Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

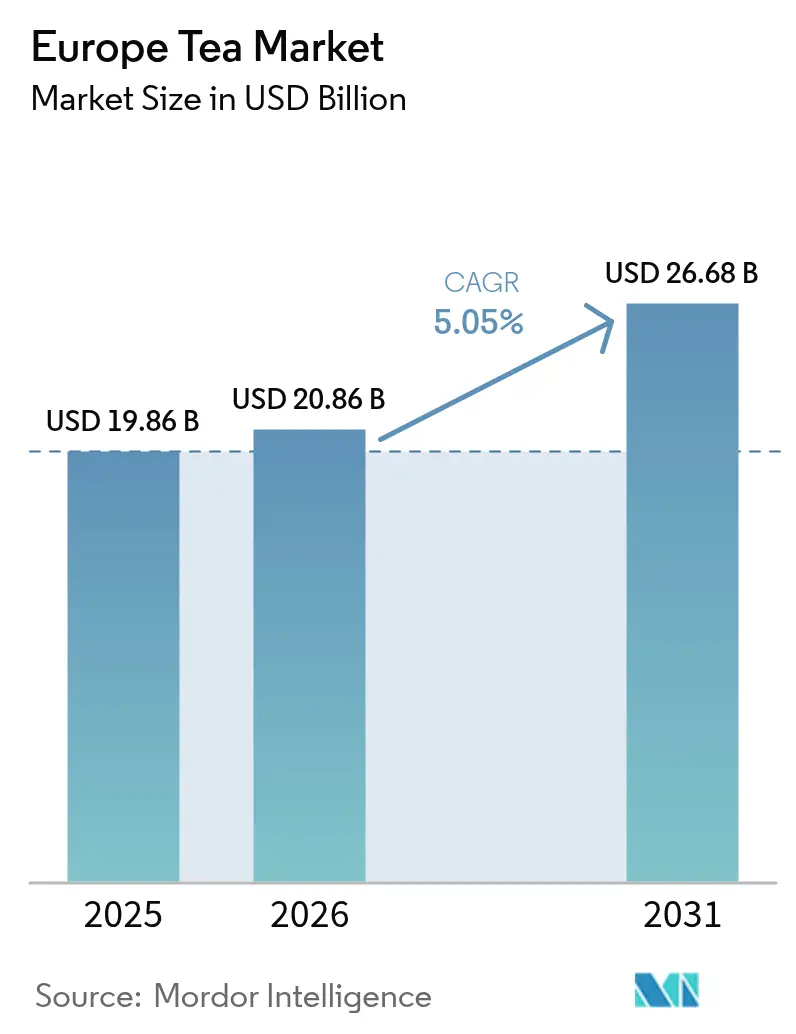

| Base Year Market Size (2025) | USD 19.86 Billion |

| Market Size (2026) | USD 20.86 Billion |

| Market Size (2031) | USD 26.68 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

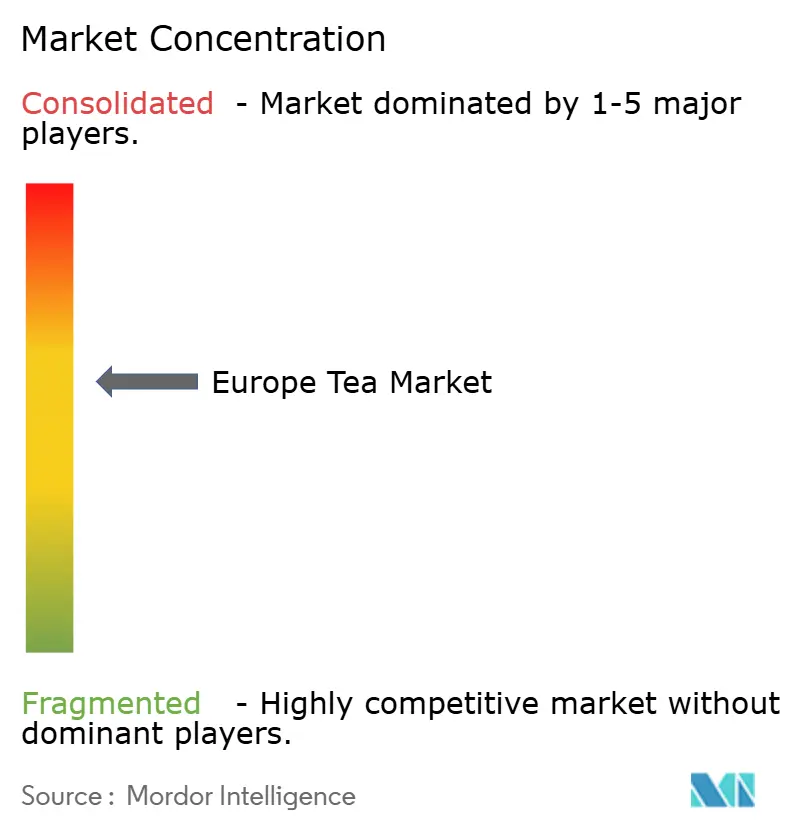

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Tea Market Analysis by Mordor Intelligence

The Europe tea market size is expected to grow from USD 19.86 billion in 2025 to USD 20.86 billion in 2026 and is forecast to reach USD 26.68 billion by 2031 at 5.05% CAGR over 2026-2031. The market is increasingly prioritizing value over volume, driven by trends like premiumization, sustainability certifications, and a focus on wellness. Consumers are showing a growing preference for high-quality, ethically sourced, and health-oriented tea products, which is reshaping purchasing patterns. E-commerce platforms are playing a pivotal role in enhancing access to niche tea offerings, enabling smaller brands to reach a broader audience. While Germany's demand is rooted in its rich cultural traditions and long-standing tea consumption habits, the UK is witnessing the quickest growth, especially with the rising popularity of specialty blends that cater to evolving consumer tastes. Climate change-induced supply chain disruptions and tighter residue regulations are nudging firms towards direct-sourcing models, benefiting those with stronger capital and robust supply chain networks. The competitive landscape is moderately intense, allowing both established players and newcomers to explore diverse categories and innovate within the European tea market.

Key Report Takeaways

- By form, leaf tea led with 61.88% of Europe tea market share in 2025; CTC tea is forecast to advance at a 7.18% CAGR through 2031.

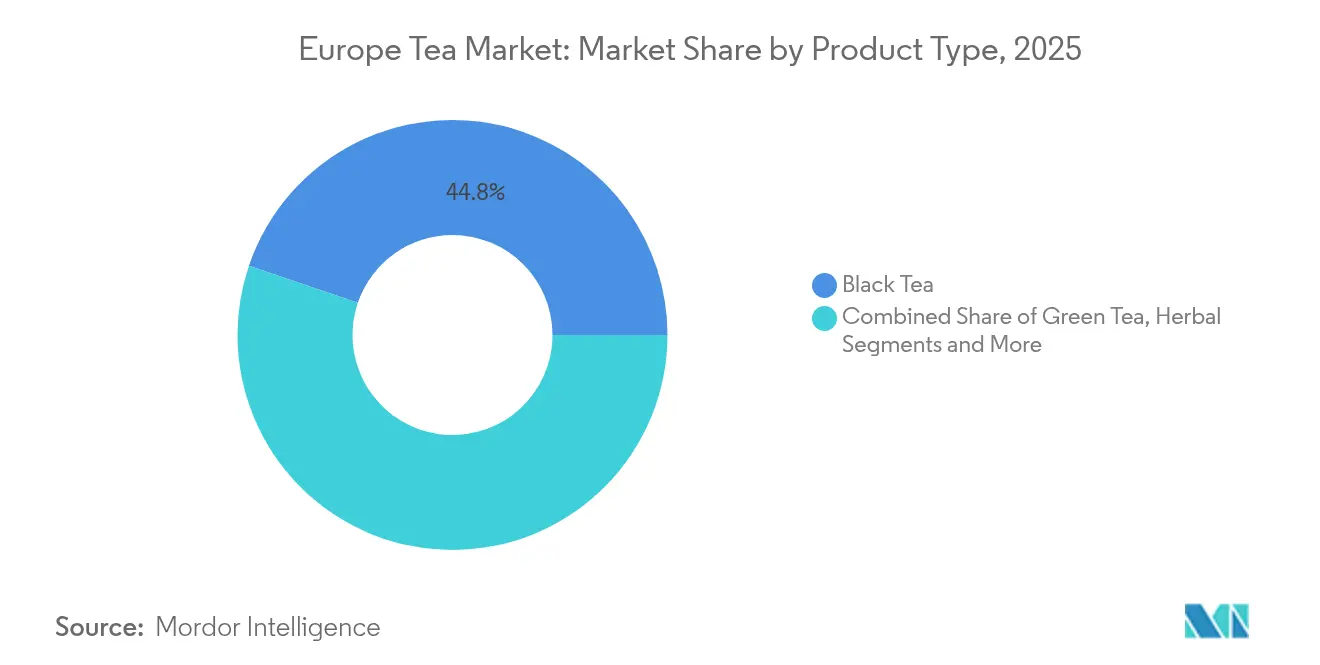

- By product type, black tea captured 44.78% of the Europe tea market size in 2025, while herbal tea is set to grow at an 8.56% CAGR to 2031.

- By category, conventional tea dominated with 84.05% revenue share in 2025, as organic tea accelerates at a 8.95% CAGR over the forecast span.

- By packaging type, box formats held 68.57% revenue share in 2025; pouches are predicted to progress at a 6.97% CAGR through 2031.

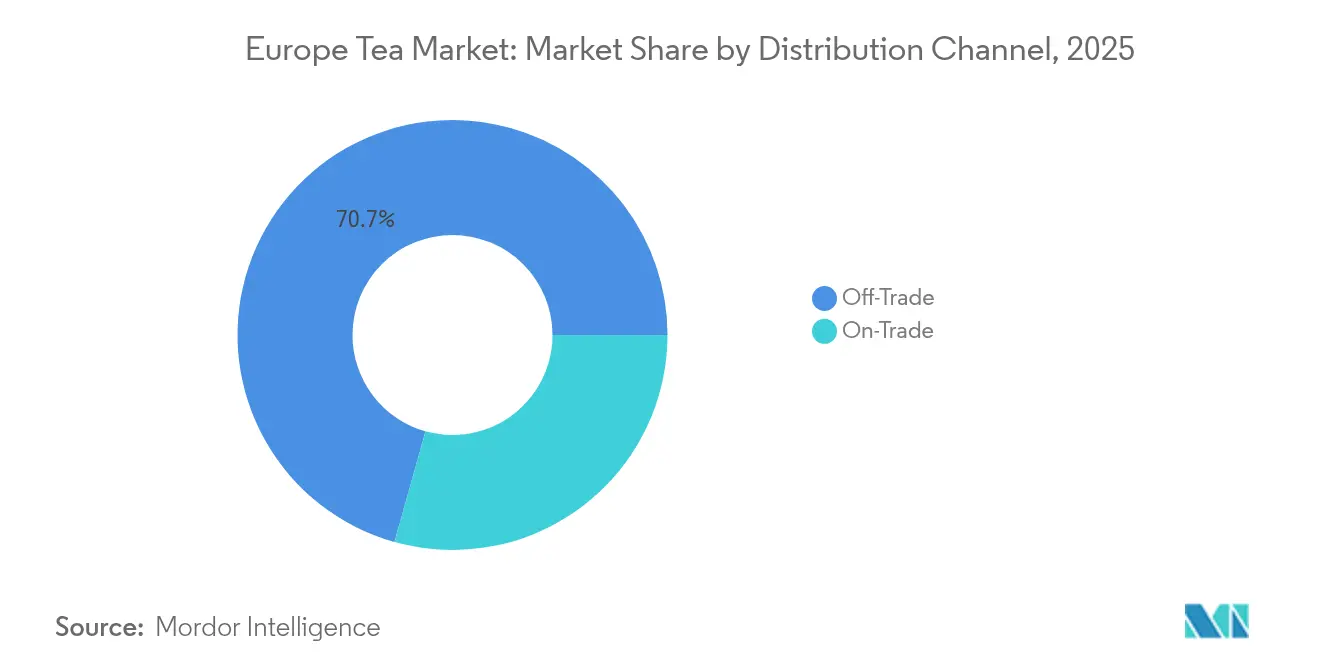

- By distribution channel, off-trade outlets controlled 70.65% of sales in 2025, whereas on-trade venues are expanding at an 8.79% CAGR as hospitality recovers.

- By geography, Germany held 24.06% of the Europe tea market share in 2025, while United Kingdom is forecast to grow at a 6.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Tea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and specialty-tea demand surge | +1.8% | Germany, UK, France, Netherlands | Medium term (2-4 years) |

| Rising demand for herbal and green teas | +1.2% | Germany, UK, Sweden, Netherlands | Long term (≥ 4 years) |

| Cultural significance and tea consumption habits | +0.8% | UK, Germany, Russia, Poland | Long term (≥ 4 years) |

| Cold-brew and RTD tea uptake | +0.9% | Germany, France, Netherlands, Sweden | Short term (≤ 2 years) |

| Sustainability and carbon-neutral certification targets | +0.7% | Germany, Netherlands, Sweden, France | Medium term (2-4 years) |

| E-commerce direct-to-consumer expansion | +0.6% | Germany, UK, France, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization and specialty tea demand surge

European consumers are increasingly willing to pay a premium for specialty tea experiences, shifting the market's value propositions away from traditional commodity views. This trend is particularly evident in Germany. In 2024, tea enthusiasts in Germany, as reported by the German Tea Association, consumed an average of 67.2 litres each. This total included 27.1 litres of traditional black and green teas, and a notable 40.1 litres of herbal and fruit infusions [1]Source: The German Tea Association, "Tea Report 2025", www.teeverband.de. Health-conscious consumers are now gravitating towards complex blends and high-quality teas. Brands that can authenticate their origin stories, processing methods, and sustainability credentials stand to benefit from this shift, creating opportunities for margin expansion. Single-estate European teas are emerging as specialty products. Comparative analyses highlight distinct flavor profiles between hot and cold brewing methods, catering to discerning consumer tastes. The premiumization trend isn't limited to product quality; it also spans packaging innovations, advanced brewing equipment, and experiential retail concepts. These developments position tea consumption as a lifestyle enhancement, rather than just a beverage choice.

Rising demand for herbal and green teas

In Europe, heightened health consciousness is fueling the demand for green and herbal teas. With non-communicable diseases, such as diabetes and heart ailments, on the rise, there's a pronounced shift towards healthier eating habits. In 2024, the International Diabetes Federation highlighted that around 66 million Europeans are contending with diabetes [2]Source: International Diabetes Federation, "The Diabetes Atlas- Data by Region", https://diabetesatlas.org. Known for their antioxidants and health advantages, green and herbal teas have surged in popularity. These teas are known to aid in weight management, improve digestion, and reduce the risk of chronic illnesses, making them a preferred choice among health-conscious consumers. Globally, governments and health entities champion these teas in their health initiatives. A case in point: the European Food Safety Authority underscores the cardiovascular perks of green tea polyphenols, advocating for their wider acceptance. Additionally, the growing trend of natural and organic products further supports the adoption of green and herbal teas. Given these dynamics, the green and herbal tea market is poised for growth in the coming years.

Cultural significance and tea consumption habits

Across Europe, deep-rooted cultural traditions foster a resilience in consumption that endures even through economic fluctuations. Tea, in particular, plays a multifaceted role – serving not just as a beverage, but as a centerpiece in ceremonies, social gatherings, and daily rituals. This is a nuance that coffee, in certain demographic segments, struggles to match. The British, with a tea culture deeply woven into their history, have seen its influence ripple through former colonial territories. Yet, even as these territories embrace tea, the British market showcases a unique characteristic: tea consumption patterns remain steadfast, largely independent of income fluctuations. In contrast, coffee's appeal seems more closely tied to income levels. Meanwhile, in Germany, tea culture isn't monolithic. East Frisian communities stand out, boasting per-capita consumption levels that not only underscore their passion for tea but also bolster a specialized retail landscape and open doors for premium product positioning. Over in Russia, tea isn't just a drink; it's a social glue. This cultural emphasis drives bulk purchases and a distinct preference for loose-leaf tea, sidelining the more convenient tea bag.

Sustainability and carbon-neutral certification targets

The Europe Tea Market is being driven by the increasing emphasis on sustainability and carbon-neutral certification targets. Tea producers and suppliers are actively adopting eco-friendly practices to meet these objectives, such as reducing carbon emissions during production, transitioning to renewable energy sources, and employing sustainable agricultural methods. Furthermore, companies are leveraging advanced technologies, including carbon footprint monitoring systems and energy-efficient equipment, to minimize their environmental impact. European governments and regulatory bodies are also playing a pivotal role by implementing strict policies and offering incentives to encourage sustainable practices across the tea industry. These efforts align with global environmental goals while addressing the rising consumer preference for ethically sourced and environmentally responsible tea products. As consumers increasingly favor brands committed to sustainability, market players are compelled to innovate and enhance their offerings to remain competitive. This shift is reshaping the market landscape in Europe, driving innovation, strengthening brand reputation, and supporting the long-term sustainable growth of the tea industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from coffee and RTD beverages | -1.1% | Germany, France, Netherlands, Italy | Short term (≤ 2 years) |

| Climate-change impact on tea yields | -0.8% | EU-wide across all countries | Medium term (2-4 years) |

| Regulatory scrutiny on pesticide residues | -0.4% | EU-wide, particularly Germany, France | Short term (≤ 2 years) |

| Labor shortage and ethical-sourcing compliance costs | -0.3% | EU-wide Supply chain impacts across all markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying competition from coffee and RTD beverages

In Europe, coffee's stronghold poses challenges for tea's growth, especially among younger consumers. These younger demographics often link coffee with productivity, social status, and a sophisticated lifestyle—associations that tea brands find hard to consistently mirror. While coffee has historically dominated continental Europe and tea has held sway in Britain, this divide is being challenged. The rise of specialty coffee culture and the boom of third-wave coffee shops are reshaping these traditional patterns. Meanwhile, ready-to-drink (RTD) beverages are evolving. They're now infused with functional ingredients, packaged for convenience, and marketed aggressively, positioning coffee and energy drinks as enhancers of performance rather than mere refreshment. Furthermore, coffee's consumption is closely tied to income, paving the way for a premium market expansion. Tea companies, however, find it challenging to tap into this luxury market without shifting their image from everyday consumption to one of luxury and exclusivity. In a bid to counter coffee's edge in convenience, the European teaware market is pivoting towards 'on-the-go' formats. But this shift demands hefty investments in supply chain and packaging, a strain that smaller tea companies often struggle to bear.

Climate-change impact on tea yields

Tea yields face challenges from climate change impacts, which act as a significant restraint in the Europe Tea Market. Changes in temperature, irregular rainfall patterns, and extreme weather events directly affect tea cultivation. These climatic variations lead to reduced productivity, altered quality, and increased vulnerability to pests and diseases. For instance, prolonged droughts or excessive rainfall can disrupt the growth cycle of tea plants, leading to lower yields and inconsistent quality. Additionally, rising temperatures can shift the optimal growing regions for tea, forcing producers to adapt to new environmental conditions or relocate plantations, which can be costly and time-consuming. Such disruptions not only increase production costs but also create supply chain uncertainties, impacting the availability of tea in the market. Furthermore, the increased prevalence of pests and diseases due to changing climatic conditions exacerbates the challenges faced by tea growers, as they must invest in additional pest control measures, further driving up costs. These factors collectively hinder the growth of the Europe Tea Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Leaf Tea Dominance Drives Premium Positioning

The tea leaf segment generated 61.88% of the overall tea market size in 2025, highlighting a strong consumer preference for authenticity and the traditional brewing ritual. Leaf tea is valued for its superior quality, versatility, and the premium experience it offers, especially to consumers who appreciate artisanal, loose-leaf varieties. This segment appeals primarily to those seeking genuine flavor profiles and engaging brewing processes, contributing to its dominance in the market. Additionally, leaf tea has environmental advantages by reducing packaging waste compared to pre-packaged tea bags, aligning well with the rising consumer demand for sustainability. Advanced brewing tools and equipment have also made leaf tea more accessible and convenient, broadening its appeal.

Conversely, the CTC (Crush, Tear, Curl) tea segment, though smaller in market share, is growing rapidly at a CAGR of 7.18%. This growth is largely driven by foodservice operators and commercial buyers who favor CTC tea for its quick extraction and robust flavor, which suits high-turn environments like cafes, restaurants, and hotels. CTC tea’s efficient brewing time allows foodservice establishments to serve customers faster without compromising on strength, making it a practical choice in busy settings. While it may not carry the same premium sentiment as leaf tea, CTC tea meets the demands of convenience and consistency, supporting steady expansion within a niche but important segment of the European tea market. Together, leaf tea and CTC tea serve distinct consumer and business needs, illustrating the diverse preferences that fuel Europe's evolving tea landscape.

By Product Type: Herbal Tea Disrupts Black Tea Hegemony

Black tea remained the dominant segment in the European tea market in 2025, holding a substantial market share of 44.78%. This enduring preference highlights black tea’s strong consumer loyalty, driven largely by its rich, robust flavor and classic appeal. It continues to be a staple in households and foodservice settings alike, often associated with traditional tea-drinking rituals and cultural heritage, particularly in countries like the UK and Germany. Black tea’s versatility allows it to be consumed plain or with additions such as milk, sugar, or lemon, catering to a broad range of taste preferences. Although innovation in black tea varieties and blends has slowed compared to specialty teas, it remains a dependable revenue generator given its entrenched position. The segment’s stability is also supported by well-established distribution channels and ongoing consumer demand for trusted, familiar products.

In contrast, the herbal tea segment, while smaller in market share, is the fastest-growing category in Europe, expanding at a remarkable CAGR of 8.56%. This rapid growth reflects a shifting consumer focus toward health and wellness, with buyers increasingly embracing herbal blends for their functional benefits such as relaxation, digestive health, and immunity support. Herbal teas often feature ingredients like chamomile, peppermint, ginger, and turmeric, which are celebrated for their natural therapeutic properties. The segment’s appeal is further boosted by rising consumer interest in caffeine-free alternatives and clean-label products with transparent sourcing. Additionally, innovative flavor combinations and convenient formats like ready-to-drink herbal teas have broadened the market’s reach. As a result, herbal tea is carving out a significant niche, attracting younger, health-conscious demographics and driving new opportunities for product development and market expansion within the European tea landscape.

By Category: Organic Surge Challenges Conventional Dominance

Conventional tea maintained a dominant position in the European tea market in 2025, accounting for 84.05% of total sales. This significant market share underscores the strong consumer preference for traditional tea offerings that have long-established brand recognition and widespread availability. Conventional teas benefit from extensive distribution networks and a broad range of products catering to various tastes and price points. Many consumers continue to choose these familiar options for their consistent quality and accessible pricing. While not necessarily seen as the most innovative segment, conventional tea remains a reliable revenue driver for major players. Its entrenched presence is supported by longstanding habits and preferences across different European regions, particularly in mature markets like Germany and the UK.

On the other hand, organic tea is the fastest-growing segment, expanding at an impressive CAGR of 8.95%. This growth is closely linked to increasing consumer demand for health-conscious and environmentally responsible products, as more buyers seek organic certifications and sustainable sourcing. The rise of carbon-neutral pledges by leading companies has further elevated the appeal of organic tea lines, aligning with broader climate and ethical consumption trends. Organic teas attract a niche yet rapidly expanding demographic that values purity, traceability, and reduced chemical usage in cultivation. Enhanced marketing efforts around organic and eco-friendly products, along with innovations in packaging and retail channels, are driving wider adoption across Europe. This dynamic signals a meaningful shift in consumer priorities and presents strong opportunities for brands to capitalize on sustainability-focused innovation in the tea market.

By Packaging Type: Innovation Challenges Traditional Formats

Boxes captured the largest share of the European tea market revenue in 2025, accounting for 68.57% of total sales. Their dominance is largely attributed to superior shelf visibility, which helps attract consumer attention in both physical retail and specialty stores. Boxes are also favored for their suitability as gifting options, often featuring attractive designs and premium packaging that enhance perceived value. This packaging format supports a wide variety of tea types, from everyday blends to luxury assortments, catering to diverse consumer preferences. Established distribution channels have helped boxes maintain their leading position, benefiting from shopper familiarity and ease of stacking and display. Additionally, boxes provide ample space for branding and detailed product information, which bolsters consumer trust and purchase decisions.

In contrast, pouches represent the fastest-growing packaging segment, expanding at a robust CAGR of 6.97%. This growth is driven by the rise of e-commerce and direct-to-consumer sales, where lightweight, space-efficient packaging is crucial for shipping cost optimization. Pouches also appeal to consumers who prioritize freshness and convenience, as many come with resealable features that help maintain the tea’s aroma and quality after opening. Their flexible format is ideal for a variety of tea blends, including premium loose-leaf and specialty products, catering to evolving consumer lifestyles focused on portability and ease of use. Innovations in pouch design have made them increasingly attractive in retail environments as well, offering distinctive shelf appeal with modern aesthetics. As digital sales continue to surge across Europe, pouches are expected to consolidate their market position by meeting the demand for sustainable, practical, and consumer-friendly packaging solutions.

By Distribution Channel: Digital Transformation Reshapes Retail Landscape

Off-trade channels dominated the European tea market in 2025, accounting for 70.65% of total revenue. This substantial share is primarily driven by the extensive reach of supermarkets and grocery stores, which offer convenience, broad product ranges, and competitive pricing. These retail outlets remain the preferred purchasing points for most consumers, supporting steady sales across various tea segments including conventional, organic, and specialty teas. Off-trade’s strength also comes from well-established distribution networks, promotional activities, and attractive shelf placement that enhance product visibility and accessibility. Furthermore, the rise of e-commerce within off-trade has contributed to maintaining this dominant position by catering to consumers valuing convenience and home delivery options.

In contrast, on-trade channels are the fastest-growing segment, expanding at a notable CAGR of 8.79%. This acceleration is fueled by the resurgence of experiential dining as consumers return to social and leisure activities post-pandemic. On-trade environments offer unique opportunities for premiumisation, brand engagement, and innovation through specialty and ready-to-drink tea offerings tailored to enhance the customer experience. The growth in on-trade also reflects strong demand for high-quality, functional, and artisanal teas that can be enjoyed in curated settings, amplifying brand exposure. Additionally, on-trade operators increasingly prioritize sustainability, ethical sourcing, and novel tea formats to meet evolving consumer expectations. This dynamic growth segment is vital for future market expansion, providing avenues for premium pricing and deeper consumer connections beyond traditional retail channels.

Geography Analysis

The European tea market in 2025 sees Germany as the clear leader with a commanding 24.06% share by volume, underpinning its status as the largest tea consumer in Europe. German consumers demonstrate strong preferences across black, green, herbal, and ready-to-drink teas, supported by a mature and diverse tea culture. While the German market shows signs of maturity with slight volume declines, it remains a cornerstone of the European tea landscape, generating substantial revenue and maintaining leadership, favoring low-sugar and functional blends. The country’s established supermarkets, e-commerce, and specialty retail channels provide a robust platform for continued product innovation and premiumization within its mature but evolving market.

The United Kingdom, by contrast, is poised for rapid growth through 2031 with a projected CAGR of 6.33%. This surge is largely attributed to the UK's deep-rooted heritage with tea and a burgeoning consumer demand for artisanal and premium blends. The UK's market capitalization, steeped in a cultural identity that venerates tea consumption, sees a pronounced demand for organic, specialty, and health-centric products. Data from ITC Trade Map reveals that the UK's tea import value surged from USD 303.18 million in 2021 to an anticipated USD 377.01 million in 2024 , further highlighting the market's robust growth trajectory. Urban millennials and health-conscious consumers are driving this growth, gravitating towards innovative tea varieties such as single-origin, herbal, and functional teas. Bolstered by expanding e-commerce channels and premium product launches that harmonize tradition with contemporary wellness trends, the UK is on track to emerge as the top European market by revenue.

Other European countries contribute actively to the market dynamics with varying growth patterns and preferences. Romania and Spain, are emerging markets with increasing tea consumption.These countries, along with the Poland, Denmark, and Sweden are witnessing expanding demand driven by rising health awareness and adoption of premium and organic teas. Meanwhile, France maintains a solid position with gradual growth, boosted by a consumer base that values quality and sustainability. This geographic diversity enriches the overall European tea market, presenting opportunities for tailored marketing, product innovation, and sustainability initiatives suited to local preferences and evolving consumer trends.

Competitive Landscape

The European tea market demonstrates a moderate level of concentration, with a market concentration score of 6, reflecting a balanced competitive environment where both large multinational corporations and niche specialty brands operate successfully. This structure allows for diverse strategies, with dominant companies leveraging their substantial scale and resources to optimize supply chains and marketing reach, while smaller, specialty brands often capitalize on unique product offerings and strong consumer relationships built around origin stories and artisanal qualities. Such a landscape fosters innovation and variety, ensuring that consumer preferences across different segments—from mass-market to premium and organic—are well addressed.

Leading players such as Unilever’s Ekaterra, Associated British Foods’ Twinings, and Bettys & Taylors of Harrogate Ltd hold prominent positions through their extensive distribution networks spanning supermarkets, convenience stores, e-commerce platforms, and foodservice channels across Europe. Their well-established brand recognition and financial capabilities enable them to maintain market leadership by investing heavily in product development, sustainability initiatives, and consumer engagement. These companies excel in combining traditional brand equity with modern trends, such as health-conscious product lines, ready-to-drink teas, and eco-friendly packaging. Their scale advantages also allow them to negotiate favorable sourcing contracts and optimize logistics, which smaller competitors find challenging to match.

Meanwhile, specialty brands and smaller players complement the market by targeting niche consumer segments seeking high-quality, single-origin, organic, or ethically sourced teas. Such brands use differentiated positioning strategies that highlight traceability, craftsmanship, and wellness benefits, often engaging consumers through storytelling and transparent supply chains. This diversity enriches the competitive landscape by driving premiumization and inspiring larger firms to innovate continuously. Ultimately, the European tea market’s moderately concentrated structure supports a dynamic interplay where scale, heritage, sustainability, and consumer-focused differentiation define success for both major players and emerging specialty brands alike.

Europe Tea Industry Leaders

-

Associated Britsh Foods PLC

-

Unilever PLC

-

Teekanne GmbH & Co. KG

-

Bettys & Taylors of Harrogate Ltd

-

Tata Consumer Products Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kaytea, has unveiled a novel line of instant iced tea powders, targeting the UK market with its vision of 'next generation hydration'. These convenient powders come in three enticing flavours: Peach & Mango, Lemon, and the ever-popular Classic Milk Tea. Crafted for effortless preparation, these pre-blended powders can be seamlessly stirred into hot water, garnished with ice, or blended with cold water for a refreshing drink.

- November 2024: PG Tips, a prominent UK tea brand, has unveiled a new lineup of specially blended black teas. This range features classics like Earl Grey, Chai, Gold, and English Breakfast, all tailored to meet the changing tastes of consumers. Notably, these new blends are crafted to harmonize with the age-old British custom of adding milk to tea.

- July 2024: Brichall Tea has launched its latest offering: Green Tea & Mint. This refreshing blend marries the calming essence of premium green tea leaves with the lively zest of all-natural mint. Designed to provide a perfect balance of flavor and wellness, this product caters to consumers seeking a revitalizing and health-conscious beverage option.

- April 2024: Typhoo, the owner of the newly launched herbal tea brand, Herbalistas, has introduced a robust lineup of five teas. Each tea is thoughtfully infused with plant adaptogens, nootropics, and amino acids. The featured teas include Bedtime Bliss, Zen Time, Shine & Rise, Happy Place, and Daily Restore.

Europe Tea Market Report Scope

Tea is a drink that is produced from the combination of cured leaves of the Camellia sinensis (tea) plant with hot water. Tea is the second most popular beverage in the world, after water. The European tea market is segmented by form, type, distribution channel, and geography. Based on form, it is segmented into leaf tea and CTC tea. By type, the market is segmented into black tea, green tea, herbal tea, and other types. Based on distribution channel, it is segmented into hypermarkets/supermarkets, specialist retailers, convenience stores, online retailers, and other distribution channels. Furthermore, based on geography, it is segmented into Spain, the United Kingdom, France, Germany, Russia, and Italy. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Form

| Leaf Tea |

| CTC Tea |

By Product Type

| Black Tea |

| Green Tea |

| Herbal Tea |

| Oolong Tea |

| Fruit-Infused and Flavoured Tea |

| Other Product Types |

By Packaging Type

| Box |

| Bag |

| Pouch |

| Sachets |

| Other Packaging Types |

By Category

| Conventional |

| Organic |

By Distribution Channel

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| On-Trade |

By Geography

| Germany |

| United Kingdom |

| France |

| Russia |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Sweden |

| Rest of Europe |

| By Form | Leaf Tea | |

| CTC Tea | ||

| By Product Type | Black Tea | |

| Green Tea | ||

| Herbal Tea | ||

| Oolong Tea | ||

| Fruit-Infused and Flavoured Tea | ||

| Other Product Types | ||

| By Packaging Type | Box | |

| Bag | ||

| Pouch | ||

| Sachets | ||

| Other Packaging Types | ||

| By Category | Conventional | |

| Organic | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| On-Trade | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected value of the Europe tea market by 2031?

It is expected to reach USD 26.68 billion, supported by a 5.05% CAGR driven by premiumization and wellness demand.

Which product type is growing fastest in Europe?

Herbal tea leads with an 8.56% CAGR, buoyed by functional benefits and botanical diversity.

How significant is organic tea’s role in Europe?

Although conventional tea dominates, organic variants are expanding at 8.95% CAGR as consumers pay premiums for certified sustainability.

Which packaging formats are gaining momentum?

Resealable pouches are rising at 6.97% CAGR due to e-commerce suitability and freshness retention.

Why is Germany pivotal to the regional tea landscape?

Germany commands 24.06% market share, extensive import infrastructure, and culturally embedded consumption traditions.

Page last updated on: