Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 44.92 Trillion |

| Market Size (2026) | USD 46.87 Trillion |

| Market Size (2031) | USD 58.02 Trillion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Wealth Management Market Analysis by Mordor Intelligence

The Europe wealth management market size is expected to grow from USD 44.92 trillion in 2025 to USD 46.87 trillion in 2026 and is forecast to reach USD 58.02 trillion by 2031 at 4.35% CAGR over 2026-2031. This growth path positions the European wealth management market as the financial backbone of the continent’s push toward a deeper Capital Markets Union, with wealth managers increasingly functioning as conduits that redirect household savings into long-term capital‐market instruments [1]European Central Bank, “Household Sector Report,” ecb.europa.eu. Strong demand for ESG-aligned portfolios, accelerated shifts into technology-enabled advisory models, and the full rollout of the Markets in Crypto-Assets (MiCA) framework are reshaping product suites, operating cost structures, and competitive dynamics. Regulatory harmonization, especially under the Sustainable Finance Disclosure Regulation (SFDR) and the Distributed Ledger Technology (DLT) pilot, is encouraging product innovation while simultaneously pushing smaller players toward consolidation as compliance costs rise. Household cash deposits of EUR 13.9 trillion remain a vast pool of under-allocated capital that wealth managers aim to migrate into investment products through open-finance capabilities. Operating margins, however, face pressure from MiFID II fee transparency, an aging advisor workforce, and higher cybersecurity spending tied to the Digital Operational Resilience Act (DORA).

Key Report Takeaways

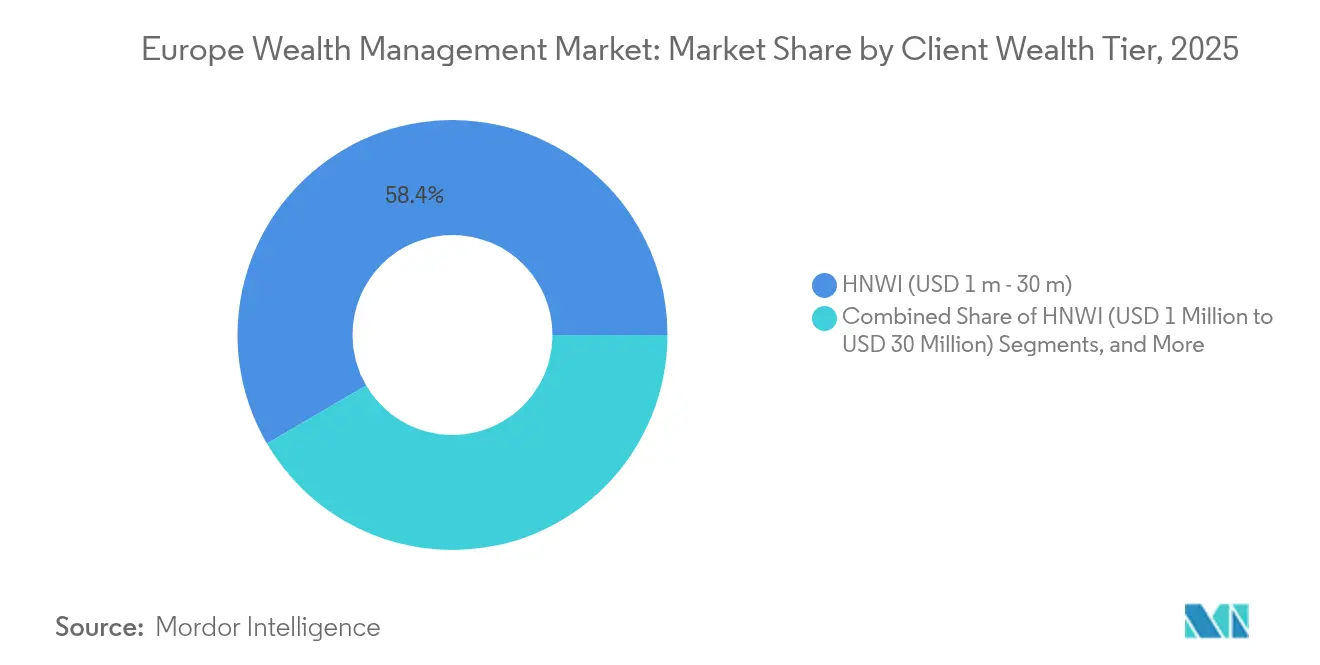

- By client wealth tier, high-net-worth individuals commanded 58.42% of Europe's wealth management market share in 2025, while the ultra-high-net-worth cohort is projected to grow at 6.98% CAGR to 2031.

- By mode of advisory, human advice retained an 85.47% share of the European wealth management market size in 2025, whereas robo-advisory solutions are advancing at a 15.42% CAGR through 2031.

- By firm type, private banks led with a 53.11% share of the European wealth management market in 2025; family offices are forecasted to expand at a 6.45% CAGR through 2031.

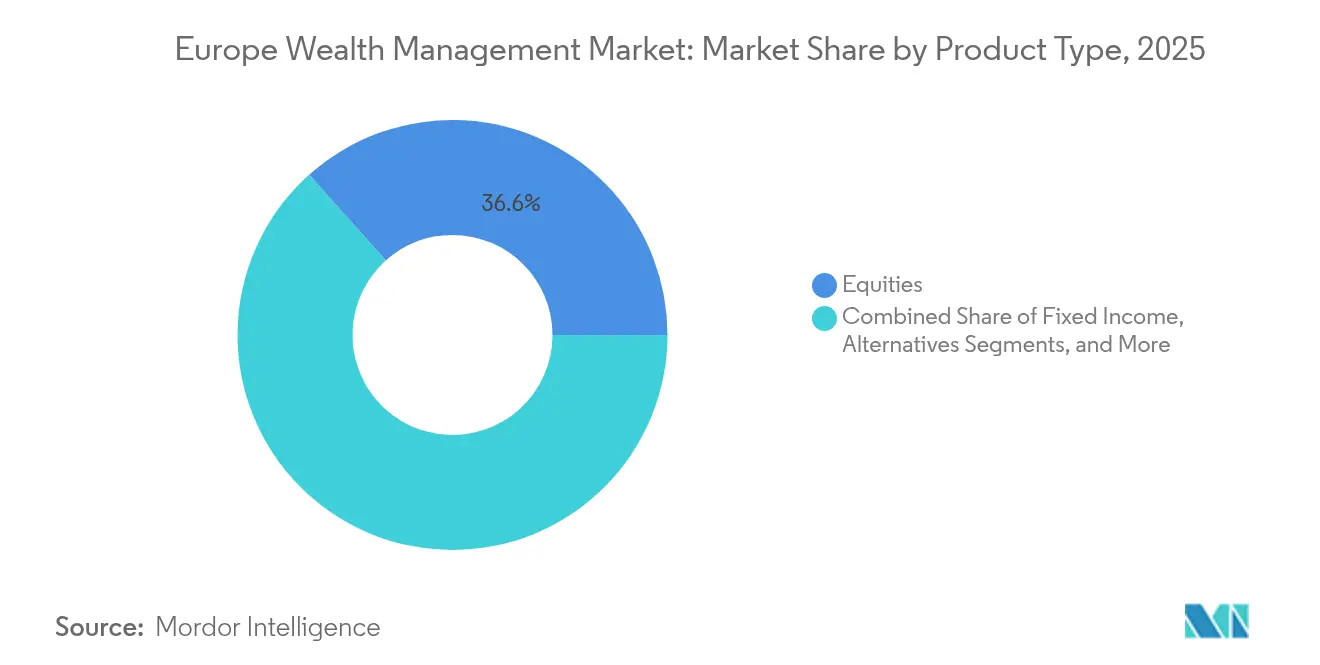

- By product group, equities held 36.62% of the European wealth management market size in 2025, yet alternative investments are expected to post the strongest 6.89% CAGR to 2031.

- By management source, onshore accounted for 75.21% of the European wealth management size in 2025 and are expected to expand at a 6.73% CAGR through 2031.

- By geography, the United Kingdom accounted for 21.32% of the European wealth management market in 2025, while Spain is on track to register the highest 5.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Wealth Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rebound in European HNWI AUM post-2024 | +0.8% | UK, Germany, France | Short term (≤ 2 years) |

| EUR 1.6 trillion Great Wealth Transfer | +1.2% | Western Europe, Nordics | Medium term (2-4 years) |

| Hybrid & robo-advisory cost reductions | +0.6% | Germany, France, Nordics | Medium term (2-4 years) |

| EU DLT-pilot tokenized private-market access | +0.4% | Luxembourg, Netherlands, Germany | Long term (≥ 4 years) |

| SFDR Level-2 premium ESG fee pools | +0.7% | EU-wide, strongest in Germany, France | Short term (≤ 2 years) |

| EUR 14 trillion cash deposit migration | +0.9% | Euro-area, led by Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rebound in European HNWI AUM post-2024

Net new money inflows rebounded in 2024 as improving fixed-income yields and stabilizing equity markets restored client confidence, lifting fee income and freeing capital for technology upgrades. Higher asset values particularly benefit private banks and family offices because concentrated portfolios naturally carry higher advisory margins. This momentum is allowing firms to accelerate hiring in tax planning, succession, and alternative-investment teams, thereby strengthening client retention. Active management regained traction after underperformance in 2022-2023, reversing fee compression caused by passive funds. The durability of this rebound will depend on moderate inflation, stable interest-rate expectations, and disciplined cost control across front-office and compliance functions.

EUR 1.6 trillion Great Wealth Transfer to Millennials & Women by 2030

Europe’s intergenerational transfer is reshaping service models as beneficiaries demand digital-first engagement, ESG integration, and direct investment opportunities[2]Henley & Partners, “Global Wealth Migration Report 2025,” henleyglobal.com. Wealth managers who deploy educational content and transparent fee frameworks are already improving the retention of next-generation heirs. Female inheritors, who receive a rising share of the transferred assets, are placing a higher value on planning clarity, catalyzing the launch of women-led advisory teams. Incumbent firms face elevated churn risk—millennials switch providers more readily—yet that risk unlocks acquisition opportunities for agile competitors offering personalized impact-oriented portfolios. To capture the flow, providers are widening their multi-family-office offerings and deepening digital engagement so that heirs can toggle between human advice and self-directed tools without friction.

Hybrid & Robo-Advisory Adoption Cuts Advice Costs 30–50%

Hybrid architectures that marry automated portfolio algorithms with human oversight are now firmly established in Germany and France, producing 30-50% cost savings versus purely human models. Robo engines handle portfolio drift checks, risk scoring, and rebalancing triggers, elevating service consistency and freeing relationship managers to focus on tax and estate complexities. Client acceptance has risen sharply because intuitive mobile dashboards demystify portfolio performance and fee breakdowns. Mass-affluent households gain institutional-grade diversification for far lower minimums, expanding the total addressable market. Implementation success hinges on robust data integration between core banking platforms and front-office portals so that advisors can convert automated insights into actionable recommendations during client meetings.

EU DLT-Pilot Regime Spurs Tokenized Private-Market Access

Luxembourg and the Netherlands are spearheading tokenized fund launches that fractionalize private equity and infrastructure stakes, letting high-net-worth clients gain exposure with ticket sizes as low as EUR 10,000[3]EY Luxembourg, “DLT Pilot Regime Readiness,” ey.com. Blockchain-based issuances improve settlement speed and secondary liquidity, addressing traditional illiquidity concerns. Early movers are packaging multi-strategy vintages that combine European mid-market buyouts, real estate, and renewables into tokenized share classes. Wealth managers earn structuring fees plus ongoing administration income, counterbalancing margin pressure in core portfolios. Adoption remains contingent on client education and vendor interoperability, but the regulatory sandbox has removed legal uncertainty that previously deterred large custodians.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fee-compression from MiFID II & passives | −0.9% | EU-wide, strongest in Germany, France | Short term (≤ 2 years) |

| Relationship-manager talent shortage | −0.6% | UK, Germany, Switzerland | Medium term (2-4 years) |

| Regulatory grey zones under MiCA | −0.3% | EU-wide, varying national rollout | Short term (≤ 2 years) |

| Escalating cyber & AI-model risk compliance | −0.5% | Global, highest in systemically important institutions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fee-Compression from MiFID II & Passives

MiFID II’s granular cost disclosures have heightened client sensitivity to advisory charges, while the surge in low-cost ETFs has eroded active-management fee headroom. Research-bundling prohibitions force wealth managers to fund analyst coverage independently, squeezing margins. Private banks counter by spotlighting tax optimization, succession planning, and access to private-market deals that ETFs cannot replicate, but these services demand higher advisor skill sets and digital tooling. Price transparency also limits cross-selling of non-portfolio banking products, tightening overall wallet share. Consequently, firms are migrating from traditional asset-based fees toward blended retainers linked to planning complexity and outcome metrics.

Relationship-Manager Talent Shortage & Ageing Advisor Base

More than 30% of European relationship managers are expected to retire within five years, yet graduate pipelines remain thin as younger professionals gravitate toward fintech roles with faster equity upside. The resulting talent gap jeopardizes the continuity of high-touch client relationships that underpin loyalty and referral flows. Wealth managers are deploying mentorship programs and accelerated certification tracks, but visa restrictions and international mobility hurdles complicate cross-border hiring. Compensation inflation further compresses profitability, especially within mid-tier Swiss banks that face head-to-head competition with London boutiques. Firms increasingly invest in digital self-service portals to relieve advisors of routine tasks, yet many clients still insist on personal counsel for complex decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Client Wealth Tier: UHNWI Growth Outpaces Mass Market

In 2025, high-net-worth individuals captured 58.42% of Europe's wealth management market share, reflecting a broad base of professionals and entrepreneurs benefiting from the post-pandemic recovery. The ultra-high-net-worth segment holds the fastest trajectory at a 6.98% CAGR, propelled by liquidity events in technology, healthcare, and renewable infrastructure ventures. The European wealth management market size linked to UHNWI clients is expected to climb steadily as their demand for bespoke direct investments and philanthropy structures boosts advisory revenue density. Wealth concentration favors private banks and multi-family offices that supply customized lending and co-investment opportunities.

UHNWI clients exhibit a higher willingness to pay for multi-jurisdictional estate plans, impact investing vehicles, and private-equity co-investment gates unavailable to retail investors. Family offices are leveraging that demand by extending in-house deal origination desks. Mass-affluent households, by contrast, remain price sensitive and gravitate toward robo platforms that parcel diversified model portfolios at sub-50-basis-point fees. Successful providers, therefore, tier their service stack: algorithmic allocation for mass-affluent clients, hybrid advice for the upper affluent, and specialist verticals for UHNWI families.

By Mode of Advisory: Digital Transformation Accelerates

Human advisers still commanded 85.47% of the European wealth management market size in 2025, but robo engines are amplifying reach among younger investors who favor transparent fee grids and mobile engagement. The segment’s 15.42% CAGR underscores persistent demand for low-cost automation complemented by selective human touchpoints. The European wealth management market continues to integrate hybrid models that embed automated tax-loss harvesting and ESG scoring while reserving relationship managers for complex credit, philanthropy, and inheritance tasks.

Pure robo players struggle with client acquisition costs, pushing them toward B2B partnerships with incumbent banks that white-label portfolios. Meanwhile, incumbent private banks retrofit legacy architectures with open-API layers, enabling advisors to generate on-demand proposals during virtual sessions. The migration toward hybrid advice lowers operating costs by trimming routine portfolio rebalancing workflows and reallocating human capital toward higher-margin strategic conversations.

By Firm Type: Family Offices Challenge Traditional Models

Private banks retained 53.11% share of the European wealth management market in 2025, leveraging broad product shelves and regulatory expertise. Yet family offices are projected to expand at a 6.45% CAGR as wealth creators seek direct control over governance, asset allocation, and philanthropic mandates. The European wealth management market size booked through single- and multi-family offices is projected to rise sharply because these entities can underwrite co-investments and club deals without intermediation fees.

Independent asset managers also gain traction by aligning remuneration to performance hurdles rather than asset-based fees, resonating with price-conscious heirs. Private banks counter by establishing dedicated family-advisory units that bundle concierge services, thematic impact portfolios, and succession consultants. Regulatory capital rules, however, restrict the flexibility of bank-owned product manufacturing, leaving room for non-bank firms to differentiate.

By Product Type: Alternatives Drive Premium Growth

Equities accounted for 36.62% share of the European wealth management market in 2025 on the back of a strong post-pandemic rally, yet alternative investments show the greatest upside with a 6.89% CAGR to 2031. The European wealth management market size attributed to real estate, private credit, and infrastructure vehicles is rising as clients pursue inflation protection and uncorrelated returns. Tokenization under the EU DLT pilot reduces the minimum ticket for such strategies, broadening access among upper-affluent investors.

Private-market allocations earn higher advisory and performance fees, insulating providers from MiFID-II price compression. Hedge-fund interest is resurging as rate volatility fuels macro and relative-value strategies. Cash allocations are receding as open banking nudges households into higher-yielding instruments. Within traditional fixed income, duration-barbell approaches attract flows, exploiting diverging central-bank policy paths across the euro area and the UK.

By Management Source: Onshore Dominance Reflects Regulatory Trends

Onshore segment held 75.21% share of the European wealth management market in 2025 and exhibits a 6.73% CAGR outlook. The European wealth management market’s shift toward onshore booking is driven by automatic exchange-of-information (AEOI) treaties and tighter anti-money-laundering scrutiny that erode offshore secrecy advantages. Luxembourg and Ireland thrive as “regulated onshore hubs” combining EU passporting certainty with efficient tax treaty networks.

Offshore strongholds such as the Channel Islands respond by emphasizing substance requirements, fiduciary expertise, and bespoke trustee services. Wealth managers now pitch onshore structures as risk mitigants that shield families from reputational harm while preserving planning flexibility. Cross-border advisers must therefore master a patchwork of tax regimes and reporting standards without compromising operational scalability.

By Country: Spain Emerges as Growth Leader

The United Kingdom remains the largest single market with a 21.32% share of the European wealth management market in 2025, thanks to London’s legal system, capital-market depth, and global connectivity, even as outbound millionaire migration picks up. Spain’s 5.74% CAGR through 2031 is powered by advantageous non-resident tax regimes and residency pathways that lure mobile wealth from Northern Europe. Meanwhile, Germany and France provide stable fee pools anchored in entrenched private-banking relationships and robust domestic wealth creation.

Benelux jurisdictions ride on Luxembourg’s fund-servicing ecosystem, capturing cross-border mandates from multinational families. Nordic markets extend leadership in ESG adoption, aligning with regional sustainability values and advanced digital infrastructure. Southern European nations such as Portugal and Greece are accelerating via “Golden Visa” programs and favorable flat-tax regimes for new residents, contributing incremental asset inflows without displacing established hubs.

Geography Analysis

The United Kingdom, with a 21.32% share in 2025, remains the nucleus of the European wealth management market despite heightened wealth-tax discussions and ongoing post-Brexit regulatory adjustments. London’s professional-services cluster, liquid capital markets, and deep talent bench sustain international mandates, but firms are bolstering booking centers in Dublin and Luxembourg to mitigate equivalence risk. A net outflow of 16,500 millionaires projected for 2025 intensifies competition for domestic assets, prompting incumbent banks to enhance digital onboarding, cross-border lending, and non-domiciled tax planning support to protect revenue.

Germany displays resilient organic wealth creation via its Mittelstand exporters, generating steady fee income from family-owned enterprises seeking succession solutions. Local institutions leverage strong brand trust to expand ESG-labelled discretionary mandates, while global banks invest in Frankfurt desks that specialize in cross-border philanthropic structures. France offers similar characteristics but contends with higher wealth taxation, driving affluent residents to diversify booking centers within the EU. Domestic policy stability nonetheless underpins a large captive base for discretionary portfolio management and life-insurance wrappers.

Spain records the region’s fastest pace at 5.74% CAGR as favorable Beckham-law tax treatment and lifestyle advantages attract Northern European retirees and digital nomads. This inflow supports real-estate backed lending and bespoke visa advisory services that augment traditional portfolio fees. Luxembourg and the Netherlands consolidate their positions as structuring hubs, processing pan-European fund vehicles that feed into private-bank platforms. Nordic countries harness long-standing digital identity frameworks to roll out fully remote wealth-advisory journeys, catering to sustainability-focused households. Italy, Portugal, and Greece round out the opportunity set with investor-visa incentives and incremental liberalization of capital markets regimes.

Competitive Landscape

Europe’s wealth arena shows moderate concentration: the top five banking groups hold significant shares of assets, leaving scope for niche challengers. Recent megadeals, such as UBS’s integration of Credit Suisse and BNP Paribas’s purchase of HSBC’s German private-bank operations, demonstrate how scale economies in compliance and technology are becoming decisive. Integration agendas focus on harmonizing core banking systems, rationalizing overlapping booking centers, and extracting procurement savings. The European wealth management market, therefore, rewards organizations capable of rapid post-merger tech migration and culturally sensitive client communications.

Technology investment has moved from differentiator to baseline requirement: 74% of firms raised digital budgets during 2024 to comply with SFDR data capture, MiCA reporting, and DORA stress-testing mandates. ESG data aggregation, AI-driven client-risk profiling, and conversational banking bots constitute the most prevalent initiatives. However, each advancement raises cyber-threat exposure, compelling parallel growth in security spending that eats into efficiency gains. Mid-tier private banks lacking economies of scale in tech procurement are now prime targets for consolidation.

Family offices, external asset managers, and fintech robo advisers intensify competition by offering fee-transparent models and access to club deals. Large incumbents respond with semi-open architecture platforms that welcome third-party specialist funds while retaining core custody, lending, and treasury flows in-house. White-space opportunities persist around tokenized private-asset distribution, intergenerational wealth-transfer coaching, and ESG impact verification. Firms that master these capabilities, while preserving the human relationship element that underpins trust, stand to gain share as the market expands.

Europe Wealth Management Industry Leaders

UBS Group AG

JPMorgan Chase & Co.

BNP Paribas Wealth Management

HSBC Holdings

Allianz SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: EFG International agreed to acquire Geneva-based Cité Gestion, adding CHF 7.5 billion in AUM and enhancing its presence in the ultra-high-net-worth niche.

- February 2025: Lombard Odier reported AUM of CHF 215 billion for 2024, up 12%, although net profit slid 19% due to higher deposit costs.

- January 2025: BPCE and Generali signed an MoU to form a combined asset manager with EUR 1.9 trillion in AUM and €4.1 billion in revenue, pending approvals.

- November 2024: Swiss private banks Gonet & Cie and ONE Swiss Bank announced a merger that will manage CHF 12 billion in assets, pending FINMA clearance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European wealth management market as the total assets under management that private banks, family offices, external asset managers, and digital-first advisory platforms steward on behalf of mass-affluent, high-net-worth, and ultra-high-net-worth clients across 27 EU states, the United Kingdom, Norway, Switzerland, and Iceland. Assets include listed securities, alternatives, cash, and deposits that sit in discretionary or advisory mandates.

Scope exclusion: corporate treasury pools and institutional-only pension mandates are outside the study.

Segmentation Overview

- By Client Wealth Tier

- UHNWI (More than USD 30 Million)

- HNWI (USD 1 Million to USD 30 Million)

- Mass Affluent (Less than USD 1 Million)

- By Mode of Advisory

- Human Advisory

- Robo-Advisory

- By Firm Type

- Private Banks

- Family Offices

- Others (Independent/External Asset Managers)

- By Product Type

- Fixed Income

- Equities

- Alternatives

- Cash and Deposits

- Others

- By Management Source

- Offshore

- Onshore

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with relationship managers, digital-platform product heads, and former regulators across the United Kingdom, Germany, France, Italy, the Nordics, and Spain. Conversations clarified fee compression trends, robo-advice adoption, and typical client asset splits, allowing us to validate desk findings and tune model assumptions before final triangulation.

Desk Research

We began with macro data from tier-1 bodies such as the European Central Bank, Eurostat, the European Banking Authority, and the OECD, which provided headline household financial-asset stocks, saving flows, and cross-border holdings. Trade associations like EFAMA and the UK Investment Association helped us split fund and mandate assets by domicile. Company filings, investor presentations, and regulatory disclosures supplied firm-level AuM and fee yields, while press archives accessed through Dow Jones Factiva and balance-sheet intelligence from D&B Hoovers grounded competitive sizing. These sources illustrate our information base; many additional publications were reviewed to round out coverage.

Market-Sizing & Forecasting

We anchor 2024 AuM by aligning ECB household asset totals with EFAMA fund shares, then applying our proprietary penetration ratios to isolate privately advised wealth. A top-down construct is cross-checked with bottom-up roll-ups of sampled bank, family office, and fintech disclosures. Key variables like client migration between advisory modes, average account balances, equity-market performance, deposit rate shifts, and net new money drive the model. Forecasts to 2030 rely on multivariate regression that blends GDP per capita growth, MSCI Europe returns, and demographic aging indices validated during primary interviews. Gaps in bottom-up coverage, especially for smaller family offices, are bridged with region-specific fee-yield proxies.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated outlier screening, peer analyst cross-checks, and senior sign-off. We benchmark against fresh regulatory releases each quarter and trigger interim refreshes after material events. The full report is rebuilt annually, and one last accuracy sweep is completed immediately before client delivery.

Why Mordor's Europe Wealth Management Baseline Stands Firm

Published estimates often diverge because firms choose different asset buckets, currency bases, and refresh cadences.

Our disciplined scope and yearly rebuild narrow that spread.

Key gap drivers are scope creep into institutional assets, single-point currency translation, and infrequent updates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 44.92 T (2025) | Mordor Intelligence | |

| USD 35.70 T (2025) | Global Consultancy A | Bundles asset-management AuM with private wealth and relies on 2023 exchange averages |

| USD 36.70 T (2024) | Industry Association B | Includes discretionary institutional mandates and excludes offshore client assets |

| USD 43.02 T (2024) | Regional Publisher C | Uses earlier base year and models forward with linear equity growth, no primary validation |

Taken together, the comparison shows that Mordor's model balances detailed segmentation with timely primary insights, giving decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current size of the Europe wealth management market?

The market stands at USD 46.87 trillion in 2026 and is projected to reach USD 58.02 trillion by 2031.

Which client segment is expanding fastest?

Ultra-high-net-worth individuals segment is projected to grow at a 6.98% CAGR through 2031, outpacing all other wealth tiers.

How quickly are robo-advisory platforms scaling in Europe?

Robo solutions are advancing at a 15.42% CAGR as hybrid models cut advisory costs by up to 50%.

Why is Spain the fastest-growing European market?

Competitive tax regimes and residency incentives are drawing high-net-worth migrants, driving a 5.74% CAGR through 2031.

What regulatory changes most influence product innovation?

The SFDR Level-2 rules and the EU DLT-pilot regime are spurring growth in ESG-labelled funds and tokenized private-market offerings.

How are compliance costs affecting smaller firms?

DORA and MiCA requirements raise cybersecurity and reporting spend, pushing sub-scale boutiques toward consolidation or strategic partnerships.

Page last updated on: