South America Ready Mix Concrete Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

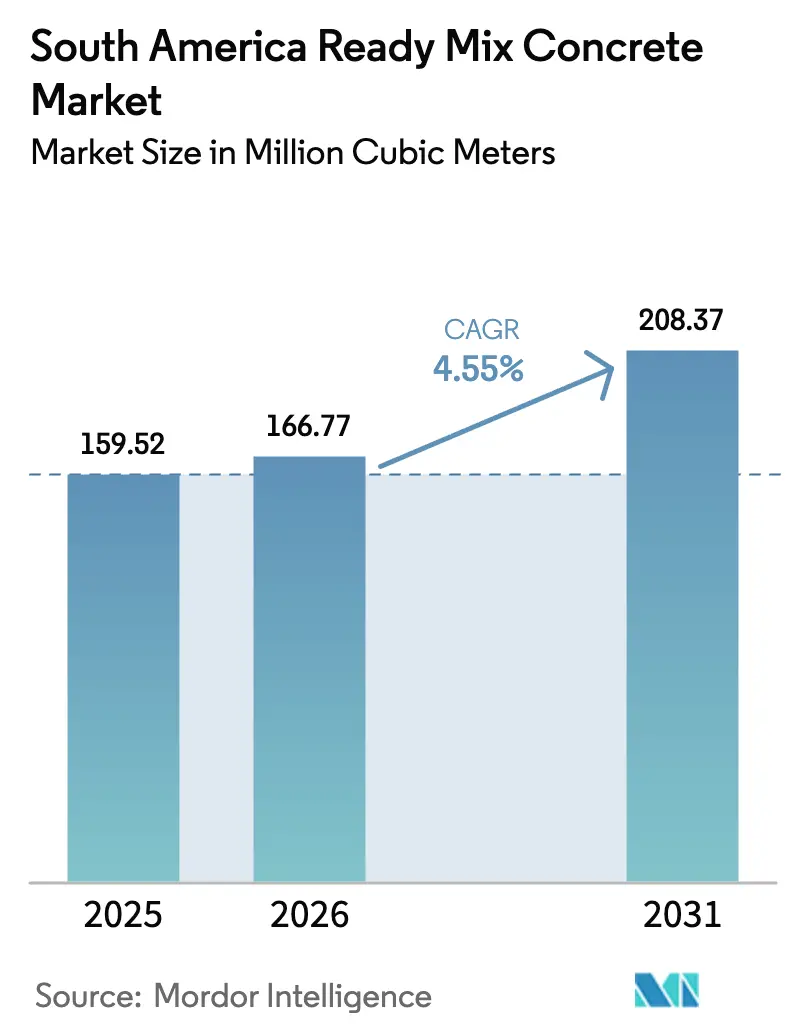

| Base Year Market Size (2025) | 159.52 Million cubic meters |

| Market Volume (2026) | 166.77 Million cubic meters |

| Market Volume (2031) | 208.37 Million cubic meters |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Ready Mix Concrete Market Analysis by Mordor Intelligence

South America Ready Mix Concrete Market size in 2026 is estimated at 166.77 million cubic meters, growing from 2025 value of 159.52 million cubic meters with 2031 projections showing 208.37 million cubic meters, growing at 4.55% CAGR over 2026-2031. Sustained government spending on transport corridors, water security programs, and urban renewal is intensifying demand, while private developers accelerate logistics hubs and modular construction projects that rely on factory-grade concrete quality. Brazil’s New Growth Acceleration Programme (PAC) and Chile’s record rail investments are anchoring near-term volume commitments, and industrial near-shoring is adding fresh order visibility for heavy-duty flooring, foundations, and utilities. Multinational producers are scaling digital batching and water-recycling technologies to defend margins against energy-linked cement price swings, and private equity is backing precast start-ups to shorten schedules and cut labor risk. Collectively, these trends point to a multi-year growth runway for the South America ready mix concrete market as the region narrows the infrastructure gap with other emerging economies.

Key Report Takeaways

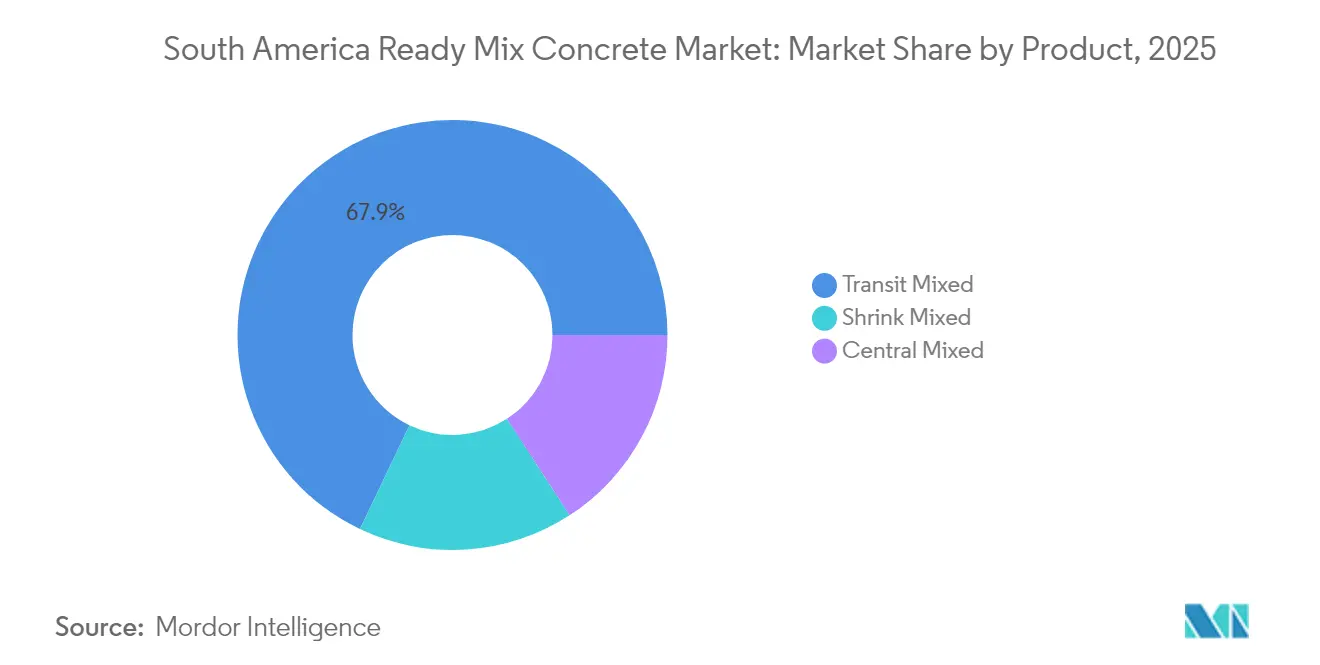

- By product, transit mixed concrete held 67.92% of the South America ready mix concrete market share in 2025. Shrink-mixed concrete is projected to expand at a 4.89% CAGR through 2031.

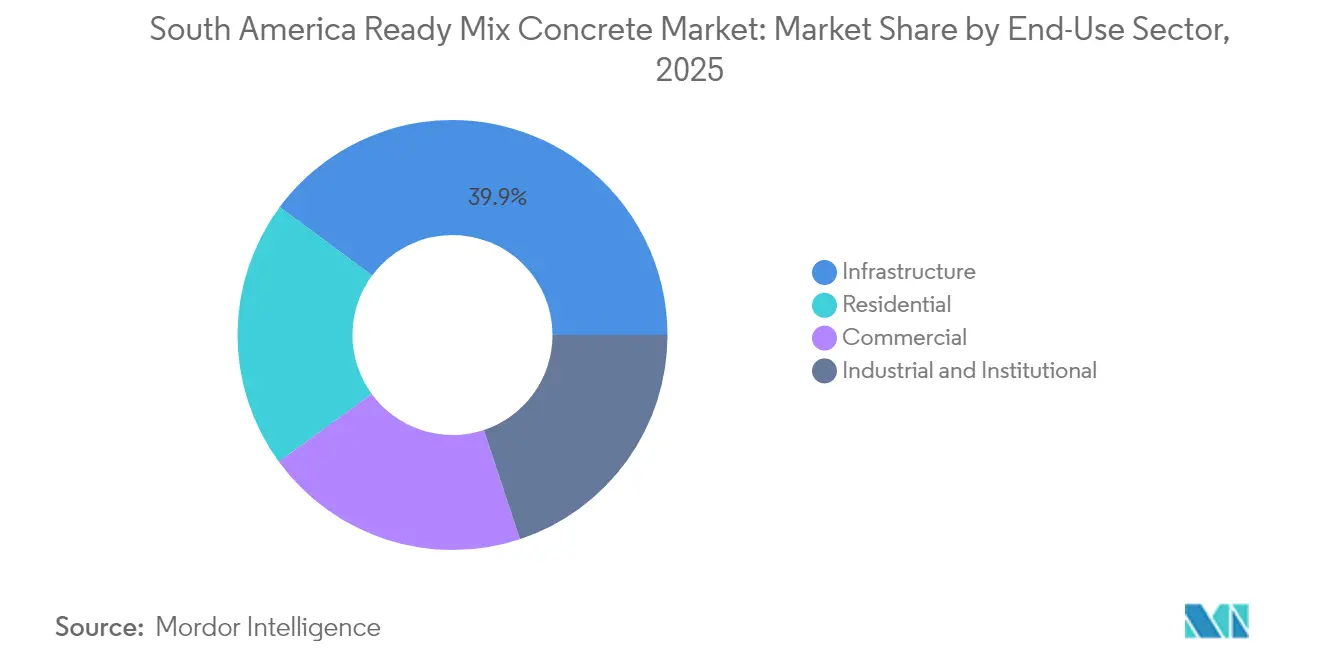

- By end-use sector, infrastructure applications commanded a 39.86% share of the South America ready mix concrete market size in 2025. Infrastructure applications are also advancing at a 5.56% CAGR through 2031.

- Brazil accounted for 47.85% share of the South America ready mix concrete market in 2025 and is expected to record a 4.84% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Ready Mix Concrete Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-sector infrastructure stimulus packages | +1.2% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Housing-deficit led residential demand rebound | +0.9% | Brazil, Colombia, Peru | Long term (≥ 4 years) |

| Commercial real-estate revival around e-commerce logistics | +0.7% | Brazil (São Paulo), Chile (Santiago) | Short term (≤ 2 years) |

| Industrial park investments tied to near-shoring | +0.6% | Paraguay, Brazil, Argentina | Medium term (2-4 years) |

| Private-equity funding of modular precast facilities | +0.4% | Brazil, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Public-Sector Infrastructure Stimulus Packages Drive Market Expansion

Latin American governments are positioning large-scale infrastructure as the central engine of post-pandemic recovery. Brazil’s PAC encompasses more than 2,000 projects spanning highways, ports, metros, and renewable energy assets, requiring an annual expenditure of nearly 3.7% of GDP through 2030[1]OECD, “Scaling-up Infrastructure Investment to Strengthen Sustainable Development in Brazil,” oecd.org . Chile is investing USD 5 billion in its rail renaissance, including the Santiago–Valparaíso line, which alone requires 1.2 million m³ of concrete. The Inter-American Development Bank has earmarked transport as 40% of its historic commitments, ensuring long-term funding support. Strict procurement rules introduced since 2019 require detailed engineering studies to be conducted before the tender launch, reducing bid cancellations and smoothing concrete demand. For suppliers, the pipeline offers revenue predictability and encourages investment in truck fleets, central plants, and digital dispatch platforms that keep the South America ready-mix concrete market on a stable growth path.

Housing-Deficit Residential Demand Emerges from Structural Shortfalls

Roughly 45% of South American households still face qualitative or quantitative housing deficits, resulting in a backlog of more than 35 million units. Peru needs 1.6 million additional homes, while Colombia’s dip in 2023 sales is widely viewed as a cyclical correction, setting the stage for a mortgage-rate-driven rebound. Brazil’s BRL 27.6 billion water security program includes the expansion of basic service grids, which unlocks residential land banks. Governments are widening subsidized credit lines and adjusting loan-to-value caps, enabling lower-income borrowers to enter the market and lifting baseline concrete consumption. Developers are also pivoting to mid-rise modular systems that cut cycle times by 30%, further supporting the uptake of shrink-mixed concrete within the South America ready-mix concrete market.

E-Commerce Logistics Drives Commercial Real Estate Revival

Warehouse completions advanced in 2025, led by additions in São Paulo and Santiago. Fulfillment centers demand high-performance floor slabs with tight flatness tolerances and load-bearing capacity for automated racking—attributes best delivered through digitally monitored ready mix. APM Terminals’ USD 500 million Suape expansion and companion USD 700 million inland depot plan underscore the linkage between port efficiency and warehouse build-outs. Vacancy rates in Tier-1 nodes slipped below 7%, signaling further speculative construction that will keep the South America ready mix concrete market closely tied to the logistics boom. Specialty mixes, including fiber-reinforced and temperature-controlled formulations, are capturing premium margins as operators prioritize durability and energy efficiency.

Near-Shoring Industrial Investments Reshape Manufacturing Geography

Companies seeking shorter supply chains are gravitating toward MERCOSUR’s 280 million-consumer market. The 14.6 km² Paraguay China Industrial Park hosts 17 firms producing auto parts and appliances, generating demand for paved yards, machine foundations, and service corridors. The 2,290 km Bioceanic Corridor will shave up to 17 days off Asia-Pacific transit, catalyzing ancillary manufacturing clusters along its route. Mexico’s earlier near-shoring success offers a blueprint: manufacturing FDI lifted domestic concrete volumes by 12% between 2021 and 2024, a trajectory regional planners aim to replicate. The construction of switchyards, dormitories, and power substations ensures that the South America ready-mix concrete market remains integral to foreign-direct-investment-led growth.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cement prices linked to energy costs | -0.8% | Argentina, Global | Short term (≤ 2 years) |

| Political delays in PPP infrastructure pipeline | -0.6% | Colombia, Argentina | Medium term (2-4 years) |

| Water-stress restrictions on concrete batching | -0.4% | Chile, Peru, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Cement Prices Constrain Market Growth

Argentina’s cement price spike during 2024—fueled by currency devaluation and utilities inflation—compressed contractors’ margins and forced temporary project suspensions. Energy constitutes up to 40% of cement costs, so diesel and gas tariffs ripple quickly through concrete invoices. The IMF notes that each 10% uptick in copper prices raises regional headline inflation by 0.2 percentage points, indirectly pressuring equipment and formwork expenses[2]IMF, “World Economic Outlook October 2024—Commodity Special Feature,” imf.org. Producers attempt to hedge fuel exposure via alternative fuels, but supply security remains uneven. Fixed-price contracts signed before cost shocks face acute profitability risk, leading some small batchers to exit or defer capacity additions within the South America ready mix concrete market.

Political Delays Disrupt PPP Infrastructure Pipeline

Colombia lists 16 road concessions behind schedule, representing USD 513.5 million of stalled works. Argentina’s austerity program froze roughly 3,500 schemes, jeopardizing 200,000 construction jobs and draining concrete demand cushions. Legacy corruption scandals, notably Odebrecht’s Ruta del Sol, have extended some project timelines by five years. While interim spending offers partial relief, volatility remains. The World Bank’s review of Peruvian PPPs warns that advance payment structures can induce surges that outstrip local supply capacity, then crash volumes once funds are exhausted. The resulting stop-start dynamic complicates capacity planning and inflates working-capital needs for participants in the South America ready-mix concrete market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Transit Mixed Concrete Leads Through Versatility

Transit-mixed output accounted for 67.92% of the total South America ready-mix concrete market volume in 2025, reflecting the format’s adaptability to congested urban routes and varying pour conditions. Plants load raw materials into drum trucks, allowing for in-transit agitation that preserves workability for up to 90 minutes, an advantage in cities like São Paulo, where the average delivery speed hovers near 18 km/h. Holcim’s SMARTCast algorithm optimizes admixture dosing on the fly, trimming slump rejections by 12%. Shrink mixed concrete, though smaller in base, is forecast to increase at a 4.89% CAGR through 2031—above the overall South America ready mix concrete market—because modular factories favor partial mix hydration to secure dimensional accuracy in precast molds. Central mixed plants continue to supply high-rise clusters in Buenos Aires and Lima, where precise quality assurance takes precedence over hauling flexibility.

Transit mixed dominance is also rooted in legacy fleet footprints, as the region operates more than 7,800 agitator trucks, most of which are based in Brazil. Firms retrofit telematics to monitor drum revolutions and temperature, enhancing compliance with new ACI 318-25 sustainability appendices. Shrink mixed adoption accelerates where jobsite crane capacities are limited, as partially hydrated loads cut gross vehicle weight. Central mixed remains a staple for mega-projects like Chile’s Santiago–Valparaíso rail where batch uniformity, rather than dispatch reach, is paramount. Combined, the product spectrum secures demand resilience within the South America ready mix concrete industry despite cyclical swings in individual project starts.

By End-Use Sector: Infrastructure Sector Drives Regional Development

Infrastructure accounted for 39.86% of the South America ready-mix concrete market in 2025 and is projected to grow at a 5.56% CAGR, the fastest among tracked sectors. Highway resurfacing, double-track rail corridors, and port dredging each require high-volume, continuous pours that favor dedicated batch plants. Government frameworks mandate life-cycle cost analysis, which elevates performance mixes by incorporating fiber reinforcement and supplementary cementitious materials. Residential construction, pressured by the 35 million-unit deficit, is staging a gradual rebound as policy rate cuts filter through mortgage spreads; national housing funds in Brazil and Colombia have already unlocked nearly 190,000 starter-home approvals for 2025. E-commerce logistics is powering commercial activity, with every 10,000 m² of modern warehouse space consuming roughly 4,500 m³ of floor-grade concrete.

Institutional buildings—including hospitals and universities—are benefiting from multilateral financing conditions that stipulate the use of LEED-compatible materials, prompting suppliers to certify their environmental product declarations. Industrial demand is closely tied to duty-free zones and near-shoring clusters; for example, Paraguay’s automotive hub requires vibration-resistant floor plates with compressive strengths exceeding 6,000 psi. Municipal water-treatment upgrades under Brazil’s BRL 27.6 billion program incorporate sulfate-resistant concrete to extend asset life in aggressive environments. Altogether, the end-use mosaic balances cyclical sensitivities and sustains a broad base for the South America ready mix concrete market.

Geography Analysis

Brazil captured 47.85% of the South America ready-mix concrete market in 2025 and is advancing at a 4.84% CAGR through 2031, driven by PAC’s multi-modal mandate. São Paulo’s ring-road overhaul and Rio’s flood-mitigation tunnels alone require more than 9 million m³ of structural and shotcrete formulations. Federal green-bond proceeds totaling USD 18.1 billion from 2012 to 2023 are earmarked for low-carbon materials, giving early movers an edge. Argentina follows with a rise in cement dispatches during the first eight months of 2025, but political austerity clouds infrastructure visibility. Chile’s USD 5 billion rail pipeline anchors steady volumes, while Colombia’s road delays temper short-term pours yet set up catch-up potential once funding issues are resolved.

Regional cross-border projects such as the Bioceanic Corridor distribute benefits to Paraguay and northern Argentina, stimulating plant upgrades along the alignment. Bolivia and Uruguay, although smaller, participate through feeder roads and cold-chain logistics nodes that support soy and beef exports. Currency volatility remains a watch point; producers hedge imported admixtures in USD to protect margins. Water-usage directives are gaining traction, with CEMEX Colombia’s 90% non-potable benchmark now referenced in Brazilian state tenders. Overall, geography-specific drivers and constraints combine to create a nuanced but growing opportunity set, anchoring future gains in the South America ready mix concrete market.

Competitive Landscape

The market is moderately fragmented. White-space innovation is emerging in carbon-negative concrete, as highlighted by Holcim and ELEMENTAL’s biochar additive, which stores biogenic carbon within the matrix. Small disruptors are pushing digital marketplaces that match surplus truck capacity with spot orders, thereby trimming empty-return kilometers. Yet price volatility tests resilience: smaller players without integrated clinker access saw margin erosion during Argentina’s 2024 cost surge. Cross-industry alliances—such as steelmakers investing in precast plants—broaden capital pools and technical expertise, intensifying competition while expanding overall capacity. Strategic stakes continue to shuffle. The competitive chessboard, therefore, balances consolidation momentum with technology-led niche entrants, shaping an ecosystem in which the South America ready-mix concrete market retains healthy rivalry and innovation.

South America Ready Mix Concrete Industry Leaders

Votorantim Cimentos

Argos Group

CEMEX, S.A.B. de C.V.

Holcim Ltd

InterCement Participações S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HOLCIM, in collaboration with ELEMENTAL, introduced a novel biochar-based technology that enables concrete to function as a carbon sink. This innovation integrates biochar, significantly reducing CO₂ emissions without compromising performance.

- August 2024: HOLCIM entered the Peruvian market through the acquisition of ready-mix concrete producer Mixercon and industrial minerals producer Comacsa for USD 100 million. This strategic move enhances Holcim’s regional supply capabilities and opens new opportunities for synergies and export market development.

South America Ready Mix Concrete Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Central Mixed, Shrink Mixed, Transit Mixed are covered as segments by Product. Argentina, Brazil are covered as segments by Country.| Central Mixed |

| Shrink Mixed |

| Transit Mixed |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| Argentina |

| Brazil |

| Rest of South America |

| By Product | Central Mixed |

| Shrink Mixed | |

| Transit Mixed | |

| By End-Use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential | |

| By Country | Argentina |

| Brazil | |

| Rest of South America |

Market Definition

- END-USE SECTOR - Ready-mix concrete consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of transit-mixed, shrink-mixed, and central-mixed ready-mix concrete are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms