Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

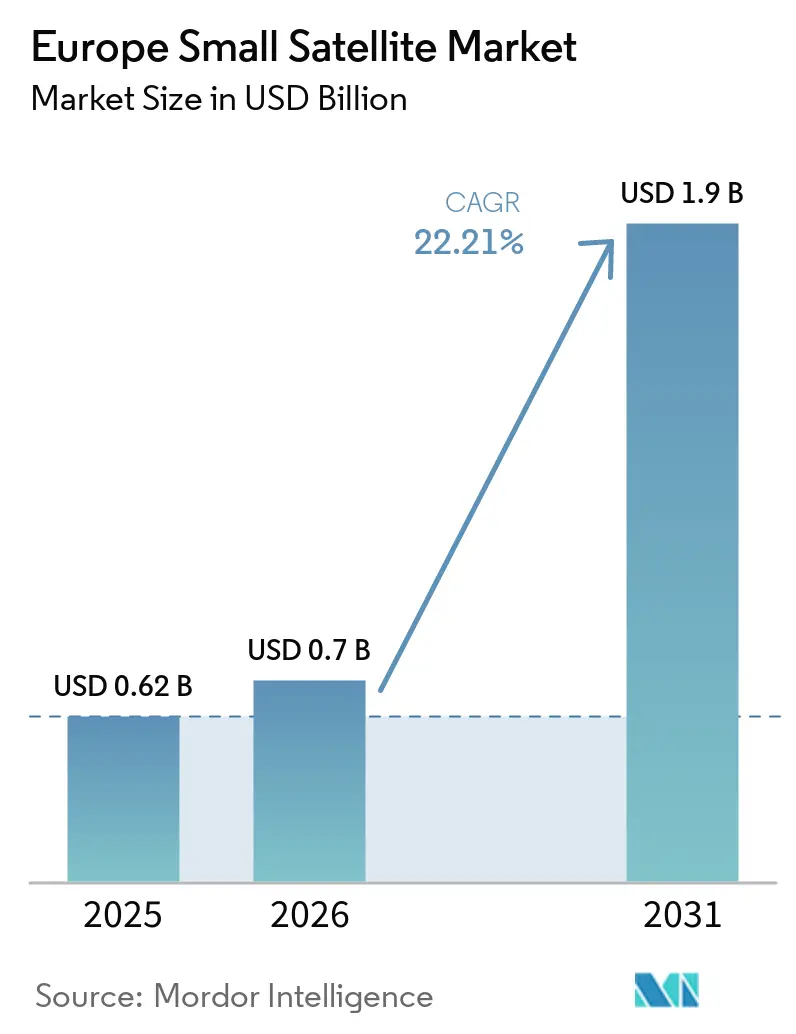

| Base Year Market Size (2025) | USD 0.62 Billion |

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 1.9 Billion |

| Growth Rate (2026 - 2031) | 22.21% CAGR |

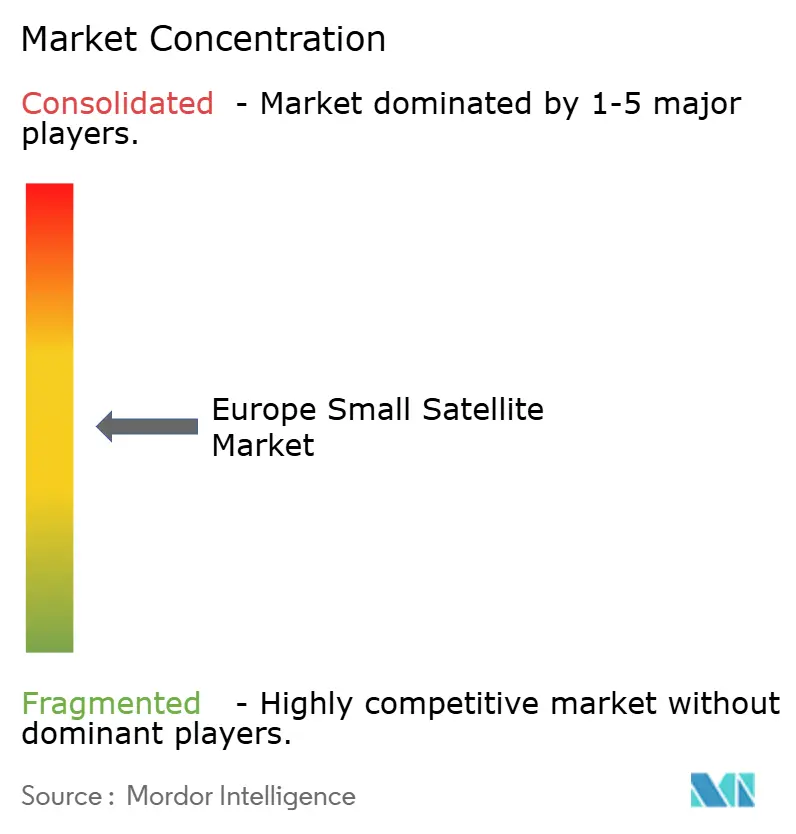

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Small Satellite Market Analysis by Mordor Intelligence

The Europe small satellite market size is projected to expand from USD 0.62 billion in 2025 and USD 0.70 billion in 2026 to USD 1.90 billion by 2031, registering a 22.21% CAGR between 2026 and 2031. The current expansion reflects a broader shift in Europe’s space posture, where defense modernization, sovereign observation needs, and a more mature commercial NewSpace base are moving in the same direction. IRIS² has become a major anchor for that shift because the EU signed the EUR 10.6 billion (USD 12.34 billion) sovereign connectivity constellation in December 2024 and is procuring 272 LEO and 18 MEO satellites, thereby creating visible institutional demand for the Europe small satellite market. Public Earth observation programs and climate monitoring requirements are also reinforcing procurement visibility, while secure connectivity programs are widening the use case for dual-use systems across civil and defense users. Execution still faces pressure because Europe entered 2026 without an operational indigenous small satellite launcher. However, CNES opened the ELM-Diamant complex in 2026, and Isar Aerospace is targeting its qualification flight in May 2026. Those bottlenecks have not changed the long-run case for the Europe small satellite market, but they have pushed more capital toward platform makers and data service providers that are less exposed to launch-scheduling risk.

Key Report Takeaways

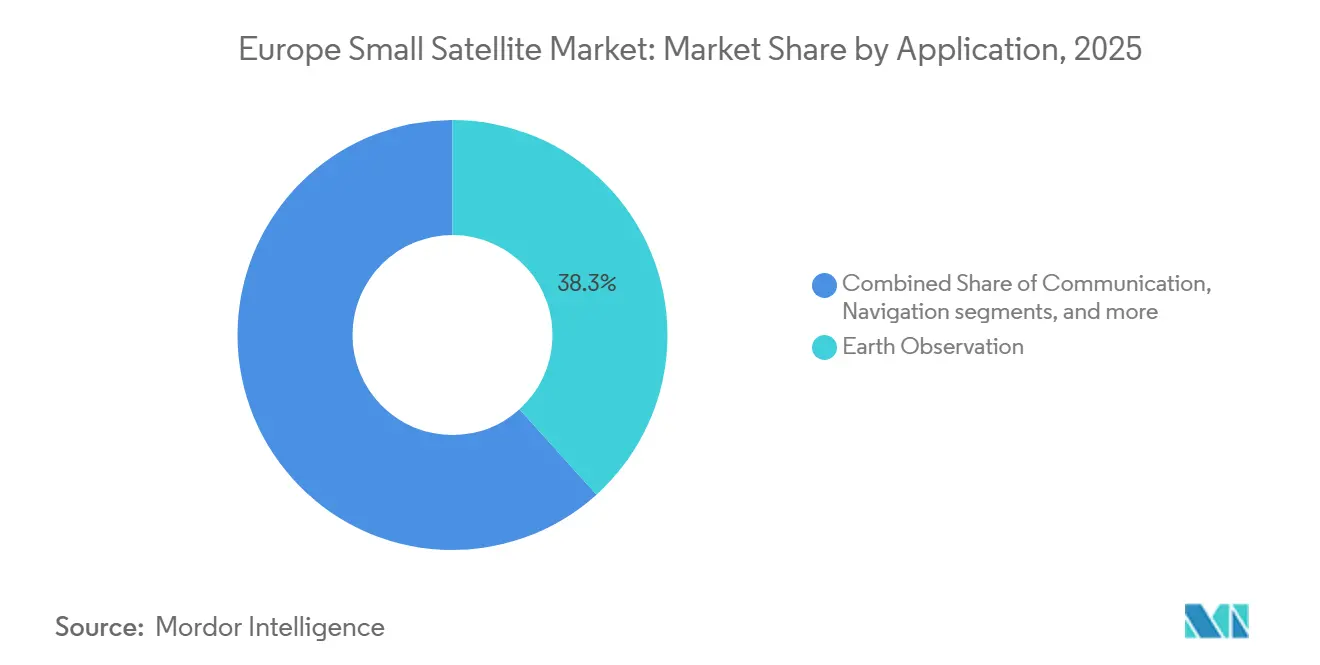

- By application, Earth observation led with 38.32% share in 2025, while communication is projected to expand at a 23.17% CAGR through 2031.

- By orbit, Low Earth Orbit (LEO) held 75.15% share in 2025, while Medium Earth Orbit (MEO) is projected to grow at a 23.81% CAGR through 2031.

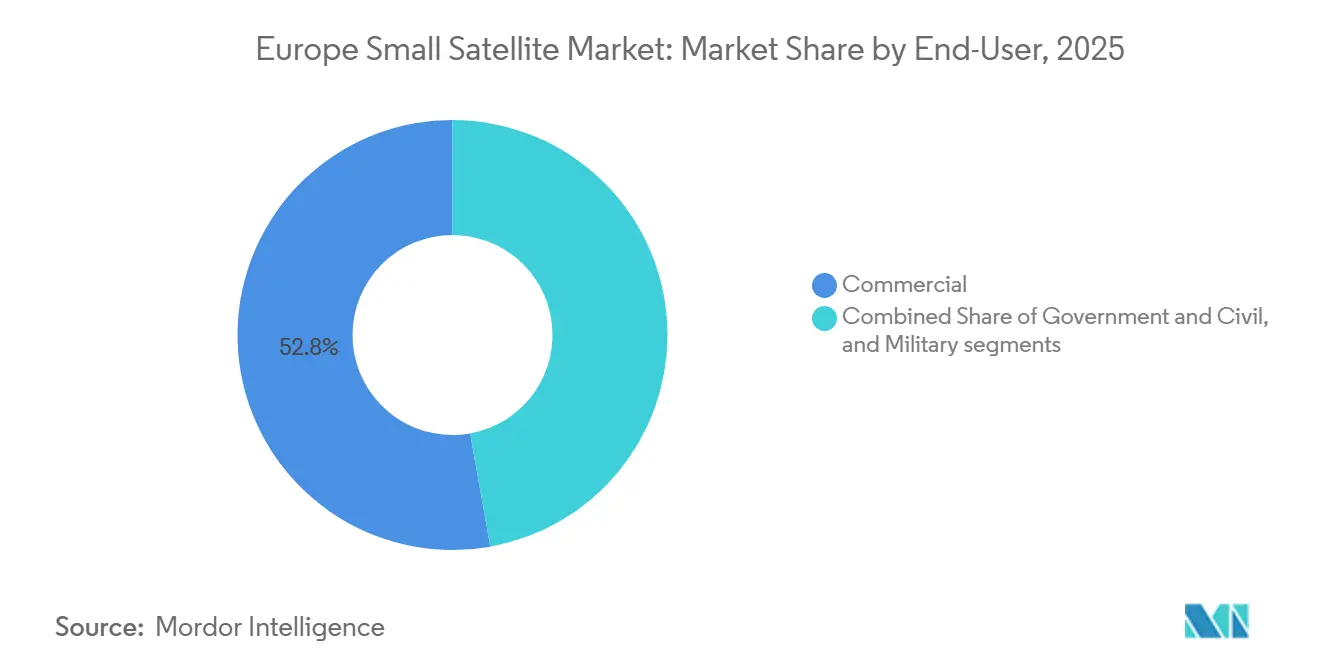

- By end-user, commercial accounted for 52.82% of the market in 2025, while military and government are projected to grow at a 24.55% CAGR through 2031.

- By satellite mass, minisatellites accounted for 44.35% of the Europe small satellite market in 2025, while nanosatellites are forecast to grow at a 25.28% CAGR through 2031.

- By geography, France held 26.45% share in 2025, while the United Kingdom is forecast to expand at a 23.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Small Satellite Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Europe Defence Fund backing small-satellite ISR assets | 5.20% | EU-27, with early gains in Germany, Poland, France | Short term (≤ 2 years) |

| Surge in European Earth-observation constellation programs | 4.50% | EU-27 core, extending to Balkans and Nordics | Short term (≤ 2 years) |

| Europe Green Deal climate-monitoring targets boosting demand | 3.10% | EU-27 core, spill-over to Balkans and Mediterranean | Medium term (2-4 years) |

| Growing venture-capital inflows into Europe NewSpace start-ups | 2.80% | Germany, Finland, France, Bulgaria, UK | Medium term (2-4 years) |

| Institutional demand for in-orbit servicing and debris removal | 2.00% | EU-27 and UK | Long term (≥ 4 years) |

| Tightened launch-window availability spurring rideshare-optimization tools | 1.80% | Continental Europe, UK, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in European Earth-observation Constellation Programs

Government-backed Earth observation constellations have become the clearest structural demand driver in the Europe small satellite market. Italy’s IRIDE program covers 68 satellites across 6 constellations, and 16 Eaglet II satellites were already in orbit by March 2026, with full deployment targeted by 2027.[1]Italian Space Agency, “IRIDE Continues Its Development: Eight More Eaglet II Satellites in Orbit,” ASI, asi.it Greece also committed EUR 130 million (USD 151.33 million) to its National Small Satellite Program, which will fund 13 satellites focused on wildfire detection, maritime awareness, and agricultural monitoring. These programs do more than create orders; they shorten technology qualification cycles for later commercial missions and lower perceived execution risk for operators entering the Europe small satellite market. European Space Agency's (ESA’s) FutureEO Scout line now includes HydroGNSS and newly approved Hibidis and SOVA-S missions, demonstrating that compact, lower-cost platforms are becoming a standard scientific option rather than a fallback.

Growing Venture-capital Inflows into Europe NewSpace Start-ups

Private capital inflows strengthened again in 2025, providing the Europe small satellite market with a broader financing base. European space ventures attracted EUR 1.4 billion (USD 1.62 billion) in private investment in 2025, while venture capital rose 13% year over year to EUR 1.2 billion (USD 1.39 billion) according to ESPI’s Space Venture 2025 report.[2]European Space Policy Institute, “Space Venture 2025,” ESPI, espi.eu Germany led that funding map, followed by Finland, France, Bulgaria, and the UK, which confirms that capital formation is spreading beyond a single national cluster. At the same time, security- and defense-oriented companies accounted for 30% of total European space investment in both 2024 and 2025, indicating that commercial and defense funding channels are increasingly converging. The funding picture remains uneven because the 5 largest rounds in 2025 accounted for EUR 629 million (USD 732.20 million), keeping smaller platform developers and data firms under pressure and raising the likelihood of consolidation across the second tier.

Europe Defence Fund Backing Small-satellite ISR Assets

The European Defence Fund has moved small satellite ISR from a niche procurement area into a core part of European defense industrial planning. Its EUR 7.3 billion (USD 8.49 billion) budget for 2021 to 2027 was followed by the 2025 work program, which earmarked EUR 66 million (USD 76.82 million) for a new LEO ISR constellation prototype and EUR 49 million (USD 57.03 million) for an on-orbit servicing feasibility study. Germany’s Ministry of Defence (MoD) then awarded a EUR 1.7 billion (USD 1.97 billion) contract in December 2025 to Rheinmetall ICEYE Space Solutions, with production of the first SAR satellite scheduled to begin in Q3 2026. That funding structure matters because institutional demand in the Europe small satellite market does not move up and down with the venture cycle in the same way that private constellations do. It also supports higher production volumes, which can lower unit costs and improve the competitive position of European suppliers in adjacent commercial work.

Europe Green Deal Climate-monitoring Targets Boosting Demand

Climate monitoring rules tied to the European Green Deal are creating a regulatory pull that is supporting the Europe small satellite market beyond normal commercial demand cycles. ESA’s Tango mission was designed to measure methane, carbon dioxide, and nitrogen dioxide at the facility level, making small satellites relevant for compliance-oriented measurement and verification tasks rather than only for broad environmental mapping. OroraTech also reached a milestone in March 2026 under ESA’s Copernicus Emerging Commercial Data Provider activity by demonstrating high-resolution thermal data for wildfire emergency response directly to Copernicus Services.[3]Copernicus Rapid Response Desk, “OroraTech’s Journey from Start-Up to Copernicus Data Provider,” Copernicus, rapidresponse.copernicus.eu The Green Transition Information Factories initiative is moving from a demonstrator phase into operational status in 2026, which widens the addressable demand base for commercial EO data providers serving public authorities and regional users. As a result, demand in the Europe small satellite market is supported by legal and policy needs as well as traditional imaging demand.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited availability and rising costs of dedicated micro-launch vehicles | -1.90% | Continental Europe, United Kingdom, Nordics | Short term (≤ 2 years) |

| Spectrum-allocation bottlenecks at ITU and CEPT | -1.20% | EU-27, with 46 CEPT member states and fragmented licensing | Medium term (2-4 years) |

| Satellite insurance premiums rising for less than 50 kg class | -1.00% | Global impact, concentrated in LEO-active regions | Short term (≤ 2 years) |

| Export-control regime divergence within Europe | -0.80% | EU-27 and UK, with crossover to NATO partners | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Availability and Rising Costs of Dedicated Micro-launch Vehicles

The most immediate structural constraint on the Europe small satellite market is the absence of an operational indigenous micro-launch option. No European micro-launcher had achieved commercial orbital delivery by early 2026, while Isar Aerospace’s Spectrum vehicle was targeting orbital qualification in May 2026, and Orbex ceased operations in February 2026. ESA responded in July 2025 by preselecting 5 companies for the European Launcher Challenge, with each eligible for contracts of up to EUR 169 million (USD 196.73 million). Until local cadence improves, operators still face scheduling dependency on US rideshares, currency exposure, and limited insurer confidence because flight heritage remains thin for new European launch systems. CNES’s ELM-Diamant complex at the Guiana Space Centre improves the physical launch base from 2026 onward, but infrastructure alone does not solve cadence in the near term.[4]National Centre for Space Studies, “ELM-Diamant Launch Complex: Space History in the Making,” CNES, cnes.fr

Satellite insurance premiums rising for less than 50 kg class

Insurance costs have become a steady drag on the Europe small satellite market, especially for nanosatellite and picosatellite operators operating in crowded LEO shells. Analysis cited in January 2026 by the Space Futures Center and the World Economic Forum found that unmanaged orbital debris could cost the sector USD 42.3 billion over the next decade, while insurance in high-density LEO zones now accounts for 5% to 10% of total mission budgets. In 2026, insurers are also requiring stronger proof of maneuverability and end-of-life disposal capability, which means compliance expectations are now shaping hardware design choices rather than sitting outside procurement decisions. That cost pressure is encouraging wider adoption of propulsion on very small platforms and strengthening the case for suppliers focused on debris mitigation and controlled deorbit capability. The UK’s GBP 75.6 million (USD 101.59 million) Active Debris Removal tender launched in 2025 also shows that governments are beginning to absorb some of the remediation burden, rather than leaving the full cost to insurers and operators.[5]UK Government, “UK Launches Tender for Mission to Clean Up Space and Safeguard Vital Services,” GOV.UK, gov.uk

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Earth Observation's Institutional Depth Contrasts with Communication's Commercial Velocity

Earth observation accounted for 38.32% of the Europe small satellite market in 2025, supported by the long procurement cycle for Copernicus-linked missions, the IRIDE deployment, and national sensing mandates. That position reflects more than current demand because many European governments now treat observation satellites as core public infrastructure rather than optional program assets. Greece’s National Small Satellite Program clearly shows that shift, with 13 satellites planned for thermal, optical, and radar monitoring under an ESA-managed framework. Airbus also strengthened the high-resolution end of this segment in January 2026, when it announced the Pléiades Neo Next program, with the first launch planned for early 2028 and 20 cm-class native-resolution imagery.

Communication is the fastest-growing application, and the Europe small satellite market size for this segment is projected to expand at a 23.17% CAGR through 2031. IRIS² remains the main anchor because its 272 LEO satellites provide the communication layer with a very large institutional backlog. At the same time, GOVSATCOM has already moved into operations and demonstrates a practical, secure connectivity use case across member states, where dual-use capability becomes more visible because the same node can support encrypted communications, maritime awareness, IoT backhaul, or sensor relay depending on the mission stack. Navigation and space observation remain smaller in absolute terms, but ESA’s Celeste constellation shows that LEO-based positioning validation is gaining policy importance within the European small satellite industry. The others category, which includes technology demonstrations and IoT missions, remains fragmented at the company level but is still building a meaningful pool of demand as device-to-satellite rules and service models mature.

By Orbit: LEO's Institutional Lock-in and MEO's Emerging Strategic Role

Low Earth Orbit (LEO) held a 75.15% share in 2025 and remains the clear operational center of the Europe small satellite market because it meets the revisit, latency, and launch-cost needs of Earth observation, IoT, and secure communications. Italy’s IRIDE program shows how deeply this orbit is now embedded in public procurement, with 16 Eaglet II satellites already in orbit by March 2026 and a path to 68 satellites across 6 constellations. The same density that makes LEO commercially attractive is also raising its operating burden, since conjunction avoidance and debris exposure are now affecting lifetime assumptions and insurance pricing. GEO still matters for legacy broadcast and fixed broadband services, but it is not where incremental growth is occurring in the European small-satellite class.

Medium Earth Orbit (MEO) is the fastest-growing orbit, and the Europe small satellite market size for this layer is projected to rise at a 23.81% CAGR through 2031. The main demand logic comes from IRIS²’s hybrid architecture with 18 MEO satellites, continued Galileo second-generation development, and ESA’s Celeste demonstration work on hybrid signal delivery. Coordination procedures for non-GSO systems also matter here because regulatory lead times of 2 to 5 years increasingly favor operators that filed early and can move faster through spectrum coordination. Europe is also testing lower operating bands through the European Defence Agency’s LEO2VLEO effort and the VLEO-DEF contract signed in March 2026, which may add a commercially relevant orbit class within the forecast window. Even so, LEO and MEO together remain the main growth path for the Europe small satellite market through 2031.

By End-User: Commercial Consolidation Masks a Military Acceleration Underneath

Commercial users accounted for 52.82% of the end-user split in 2025, reflecting the combined weight of platform manufacturers, EO data firms, IoT operators, and connectivity ventures selling services to both public and private buyers. This share is reinforced by dual-use contract structures in which commercial firms provide sovereign or defense capabilities through service agreements rather than through direct state ownership. ESPI reported that security- and defense-oriented companies accounted for 30% of total European space investment in both 2024 and 2025, indicating that commercial capital is increasingly underwriting national security missions. The accounting effect matters because part of that revenue still enters the commercial column even when the end use is closely tied to state security needs.

The military and government sector is one of the fastest-rising end-user pools, with a 24.55% CAGR through 2031, matching the pace of the commercial side rather than trailing it. Poland’s MikroSAR procurement from ICEYE in May 2025 and delivery of a 4-satellite SAR system in May 2026 within 12 months show how defense users are now relying on commercial manufacturing pipelines for rapid sovereign capability build-out. The other end-user group, which includes universities, research institutes, and intergovernmental bodies, still plays a useful incubation role for the Europe small satellite industry. ESA’s CleanCube activity supports that role by co-funding Zero Debris nanosatellite platforms and linking experimental missions with future product pathways. That mix keeps the Europe small satellite market broad-based, even as defense demand rises more quickly within the overall revenue pool.

By Satellite Mass: Minisatellites Hold Scale While Nanosatellites Redefine the Cost Curve

Minisatellites held 44.35% share in 2025 and remain the workhorse class for high-value Earth observation and defense ISR missions in the Europe small satellite market. Their 100 kg to 500 kg range allows for higher-end payloads, including high-resolution optical systems and SAR packages that still exceed what most smaller buses can deliver. ICEYE’s fourth-generation SAR satellites illustrate that staying power because the company has pushed resolution to 16 cm from platforms weighing around 200 kg, keeping the minisatellite class commercially relevant even as smaller buses improve. Large institutional programs such as Germany’s Rheinmetall ICEYE constellation also support this mass category because mission assurance and payload performance remain more important than absolute unit count for many sovereign ISR buyers.

Nanosatellites are the fastest-growing mass category, and the Europe small satellite market size for nanosatellites is projected to expand at a 25.28% CAGR through 2031. That growth is linked to standardized CubeSat buses, lower entry costs for constellation builds, and the ability to replace failed assets quickly without the financial exposure associated with larger spacecraft. GomSpace, NanoAvionics, and EnduroSat have helped industrialize the 6U to 16U format, which makes 20-satellite to 50-satellite constellation concepts realistic for national agencies and smaller operators. ESA’s CleanCube program is reinforcing that shift by tying in-orbit demonstration work to Zero Debris design rules ahead of a competitive in-orbit demonstration path by 2027. Microsatellites remain an important bridge class, as shown by Spain’s GARAI-A and GARAI-B missions in the 20 kg to 30 kg range, while femtosatellites and picosatellites continue to be concentrated in demonstration and academic use rather than near-term revenue generation.

Geography Analysis

France held 26.45% of Europe small satellite market share in 2025, supported by its deep manufacturing base, CNES-backed procurement channels, and long-standing presence in both civil and defense programs. That position is reinforced by France’s role as an anchor market for Airbus Defence & Space and Thales Alenia Space, which gives the country a persistent advantage in multi-year institutional contracts. CNES also signed a multi-year France 2030 contract with Loft Orbital and Magellium Artal Group for a next-generation EO constellation, with the first satellite scheduled for Q4 2026. France’s depth matters to the Europe small satellite market because it links public funding, manufacturing capability, and downstream data applications in one national ecosystem. That combination helps France sustain leadership even as other countries accelerate.

The Europe small satellite market size for the UK is projected to advance at a 23.9% CAGR through 2031. UK entities contributed to the launch of more than 1,000 spacecraft between 2010 and mid-2025, and more than three-quarters were commercial, suggesting a stronger private-sector tilt than among most European peers. The UK government added GBP 500 million (USD 674.64 million) for the sector in 2025, including GBP 65 million (USD 87.37 million) for the National Space Innovation Program and GBP 40 million (USD 53.97 million) for the Unlocking Space Program. SaxaVord Spaceport is expected to host the United Kingdom’s first vertical orbital launch attempts in 2026, which could materially improve domestic launch autonomy if execution holds. The country is also building a strong servicing niche through its Active Debris Removal tender and Astroscale UK’s ELSA-M design progress.

Germany ranked third in 2025 but remains one of the strongest rising demand centers in the Europe small satellite market because sovereign security programs are expanding and pulling more suppliers into defense-linked contracts. The Rheinmetall ICEYE constellation, additional SPOCK-related activity, and Airbus-led military LEO communication plans all point to sustained demand for satellite buses and subsystems across the wider European supply chain. Poland, Finland, Spain, and the Netherlands are also becoming credible second-tier demand centers through MikroSAR, GARAI, the Canary Islands constellation, and specialist manufacturing capabilities. Russia’s role in the Europe small satellite market has weakened since 2022 as institutional partnerships and joint activity shifted toward EU-based alternatives, while the rest of Europe continues to add depth through focused capabilities in Finland, the Netherlands, Italy, and Belgium.

Competitive Landscape

The Europe small satellite market is moderately fragmented at the platform layer and more concentrated at the mission-prime layer, where Airbus SE, OHB SE, and Thales Alenia Space continue to anchor major institutional programs. A clear shift from 2024 to 2026 has been toward service-led business models, with firms selling data access, constellation capacity, or mission support rather than one-off hardware. ICEYE is the strongest example because its 2025 revenue reached EUR 250 million (USD 294.02 million), profit exceeded EUR 100 million (USD 116.40 million), and backlog exceeded EUR 1.5 billion (USD 1.74 billion), driven by defense service contracts rather than simple satellite sales. Its German manufacturing joint venture with Rheinmetall and the SPOCK 1 program, running to 2030, has given it a durable position in European SAR competition. That combination makes the Europe small satellite market more difficult for smaller SAR challengers that lack either defense access or manufacturing scale.

White-space opportunities remain visible in propulsion systems for post-mission disposal, rideshare optimization software, and data fusion platforms that combine optical, SAR, and hyperspectral feeds into a more usable commercial product. Exotrail and similar suppliers are well-positioned in propulsion, as debris rules and insurance requirements are pushing controlled maneuverability closer to a standard feature. Planet Labs PBC also remains a useful benchmark for European Earth observation competitors because it has meaningful relationships with government and commercial buyers across the region. Mid-tier companies such as SatRev and Berlin Space Technologies face a narrow strategic choice: scale-up constellation manufacturing or be absorbed into larger prime structures. The Europe small satellite market is therefore not only growing in value but also consolidating around firms that can combine technical specialization with public-sector credibility.

Strategic activity since 2025 supports that pattern. Airbus strengthened its dual-use imaging position with the announcement of Pléiades Neo Next in January 2026. Loft Orbital deepened its French public-sector access through a France 2030 EO constellation contract with CNES, and ESA’s RISE mission reached its Systems Requirements Review in September 2025, which keeps in-orbit servicing open as a future competitive adjacency with no single dominant incumbent yet. Over the forecast period, the Europe small satellite market is likely to see more alliances and selective consolidation than pure greenfield expansion.

Europe Small Satellite Industry Leaders

Airbus SE

OHB SE

Thales Alenia Space

GomSpace A/S

AAC Clyde Space AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ICEYE delivered its MikroSAR sovereign radar satellite reconnaissance system to the Polish Armed Forces in under 12 months from contract signing, with 4 SAR satellites built and launched. According to ICEYE, this represents the fastest operational satellite program deployment globally and the fastest procurement program in the history of the Polish military, establishing a new benchmark for European small-satellite delivery timelines.

- May 2026: Telespazio Ibérica was awarded a EUR 20 million (USD 23.28 million) contract to develop the Canary Islands satellite constellation, Spain’s first autonomous-community-owned Earth observation system, comprising 3 operational satellites and 1 demonstrator in LEO at 450 km to 700 km, each weighing 20 kg to 30 kg. The contract was announced at SSSIF Málaga 2026 and positions Spain as a growing actor in satellite procurement beyond national agency budgets.

- March 2026: ASI and ESA launched 8 additional Eaglet II satellites for Italy’s IRIDE constellation, bringing the total Eaglet II count to 16 in orbit. The IRIDE program is targeting 68 satellites across 6 constellations, with full deployment by 2027, establishing Italy as one of the largest multi-application small-satellite constellation operators in Europe.

- March 2026: The European Defence Agency signed a USD 18.27 million research contract with an industrial consortium for VLEO-DEF, the design of Europe’s first military satellite concept, specifically optimized for Very Low Earth Orbit (VLEO) at altitudes of 250 km to 350 km. Funded by 5 member states and running for 36 months, the project builds on the LEO2VLEO initiative launched in 2024.

Europe Small Satellite Market Report Scope

Small satellites are those satellites weighing under 500 kg. The small satellite market report excludes sounding rockets, high-altitude balloon platforms, and purely experimental payloads.

The Europe small satellite market is segmented by application, orbit, end-user, satellite mass, and geography. By application, the market is segmented into communication, Earth observation, navigation, space observation, and others. By orbit, the market is segmented into low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary orbit (GEO). By end-user, the market is segmented into commercial, government and civil, and military. By satellite mass, the market is segmented into femtosatellites, picosatellites, nanosatellites, microsatellites, and minisatellites. The report also covers the market sizes and forecasts for the Europe small satellite market in six countries across the region. For each segment, the market size is provided in terms of value (USD).

By Application

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

By Orbit

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geostationary Orbit (GEO) |

By End-User

| Commercial |

| Government and Civil |

| Military |

By Satellite Mass

| Femtosatellites |

| Picosatellites |

| Nanosatellites |

| Microsatellites |

| Minisatellites |

By Geography

| United Kingdom |

| France |

| Germany |

| Russia |

| Rest of Europe |

| By Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others | |

| By Orbit | Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) | |

| Geostationary Orbit (GEO) | |

| By End-User | Commercial |

| Government and Civil | |

| Military | |

| By Satellite Mass | Femtosatellites |

| Picosatellites | |

| Nanosatellites | |

| Microsatellites | |

| Minisatellites | |

| By Geography | United Kingdom |

| France | |

| Germany | |

| Russia | |

| Rest of Europe |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.