Asia-Pacific Satellite Attitude And Orbit Control System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 0.6 Billion |

| Market Size (2030) | USD 1.06 Billion |

| Growth Rate (2025 - 2030) | 12.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Satellite Attitude And Orbit Control System Market Analysis by Mordor Intelligence

The Asia-Pacific satellite attitude and orbit control system (AOCS) market size is valued at USD 0.60 billion in 2025 and is forecasted to reach USD 1.06 billion by 2030, advancing at a 12.23% CAGR. Rising geopolitical tension, heavier defense appropriations, and a deliberate pivot toward space sovereignty are the principal demand catalysts. Increased satellite launches, space program expansion, and higher demand for Earth observation, communication, and navigation services drive the market growth. China, India, Japan, and South Korea's investments in satellite development and domestic space technologies contribute to market growth in the region. Regional constellation programs such as China's Guowang and India's NavIC-2 lock in multi-year procurement pipelines, while electric-propulsion adoption lifts system ASPs.

Parallel supply chains forming in response to export-control frictions stimulate indigenous component production, lowering lead times and de-risking logistics. Commercial constellation economics keep per-platform prices in check, yet mission-profile complexity pushes average content per satellite higher, preserving vendor margins amid volume expansion. Incorporating advanced sensors, actuators, and AI-based control algorithms improves satellite precision, reliability, and operational life. The increased deployment of small satellites and CubeSats in commercial and defense applications has led to greater adoption of compact and efficient AOCS solutions. Government support for space innovation and new private sector participants indicate continued market expansion in the Asia-Pacific region over the next decade.

Key Report Takeaways

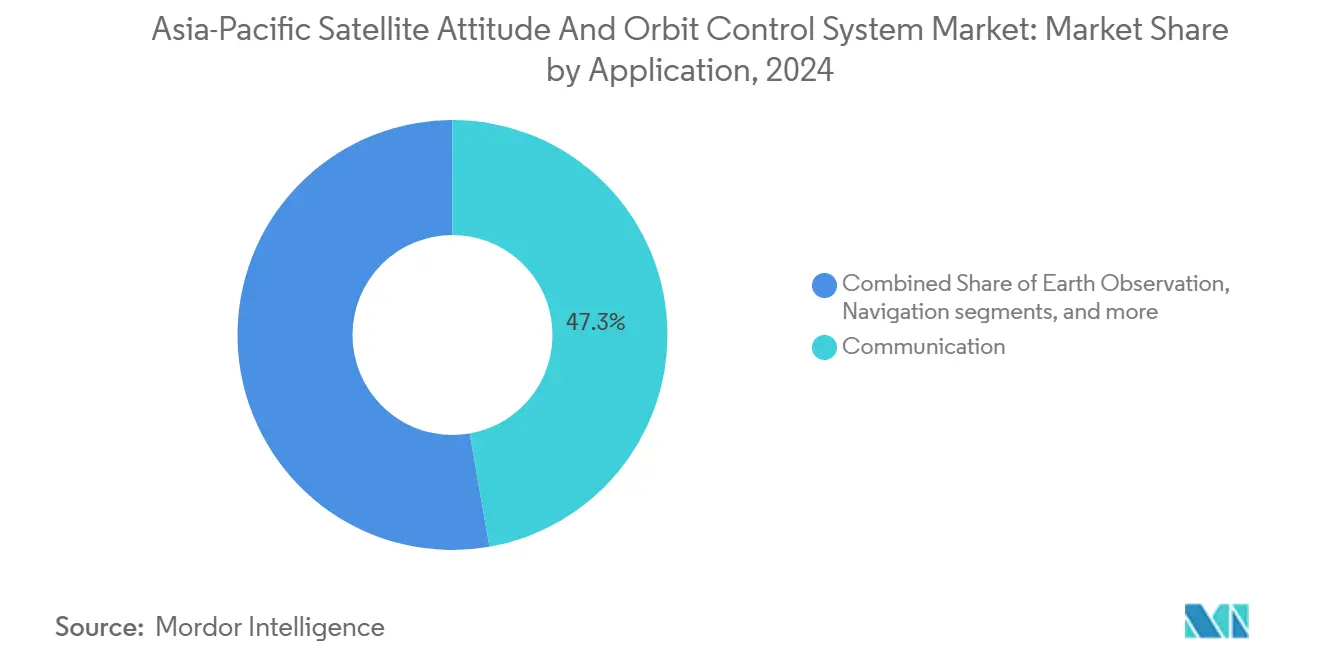

- By application, communication satellites held 47.25% of the Asia-Pacific satellite AOCS market share in 2024; Earth observation systems are projected to grow at a 13.71% CAGR to 2030.

- By satellite mass, the 100 to 500 kg segment captured 47.75% of the Asia-Pacific satellite AOCS market size in 2024, while 10 to 100 kg platforms are set to expand at 13.83% CAGR through 2030.

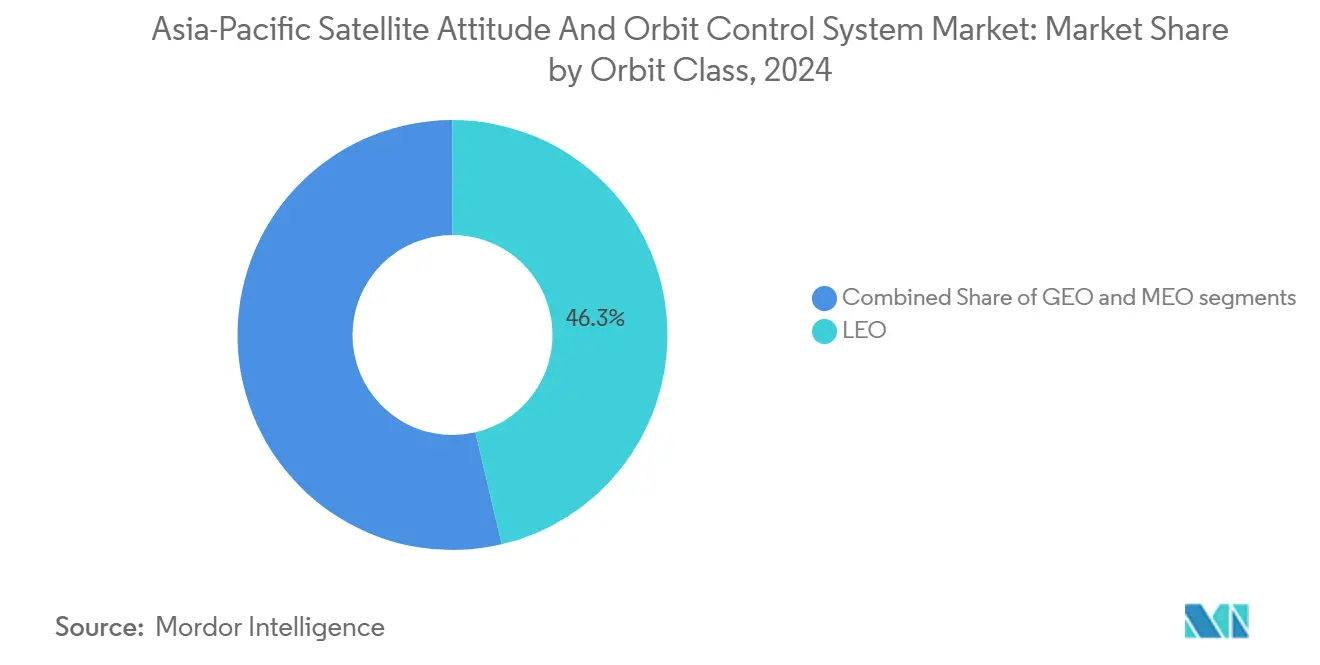

- By orbit class, LEO platforms commanded 46.32% share of the Asia-Pacific satellite AOCS market size in 2024, whereas MEO platforms are forecast to register the fastest 13.91% CAGR to 2030.

- By end user, commercial operators accounted for a 43.69% share in 2024; military and government demand is advancing at a 14.52% CAGR to 2030.

- By geography, China led with 40.22% revenue share in 2024, and India is poised for the quickest 14.23% CAGR through 2030.

Asia-Pacific Satellite Attitude And Orbit Control System Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of small-sat constellations in Asia-Pacific | +3.2% | China, India, Japan core; spillover to ASEAN | Medium term (2-4 years) |

| Expanded defense and civil space budgets across Asia-Pacific | +2.8% | Regional, concentrated in China, India, Japan, Australia | Short term (≤ 2 years) |

| Shift to electric propulsion and high-precision AOCS | +2.1% | Global; early adoption in Japan and Australia | Long term (≥ 4 years) |

| Surge in Asia-Pacific LEO PNT constellation programs | +1.9% | China, India primary; regional navigation spillover | Medium term (2-4 years) |

| On-orbit servicing and debris-removal startups | +1.4% | Japan, Australia lead; China following | Long term (≥ 4 years) |

| Indigenous AOCS supply-chain policies | +1.2% | China, India, Japan domestic focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Small-Sat Constellations Reshapes AOCS Architecture

The increasing deployment of small-satellite constellations in the Asia-Pacific transforms AOCS design. Manufacturers are developing compact, energy-efficient control systems with high precision to support the growing number of lightweight, low-cost satellites. Rapid constellation rollouts redefine system design by favoring standardized modules that slash unit costs and heighten manufacturability. Guowang’s launch cadence demonstrated 35% per-unit savings once mass production crossed 100 platforms.[1]China launches 18 satellites for Guowang constellation,” SpaceNews, spacenews.com Fleet-level coordination shifts sophisticated maneuver planning to ground segments, letting onboard controllers focus on localized attitude tasks and trim hardware redundancy. India’s NavIC-2 and Japan’s QZSS expansions mirror this template, cementing volume certainty for regional suppliers and encouraging software-defined control architectures that can be batch-updated to support evolving mission profiles. The market shows increased adoption of miniaturized components, including micro-reaction wheels, MEMS sensors, and AI-enabled autonomous control systems for coordinated orbit management. This expansion of small-satellite constellations is increasing AOCS demand and advancing the development of modular, scalable, intelligent control architectures.

Expanded Defense Budgets Accelerate Indigenous AOCS Development

The increase in defense spending across the Asia-Pacific drives the development of domestic satellite technologies, including advanced AOCS solutions. Governments in China, India, and Japan are focusing on self-reliance in space defense through increased investment in locally designed and manufactured control systems. Asia-Pacific defense outlays touched USD 18.5 billion in 2024, roughly 8% earmarked for attitude and orbital control solutions.[2]Defence Space Strategy 2024-2028,” Australian Department of Defence, defence.gov.au Programs in Australia and Japan mandate radiation-hard, cyber-resilient designs that withstand contested domains, accelerating technology transfer into commercial fleets. India's 25% budget jump in 2024 raised R&D subsidies for start-ups delivering dual-use architectures, while widespread offset policies further deepen domestic content and skill development. These investments aim to enhance national security, reduce foreign supplier dependence, and strengthen strategic surveillance, communication, and navigation capabilities. The expansion of defense budgets is accelerating the region's innovation and domestic production of high-performance AOCS technologies.

Electric Propulsion Integration Demands Advanced Control Systems

The increasing adoption of electric propulsion systems in satellites across the Asia-Pacific drives the demand for sophisticated AOCS. Electric propulsion enables extended mission life and improved fuel efficiency but requires precise control for managing low-thrust, continuous operations. Hall-effect thrusters now equip 65% of new satellites over 100 kg, introducing thrust-vector dynamics that require microsecond controller response and robust power-thermal orchestration.[3]Electric propulsion integration in modern satellites,” Journal of Spacecraft and Rockets, arc.aiaa.org Integrated propulsion-AOCS modules from regional OEMs cut total mass 15% and improve pointing accuracy to 0.01°.[4]Advanced AOCS-propulsion integration modules,” Mitsubishi Electric Corporation, mitsubishielectric.com Though such integration lifts upfront costs 25–30%, lifecycle extension of 40% supports favorable total-cost-of-ownership economics, especially for broadband constellations forecasting multi-launch refresh cycles. This has led to the development of advanced AOCS architectures that provide fine attitude adjustments, real-time orbit correction, and optimized power management. The regional shift toward electric propulsion in satellite programs increases the demand for intelligent, adaptive AOCS technology.

LEO PNT Constellations Drive Precision Requirements

The growth of Low Earth Orbit (LEO) Positioning, Navigation, and Timing (PNT) constellations in the Asia-Pacific is increasing the demand for high-precision AOCS solutions. These satellites need precise attitude and orbit control to maintain signal coverage and synchronization. Emerging regional navigation networks demand orbit-knowledge accuracies within centimeters and timing coherence at millisecond scales. BeiDou-4 plans specify relative positioning tolerance of 10 cm across 1,000 km baselines, pushing uptake of star trackers rated at 0.1 arcsec and fiber-optic gyros with 0.001 °/hr bias stability.[5]BeiDou-4 constellation planning and precision requirements,” China Satellite Navigation Office, beidou.gov.cn Elevated sensor specs inflate unit cost but unlock downstream revenue in autonomous vehicles and precision agriculture, expanding constellation operators' total reachable user base. AOCS systems now integrate advanced sensors, high-speed processors, and AI-driven control algorithms to meet these requirements. The development of LEO-based PNT networks by regional space agencies and private companies drives the demand for precise control systems.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development and qualification costs | −2.4% | Region-wide; sharper for SMEs | Short term (≤ 2 years) |

| Export-control limits on sensors/electronics | −1.8% | China, Russia primary; region-wide spillover | Medium term (2–4 years) |

| Rad-hard semiconductor fab constraints in Asia-Pacific | −1.5% | Global; acute in LEO | Long term (≥ 4 years) |

| Cyber-verification burden for autonomous avoidance | −1.2% | Emerging Asia-Pacific markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Development Costs Constrain Market Entry

The satellite AOCS requires complex design and precision engineering, which increases development and testing costs. The system's advanced sensors, actuators, and control algorithms require significant investment in research, development, simulation, and qualification processes. Qualification regimes consume up to 60% of total R&D spending, with thermal-vacuum and radiation tests topping USD 8 million per variant.[6]AOCS system qualification costs and barriers,” IEEE Transactions on Aerospace and Electronic Systems, ieeexplore.ieee.org New entrants face three-to-five-year breakeven horizons, nudging them toward joint ventures with heritage players that can amortize facility overhead. Capital intensity also accelerates mergers among niche providers, consolidating expertise and safeguarding supply for large constellation contracts. These financial and technical requirements create barriers for smaller companies and emerging space startups. The need for extensive space environment testing further increases costs, which limits innovation and market entry, particularly for cost-sensitive companies in the Asia-Pacific region.

Export Controls Fragment Supply Chains

Export regulations on satellite components and technologies from the United States and Europe affect the Asia-Pacific AOCS market supply chains. The restrictions on sensors, actuators, and control electronics limit access to high-end components for regional manufacturers. ITAR and Wassenaar constraints extend lead times for flight-qualified sensors by 18 months and raise inventory holding costs by 20–30%. Chinese and Indian firms now pour billions into domestic sensor programs, while joint development pacts with non-US vendors diversify risk. Although short-term friction hampers schedule certainty, long-run localization efforts promise lower bill-of-materials expenses and fresh competition for legacy Western suppliers. These constraints compel local companies to use alternative or domestically developed solutions, increasing costs and extending development cycles. The export controls restrict technology transfer and innovation, impacting the growth of the regional AOCS market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Communication Dominance, Earth Observation Momentum

Communication platforms captured 47.25% of the Asia-Pacific satellite AOCS market in 2024, buoyed by mass-manufactured broadband constellations that prize cost-optimized, standardized controllers. Earth observation is the growth pacesetter at 13.71% CAGR as climate surveillance, precision farming, and disaster mapping mandates proliferate. Navigation missions remain the most technically stringent, demanding atomic-clock stability and centimeter-level orbit control. At the same time, space-observation and emerging tourism payloads carve high-value niches requiring micro-arcsecond pointing. Earth observation’s ascendancy pushes vendors to fine-tune torque-rod bandwidth, reaction-wheel jitter levels, and slew-rate profiles that capture fast-moving phenomena. Communication operators, conversely, leverage volume to negotiate lower ASPs, yet still invest in AI-based autonomous collision avoidance for congested LEO lanes. Collectively, these trends entrench the Asia-Pacific satellite AOCS market as the fulcrum of next-gen platform capability upgrades.

By Satellite Mass: Mid-Class Sweet Spot, Mini-Class Surge

Platforms weighing 100 to 500 kg held 47.75% of 2024 revenue because they balance launch-per-gigabit economics with payload flexibility, a dynamic reflected in multiple constellation rollouts. The 10 to 100 kg band shows 13.83% CAGR as CubeSat standards cut structural and testing overhead, letting universities and start-ups enter revenue service rapidly. Miniaturization spawns controller boards under 500 g that fuse attitude sensors, power management, and RF links, enabling “plug-and-play” architectures across mass classes. For platforms weighing above 1,000 kg, redundancy requirements drive dual-string electronics and multi-wheel arrays, elevating BOM but ensuring mission assurance. Vendors thus craft modular portfolios to address varied mass-class economics within the Asia-Pacific satellite AOCS market.

By Orbit Class: LEO Volume, MEO Upswing

LEO retained 46.32% share in 2024, chiefly because low latency favors broadband and IoT use cases, while ride-share launch economics pare per-satellite cost. MEO, however, records the fastest 13.91% CAGR as regional positioning and timing systems demand radiation-tolerant, long-lived platforms where orbital stability trumps latency advantages. Radiation belts necessitate hardened processors and shielded star trackers, pushing average sales prices (ASPs) upward yet attracting defense and infrastructure buyers willing to pay for reliability. GEO missions maintain premium demand for 15-year lifecycles, requiring continuous station-keeping within 0.1° accuracy. Orbit-specific challenges, therefore, underpin diversified product strategies across the Asia-Pacific satellite AOCS industry.

By End User: Commercial Scale, Government Precision

Commercial operators generated 43.69% of 2024 revenue, propelled by constellation scale-economy imperatives that incentivize B2B connectivity services. Government and military demand rises at 14.52% CAGR as sovereign-capability programs mandate cyber-secure, autonomous systems able to function under communication denial. Dual-use synergies emerge: civilian makers lower component cost curves, while defense customers push performance envelopes that cascade to commercial variants later. Scientific agencies further spur innovation in formation-flying and distributed sensing, broadening the Asia-Pacific satellite AOCS market addressable base with mission-specific controller features.

Geography Analysis

The Asia-Pacific region has become a significant center for satellite AOCS development, supported by established space programs and increased commercial activities. China dominates the market through extensive satellite launches and investments in AOCS technology. Through ISRO's satellite missions and private sector growth, India maintains a strong position. Japan specializes in developing precise and autonomous systems for government and commercial satellites. South Korea and Australia are strengthening their capabilities in small satellites and defense applications. China's 40.22% share stems from state-backed vertical integration and aggressive constellation timelines.

In 2024, USD 8.2 billion flowed to China Academy of Space Technology (CAST) to localize radiation-hard electronics and scale production lines, tightening domestic supply loops and boosting export competitiveness. India posts the swiftest 14.23% CAGR as policy liberalization allows 100% FDI, catalyzing joint ventures that blend ISRO heritage with private capital. Indigenous vendors such as Skyroot and Agnikul shorten development cycles and target regional export markets.

Japan and Australia sustain steady growth via precision manufacturing and defense collaboration. Tokyo's high-spec orientation favors premium AOCS exports, whereas Canberra's Five Eyes commitments accelerate sovereign-secure technology adoption, supported by AUD 12 billion (USD 7.92 billion) space-economy targets. Regional cooperation, increased research and development funding, and government support continue to drive market expansion in the Asia-Pacific.

Competitive Landscape

Market concentration is moderate and trending downward as regional champions erode Western incumbents’ share through cost-effective, ITAR-free designs. Honeywell International Inc., NEC Corporation, and L3Harris Technologies, Inc. defend high-end niches with proven radiation tolerance. Meanwhile, Mitsubishi Electric Corporation and CAST leverage state orders to refine integrated propulsion-control stacks. AAC Clyde Space AB operates in the Asia-Pacific AOCS market as an established NewSpace supplier, providing flight-proven, plug-and-play ADCS components for CubeSats and small satellites. Indigenous sensor production in China and India promises lower lead times and pricing, squeezing vendors reliant on imported optics. Overall, incumbent-newcomer interplay accelerates innovation cycles within the Asia-Pacific satellite AOCS market.

Asia-Pacific Satellite Attitude And Orbit Control System Industry Leaders

Mitsubishi Electric Corporation

Honeywell International Inc.

NEC Corporation

AAC Clyde Space AB

L3Harris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Astroscale (Japan) partnered with Indian firms Digantara and Bellatrix Aerospace to collaborate on orbital services, signaling increased activity in the Asia-Pacific space ecosystem. This drives AOCS demand for attitude/orbit control in servicing missions.

- January 2025: Planet Labs secured a USD 230 million contract to build satellites for a commercial partner in the Asia-Pacific region, scheduled for delivery by 2026. This underscores the growing demand for satellite platforms and thus AOCS subsystems in the region.

Asia-Pacific Satellite Attitude And Orbit Control System Market Report Scope

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

| Below 10 kg |

| 10 to 100 kg |

| 100 to 500 kg |

| 500 to 1000 kg |

| Above 1000 kg |

| Geostationary Earth Orbit (GEO) |

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Commercial |

| Military and Government |

| Other |

| China |

| India |

| Japan |

| Australia |

| Rest of Asia-Pacific |

| By Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others | |

| By Satellite Mass | Below 10 kg |

| 10 to 100 kg | |

| 100 to 500 kg | |

| 500 to 1000 kg | |

| Above 1000 kg | |

| By Orbit Class | Geostationary Earth Orbit (GEO) |

| Low Earth Orbit (LEO) | |

| Medium Earth Orbit (MEO) | |

| By End User | Commercial |

| Military and Government | |

| Other | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.