Europe Ready-to-Assemble (RTA) Furniture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

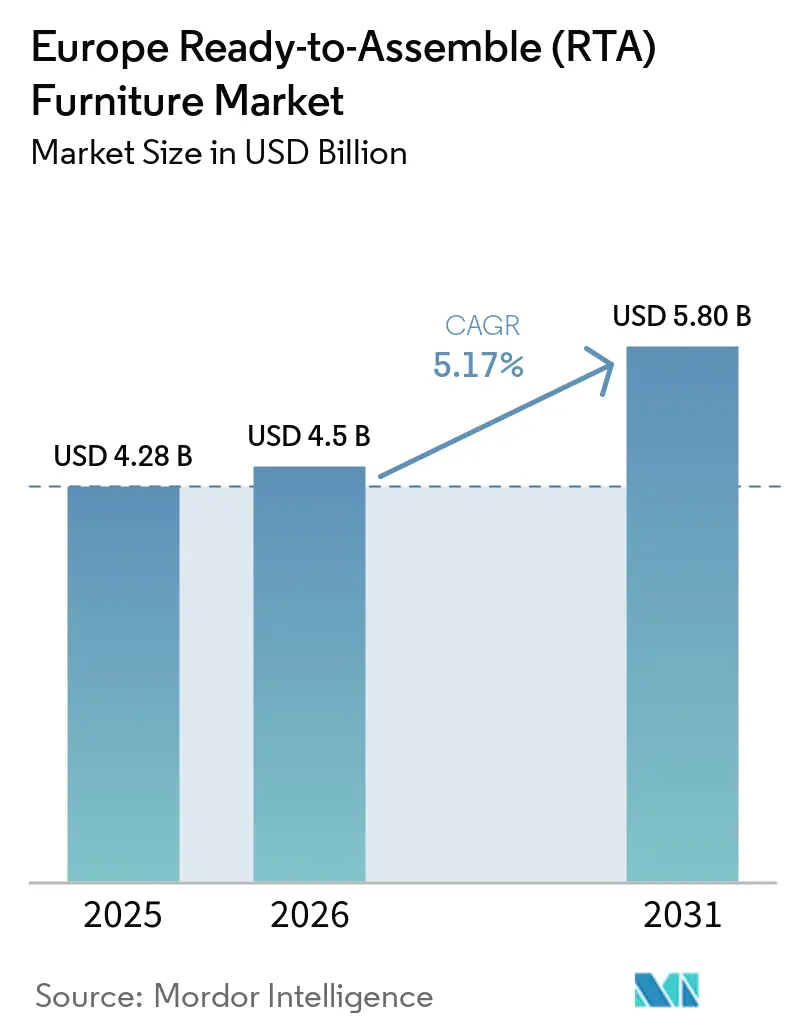

| Base Year Market Size (2025) | USD 4.28 Billion |

| Market Size (2026) | USD 4.5 Billion |

| Market Size (2031) | USD 5.80 Billion |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ready-to-Assemble (RTA) Furniture Market Analysis by Mordor Intelligence

The Europe Ready-to-Assemble (RTA) furniture market size is expected to increase from USD 4.28 billion in 2025 to USD 4.50 billion in 2026 and reach USD 5.8 billion by 2031, growing at a CAGR of 5.17% over 2026-2031. Product design is shifting toward tool-free assembly and modular construction to cut returns and support circular resale and refurbishment pathways, with several leading manufacturers rolling out 2026 lines optimized for quick disassembly. Pricing resets across leading retailers are now a structural lever to widen affordability, which has tightened margins but unlocked higher unit throughput in key categories. Hybrid work patterns continue to drive demand for ergonomic desks and task seating that meet compliance-grade standards in home settings, while visualization and augmented-reality tools lower friction for the digital purchase of larger flat-pack pieces. A steady pivot to recycled plastics and circular feedstocks is also underway, partly to simplify compliance workloads associated with wood traceability while maintaining durable, value-priced SKUs. Near-term store-network changes, including smaller-format locations and click-and-collect nodes, are lifting accessibility and reinforcing omnichannel convenience for the European ready-to-assemble furniture market.

Key Report Takeaways

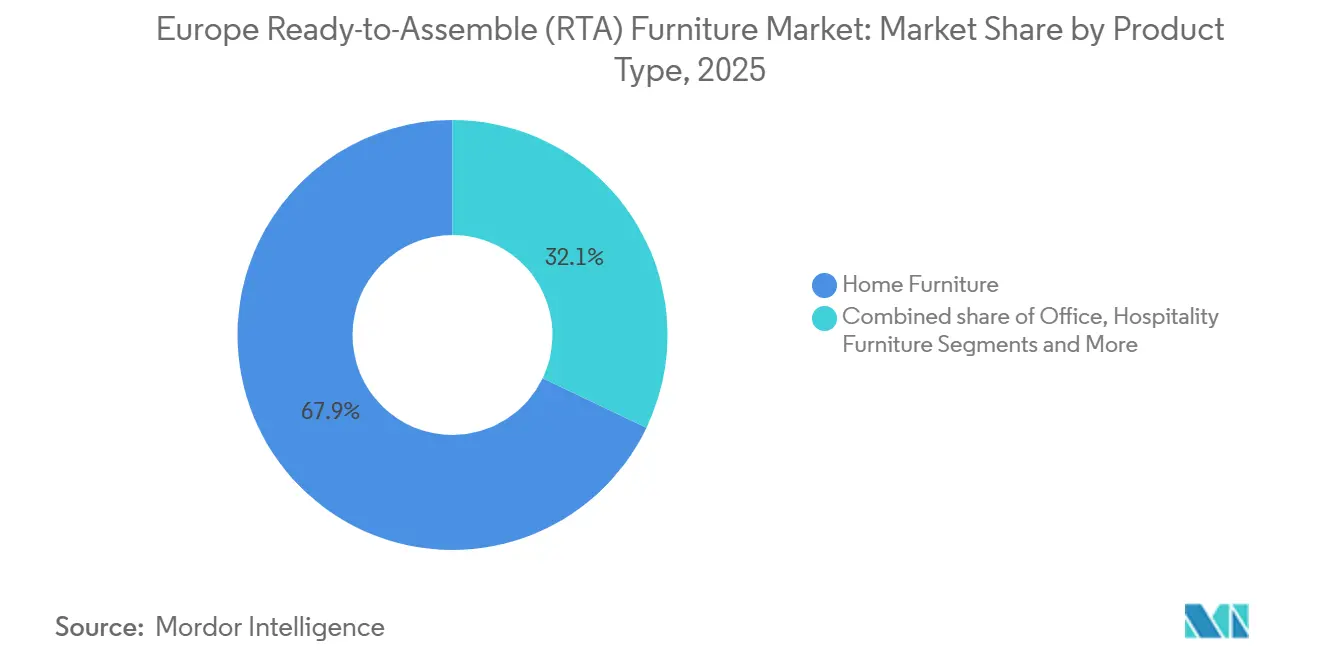

- By product type, home furniture led with 67.85% of the European ready-to-assemble furniture market share in 2025, while office furniture is projected to expand at a 6.55% CAGR through 2031.

- By material, wood dominated the European ready-to-assemble furniture market with 56.62% in 2025 across mass and mid-market assortments, whereas plastic is forecast to grow at a 7.03% CAGR through 2031.

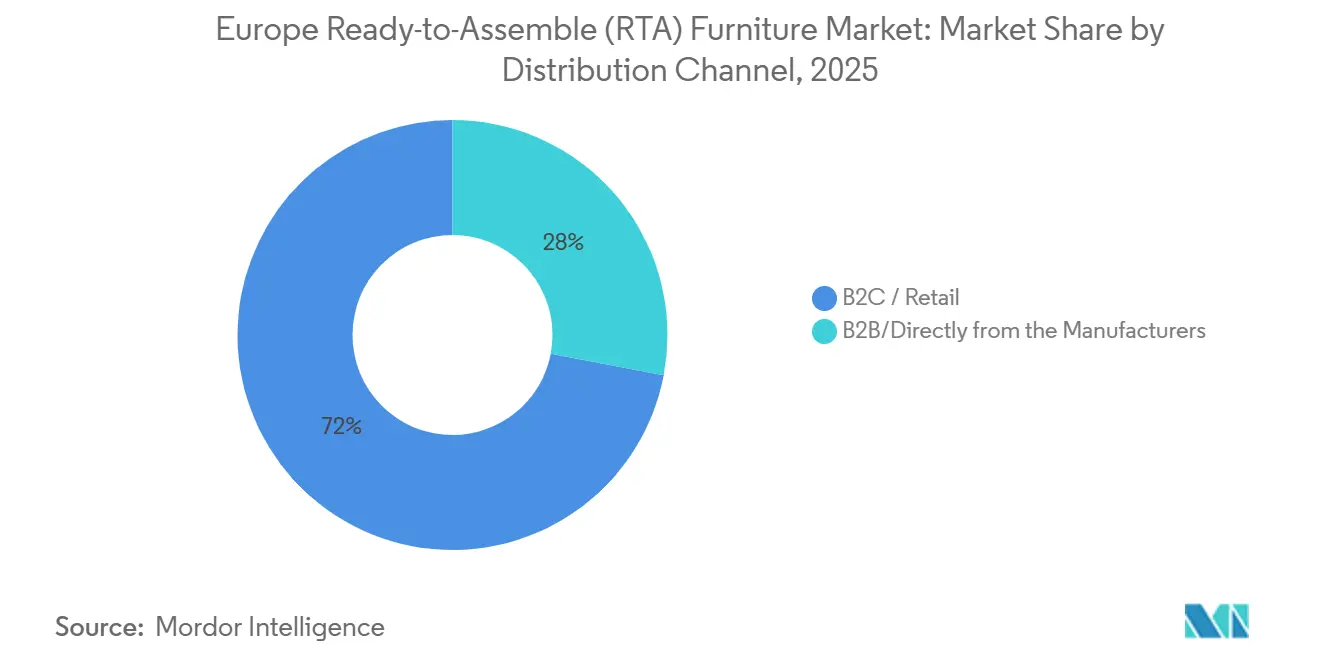

- By distribution channel, B2C retail remained the dominant route to the Europe-ready-to-assemble furniture market in 2025, accounting for 72.00%, while business-to-business demand is witnessing accelerated growth at a 6.27% CAGR through 2031, driven by modular room packages and circular take-back models.

- By geography, Germany accounted for 22.37% of the European ready-to-assemble furniture market in 2025, while Italy is expected to register notable growth of 5.42% through 2031, supported by factory innovation and export-oriented modular assortments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Ready-to-Assemble (RTA) Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce scaling and omnichannel logistics lower CAC and last-mile costs for flat-pack SKUs | +1.2% | Global, with the highest penetration in the United Kingdom (>30% online share), Germany, Nordics | Medium term (2-4 years) |

| Shrinking urban living spaces increase demand for modular, space-saving RTA formats | +0.9% | APAC core, spill-over to Western Europe | Medium term (2-4 years) |

| Hybrid work sustains home-office RTA demand (desks, storage, ergonomic add-ons) | +1.3% | Nordics, UK, Germany, France | Short term (≤ 2 years) |

| DIY/organized specialist and DIY retail push (private label breadth, price points) | +0.7% | Germany, UK, France | Short term (≤ 2 years) |

| EU circularity preferences favor easy-to-disassemble, repairable designs | +0.8% | EU-27, spill-over to the UK | Long term (≥ 4 years) |

| Nearshored CEE supply clusters improve lead times and resilience | +0.6% | Regional, benefiting Western hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Scaling and Omnichannel Logistics Lower CAC and Last-Mile Costs for Flat-Pack SKUs

The Europe ready-to-assemble furniture market benefits directly from rising digital penetration and improved online conversion driven by richer content and checkout experiences. Leading retailers report growing online engagement alongside stable store footfall, indicating that smaller-format stores, click-and-collect, and parcel-friendly flat-pack SKUs are reinforcing reach without imposing heavy delivery surcharges. The 2025 trading year saw online visits rise, while the online share approached one-third of sales for one of the largest banners, affirming the fit between compact RTA parcels and urban distribution networks. Players like IKEA, with their flat-pack product design, are capitalizing on the surge in online sales of RTA furniture. The compact, modular design of RTA furniture not only fits seamlessly into urban logistics networks but also boosts online sales and simplifies last-mile delivery in crowded urban areas.[1]Ingka Group Newsroom, “IKEA serves more customers and increases volumes in a challenging year,” Ingka Group, ingka.comRich visualization and augmented-reality workflows are also becoming mainstream as furniture sellers standardize 3D assets and mobile-first pathways, which reduces returns and assembly disputes while enabling confident purchases of higher-ticket flat-pack items. Together, these factors compress cost to serve and reduce customer acquisition cost for the Europe-ready-to-assemble furniture market, as repeatability in the last mile and returns enable scale.

Hybrid Work Sustains Home-Office RTA Demand (Desks, Storage, Ergonomic Add-Ons)

Hybrid work patterns keep a consistent floor of demand for compliant desks, storage, and ergonomic seating, which supports premium RTA configurations priced well above entry-level kits. Within the European ready-to-assemble furniture market, many of these purchases are planned replacements funded by remote work allowances or self-directed investment by professionals who now value ergonomic continuity at home. Demand is also supported by the steady refinement of smart adjustability and cable management, which increasingly comes pre-engineered into mid-range products. Several European suppliers have showcased upgraded mechanisms and digital integration features in the 2025 and 2026 cycles, signaling a broadening of smart benefits into flat-pack. This dynamic is reflected in sustained mid-to-high single-digit growth forecasts for office-oriented lines inside the overall RTA mix through 2031. As a result, the Europe ready-to-assemble furniture market continues to see above-baseline growth in the home-office segment as households finalize permanent workspace setups[2]Vidojevic Biljana, “The State of the Furniture Industry and How to Excel in 2026,” Cylindo, cylindo.com.

DIY/Organised Specialist and DIY Retail Push (Private Label Breadth, Price Points)

DIY and specialist chains are expanding private-label RTA offerings and improving circularity stories around plastics and returns logistics. One large home-improvement banner piloted in-store collection of hard plastics with conversion into new organizers priced for mass adoption, a model now scaling in Europe to bolster affordability and feed recycled content targets. In the RTA furniture segment, DIY retailers like Leroy Merlin are adopting circular supply models. Take, for example, Leroy Merlin's partnership with FINSA in Spain, dubbed the “Circlewood” initiative. Here, wood waste from stores gets transformed into chipboard panels. These panels subsequently serve as the foundation for crafting furniture items, including kitchen units and storage systems. This strategy not only bolsters the expansion of private labels but also aligns with sustainability goals and enhances cost efficiency.[3]Keter Group Sustainability Team, “Sustainability Report 2024,” Keter Group, ketergroup.com. This behavior aligns well with RTA, as private-label kits can maintain low price points even as raw material and compliance overheads fluctuate. It also exploits cross-category traffic at home centers where shoppers add flat-pack storage or shelving to baskets built around paint, flooring, or hardware. By combining closed-loop plastics, modular designs, and low-friction returns through existing reverse logistics, this channel configuration favors high-velocity SKUs suited to urban apartments. These mechanics collectively sustain steady unit growth for the Europe-ready-to-assemble furniture market in store-based and omnichannel formats.

EU Circularity Preferences Favor Easy-to-Disassemble, Repairable Designs

Design-for-disassembly is becoming a default brief for 2026 collections across leading European manufacturers, with tool-free joints, repairable modules, and spare parts availability improving the second and third life of products. One major kitchen and cabinet producer introduced rotating-cabinet systems, corner solutions, and wider base-cabinet formats that improve access, cut installation friction, and raise storage flexibility without relying on complex hardware bags. These patterns are intended to shrink returns linked to missing fasteners or misapplied torque and to simplify refurbishment when pieces are resold or recovered under take-back. At the same time, large-scale retail banners are expanding buyback and pre-owned marketplaces. They are investing in recycling infrastructure for plastics and mattresses to close material loops at scale by 2030. The combination of modular cabinet geometries, QR-coded parts catalogs, and in-market refurbishment flows reduces total ownership cost and aligns with consumer expectations for circular value. As these practices diffuse across price points, they support loyalty and repeat purchases in the European ready-to-assemble furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight timber supply and compliance raise input and audit costs | -1.4% | EU-27, with acute pressure in key wood-processing regions | Short term (≤ 2 years) |

| Consumer pain points in assembly and returns for complex SKUs | -0.6% | Germany, UK, France | Medium term (2-4 years) |

| Aggressive price investments by large-format retailers intensify margin pressure | -0.9% | Pan-European, most acute in Western Europe | Short term (≤ 2 years) |

| Demand softness and concentration risk in mature Western hubs | -0.5% | Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Pain Points in Assembly and Returns for Complex SKUs

Complex wardrobes, drawer banks, and multi-panel systems can lead to assembly errors and extended installation time, which increases support tickets and the odds of returns. Tool-free mechanisms and improved hinge geometries are being introduced to reduce the reliance on large hardware kits and to simplify alignment in tight spaces. Several 2026 cabinet innovations now target wider opening angles and rotating access to minimize mis-assembly while preserving storage volume. These changes are designed to reduce returns due to missing parts, unclear instructions, or misapplied hardware, and to support reassembly when households relocate. As brands add QR-coded parts catalogs and clearer guidance, they also set the stage for circular take-back and refurbishment services that depend on fast, reliable disassembly. These steps ease friction for the Europe-ready-to-assemble furniture market by lowering service burden and lifting first-time-right outcomes[4]Nobilia Editorial Team, “Kitchen novelties 2026,” Nobilia, nobilia.de.

Aggressive Price Investments by Large-Format Retailers Intensify Margin Pressure

Two significant rounds of price reductions during 2024 and 2025 brought shelf prices closer to pre-pandemic levels at Europe’s largest home-furnishings retailer. The move benefited consumers with lower outlays across thousands of RTA and home lines, yet it compressed industry operating margins among peers that lack integrated material supply and scale procurement. FY25 results showed a modest decline in retail sales value while quantities sold and visits rose, indicating that price investments supported unit growth and traffic despite revenue pressure. Store expansion also continued, with dozens of new locations and higher online visits, which together underscore the scale advantages that enable sustained price actions. Competitors seeking to protect share responded with greater private-label depth and faster cost-down automation, but many face a choice between price matching and protecting margins. These conditions elevate the role of nearshored manufacturing, recycled feedstocks, and design simplification to preserve cost positions within the European ready-to-assemble furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Office Furniture Propels Hybrid-Work Refresh

Home furniture accounted for 67.85% of 2025 revenue as households completed deferred upgrades and compact-living improvements, while office furniture is forecast to expand at a 6.55% CAGR through 2031 in step with normalized hybrid schedules and sustained ergonomic investment. The Europe-ready-to-assemble furniture market continues to see replacement cycles migrate into 2024 and 2025, with consumers prioritizing functional refreshes that fit smaller footprints and multipurpose use. Within home furniture, modular tables, storage, and beds carry volume, while wardrobes and kitchen fixtures drive value through thicker boards, improved finishes, and better hardware. The Europe-ready-to-assemble furniture market for office-oriented categories is projected to grow more rapidly, as remote professionals invest in compliance-grade chairs and desks to formalize workspace ergonomics. Height presets, cable management, and smarter adjustment are becoming standard in the mid-range, which raises willingness to pay and supports premium cadence in the category. Brands that streamline assembly for these feature-rich products tend to reduce returns and protect margins as they add weight and complexity to higher-tier kits.

The Europe-ready-to-assemble furniture market leverages broad home demand, while office subcategories benefit from durable hybrid behavior. Chairs, desks, and storage that meet recognized ergonomics standards are spreading into price bands reachable by self-funded home offices, which increases the mix value. For home categories, modular units, reconfigurable shelves, and lighting-integrated panels reinforce appeal in small apartments where rooms play multiple roles over a week. Hospitality refresh cycles are also oriented toward modularity and circular take-back, a pattern that supports predictable quality and higher specification consistency over longer contract horizons. Educational and healthcare applications remain smaller within RTA but continue to require durable, wipeable surfaces and safe edges at accessible price points, which depend on efficient flat-pack engineering.

By Material: Plastic Advances on Compliance, Simplicity, and Circular Content

Wood dominated the European ready-to-assemble furniture market, accounting for 56.62% in 2025 across mass and mid-market assortments. Plastic is projected to expand at a 7.03% CAGR as recycled polypropylene and PET gain share in outdoor and indoor storage kits where durability, water resistance, and price hold priority. The Europe-ready-to-assemble furniture market benefits from recycled-content scale-ups at major manufacturers that can feed consistent resin grades into high-volume SKUs. One European producer documented rising recycled content across its portfolio and zero-waste-to-landfill at several plants, signaling operational readiness for mainstream circular plastics use. These improvements sit alongside innovations in composite materials derived from beverage-carton waste streams, which can be molded into durable planters and organizers at mass-market price points. As plastic designs standardize modular fittings and repairable parts, they match consumer expectations for quick assembly and reuse while dodging complex wood-traceability workflows. This supports healthy assortment growth in value tiers and aligns with retailer sustainability narratives across the European ready-to-assemble furniture market.

Wood remains central to the aesthetic appeal and perceived quality of cabinets, wardrobes, and tables, supported by modern machining that enables precise flat-pack fits. The European ready-to-assemble furniture market balances this with the availability of certified sources and efficient panel processing for consistent board quality at scale. Manufacturers also integrate metal and glass selectively, adding reinforcement in load-bearing structures and transparency where designs call for lighter spaces. Continued product advances in hinges and lift mechanisms enable better function in wood-heavy pieces while keeping assembly intuitive and repair-friendly. Where recycled plastics can replace non-structural elements, brands can reduce cost volatility and emphasize circular value without compromising core design language. The blend of wood’s warmth and plastics’ circular credentials now shapes the material roadmap for the Europe-ready-to-assemble furniture market through the forecast period.

By Distribution Channel: B2C Retail Dominance Faces B2B Disruption

B2C retail captures 72.00% of the European ready-to-assemble furniture market share, big-box DIY chains, and web-first specialists, where shoppers compare finishes across price tiers in one visit. Yet B2B direct revenue is on a 6.27% CAGR trajectory through 2031 as manufacturers court landlords, outfitting hundreds of build-to-rent flats at once. One leading retailer expanded its network with compact stores that hold 2,000 to 4,000 square meters, supporting curated assortments and flexible pickup in suburban nodes. Concurrently, business-to-business demand accelerated as hospitality groups and multifamily developers favored modular packages with installation, maintenance, and take-back clauses that shift costs from capex to opex. This channel structure rewards suppliers that can guarantee right-first-time deliveries, clear instructions, and predictable refurbishment flows suitable for redeployment. Growth in B2B within the European ready-to-assemble furniture market also reflects the appeal of standardized room sets that can be scaled quickly across properties and refreshed without landfilling.

The European ready-to-assemble furniture industry is increasingly shaped by the economics of service for enterprise buyers. As take-back programs expand and pre-owned marketplaces grow, retailers and manufacturers can close loops while preserving material value at the end of the first life. For consumers, RTA continues to benefit from improved visualization and store footprints that reduce friction at the point of decision, including mobile-first pathways that support quick comparison. Brands that harmonize packaging for easy parcel shipping and automated returns achieve better unit economics through urban sortation hubs. Meanwhile, business-to-business buyers value predictable component availability and long-term parts catalogs that reduce downtime and support environmental reporting. These changes are consolidating the strategic role of RTA assortments across both channels within the Europe ready to assemble furniture market.

Geography Analysis

Germany commands 22.37% of the European ready-to-assemble furniture market in 2025, supported by a sophisticated logistics grid linking Central European panel mills to dense retail clusters. In January 2024, prices were reduced on thousands of SKUs in Germany and neighboring markets, which rebalanced affordability during a challenging inflationary period. FY25 results showed a modest drop in sales value despite gains in quantities and visits, implying that price investments boosted traffic and unit throughput even as revenue compressed. The planned 2026 expansion of smaller urban stores across Germany and adjacent countries supports localized convenience and faster pickup options for RTA purchases. German supply partners are also rolling out 2026 product updates to improve access angles, reduce reliance on hardware, and support tight-space layouts, thereby boosting perceived value without inflating assembly time. Together, these steps frame Germany as both a demand anchor and a product-innovation customer base for the Europe-ready-to-assemble furniture market.

Italy, forecast to grow at a 5.42% CAGR (2026-2031), benefits from urbanization around Milan, Rome, and Naples, where rental listings spike and graduates share flats for longer. Product launches for 2026 feature diagonal cabinets for tight corners, wider base units for flexible layouts, and dynamic rotating base solutions that ease access in compact kitchens, all of which favor installation speed and fewer moving parts. These functional upgrades address both residential and contract needs, enabling repeatable fit-outs and lower return rates on complex orders. At the same time, the shift toward modular pieces supports take-back and refurbishment models that are gaining adoption in hospitality. As such, Italy’s product and production advantages align tightly with growing circular preferences and the logistics realities of cross-border e-commerce in Europe. This setup supports a resilient foothold for Italian suppliers within the Europe-ready-to-assemble furniture market.

Northern Europe and Benelux sustain high digital engagement and strong do-it-yourself cultures that reward compact, modular storage solutions and quick assembly. Retailers in these regions continue to expand pre-owned marketplaces and circular services, which benefit RTA designs engineered for disassembly and repair. In parallel, new small-format stores are opening in Sweden and across Western Europe, shortening travel times and supporting hybrid click-and-collect behavior among urban households. In Central and Eastern Europe, manufacturers are central to European supply strategies, with Scandinavian distributors reinforcing their footprint through acquisitions in Poland to improve speed and control over upholstery and flat-pack components. Circular plastics initiatives are also scaling across Spain, Portugal, and the United Kingdom, where planters and organizers made from recycled materials align with policy direction on packaging and waste. These geographic patterns illustrate how policy, product engineering, and network choices reinforce one another in the Europe-ready-to-assemble furniture market.

Competitive Landscape

Competitive intensity remains moderate as the leading European banner leans into affordability through large-scale price investments and a widening mix of store formats, hence the market is moderately fragmented. FY25 performance confirmed that price cuts brought value down even as unit volumes and traffic improved, suggesting that the model can be self-reinforcing when combined with broad omnichannel reach. Smaller urban stores slated for 2026 will add density around existing big-box anchors and regional e-commerce nodes, which further improves the cost to serve for RTA parcels. In response, peers are moving faster on private-label assortments and cost-down automation that reduces chipboard waste and shortens cycle times without sacrificing quality. Manufacturers with design-for-disassembly features, QR-coded catalogs, and standardized parts are also differentiating on circular compliance and customer satisfaction. The net effect is a steady climb in baseline expectations for service levels and product experience within the Europe ready to assemble furniture market.

Strategic moves underline the value of proximity and control in the supply base. A Scandinavian distributor acquired a Polish upholstery manufacturer to deepen integration and speed, joining earlier investments across the Baltic region that anchor reliable capacity for European orders. On the retail side, the largest banner is streamlining its organization to place stores at the center of an omnichannel structure that promises faster decision-making and lower costs, while retraining impacted teams. At the same time, product leaders are releasing 2026 collections that bake in corner access, rotating units, and wider doors to speed assembly and reduce error, reinforcing the link between product architecture and service cost. Plastics initiatives from leading producers show the scaling of recycled content, zero-waste-to-landfill progress, and innovation in composite materials, which together support circular narratives across garden and storage lines. These moves tighten the alignment between product design, logistics execution, and environmental performance in the Europe ready to assemble furniture market.

White-space opportunities favor DPP-ready and tool-free ranges that deliver faster first-time-right outcomes and reduce post-purchase support costs. Hospitality and multifamily customers prefer modular room sets with take-back guarantees and documented parts availability, which pairs well with RTA designs optimized for rapid install and disassembly. Pre-owned marketplaces and buyback programs continue to scale as retailers target full circularity by 2030 with major investments in recycling infrastructure and in-platform resale. European cabinet makers are leaning into these trends with 2026 novelties that improve access, reduce the need for tools, and cut misalignment risk, which in turn supports circular redeployment. Value capture will depend on aligning material choices with compliance and circular targets, strengthening reverse logistics, and deepening online configuration and visualization to lock in conversion. These tactics together sustain strategic advantages in the Europe ready to assemble furniture market.

Europe Ready-to-Assemble (RTA) Furniture Industry Leaders

IKEA

Tvilum A/S

Fabryki Mebli FORTE S.A.

Rauch Möbelwerke GmbH

Parisot Industrie (P3G Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: IKEA (Ingka Group) announced plans to open twenty new smaller-format stores across Europe (France, Germany, Italy, Spain, Portugal) and North America within six months, ranging from 2,000 to 4,000 square metres. These compact locations offer over 2,000 home-furnishing products with flexible pick-up or delivery, complementing traditional large-format stores as part of a EUR 5 billion three-year investment to enhance accessibility in suburban markets.

- February 2026: Nobilia unveiled its 2026 Kitchen Collection, featuring the FurnSpin dynamic rotating cabinet (award-winning swivel base unit eliminating traditional doors), diagonal units for tight spaces, new 762 mm wide cabinets for enhanced storage flexibility, and a Butterfly pull-out mechanism for dining tables. All access doors now include 110° hinges for wider cabinet access.

- December 2025: Ingka Group streamlined its organizational structure to strengthen focus on IKEA retail, placing stores at the core of its omnichannel business. The restructuring aims for faster decision-making and lower costs, potentially resulting in 800 redundant roles within Group Functions, with commitments to re-skilling and up-skilling affected personnel.

Europe Ready-to-Assemble (RTA) Furniture Market Report Scope

| Home Furniture | Chairs |

| Tables (side, coffee, dressing, etc.) | |

| Beds | |

| Wardrobes | |

| Sofas | |

| Dining Tables / Dining Sets | |

| Kitchen Cabinets | |

| Other Home Furniture | |

| Office Furniture | Chairs |

| Tables | |

| Storage Cabinets | |

| Desks | |

| Sofas & Other Soft Seating | |

| Other Office Furniture | |

| Hospitality Furniture | |

| Educational Furniture | |

| Healthcare Furniture | |

| Other Applications (public places, retail malls, government offices, etc.) |

| Wood |

| Metal |

| Plastic |

| Glass |

| Other Materials |

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly from the Manufacturers |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product Type | Home Furniture | Chairs |

| Tables (side, coffee, dressing, etc.) | ||

| Beds | ||

| Wardrobes | ||

| Sofas | ||

| Dining Tables / Dining Sets | ||

| Kitchen Cabinets | ||

| Other Home Furniture | ||

| Office Furniture | Chairs | |

| Tables | ||

| Storage Cabinets | ||

| Desks | ||

| Sofas & Other Soft Seating | ||

| Other Office Furniture | ||

| Hospitality Furniture | ||

| Educational Furniture | ||

| Healthcare Furniture | ||

| Other Applications (public places, retail malls, government offices, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Plastic | ||

| Glass | ||

| Other Materials | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly from the Manufacturers | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the Europe ready to assemble furniture market size outlook to 2031?

The Europe-ready-to-assemble furniture market size is expected to reach USD 5.8 billion by 2031, expanding from USD 4.50 billion in 2026 at a 5.17% CAGR.

Which product categories are driving growth through 2031 in Europe?

Office furniture is projected to advance at a 6.55% CAGR through 2031 as hybrid work normalizes and home ergonomics improve, while home furniture maintains the largest base.

How are retailers improving affordability and access in the Europe ready to assemble furniture market?

Large retailers invested in price reductions during 2024–2025 and plan compact stores across major European markets in 2026 to enhance convenience and lower total cost to serve.

What role does circularity play in Europe’s RTA purchasing decisions?

Tool-free assembly, modular parts, buyback, and pre-owned programs are reducing returns and enabling refurbishment and redeployment, which align with consumer expectations and policy direction.

Which materials are gaining momentum in European RTA products?

Recycled plastics and composites are rising in storage and garden SKUs due to durability, compliance simplicity, and cost control as producers scale recycled content and zero-landfill operations.

What capabilities help suppliers win B2B contracts in Europe?

Predictable right-first-time delivery, standardized modules, long-term parts availability, and service bundles with take-back and refurbishment clauses are now baseline in hospitality and multifamily.

Page last updated on: