Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.66 Billion |

| Market Size (2026) | USD 9.02 Billion |

| Market Size (2031) | USD 11.09 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Seasoning And Spices Market Analysis by Mordor Intelligence

The Europe seasoning and spices market size was valued at USD 8.66 billion in 2025 and estimated to grow from USD 9.02 billion in 2026 to reach USD 11.09 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031). This growth is primarily attributed to evolving consumer preferences, with Europeans becoming increasingly health-conscious and seeking natural ingredients in their food. The market is also benefiting from demographic changes as multicultural communities bring diverse culinary traditions to the region. The demand for organic and clean-label products remains robust, reflecting consumers' growing interest in transparent and natural food ingredients. European consumers now recognize herbs and spices not just as flavor enhancers but as functional ingredients that offer significant health benefits, including antioxidant properties, anti-inflammatory effects, and improved digestion. This perception has helped manufacturers maintain premium pricing strategies even during periods of economic pressure. The expanding convenience food sector and ready-to-cook meal segment, alongside new regulatory frameworks such as the European Union Deforestation Regulation (EUDR) and Corporate Sustainability Reporting Directive (CSRD), are compelling manufacturers to establish more transparent and environmentally responsible sourcing networks. While larger industry players with strong compliance capabilities continue to strengthen their market positions, investments in biotechnology and advanced processing techniques are helping improve supply chain reliability and ensure consistent product quality across the market.

Key Report Takeaways

- By type, salt and salt substitutes held 36.88% of value in 2025 while herbs and seasonings are expected to post a 5.49% CAGR through 2031.

- By category, conventional products controlled 79.55% of 2025 sales while organic variants are projected to advance at a 5.31% CAGR between 2026 and 2031.

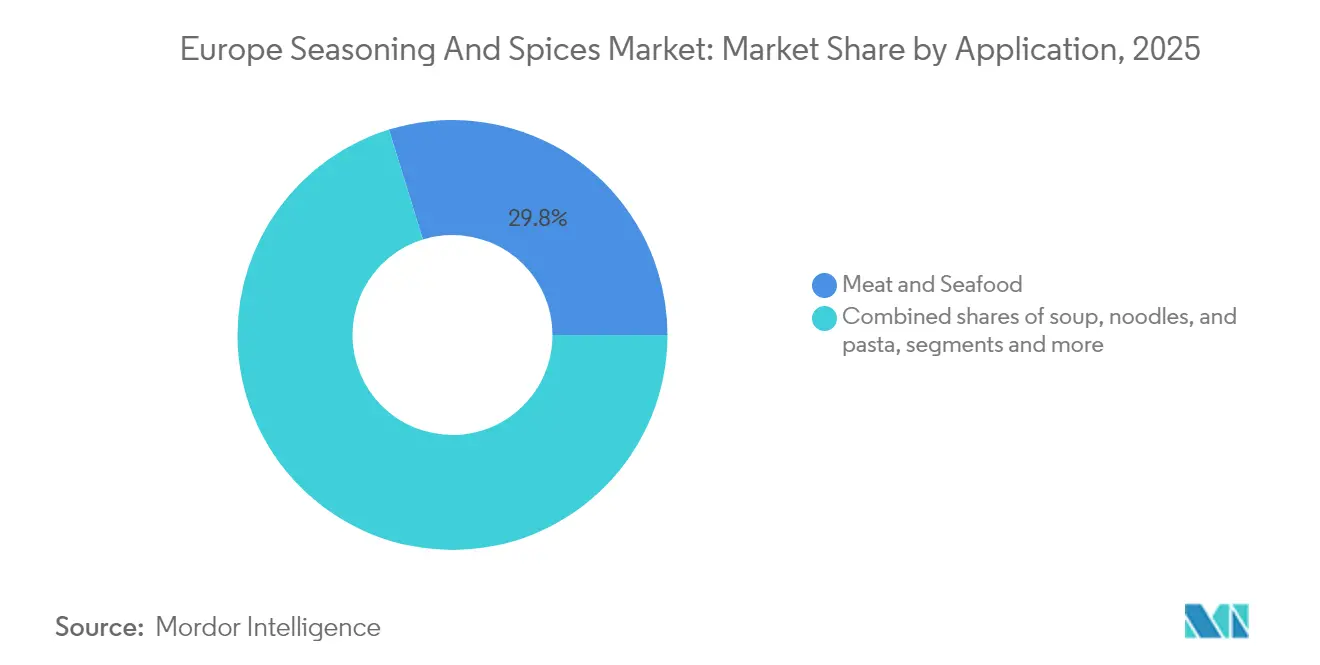

- By application, meat and seafood accounted for 29.78% of 2025 demand while savory snacks are forecast to expand at a 5.62% CAGR through 2031.

- By geography, Germany contributed 22.64% of 2025 revenue while Italy exhibits the fastest trajectory with a 5.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Seasoning And Spices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding consumer demand for healthier and better-quality ingredients | +1.2% | Germany, Netherlands, Nordic countries | Medium term (2-4 years) |

| Increasing adoption of multicultural diet patterns and international cuisines | +0.8% | Urban centers across Western Europe, United Kingdom | Short term (≤ 2 years) |

| Trend toward organic and clean-label spices and seasonings | +0.6% | Germany, France, Netherlands, Scandinavia | Long term (≥ 4 years) |

| Growth in convenience, ready-to-cook, and processed foods industries | +0.5% | United Kingdom, Germany, France, urban markets | Medium term (2-4 years) |

| Focus on sustainable and eco-conscious sourcing methods | +0.4% | Europe-wide, strongest in Germany and Netherlands | Long term (≥ 4 years) |

| Tourism and migration are broadening palate preferences | +0.3% | Southern Europe, major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Consumer Demand for Healthier and Better-Quality Ingredients

European consumers increasingly view spices as functional ingredients with health benefits beyond flavoring. Turmeric (for anti-inflammatory properties), ginger (for digestive health), and cinnamon (for blood sugar regulation) experience growing demand. This consumer perception enables premium pricing for spices with verified potency levels. Single-estate turmeric with higher curcumin concentrations commands a 40% price premium compared to commodity-grade variants. German consumers drive this trend, with organic spices sales experiencing significant annual growth due to demand for pesticide-free certification and supply chain transparency. The health and wellness positioning elevates spices from commodity items to premium health products, enabling margin growth across the value chain. European Food Safety Authority (EFSA) health claim approvals provide regulatory support for functional spice marketing, while ISO 22000 food safety standards serve as baseline requirements for health-oriented products.

Increasing Adoption of Multicultural Diet Patterns and International Cuisines

Migration patterns and tourism have reshaped European food preferences, transforming consumer behavior across major metropolitan areas. Urban centers in Germany, France, and the Netherlands demonstrate strong adoption of Middle Eastern (baharat, za'atar), North African (harissa, ras-el-hanout), and Asian (gochujang, miso-based) seasoning blends. The trend extends beyond immigrant communities, as European consumers incorporate global flavors influenced by social media content and international travel experiences. Restaurant chains now offer fusion dishes combining traditional European techniques with international spice profiles, driving mainstream demand for previously specialty ingredients. This shift has led to premiumization in the market, with authentic imported spice blends commanding substantial price premiums compared to standard European seasonings.

Trend Toward Organic and Clean-Label Spices and Seasonings

The organic spice market in Western Europe continues to show remarkable momentum, with growth rates tripling those of conventional spices. Consumer behavior indicates a strong acceptance of premium pricing, with buyers willingly paying 40-60% more for certified organic products. The implementation of European Union regulation (EU 2018/848) has established comprehensive certification protocols, creating favorable conditions for established suppliers who have invested in sophisticated traceability systems [1]Source: European Union, "Regulation (EU) 2018/848 Of The European Parliament And Of The Council," eur-lex.europa.eu. The growing demand for clean-label products has transformed product formulations, as manufacturers shift from artificial preservatives, colors, and flavor enhancers to natural alternatives. This change has increased the use of natural preservation methods, such as rosemary extracts and citric acid-based solutions. In response, Syensqo introduced Riza rosemary extracts, offering food manufacturers natural antioxidant protection for processed foods. This shift has created opportunities for suppliers of certified organic, non-GMO, and additive-free products, while traditional manufacturers must adapt their product lines to meet new market demands. The European Union (EU) organic market showed recovery in 2023 following a decline in 2022, driven by improved consumer financial conditions and consistent demand from established organic product consumers. Most EU member states are expected to experience growth through 2025, though at a slower pace than in previous years. France and Germany remain the largest organic markets in the region [2]Source: United States Department of Agriculture, "EU Organics Market Begins to Recover", apps.fas.usda.gov.

Growth in Convenience, Ready-to-Cook, and Processed Foods Industries

European consumers increasingly embraced restaurant-quality meals in home-preparation formats, driving significant growth in convenience food sales. The rising popularity of ready-to-cook meal kits has fueled the demand for encapsulated and stabilized seasoning systems, which ensure precise spice portions and maintain flavor throughout their shelf life. To cater to evolving tastes, food manufacturers have introduced cross-cultural flavor combinations, such as Italian pasta sauces infused with North African spices and German sausages paired with Asian seasonings. This shift has boosted the sales of spice blends over whole spices, enhancing market profitability. Large seasoning companies with industrial blending capabilities have leveraged economies of scale in procurement and processing to strengthen their market position. In 2024, the processed food segment in European convenience stores continued to grow, contributing to overall regional sales. Although growth in Europe remained modest, promotions in categories like soft drinks, frozen foods, snacks, and perishables attracted shoppers with broader purchase intentions, such as “dinner for tonight.” These promoted categories now account for approximately 45% of convenience store sales [3]Source: NACS, "Global Convenience Store Industry Reports," convenience.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and complex regulatory requirements | -0.7% | European-wide, particularly Germany and Netherlands | Medium term (2-4 years) |

| Limited availability of organic and sustainably sourced raw materials | -0.5% | Northern Europe, premium market segments | Long term (≥ 4 years) |

| Technical challenges in formulating new spice blends without compromising flavor | -0.4% | Innovation-focused markets, Germany, France | Short term (≤ 2 years) |

| Challenges with shelf life, stability, and sensory quality | -0.3% | Export markets, processed food applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent and Complex Regulatory Requirements

The European Union Deforestation Regulation (EUDR), taking effect in 2024, introduces comprehensive supply chain traceability requirements for spice imports. This regulation imposes substantial compliance costs on affected suppliers, impacting their operational expenses and profit margins. The requirements particularly affect pepper, cinnamon, and nutmeg imports from Southeast Asia, where smallholder farming operations lack GPS-verified deforestation-free certification. The Corporate Sustainability Reporting Directive (CSRD) requires companies operating in the EU to report environmental and social impacts throughout their supply chains, resulting in increased administrative and audit expenses. These regulations benefit larger companies with existing compliance systems while creating entry barriers for smaller importers and specialty spice traders. The regulatory requirements accelerate market consolidation as smaller operators either exit the market or become acquisition targets for larger, compliant companies.

Limited Availability of Organic and Sustainably Sourced Raw Materials

The organic spice market continues to experience significant supply limitations globally, as certified organic farmland constitutes only a minimal portion of worldwide spice cultivation areas. Throughout European markets, the escalating consumer demand for organic spices persistently surpasses available supply capabilities, resulting in considerable market instability and creating complex distribution challenges for processing companies. The implementation of environmental compliance measures through sustainable sourcing initiatives requires processors to offer premium compensation to farming communities, which subsequently drives up raw material acquisition costs in comparison to traditional spice cultivation methods. These ongoing supply restrictions particularly impact the premium market segments, where organic certification has evolved from being a competitive advantage to becoming an essential market entry requirement. The situation has created a complex dynamic between producers, processors, and end-market demands, affecting the entire organic spice supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Salt Substitutes Drive Health-Conscious Innovation

The European food ingredients market demonstrates a significant shift toward healthier alternatives, with salt and salt substitutes commanding a substantial 36.88% market share in 2025. This trend directly correlates with increasing consumer awareness about hypertension and its health implications. Kerry Group's innovative Tastesense Salt technology has emerged as a notable solution in this segment, successfully reducing sodium content by 50% while preserving the desired taste profile through a combination of potassium chloride and natural flavor enhancers.

The herbs and seasonings segment exhibits robust growth prospects, with projections indicating a 5.49% CAGR through 2031. This growth is primarily attributed to increasing consumer preference for clean-label products and their associated health benefits. Traditional Mediterranean herbs, including thyme, basil, and oregano, continue to gain market traction, while mint has evolved beyond conventional applications to establish a strong presence in the functional beverages and wellness products categories, reflecting broader consumer health trends.

By Category: Organic Growth Accelerates Despite Premium Pricing

The conventional seasonings market maintains its dominant position with a 79.55% market share in 2025. This substantial market presence stems from well-established supply chain networks that have evolved over decades, enabling manufacturers to maintain competitive pricing strategies across various mass market applications. These traditional seasonings continue to meet the fundamental requirements of both industrial food processors and retail consumers, providing reliable quality at accessible price points.

The organic seasonings segment is experiencing robust growth at a 5.31% CAGR through 2031, primarily driven by European consumer preferences. These consumers demonstrate a clear willingness to pay premium prices, ranging from 40-60% higher for certified organic products. The implementation of EU Organic Regulation (2018/848) has introduced comprehensive certification requirements, naturally favoring suppliers who have invested in sophisticated traceability systems. While organic seasonings particularly appeal to health-conscious urban consumers in Germany, Netherlands, and Scandinavian countries, the segment faces growth limitations due to supply constraints, as certified organic farmland represents only a small fraction - less than 5% - of global spice cultivation area.

By Application: Savory Snacks Emerge as Growth Engine

The meat and seafood segment held a 29.78% market share in 2025, supported by traditional European protein consumption patterns and established seasoning preferences. This segment benefits from premium processed meat products that use authentic spice blends for product differentiation. The savory snacks segment is projected to grow at a 5.62% CAGR through 2031, driven by new flavor development and product formats beyond potato chips. Key growth factors include African spices, fruit-floral combinations, and global street food flavors.

The bakery and confectionery segment maintains consistent demand for cinnamon, vanilla, and cardamom, while the soup, noodles, and pasta segment grows with the expansion of convenience foods. The sauces, salads, and dressing segment shows growth through ethnic fusion trends, particularly with harissa, za'atar, and Asian seasonings gaining wider acceptance. Additional applications in beverages and functional foods present new opportunities, especially for spices like turmeric and ginger with adaptogenic properties. This diverse application range reflects European consumers' increasingly sophisticated taste preferences and openness to global flavors across food categories.

Geography Analysis

Germany's dominant position in the European spice market, holding a 22.64% share in 2025, stems from its well-established food processing industry and sophisticated consumer base that prioritizes quality ingredients with verified sourcing. German consumers have developed a strong inclination toward organic and sustainably sourced spices, which has propelled significant growth in the premium segment across major retail chains. The industrial sector, particularly processed meat, bakery, and convenience food manufacturers, contributes substantially to market demand as they seek spices that deliver consistent flavor profiles while meeting stringent regulatory requirements. The market's attractiveness is further evidenced by strategic acquisitions, such as Nova Taste's purchase of German spice manufacturer Eppers, indicating ongoing industry consolidation in this vital market.

Italy has emerged as the market's growth engine, achieving a remarkable 5.78% CAGR through 2031. This growth trajectory is primarily attributed to the country's evolving culinary landscape, which has expanded beyond traditional Mediterranean herbs to embrace global flavor profiles. In urban areas, consumers are increasingly experimenting with ethnic cuisines, while food processors are actively developing innovative fusion concepts that blend traditional Italian culinary techniques with diverse international spice profiles. The Netherlands has strengthened its strategic position as Europe's primary spice trading hub, with Rotterdam port functioning as a crucial gateway for spice imports from Asia and Africa. The significance of this position is underscored by Marubeni Corporation's substantial USD 500 million investment in acquiring Dutch spice manufacturer Euroma in 2024, highlighting the critical role of Netherlands-based operations in global supply chain networks.

Several other European countries maintain significant market presence through their distinct market characteristics. France, Spain, and the United Kingdom leverage their established food processing industries and evolving consumer preferences for international cuisines to maintain substantial market positions. Poland and Belgium are experiencing market growth driven by their expanding processed food sectors and increasing consumer purchasing power, which supports premium spice purchases. In the Nordic region, Sweden and its neighboring countries demonstrate particularly strong growth in the organic segment, reflecting heightened environmental consciousness and consumers' willingness to pay premium prices for sustainable products. This diverse geographic landscape presents opportunities for companies to implement targeted product positioning strategies and optimize supply chain operations across varying consumer preferences and regulatory frameworks.

Competitive Landscape

The European seasoning and spices market shows moderate concentration, with several key players dominating the industry. However, the market structure indicates substantial opportunities for strategic acquisitions and consolidation. Market leaders are actively pursuing vertical integration strategies, as evidenced by Kerry Group's strategic acquisitions of biotech companies c-LEcta and Enmex, which specialize in biotechnological production of natural flavor compounds. This strategic shift addresses both sustainability requirements and supply security concerns, particularly as climate changes continue to affect traditional spice-growing regions.

Companies are strengthening their competitive positions through significant technology investments, implementing advanced processing systems such as BHS-Sonthofen's dynamic pressure sterilization equipment. These systems achieve 5-log microbial reduction while maintaining the sensory quality of the products. New market entrants have successfully penetrated premium market segments by focusing on sustainability initiatives and establishing direct-trade relationships, prompting established companies to respond by obtaining organic certifications and improving their traceability systems.

The market presents several growth opportunities, particularly in biotechnology-produced natural flavors, encapsulated delivery systems, and specialized seasoning solutions designed specifically for plant-based proteins. Companies that possess clinical substantiation capabilities are gaining competitive advantages through European Food Safety Authority (EFSA) health claim approvals. Additionally, compliance with EU Deforestation Regulation has become a fundamental requirement for companies to participate in the market, reflecting the increasing importance of environmental sustainability in the industry.

Europe Seasoning And Spices Industry Leaders

-

SHS Group

-

Prymat Group

-

Olam International

-

Kerry Group PLC

-

Arikon Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Austrian company Nova Taste acquired German spice and sauce manufacturer Eppers, employing approximately 140 people in Saarbrücken-Bübingen, as part of strategic expansion to secure growth opportunities and leverage Nova Taste's global network of over 2,000 employees

- October 2024: German natural aroma ingredients manufacturer Axxence Aromatic, known for its expertise in natural flavor compounds, signed a definitive agreement to merge with US-based Natural Advantage, a well-established player in the aroma ingredients industry. The merger aims to create a combined entity that will strengthen their market presence and enhance their product portfolio.

- December 2023: Marubeni Corporation completed full acquisition of Netherlands-based Euroma Holding B.V., the third-largest spices and seasonings manufacturer in Europe with approximately 530 employees, for strategic expansion leveraging Marubeni's agricultural networks

Europe Seasoning And Spices Market Report Scope

Spices and seasonings are widely used to add flavor, aroma, color, and taste to food and beverages and sometimes act as preservatives or antibacterial agents. Manufacturers use these attributes of spices and seasonings to improve their product quality and taste and increase their shelf life. The European seasoning and spices market is segmented into product type, application, and geography. By product type, the market is segmented into salt and salt substitutes, herbs and seasonings, and spices. Herbs and seasonings are further sub-segmented into thyme, basil, oregano, parsley, and other herbs. Spices are sub-segmented into pepper, cardamom, cinnamon, clove, nutmeg, turmeric, and other spices. By application, the market is segmented into bakery and confectionery, soup, noodles, and pasta, meat and seafood, sauces, salads, and dressing, savory snacks, and other applications. The market is also segmented by country into Spain, United Kingdom, France, Germany, Russia, Italy, and Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Type

| Salt and Salt Substitutes | |

| Herbs and Seasonings | Thyme |

| Basil | |

| Oregano | |

| Parsley | |

| Mint | |

| Other Herbs and Seasonings | |

| Spices | Pepper |

| Sesame | |

| Cinnamon | |

| Mustard | |

| Onion | |

| Garlic | |

| Paprika | |

| Chili Pepper | |

| Other Spices |

By Category

| Organic |

| Conventional |

By Application

| Bakery and Confectionery |

| Soup, Noodles, and Pasta |

| Meat and Seafood |

| Sauces, Salads, and Dressing |

| Savory Snacks |

| Other Applications |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Type | Salt and Salt Substitutes | |

| Herbs and Seasonings | Thyme | |

| Basil | ||

| Oregano | ||

| Parsley | ||

| Mint | ||

| Other Herbs and Seasonings | ||

| Spices | Pepper | |

| Sesame | ||

| Cinnamon | ||

| Mustard | ||

| Onion | ||

| Garlic | ||

| Paprika | ||

| Chili Pepper | ||

| Other Spices | ||

| By Category | Organic | |

| Conventional | ||

| By Application | Bakery and Confectionery | |

| Soup, Noodles, and Pasta | ||

| Meat and Seafood | ||

| Sauces, Salads, and Dressing | ||

| Savory Snacks | ||

| Other Applications | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected value of the Europe seasoning and spices market by 2031?

The market is forecast to reach USD 11.09 billion by 2031, supported by a 4.18% CAGR.

Which product type currently dominates sales?

Salt and salt substitutes lead with 36.88% of 2025 revenues.

Which product category is growing fastest?

Certified organic seasonings are poised for a 5.31% CAGR to 2031.

Which application will add the most incremental demand?

Savory snacks are expected to expand at a 5.62% CAGR as brands diversify flavors.

Which country offers the highest growth potential?

Italy shows the strongest outlook with a 5.78% CAGR through 2031.

Page last updated on: