Europe Protective Footwear Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

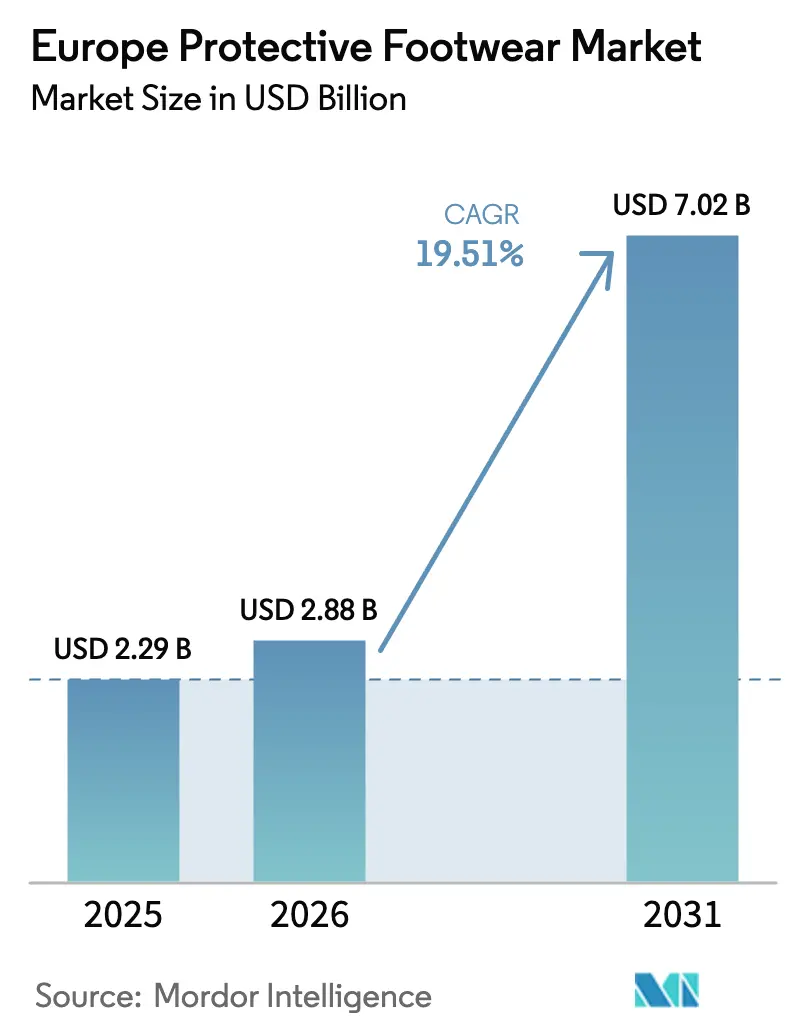

| Base Year Market Size (2025) | USD 2.29 Billion |

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 7.02 Billion |

| Growth Rate (2026 - 2031) | 19.51% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Protective Footwear Market Analysis by Mordor Intelligence

The Europe protective footwear market size is projected to expand from USD 2.29 billion in 2025 and USD 2.88 billion in 2026 to USD 7.02 billion by 2031, registering a CAGR of 19.51% between 2026 to 2031. The current European protective footwear market size reflects the accelerated adoption of ISO 20345:2021-compliant designs, rising construction activity tied to renewable energy buildouts, and tighter enforcement of Regulation (EU) 2016/425. Stricter audits, together with persistent accident rates involving lower-extremity injuries, continue to shift employer preferences toward composite-toe solutions that lower weight and eliminate electromagnetic interference. At the same time, thermoplastic polyurethane blends featuring lower embodied carbon and full recyclability are capturing share from leather. Digital product passports required under the Ecodesign for Sustainable Products Regulation are channeling an ever-larger share of transactions through manufacturer-operated e-commerce portals that offer traceability data and real-time inventory. Together, these forces keep the Europe protective footwear market on a steep growth trajectory even as raw-material volatility injects short-term cost pressure.

Key Report Takeaways

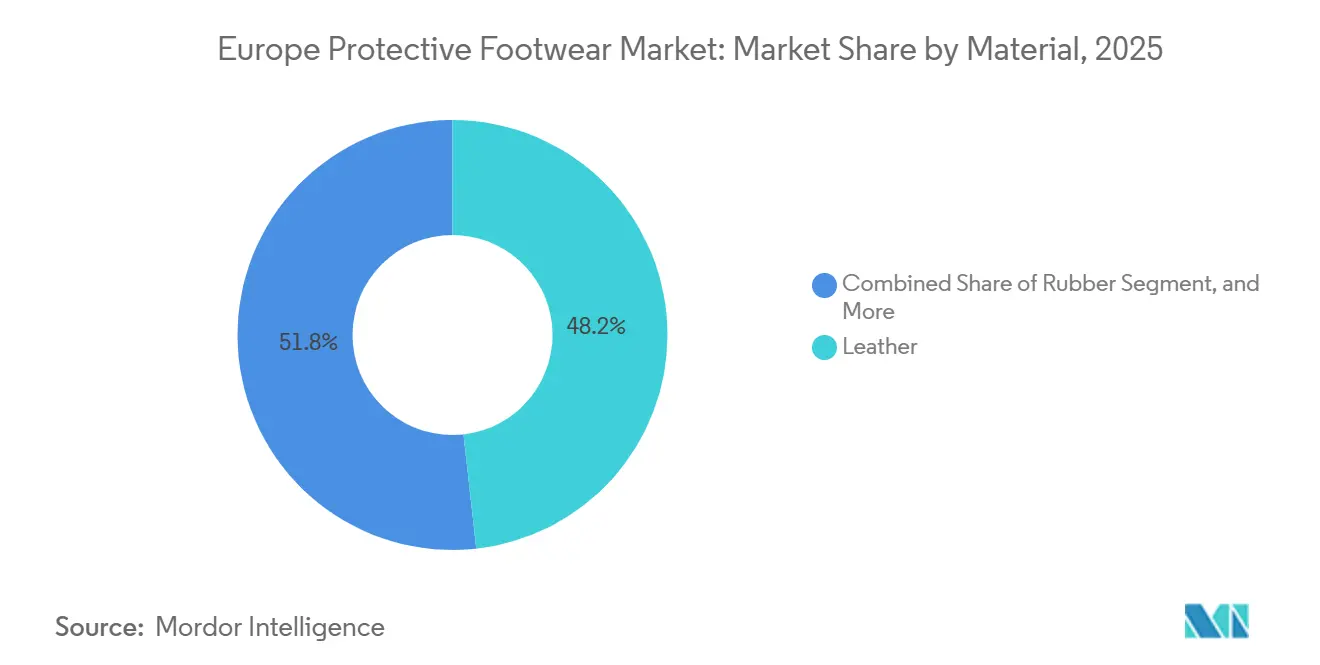

- By material, leather led with 48.24% of the Europe protective footwear market share in 2025, while polyurethane and thermoplastic polyurethane blends are expanding at a 20.33% CAGR through 2031.

- By end-user, construction held 28.67% of the Europe protective footwear market share in 2025; however, utilities and energy are forecast to rise at a 21.13% CAGR to 2031.

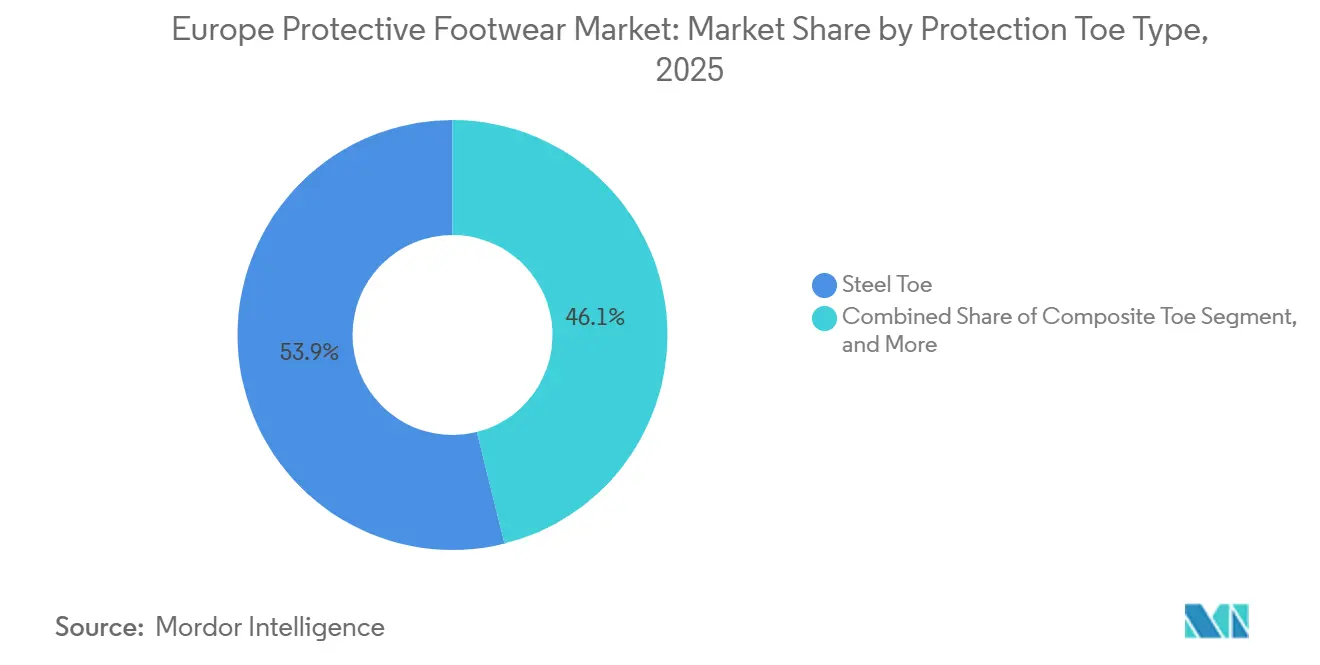

- By protection type, steel-toe designs retained a 53.89% share in 2025, whereas composite-toe variants are projected to advance at a 20.38% CAGR through 2031.

- By channel, direct and industrial distributors captured 39.17% of 2025 sales; however, e-commerce is expected to grow at a 20.29% CAGR through 2031.

- By country, Germany generated 22.58% of regional revenue in 2025, yet Spain is on track to achieve the fastest 20.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Protective Footwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Regulations for Labour Protection | +3.2% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Increasing Number of Industrial Accidents | +2.8% | Construction-heavy markets: Germany, UK, France, Spain | Short term (≤ 2 years) |

| Stricter EU PPE Regulation (EU) 2016/425 Updates | +4.1% | EU-wide, phased enforcement in Eastern Europe | Long term (≥ 4 years) |

| Expansion of E-Commerce Channels for B2B PPE Procurement | +3.5% | Germany, UK, France, Spain, Benelux | Medium term (2-4 years) |

| Adoption of Smart Boots with Embedded IoT Sensors | +2.9% | Germany, Netherlands, Nordics, early pilots in Spain | Long term (≥ 4 years) |

| Circular-Economy Demand for Recyclable Safety Footwear | +2.4% | Germany, France, Netherlands, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Regulations for Labour Protection

National labor inspectorates intensified onsite audits during 2024-2025, issuing more citations for inadequate foot protection, particularly in the construction and logistics sectors. The Machinery Regulation (EU) 2023/1230, applicable from January 2027, extends PPE requirements to collaborative-robot zones, encouraging employers to buy slip-resistant, metatarsal-guard footwear.[1]European Commission, “Ecodesign for Sustainable Products Regulation,” ec.europa.eu As inspectors increasingly flag steel-toe models for electromagnetic interference in electronics and pharmaceutical cleanrooms, sales of composite-toe models accelerate. Stricter oversight increases the baseline replacement cycle and expands orders from subcontractors that formerly relied on low-spec footwear.

Increasing Number of Industrial Accidents

In 2023, EU-OSHA recorded 2.82 million non-fatal workplace accidents, with 30% involving the lower limbs.[2]European Agency for Safety and Health at Work, “Workplace Accident Statistics 2023,” osha.europa.eu Construction alone contributed 22.9% of fatal cases, reinforcing employer demand for puncture-resistant midsoles rated to 1,100 N and heat-resistant outsoles capable of withstanding 300 °C contact for metal fabrication. The incident profile is also driving the development of dual-density nitrile-rubber designs that maintain slip resistance on oily floors, as well as lightweight composite-plate boots that reduce fatigue during extended shifts.

Stricter EU PPE Regulation (EU) 2016/425 Updates

Delegated acts under Regulation (EU) 2016/425 mandate third-party conformity assessment for every Category II safety footwear style sold after January 2025. Notified bodies are reporting 18-month testing queues, so firms with ISO/IEC 17025-accredited labs fast-track new product launches. Incumbents such as Uvex and COFRA gain an advantage, while small brands face capital costs exceeding EUR 500,000 (USD 565,000) for compression rigs and slip-testing tribometers. The tightening closes self-certification loopholes and locks sub-standard imports out of the Europe protective footwear market.

Expansion of E-Commerce Channels for B2B PPE Procurement

B2B marketplaces across North America and Europe hit USD 4.8 trillion in 2023, growing seven times faster than traditional channels. Half of procurement managers now prefer manufacturer portals that provide real-time inventory, automated reorder links, and digital product passports that comply with the July 2024 Ecodesign Regulation. Although commission rates can reach 20%, suppliers accept the cost to gain direct usage data and improve forecasting. Faster lead times and transparent traceability are accelerating the European protective footwear market toward digital procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Prices Compared to Normal Footwear | -1.8% | Price-sensitive SMEs in Eastern Europe, Spain, Italy | Short term (≤ 2 years) |

| Volatility in Raw Material (Leather and Rubber) Costs | -2.3% | EU-wide, acute in leather-dependent segments | Short term (≤ 2 years) |

| Low Compliance Levels among SMEs in Eastern Europe | -1.5% | Poland, Romania, Bulgaria, Hungary | Medium term (2-4 years) |

| Complex Recycling of Multi-Material Safety Boots | -1.1% | Germany, France, Netherlands, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prices Compared to Normal Footwear

Certified safety boots that meet EN ISO 20345:2011 S3 specifications retail for EUR 80 to EUR 150 (USD 90 to USD 170) per pair, representing a three-to-five times premium over mainstream athletic shoes. Small and medium-sized enterprises in Eastern Europe operate on monthly construction and manufacturing wages ranging from EUR 800 to EUR 1,200, forcing many to stretch replacement cycles beyond the recommended 12- to 18-month window. Deferred purchases increase exposure to sole delamination, compromised puncture resistance, and reduced slip-grip performance, particularly among subcontractor crews that frequently shift between short-term projects. Because national subsidies for personal protective equipment are absent in Poland, Romania, and Bulgaria, buyers prioritize the initial price over the lifecycle cost, hampering the uptake of lighter composite-toe or recyclable thermoplastic designs. Distributors report that orders for entry-level steel-toe boots spike whenever natural-rubber or leather prices jump, demonstrating the tight link between commodity volatility and price-sensitive procurement behavior. This affordability gap continues to constrain market penetration among the region’s millions of tradespeople, thereby slowing overall progress toward EU safety compliance targets.

Volatility in Raw Material Costs

Natural-rubber futures climbed to 185.10 US cents per kilogram in January 2026 after monsoon floods damaged 600,000 hectares of Thai plantations. Meanwhile, the U.S. leather producer price index, though off its 2024 peak, still sits 22% above pre-pandemic averages.[3]U.S. Bureau of Labor Statistics, “Producer Price Index – Leather and Allied Products,” bls.gov Manufacturers locked into fixed-price contracts for rubber and leather, signed in 2024, now face margin compression that limits their promotional spending. Those passing increases to buyers risk order cancellations among cost-sensitive distributors in Southern and Eastern Europe, temporarily slowing the growth of the European protective footwear market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Thermoplastic Blends Challenge Leather Dominance

Leather captured 48.24% of the revenue in 2025, driven by its high abrasion resistance and breathability. Yet polyurethane and thermoplastic polyurethane blends are forecast to expand at a 20.33% CAGR, propelled by BASF’s Elastollan 1400 series that cuts carbon footprint by 30% and meets SRC slip-resistance without added weight. The European protective footwear market size for polyurethane and thermoplastic polyurethane is projected to reach approximately USD 2.5 billion by 2031, as brands transition away from leather, which is burdened by traceability requirements under the EU Deforestation Regulation. Rubber remains essential for oil-and-gas outsoles due to its chemical resistance, while plastic uppers dominate in cleanrooms, where non-shedding surfaces are required.

ISO 20345:2021 introduced new ceramic-tile and steel-deck slip tests, prompting the reformulation of polyurethane outsoles that shed 150–200 g per pair relative to rubber, thereby reducing worker fatigue over 10-hour shifts. BASF’s Elastopan systems now deliver electrostatic-discharge safety without compromising flexibility, allowing manufacturers to penetrate the pharmaceutical and electronics assembly markets. The Europe protective footwear market benefits from these lighter, recyclable compounds, especially in countries with extended producer responsibility mandates.

By End-User Industry: Utilities Surge on Renewable Buildout

Construction generated 28.67% of 2025 demand; however, utilities and energy are forecast to rise at a 21.13% CAGR through 2031, driven by record wind and solar installations. The Europe protective footwear market size for utilities alone is estimated to double between 2026 and 2031 as technicians require arc-rated boots for turbine work at heights. Manufacturing, mining, and oil and gas companies remain stable buyers of metatarsal-guard footwear, while chemical and pharmaceutical plants specify electrostatic-discharge boots that comply with ATEX zones.

Spain leads growth, fueled by 8.2 GW of renewable capacity additions in 2025 and supportive safety equipment grants, raising composite toe adoption among installation crews. Germany’s Energiewende stimulates demand for cold-insulated footwear rated to −17 °C for offshore platforms. Logistics operators in Poland and the Netherlands deploy smart-insole solutions to cut lost-time incidents, further diversifying end-user needs across the Europe protective footwear market.

By Protection Toe Type: Composite Gains on Weight and Conductivity

Steel-toe boots accounted for 53.89% of revenue in 2025 due to their proven impact resistance and lower cost. Composite-toe models, however, are growing at a 20.38% CAGR as Kevlar, carbon fiber, and fiberglass caps eliminate cold conduction and electromagnetic interference. The Europe protective footwear market size for composite toes is forecast to exceed USD 2 billion by 2031. Alloy-toe options cater to a niche among aerospace workers who frequently climb ladders. Metatarsal guards gain ground in foundries where molten-metal splash hazards surpass standard toe protection.

Composite uptake accelerates as BASF’s Elastollan bonds directly to carbon-fiber caps without delamination under cyclic loading. Revised ISO cold-insulation tests expose steel caps to failure at sub-zero conditions, giving composites a clear advantage. Employers also point to a 15–20% reduction in musculoskeletal claims after switching to lighter footwear, reinforcing momentum across the Europe protective footwear market.

By Distribution Channel: Digital Platforms Reshape Procurement

Direct and industrial distributors held 39.17% of 2025 revenue, leveraging onsite fittings and bulk discounts. E-commerce, however, is expanding at a 20.29% CAGR as digital product passports become mandatory. The Europe protective footwear market size transacted online is expected to exceed USD 2 billion by 2031, as buyers prioritize real-time inventory and automated reordering. Retail stores, anchored in DIY chains, face traffic declines, while rental models are gaining traction for project-based staff in Germany and the Netherlands.

Manufacturers accept e-commerce commission rates to harvest usage data and improve demand planning. Distributors that integrate augmented-reality sizing tools can replicate store-level fitting accuracy, reducing return rates below 8%. Rental operators are investing in reverse logistics to sanitize boots between projects, tackling the EUR 90–EUR 170 upfront price barrier for temporary workers and further diversifying the Europe protective footwear market.

Geography Analysis

Germany led with 22.58% of 2025 revenue, supported by 10.4 million industrial workers, but tempered by a 1.8% contraction in the construction sector in early 2025. The United Kingdom, France, and Italy together accounted for almost 40%, each influenced by domestic incentives such as France’s tax credit for occupational health and Italy’s renovation pipeline. Russia relies largely on domestically produced steel-toe designs as sanctions restrict composite imports, leaving growth flat relative to Western peers.

As wind and solar projects proliferate, Spain is set to achieve a rapid 20.93% CAGR, driven by the rising demand for arc-rated boots among technicians maintaining turbines. The increasing focus on renewable energy infrastructure in the country further supports this growth trajectory. In France, the swift adoption of recyclable polyurethane designs is fueled by the country's extended producer responsibility regulations, which encourage sustainable manufacturing practices. Meanwhile, Germany's North Sea wind platforms are driving a demand for cold-insulated composites, essential for ensuring worker safety and equipment durability in harsh offshore conditions.

While Eastern Europe shows slower compliance with protective footwear standards, its swift e-commerce growth offers suppliers a cost-effective market entry, enabling them to tap into a growing consumer base. In the Nordic region, buyers are prioritizing sustainability certifications and pioneering smart-insole initiatives, which enhance worker comfort and safety. These trends are contributing to elevated average selling prices in the European protective footwear market, reflecting the increasing value placed on innovation and eco-friendly solutions.

Competitive Landscape

The Europe protective footwear market is moderately fragmented, with the top five players holding roughly 35–40% share. Honeywell’s USD 1.325 billion divestiture of its PPE unit to Protective Industrial Products in November 2024 removes a conglomerate competitor and opens space for specialists. Uvex, COFRA, Elten, Emma Safety Footwear, and Rock Fall utilize ISO/IEC 17025-accredited laboratories to expedite certification cycles.

Wolverine World Wide and VF Corporation bolster their safety ranges by cross-subsidizing them with lifestyle brands, ensuring they maintain prominent shelf space throughout Europe. Dunlop Protective Footwear leads the charge in the rubber-boot niche. Meanwhile, Haix and Sixton Peak are fortifying their positions in the premium firefighter and construction segments, especially in light of Dr. Martens' recent shift towards consumer channels.

Competition now centers on embedded IoT sensors. Arion’s 8-point pressure-mapping insoles and SolePower’s energy-harvesting boots enable employers to monitor gait and reduce compensation claims. Capital barriers remain high: establishing an accredited in-house lab costs more than EUR 500,000, reinforcing incumbent advantages. White-space opportunities persist in rental programs, circular-economy designs, and cold-insulated composites for offshore wind, all of which support continued expansion of the Europe protective footwear market.

Europe Protective Footwear Industry Leaders

Honeywell International Inc.

Bata Corporation

Wolverine World Wide Inc.

VF Corporation

Dunlop Protective Footwear

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Severe monsoon flooding in Thailand damaged about 600,000 hectares of rubber plantations, tightening global supply and pushing natural-rubber futures to 185.10 US cents per kilogram, the highest level in nine months for European footwear manufacturers.

- September 2025: Dr. Martens plc reported first-half fiscal 2026 revenue of GBP 322.0 million (USD 408.4 million), a 0.8% decline year-on-year in constant currency, and opened new stores in France, Germany, Spain, the Netherlands, Italy, Sweden, and Austria to support its consumer-first shift.

- March 2025: Dr. Martens plc announced fiscal 2025 group revenue of GBP 787.6 million (USD 999.0 million), down 10.2% year-on-year, while achieving 97% leather traceability and expanding its U.K. repair service to lengthen product lifecycles.

- January 2025: The EU Textiles Strategy’s mandatory separate collection requirement took effect across all member states, launching extended producer responsibility schemes in France, Germany, and the Netherlands that obligate footwear brands to fund collection, sorting, and recycling infrastructure.

Europe Protective Footwear Market Report Scope

The Europe Protective Footwear Market Report is Segmented by Material (Leather, Rubber, Plastic, PU and TPU Blends), End-User Industry (Construction, Manufacturing, Mining, Oil and Gas, Chemical, Pharmaceutical, Transportation and Logistics, Utilities and Energy), Protection Toe Type (Steel Toe, Composite Toe, Alloy Toe, Metatarsal Guard), Distribution Channel (Direct/Industrial Distributors, Retail Stores, E-Commerce, Rental and Leasing Services), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Leather |

| Rubber |

| Plastic |

| PU and TPU Blends |

| Construction |

| Manufacturing |

| Mining |

| Oil and Gas |

| Chemical |

| Pharmaceutical |

| Transportation and Logistics |

| Utilities and Energy |

| Steel Toe |

| Composite Toe |

| Alloy Toe |

| Metatarsal Guard |

| Direct/Industrial Distributors |

| Retail Stores |

| E-Commerce |

| Rental and Leasing Services |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Material | Leather |

| Rubber | |

| Plastic | |

| PU and TPU Blends | |

| By End-User Industry | Construction |

| Manufacturing | |

| Mining | |

| Oil and Gas | |

| Chemical | |

| Pharmaceutical | |

| Transportation and Logistics | |

| Utilities and Energy | |

| By Protection Toe Type | Steel Toe |

| Composite Toe | |

| Alloy Toe | |

| Metatarsal Guard | |

| By Distribution Channel | Direct/Industrial Distributors |

| Retail Stores | |

| E-Commerce | |

| Rental and Leasing Services | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe protective footwear market in 2026?

The market was worth USD 2.88 billion in 2026 and is forecast to reach USD 7.02 billion by 2031.

What is driving the fastest growth within protective-footwear materials?

Polyurethane and thermoplastic polyurethane blends are expanding at a 20.33% CAGR because they weigh less, reduce carbon footprint, and comply with new slip-resistance tests.

Which European country is expected to grow the quickest?

Spain is projected to post a 20.93% CAGR through 2031 due to large-scale wind and solar installations that require arc-rated, puncture-resistant boots.

Why are composite-toe boots gaining share?

Composite caps eliminate electromagnetic interference, weigh 20–30% less than steel, and pass new cold-insulation tests, reducing fatigue and meeting cleanroom protocols.

How is e-commerce influencing buying behavior?

Half of procurement managers now prefer manufacturer portals that offer digital product passports, real-time stock, and automated reorder links, lifting online sales at a 20.29% CAGR.

What impact do rising rubber prices have on suppliers?

Higher input costs compress margins unless passed to buyers, encouraging a shift toward synthetic alternatives and reinforcing price sensitivity among small distributors.

Page last updated on: