years) |

| ESG-Compliant FM Solutions | +3.1% | National (government and corporate) | Medium term (2-4 years) |

| Outcome-Based Contracts | +2.9% | National (outsourced FM) | Short term (≤2 years) |

| Vision 2035 Infrastructure Spending Surge | +5.4% | National (mega-project sites) | Long term (≥4 years) |

| PPP and Privatization Initiatives Accelerating FM Outsourcing | +2.8% | National (public infrastructure) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanization and Population Growth: Catalyst for FM Expansion

Kuwait’s plan to add 250,000 new housing units and modern mixed-use districts intensifies the need for integrated services that can coordinate security, cleaning, waste, and energy management across dense developments. Greater population concentration in Kuwait City raises expectations for digitally enabled building performance, pushing providers toward predictive maintenance and sensor-based energy dashboards. Urban mixed-use designs also blur traditional service boundaries, so contractors must synchronize residential, retail, and municipal assets within single service-level agreements. Training and certification programs for local technicians gain importance because complex urban assets require skilled MEP and HVAC specialists to guarantee uptime during summer peaks that exceed 48 °C.[2]American Society of Mechanical Engineers, “Energy Saving Opportunities Using Building Energy Simulation,” ASMEDIGITALCOLLECTION.ASME.ORG Demand is highest for providers who can deliver 24/7 control-room monitoring that links occupancy data with automated work-order generation.

Technology-Led Integrated FM: Redefining Service Delivery

IoT sensors embedded in chillers, pumps, and elevators now feed real-time data into building management systems that cut energy use by up to 40% when paired with AI routines.[3]Abdullah H. Alkhalidi, “AI-Based Optimization of HVAC Systems in Kuwait,” SCIENCEDIRECT.COM Oil and gas operators have proven the model at assets such as Greater Burgan, where integrated digital‐field technology reduced unscheduled downtime and lifted throughput. Cost barriers are declining because cloud platforms reduce on-premise hardware, yet skills shortages persist; firms therefore invest in remote diagnostics centers that pool scarce data-science talent and support multisite portfolios. Use-case adoption starts with HVAC optimisation, then expands to smart lighting, asset tracking, and occupant experience apps. Cyber-security protocols aligned with Kuwait’s national data-protection law are increasingly written into FM contracts as digital maturity rises.

ESG-Compliant FM Solutions: New Value Proposition

The government’s 2060 carbon-neutral target embeds sustainability criteria into tenders, making energy audits, green cleaning chemicals, and waste diversion metrics standard contract deliverables. National Bank of Kuwait’s rollout of rooftop solar on 18 branches saved 28.3% in emissions from a 2021 baseline, showcasing the operational pay-off of green retrofits.[4]National Bank of Kuwait, “2024 Sustainability Report,” NBK.COM Lenders reinforce momentum by issuing green bonds that price in environmental performance, which lowers funding costs for compliant assets. Facility managers, therefore, bundle LED relamping, high-efficiency chiller retrofits, and real-time consumption dashboards into integrated offerings that promise up to 70% energy savings relative to baseline. Healthcare and education owners increasingly make tender awards contingent on audited ESG scorecards, accelerating market differentiation for providers with certified sustainability professionals.

PPP and Privatization Initiatives Accelerating FM Outsourcing

The Kuwait Authority for Partnership Projects standardises PPP frameworks that allow private operators to design, build, finance, and operate public assets, transferring performance risk while earning revenues through availability payments. Power and water projects such as Az-Zour North rely on specialist operators for plant O&M, creating steady demand for industrial facility services. PPP models spur competitive tendering, which encourages value-based bids tied to reliability guarantees rather than head-count metrics. Providers use these deals to lock in multidecade cash flows that support investment in training and technology upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workforce Constraints | −2.1% | National (technical roles) | Short term (≤2 years) |

| Regulatory & Legislative Framework | −1.8% | National (public sector) | Medium term (2-4 years) |

| Persistent Client Preference for In-house FM in Public Sector Contracts | −1.3% | National (government facilities) | Long term (≥4 years) |

| Extreme Climatic Conditions Increasing Maintenance and Energy Costs | −2.4% | National (industrial and commercial) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Workforce Constraints: Limiting Market Expansion

Cabinet Resolution 1179 of 2023 accelerates Kuwaitization quotas on public contracts, limiting access to the foreign technicians that historically staffed complex MEP roles.[5]Suzanne Horne, “Kuwait,” LEXOLOGY.COM Local talent pipelines remain nascent, so firms scale up scholarship and on-the-job training programs to certify Kuwaiti nationals in HVAC, electrical, and digital-controls disciplines. Visa restrictions for certain expatriate nationalities further tighten supply and push wages upward. Automation through remote monitoring and robotics partially offsets labour gaps, yet capital intensity rises, squeezing smaller contractors. Private employers also compete with public-sector institutions that offer higher job security, making retention difficult despite wage premiums.

Regulatory and Legislative Framework: Reshaping Labor Dynamics

New tax rules such as the Domestic Minimum Top-Up Tax introduce 15% levies on large multinationals, which may discourage some global FM firms from setting up local entities. Revised procurement procedures add compliance layers, prolonging bid timelines and driving up legal costs. Labour code updates increase health-insurance and end-of-service liabilities, particularly for high-risk industrial deployments. Firms therefore renegotiate price-adjustment clauses that share regulatory cost escalation with clients, but margin pressure persists until the rule set stabilises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Infrastructure Modernization

Hard services contributed 62.10% of Kuwait's facility management market revenue in 2025 as mega-projects, refineries, and high-rise offices required robust MEP, HVAC, and fire-protection systems able to withstand harsh desert conditions. Demand is underpinned by the USD 124 billion project pipeline, which assigns priority to asset reliability and life-cycle operating cost reduction. Within hard services, HVAC optimisation represents the largest spend theme because cooling loads account for the bulk of building energy budgets; predictive algorithms have become standard in new tenders. Fire-safety retrofits follow closely, reflecting tighter enforcement after recent industrial incidents. Energy-performance contracts increasingly bundle chiller isolation valves, motor upgrades, and smart metering into multi-year agreements that guarantee consumption baselines.

Soft services, although smaller, post a 23.15% CAGR as mixed-use developments and international office tenants demand concierge-style security, premium cleaning, and workplace experience programs that meet global standards through 2031. Technology infusion is evident in robotic floor scrubbers and app-based visitor management, but human capital still dominates the cost structure. Synergies emerge when a single provider rationalises both hard and soft scopes across campuses, supporting the growth of integrated FM packages. ESG targets promote green-cleaning chemicals and waste segregation, spurring provider investments in supply-chain certification.

By Offering Type: Outsourcing Accelerates Through PPP Initiatives

Outsourced contracts held 60.75% share in 2025 and expand at 21.95% CAGR as ministries and state-owned enterprises convert fixed payrolls into flexible service fees through competitive tenders linked to PPP rules. Integrated FM sub-contracts gain momentum within power and water concessions, where performance-linked payments align operator and authority objectives.

Bundled FM grows among mid-tier commercial assets that cannot justify full integration but value single-invoice simplicity. In-house models fall to 39.25% share as lifecycle complexity rises and clients seek access to data analytics platforms that most internal teams cannot fund. Early-stage projects often embed transition clauses that transfer operations to outsourced providers once construction achieves substantial completion, locking in long-term service pipelines.

By End-user Industry: Commercial Leadership Meets Industrial Growth

Commercial facilities delivered 41.10% of total 2025 revenue as malls, financial institutions, and telecom campuses relied on premium facility operations to attract tenants and meet uptime SLAs. Service intensity in this segment remains high due to 24/7 cooling and stringent cyber-security for critical data infrastructure. The Kuwait facility management market size for industrial and process plants is smaller today but logs the fastest 22.10% CAGR through 2031, powered by nearly USD 100 billion of Kuwait Petroleum Corporation investments aimed at lifting oil output by 33%.

Healthcare projects valued above USD 4 billion contribute steady growth as hospitals outsource non-clinical support to focus on patient care. Hospitality assets recover alongside tourism promotion, prompting retrofits that elevate brand standards to regional benchmarks. Public infrastructure facilities gradually embrace outsourcing, yet long approval cycles temper near-term revenue.

Geography Analysis

Kuwait City and its adjacent suburbs anchor most projects, making the capital the epicenter of the Kuwait facility management market. The cluster includes government ministries, head-office towers, and mixed-use districts that require integrated command centers linking HVAC sensors, security cameras, and work-order software. Outside the capital, northern oilfields such as Greater Burgan and the Al-Zour industrial zone generate concentrated industrial service demand tied to refinery and petrochemical uptime. These sites favour long-term master agreements covering rotating equipment, electrical substations, and safety-instrumented systems.

Healthcare capacity expansion spreads demand across multiple governorates because new hospitals aim to shorten patient travel times. Facility managers therefore establish mobile response teams that rotate across facilities using cloud-based maintenance platforms. Coastal districts adjacent to tanker terminals demand corrosion-management programs due to salt-laden air that accelerates metal fatigue. Interior logistics parks built along new road corridors add warehousing volumes that require cold-chain monitoring and fire-suppression audits.

The government’s smart-city pilots integrate district cooling, smart lighting, and autonomous transit, which elevate service complexity but also concentrate data for portfolio-wide analytics. As asset density rises, providers leverage economies of proximity, enabling multi-client technician pools that cut travel time and raise first-fix rates. Overall, geography shapes service mix, with industrial north and coastal zones prioritising heavy-duty maintenance, while urban cores emphasize occupant experience and energy optimisation.

Competitive Landscape

The Kuwait facility management market features moderate concentration; the top five providers collectively control roughly 55% of outsourced spend. Leading incumbents combine decades of local project delivery with global alliances that supply IoT platforms and energy-performance methodologies. Contract wins often hinge on proven ability to mobilise multi-disciplinary teams quickly during peak summer months when asset failure risk is highest. International entrants form joint ventures with local firms to navigate labour laws and meet Kuwaitization quotas while importing best-practice processes.

Technology capability serves as the primary differentiator. Providers that embed AI-powered chiller optimisation and fault-diagnostic dashboards secure premium pricing. ESG competence also drives awards as owners seek measurable carbon reductions to qualify for green financing. Mergers and acquisitions accelerate because scale helps amortise digital-platform costs and strengthens negotiation leverage with sub-contractors. Smaller specialists survive by focusing on healthcare sterility services, high-voltage substation maintenance, or industrial rope access, often acting as tier-two suppliers under integrated FM umbrellas.

Performance-based contracting shifts risk toward operators but opens upside through gain-share clauses tied to energy savings. Larger firms accept this evolution thanks to diversified portfolios that balance high-risk industrial assets with lower-risk commercial offices. Supply-chain resilience rises on the agenda after global logistics disruptions, prompting providers to stock critical spares locally and qualify multiple suppliers for key components. Overall, competition revolves around reliability, technology adoption, and compliance agility rather than sheer manpower scale.

Kuwait Facility Management Industry Leaders

PIMCO Kuwait

Kharafi National FM

EcovertFM

Al Mazaya Holding Company KSCP

ENGIE Services General Contracting for Buildings Company WLL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Acwa Power completed a USD 693 million acquisition of an 18% stake in the Az-Zour North utility complex, creating a platform for expanded facilities services across power and water assets.

- March 2025: Kuwait Petroleum Corporation confirmed nearly USD 100 billion of upstream and downstream investment over five years to lift oil production capacity by 33% by 2040, underpinning long-term industrial FM demand

- February 2025: Kuwait Authority for Partnership Projects refined PPP regulations, easing private participation in infrastructure and enlarging the outsourced services pipeline.

- January 2025: Kuwait enacted a 15% Domestic Minimum Top-Up Tax on large multinationals, potentially affecting cost structures for global FM firms.

Kuwait Facility Management Market Report Scope

Facility management (FM) services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further segmented by hard facility management services and soft facility management services. The adoption of FM solutions and services is likely to be driven by several factors, including an increase in demand for cloud-based FM solutions and a rise in demand for FM systems linked to intelligent software.

Kuwait Facility Management Market is Segmented by type of facility management (In-house Facility Management, Outsourced Facility Management (Single FM, Bundled FM, Integrated FM)), by Offering Type ( Hard FM, Soft FM), and by End-User (Commercial, Institutional, Public/ Infrastructure, Industrial). The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the market size of the Kuwait facility management market in 2026?

The market is valued at USD 6.26 billion in 2026.

What CAGR will the Kuwait facility management market register between 2026 and 2031?

It is forecast to expand at a 21.68% CAGR through 2031.

Which service type holds the largest share of the market?

Hard services lead with 62.10% revenue share in 2025.

Which service type is growing the fastest?

Soft services post the quickest growth, recording a 23.15% CAGR over 2026–2031.

Which end-user segment shows the highest growth potential?

The industrial and process segment is advancing at a 22.10% CAGR on the back of nearly USD 100 billion of oil-sector investments.

What are the top two headwinds facing facility managers in Kuwait?

Abour shortages linked to Kuwaitization policies and the high maintenance costs imposed by extreme summer temperatures present the most significant challenges.

Page last updated on: