Intumescent Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

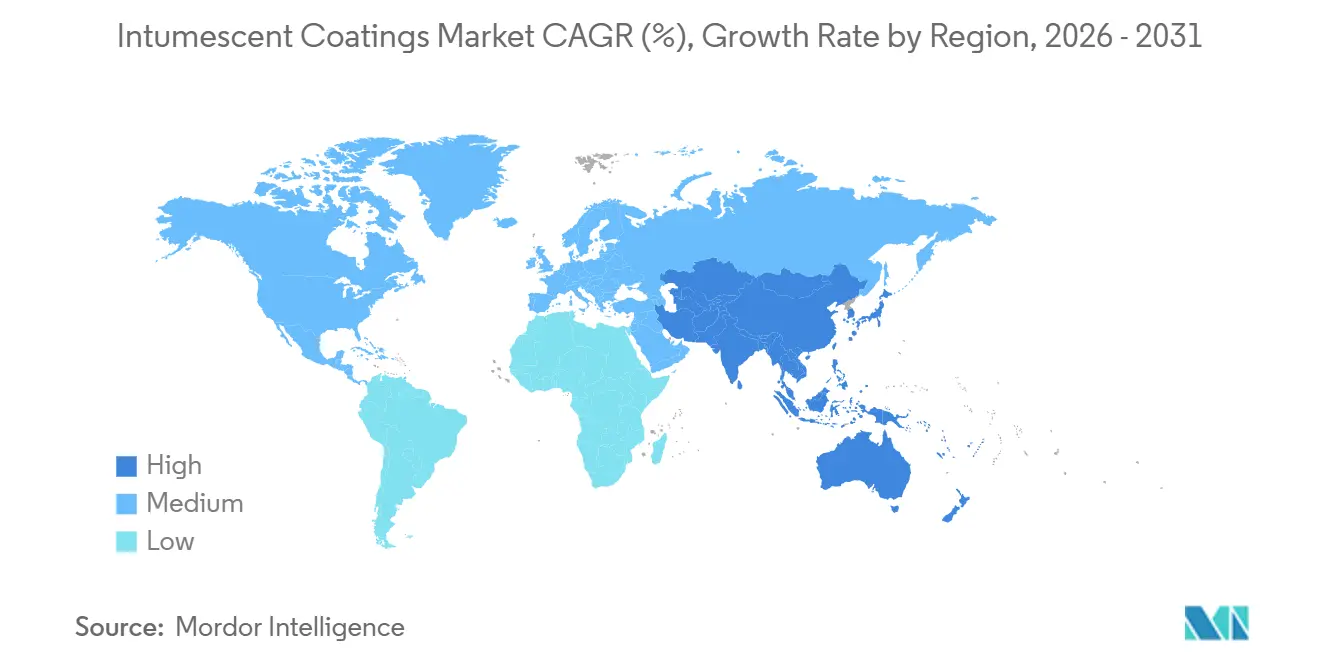

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

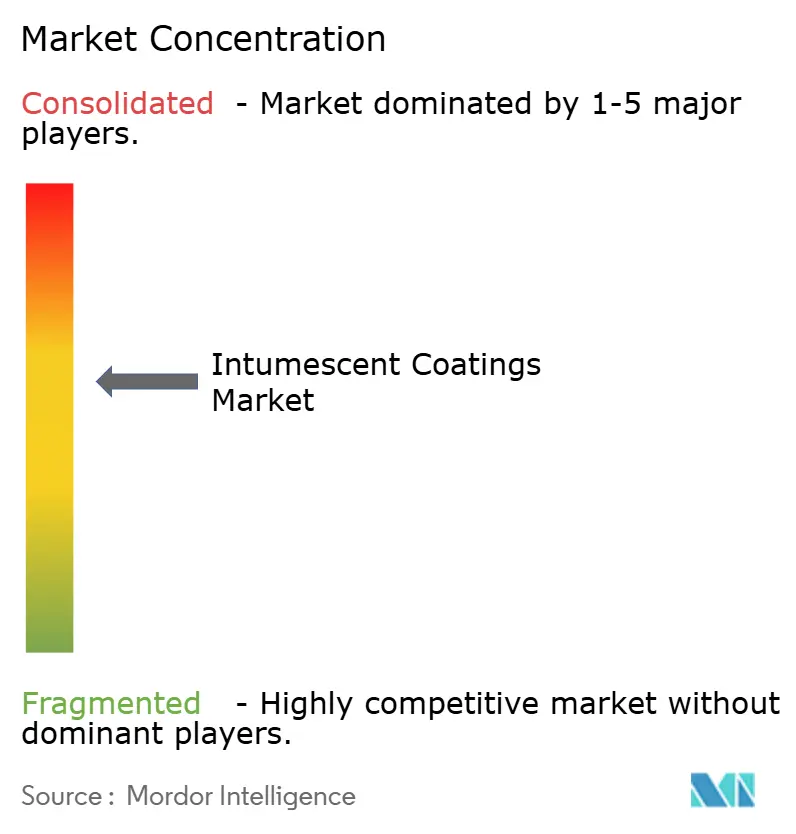

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intumescent Coatings Market Analysis by Mordor Intelligence

The Intumescent Coatings Market size is projected to be USD 1.37 billion in 2025, USD 1.42 billion in 2026, and reach USD 1.74 billion by 2031, growing at a CAGR of 4.14% from 2026 to 2031. Demand is shifting toward water-based chemistries that expand at 5.44% annually as European volatile-organic-compound limits tighten and Middle Eastern contractors seek faster turnaround times. Epoxy-based formulations still command almost one-half of global revenue, yet nano-engineered char-formers now allow up to 40% thinner films that cut material use and shorten curing schedules. Asia-Pacific leads growth at 5.86% CAGR because China and India now mandate passive fire protection for steel frames taller than 15 meters, accelerating retrofit activity in tier-1 and tier-2 cities. Construction has become the fastest-growing end-user segment at 4.95% CAGR as building owners prioritize 120-minute ratings in high-occupancy projects, while hydrocarbon facilities keep oil and gas the single largest application by revenue.

Key Report Takeaways

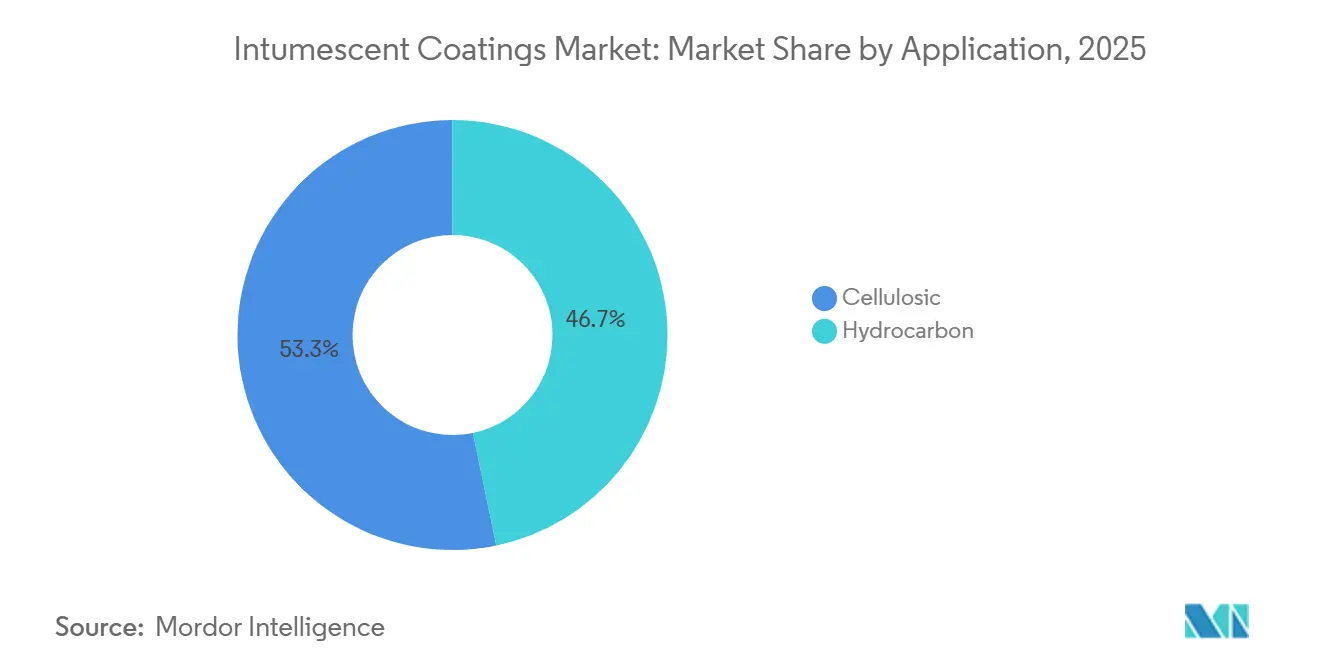

- By application, cellulosic coatings led with 53.27% of the intumescent coatings market share in 2025, while hydrocarbon systems are advancing at a 5.18% CAGR to 2031.

- By technology, water-based systems captured 40.36% revenue in 2025 and are forecast to expand at a 5.44% CAGR between 2026-2031.

- By resin type, epoxy-based had a share of 49.52% in 2025 and is expected to grow with a CAGR of 4.91% during the forecast period (2026-2031).

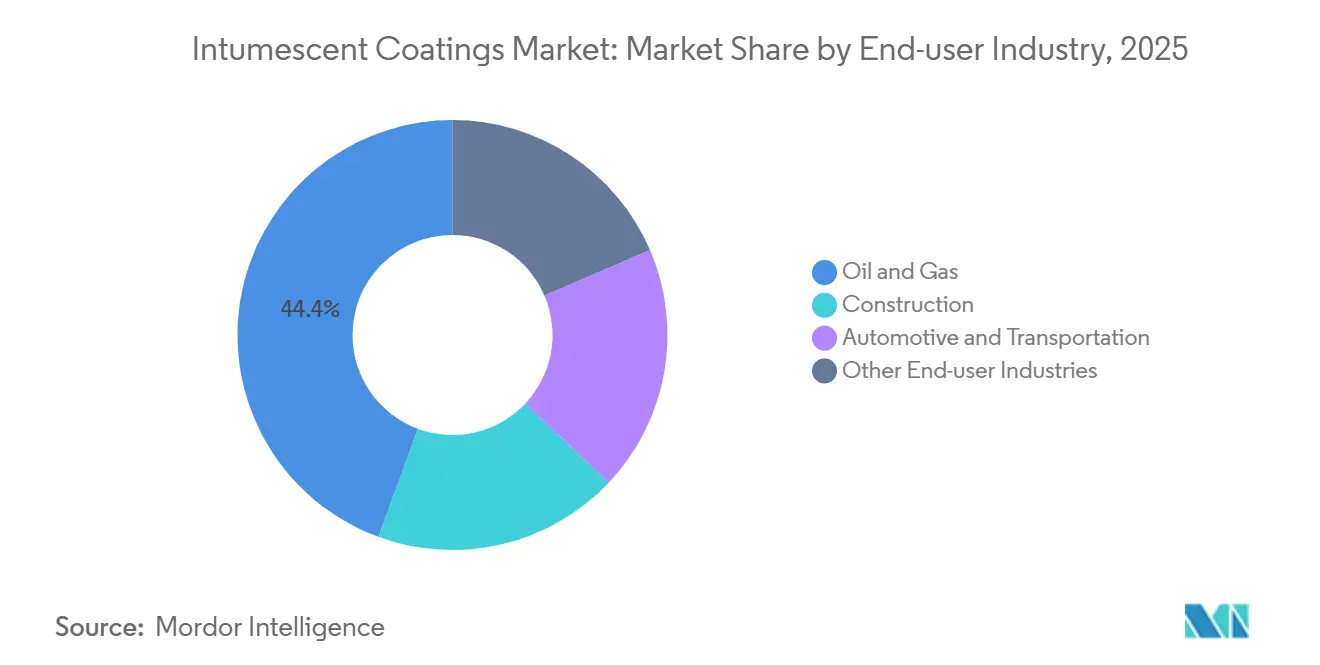

- By end-user, oil and gas held a 44.41% share of the intumescent coatings market size in 2025, and construction is projected to grow at a 4.95% CAGR through 2031.

- By geography, Asia-Pacific accounted for 35.55% of the intumescent coatings market size in 2025, outpacing other regions at a 5.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intumescent Coatings Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated High-Rise Fire Codes in Asia-Pacific | +0.8% | Asia-Pacific core (China, India, Southeast Asia); spillover to Middle East | Medium term (2-4 years) |

| Growth in Oil & Gas Exploration Activities | +0.7% | Global, with concentration in Middle East, Asia-Pacific, and offshore North America | Short term (≤ 2 years) |

| EU Low-VOC Mandate Boosting Water-Borne Formulations | +0.6% | Europe primary; North America and Asia-Pacific adoption following | Long term (≥ 4 years) |

| Modular Off-Site Steel Fabrication in North America | +0.5% | North America, with emerging adoption in Europe and Asia-Pacific | Medium term (2-4 years) |

| Advent of Nano-Engineered Char-Formers for Ultra-Thin Films | +0.4% | Global, led by Europe and North America; premium segment in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated High-Rise Fire Codes in Asia-Pacific

China and India now require intumescent protection for structural steel above 15 meters, a rule that covers most new urban towers and many retrofits. Singaporean and Australian standards have followed, so developers pre-qualify only suppliers that hold EN 13381 or AS 1530 approvals, raising entry barriers for smaller regional formulators[1]Singapore Civil Defence Force, “Fire Code 2024,” scdf.gov.sg. Large multinationals, therefore, consolidate shares by combining global certificates with local technical service. Market volumes also benefit when maintenance codes extend obligations to existing buildings under renovation, doubling retrofit demand without new construction.

Growth in Oil & Gas Exploration Activities

Liquefied-natural-gas terminals and petrochemical complexes across Saudi Arabia and Southeast Asia specify four-hour hydrocarbon ratings that only epoxy-based systems can meet. Capital expenditure in energy and utilities is rising, so formulators keep dual product lines for both hydrocarbon and cellulosic needs. This two-speed pattern locks high margins in upstream installations even as water-borne products gain share elsewhere. Specifiers accept higher volatile-organic-compound levels because safety codes override green-building priorities in process plants[2]Clariant Ltd., “High Performance Additives for Intumescent Coatings,” clariant.com.

EU Low-VOC Mandate Boosting Water-Borne Formulations

Revised European rules and impending PFAS limits force a shift from solvent-based chemistry to water-borne alternatives that already grow faster than the overall intumescent coatings market. New epoxy systems such as Hempafire Extreme 550 meet four-hour ratings with thinner films and zero solvent emissions, but they require humidity-controlled curing bays that only large contractors can finance. Suppliers therefore bundle training and equipment packages to help applicators transition, capturing service revenue and strengthening account stickiness.

Modular Off-Site Steel Fabrication in North America

Factory-applied coatings gain popularity as modular builders seek schedule certainty in data-center and power projects. Controlled environments improve film uniformity and reduce rework, but they also transfer purchasing power from field contractors to fabricators that negotiate bulk supply contracts. Manufacturers respond by embedding technicians in panel lines and integrating Building Information Modeling data to prove as-built fire protection, a capability unattainable for smaller regional brands.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Epoxy Resin Price Volatility | -0.6% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Competition from Alternative Methods | -0.5% | Global, especially cost-sensitive retrofits | Medium term (2-4 years) |

| Skilled-Applicator Shortage | -0.3% | Emerging Asia-Pacific, Middle East, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Epoxy Resin Price Volatility

Spot prices for bisphenol-A and epichlorohydrin moved in opposite directions during 2025, unsettling cost forecasts and complicating fixed-price bids. European anti-dumping duties on Chinese epoxy raise local procurement costs further, so only large producers with supply contracts or partial backward integration can defend margins. Smaller formulators delay R&D spending, which widens the technology gap and hastens consolidation.

Competition from Alternative Fire-Protection Methods

Gypsum board, mineral wool, and spray-applied fire-resistive materials undercut intumescent coatings on first cost when 60-minute ratings suffice. Architects often choose boards for concealed steel in budget-constrained projects, reserving coatings for architecturally exposed sections. The outcome is slower share gain for coatings compared with the broader passive-fire-protection segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Hydrocarbon Gains as LNG Projects Multiply

Cellulosic application had a share of 53.27% in 2025, and cellulosic products compete on aesthetics and low volatile-organic-compound profiles inside commercial buildings. Suppliers that maintain dual certification for UL 1709 and EN 13381 win contracts in mixed-use industrial campuses, securing bundled warranties and simplifying procurement. Hydrocarbon systems grew faster at 5.18% CAGR because liquefied-natural-gas terminals and petrochemical plants demand four-hour protection that cellulosic coatings cannot deliver. The intumescent coatings market size for hydrocarbon projects is projected to expand steadily through 2031 as Saudi Arabia’s energy construction alone reaches USD 46.5 billion.

Second-order effects reinforce divergence. Hydrocarbon coatings command higher margins because specialized resins and additives raise formulation cost, but procurement volumes are lumpy and tied to capital-expenditure cycles. Cellulosic volumes flow more consistently with residential and office construction, yet price pressure is intense. Together, these dynamics create balanced portfolio exposure for diversified producers, cushioning downturns in either sector.

By Technology: Water-Based Systems Ride Regulatory Tailwinds

Water-based coatings already control 40.36% revenue and are on a 5.44% CAGR trajectory as low-solvent mandates spread beyond Europe. The intumescent coatings market share for solvent-free epoxies increases when owners pursue green-building credits, although ambient-temperature limits still favor solvent products in cold or humid climates. Single-coat solvent-free epoxies that reach 4 millimeters dry film in one pass now reduce application steps, a key advantage in off-site fabrication. Technology choice thus hinges less on fire performance and more on job-site logistics, climate, and sustainability scoring.

Suppliers hedge by offering all three chemistries, water, solvent, and solvent-free, backed by digital tools that calculate optimal film build under project-specific heat-transfer models. Contractors then select formulations that balance schedule, environmental targets, and life-cycle cost, an approach that limits technology lock-in and keeps cross-segment competition healthy.

By Resin Type: Epoxy Dominance Tested by Acrylic Innovation

Epoxy resins accounted for 49.52% of 2025 intumescent coatings demand, valued for their adhesion to steel, chemical resistance, and ability to form dense, stable char layers under fire exposure. Yet epoxy's dominance faces pressure from raw-material volatility and regulatory scrutiny of bisphenol-A, a precursor classified as a substance of very great concern under REACH. Epoxy's 4.91% CAGR during 2026-2031, though trailing water-based technology growth, reflects its irreplaceability in hydrocarbon applications and offshore platforms where mechanical strength and chemical resistance are non-negotiable.

Acrylic resins, though holding smaller share, are gaining traction in water-based cellulosic formulations where flexibility and tintability matter more than hydrocarbon-fire performance. Polyurethane resins serve niche applications requiring abrasion resistance and UV stability, such as exposed structural steel in coastal environments, while alkyd resins persist in legacy retrofit projects where compatibility with existing coatings outweighs performance optimization.

By End-User Industry: Construction Overtakes Oil & Gas Growth

Oil and gas commanded 44.41% of 2025 intumescent coatings demand, driven by offshore platform maintenance, refinery turnarounds, and liquefied natural gas terminal expansions across the Middle East and Asia-Pacific. Yet construction is the fastest-growing end-user at 4.95% CAGR, propelled by high-rise residential projects in India and China, data-center construction in North America (up 34% in 2025), and Saudi Arabia's Vision 2030 infrastructure pipeline valued at over USD 1.25 trillion. This growth-rate inversion signals a structural shift: while oil and gas provide stable, high-margin demand for specialized hydrocarbon coatings, construction offers volume growth and geographic diversification that reduce supplier dependence on cyclical energy-sector capital expenditure.

Automotive and transportation, though smaller end-users, merit attention for their regulatory influence. Wildland-urban interface codes in California and Australia now mandate intumescent strips in roof vents and eave assemblies to prevent ember intrusion, creating a retrofit market for residential fire protection that extends beyond structural steel. The International Wildland-Urban Interface Code 2024 edition specifies Class 1 ignition-resistant ratings for assemblies in high-risk zones, driving demand for thin-film intumescent coatings that preserve architectural finishes while meeting performance thresholds.

Geography Analysis

Asia-Pacific generated 35.55% of global revenue in 2025 and leads growth at 5.86% CAGR through 2031 because tighter building codes now mandate intumescent protection in most high-rise projects. Factory-applied coatings in China’s modular construction exports add a new demand stream independent of domestic housing cycles. India’s retrofit obligation under SP 73:2023 further enlarges the addressable base for water-based cellulosic products.

North America’s 2025 sales were lifted by a 34% surge in data-center construction and steady 5-6% gains in power-sector capital spending. Fabricators have grown into dominant buyers who expect bulk discounts and integrated digital documentation, prompting suppliers to invest in plant-floor technical teams and Building Information Modeling plugins.

Europe, the Middle East, and South America share the remaining market value. European sales favor water-borne and solvent-free epoxies because of PFAS restrictions and volatile-organic-compound caps, while anti-dumping tariffs on Asian epoxy intensify local cost inflation. Middle Eastern megaprojects valued at more than USD 1 trillion require ultra-low-solvent systems that cure in 40°C desert environments, restricting qualified suppliers to a handful of multinationals. South America remains smaller and cyclical, but Brazilian offshore investments keep a niche hydrocarbon segment intact.

Competitive Landscape

The Intumescent Coatings market is moderately concentrated. Sherwin-Williams, PPG Industries, AkzoNobel, and RPM International headline the field on the strength of broad certification portfolios and global service networks. BASF’s planned coatings divestiture indicates that diversified chemical companies may exit lower-margin niches, while RPM’s acquisitions show a trend toward vertical integration into fabrication services. Smaller entrants aim to break through with bio-based epoxy precursors and melamine-free ammonium polyphosphate blends that clear REACH thresholds. High certification costs and liability exposure continue to shield incumbents from fast follower threats.

Intumescent Coatings Industry Leaders

Jotun

The Sherwin-Williams Company

PPG Industries Inc.

Hempel A/S

Akzo Nobel N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Huntsman International LLC launched a new intumescent polyurethane coating system developed for automotive applications, which can provide passive fire protection to metal and composite substrates used in electric vehicles (EVs).

- July 2024: Hexion Inc. and Clariant partnered to develop advanced intumescent coatings, combining Hexion's VeoVa vinyl ester-based binders with Clariant's additives to enhance fire protection systems.

Global Intumescent Coatings Market Report Scope

The intumescent coating layer expands and produces a 'char,' which insulates the material inside from flames by cutting off the oxygen necessary for combustion. Due to these properties, intumescent is used as a coating material to protect substances from heat and fire damage.

The intumescent coatings market is segmented by application, technology, resin type, end-user industry, and geography. By application, the market is segmented into cellulosic and hydrocarbon. By technology, the market is segmented into solvent-based, water-based, and epoxy-based. By resin type, the market is segmented into epoxy, acrylic, polyurethane, alkyd, and other resins. By end-user industry into construction, automotive and other transportation, oil and gas, and other end-user industries. The report also covers the market size and forecast for the intumescent coatings market in 16 countries across major regions. For each segment, the market sizing and forecast have been done based on value (USD).

| Cellulosic |

| Hydrocarbon |

| Solvent-Based |

| Water-Based |

| Epoxy Based |

| Epoxy |

| Acrylic |

| Polyurethane |

| Alkyd |

| Other Resins |

| Construction |

| Oil & Gas |

| Automotive & Transportation |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Cellulosic | |

| Hydrocarbon | ||

| By Technology | Solvent-Based | |

| Water-Based | ||

| Epoxy Based | ||

| By Resin Type | Epoxy | |

| Acrylic | ||

| Polyurethane | ||

| Alkyd | ||

| Other Resins | ||

| By End-user Industry | Construction | |

| Oil & Gas | ||

| Automotive & Transportation | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is demand for intumescent coatings growing in Asia-Pacific?

Regional revenue is rising at a 5.86% CAGR to 2031 on the back of stricter fire codes in China and India.

Which application is expanding quickest?

Hydrocarbon coatings post a 5.18% CAGR because LNG terminals and petrochemical plants require four-hour fire ratings.

Why are water-based intumescent products gaining share?

EU low-VOC rules and green-building labels push specifiers toward solvent-free options that now grow at 5.44% annually.

What limits adoption in emerging markets?

A shortage of skilled applicators and volatile epoxy prices slow penetration despite strong construction growth.

Who are the leading global suppliers?

Sherwin-Williams, PPG, AkzoNobel, RPM International, and Hempel collectively hold close to two-thirds of global sales.

What is the current market size of Intumescent Coatings Market?

The Intumescent Coatings Market size is projected to be USD 1.37 billion in 2025, USD 1.42 billion in 2026, and reach USD 1.74 billion by 2031, growing at a CAGR of 4.14% from 2026 to 2031.

Page last updated on: