Market Overview

| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

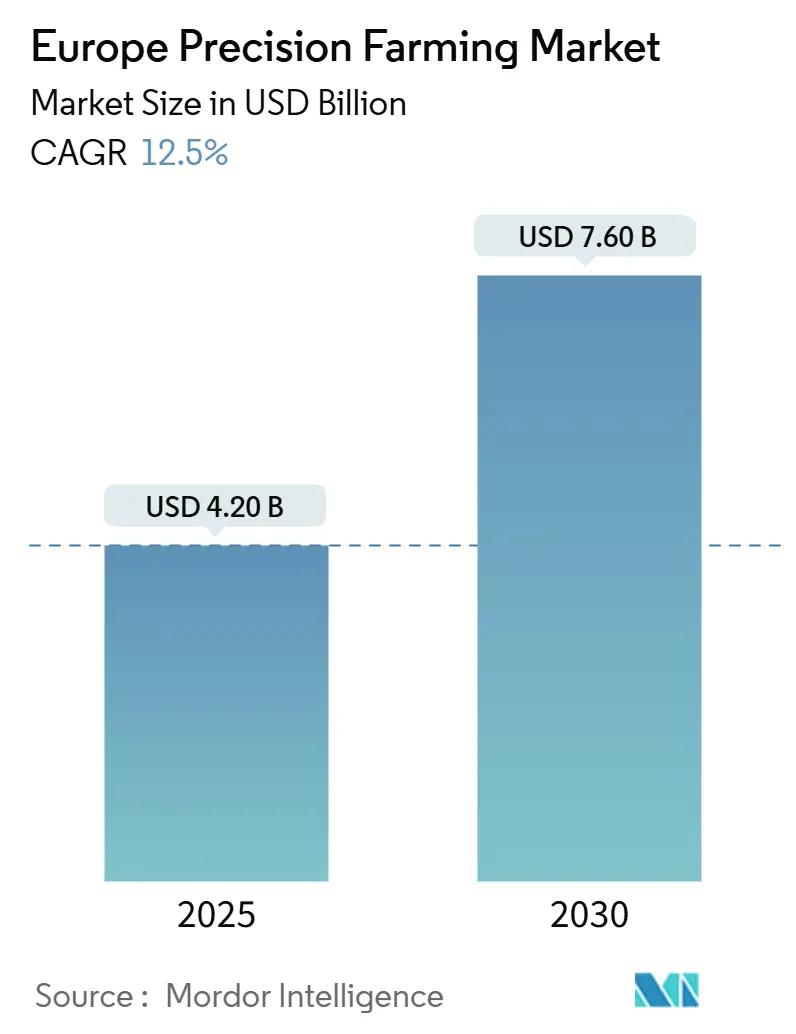

| Market Size (2025) | USD 4.20 Billion |

| Market Size (2030) | USD 7.60 Billion |

| Growth Rate (2025 - 2030) | 12.50% CAGR |

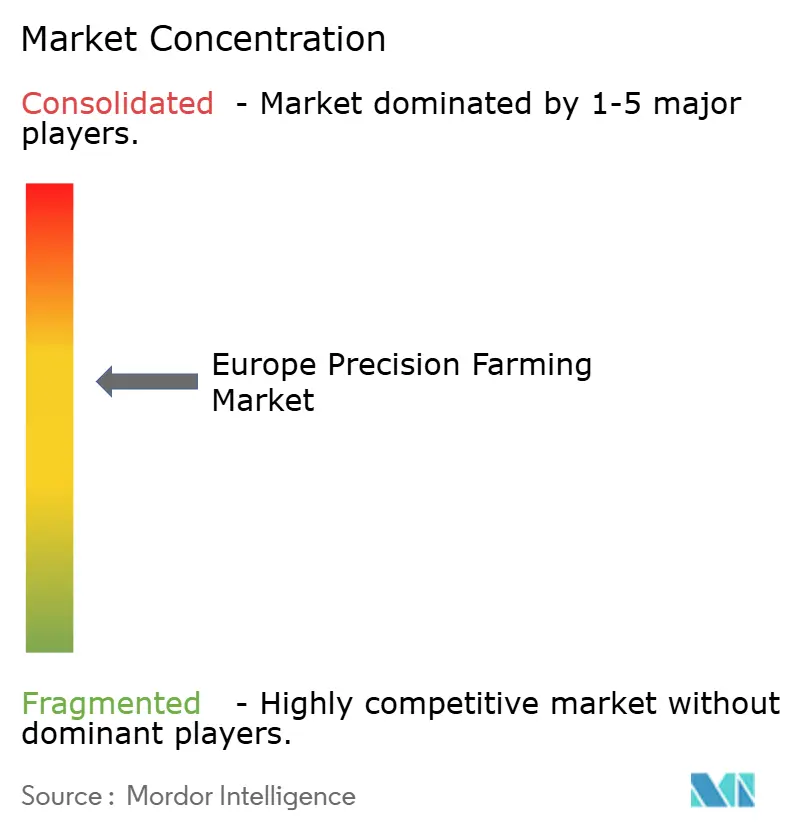

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Precision Farming Market Analysis by Mordor Intelligence

The Europe precision farming market stands at a current value of USD 4.2 billion and is forecast to reach a Europe precision farming market size of USD 7.6 billion by 2030, corresponding to a 12.5% CAGR across the period. This trajectory elevates the Europe precision farming market to the vanguard of the continent’s digital-agriculture transition, propelled by the Common Agricultural Policy’s EUR 387 billion ring-fenced investment, a widening 5G footprint, and tightening environmental mandates. Technology uptake now cuts across holdings of every scale as guidance, telematics, and data-driven decision tools address efficiency, input-reduction, and compliance goals in a single workflow. The Europe precision farming market is further shaped by Galileo satellite accuracy, Copernicus Earth-observation feeds, and space-to-farm APIs that sharpen field-level prescriptions. Nonetheless, broadband black spots, fragmented data-privacy codes, and large ticket prices slow diffusion among resource-constrained smallholders, setting up a dual-speed playing field inside the Europe precision farming market.

Key Report Takeaways

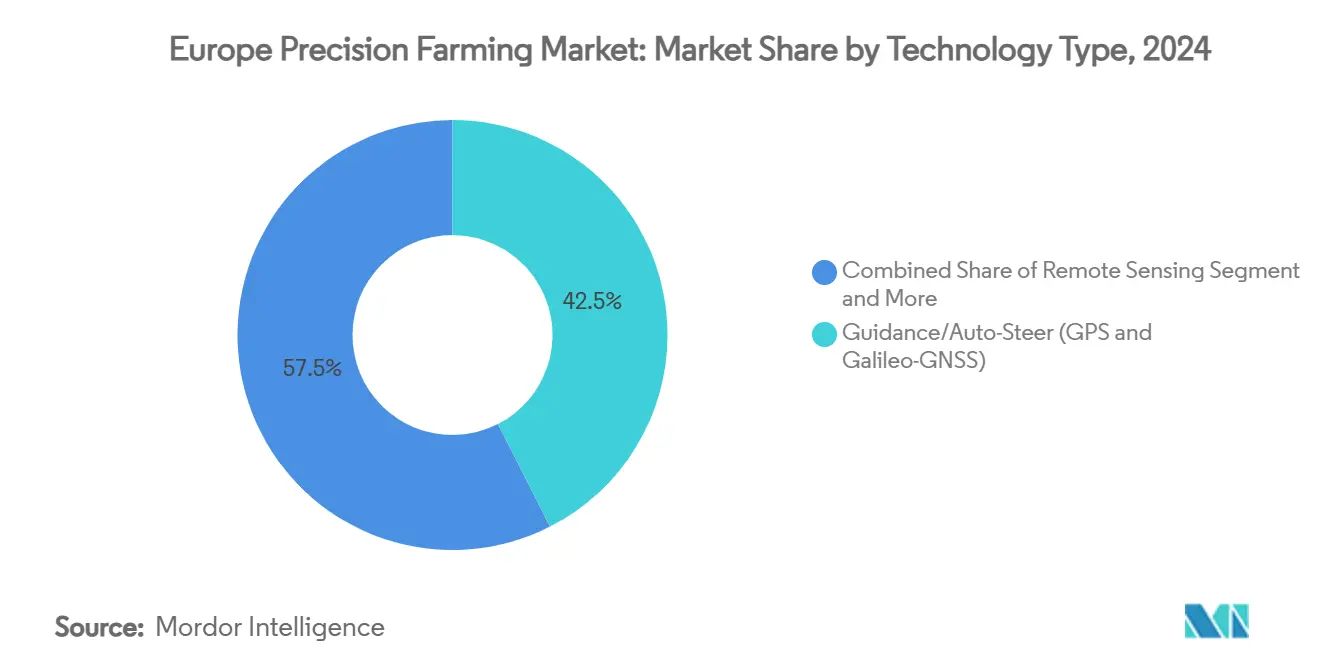

- By technology, guidance and auto-steer solutions led with 42.5% of Europe's precision farming market share in 2024, while VRT is projected to expand at a 13.4% CAGR to 2030.

- By component, hardware captured 55% of the Europe precision farming market size in 2024, and software is forecast to grow at 12.2% CAGR through 2030.

- By farm size, holdings above 500 ha accounted for 64% of Europe's precision farming market share in 2024, and farms under 100 ha are advancing at a 14% CAGR.

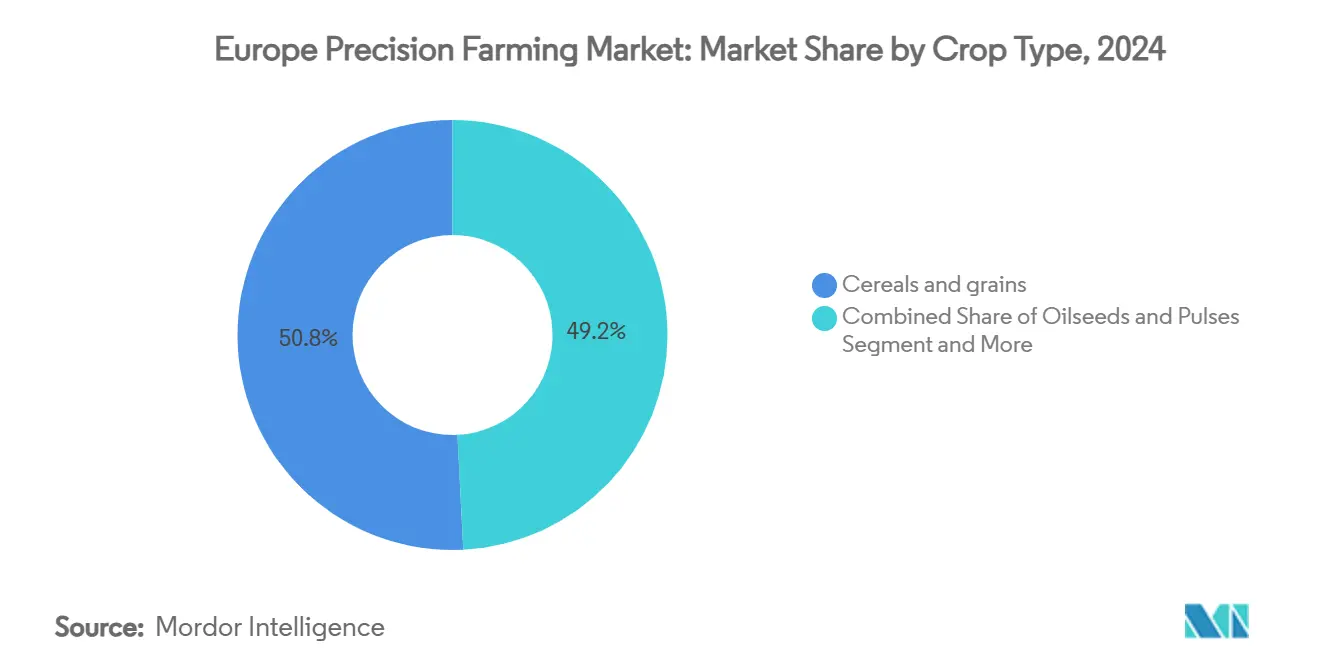

- By crop type, cereals and grains held 50.8% of the Europe precision farming market size in 2024, and precision viticulture is rising at an 11.6% CAGR.

- By application, yield monitors captured 31% of 2024 income, yet crop scouting pest detection climbs fastest at 11.2% CAGR.

- By country, Germany remained the largest national market in 2024, while Italy is set to register the highest 14% CAGR to 2030.

Europe Precision Farming Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies under EU CAP digitalization schemes | +3.2% | EU-wide, strongest in Germany, France, Italy | Medium term (2-4 years) |

| Rapid progress in on-farm AI, IoT and 5G connectivity | +2.8% | Germany, Netherlands, UK; widening East | Short term (≤2 years) |

| EU Green Deal-linked demand for low-input, sustainable food | +2.1% | EU-wide, high in the Netherlands, Denmark, Germany | Long term (≥4 years) |

| Monetization of carbon credits via machine-generated field data | +1.7% | France, Germany, Italy, spreading East | Medium term (2-4 years) |

| Labor scarcity is accelerating autonomous machinery | +1.9% | Western Europe | Short term (≤2 years) |

| Galileo GNSS and Copernicus EO data integration | +1.8% | EU-wide, strongest in Germany, France | Medium term (2-4 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Government subsidies under EU CAP digitalization schemes

The 2023-27 CAP allocates 25% of direct payments to eco-schemes, unleashing EUR 96.75 billion specifically for precision-agriculture tools and advisory services. Germany earmarks EUR 6.2 billion for digital infrastructure, while France injects EUR 4.8 billion into sensor and software grants[1]Source: European Commission, “CAP Strategic Plans 2023-2027,” ec.europa.eu . The result is a compulsory pull mechanism that farms must digitize to unlock payments, even when internal ROI remains debatable. Portugal’s strategy goes further by tying 20% of farmland to organic certification triggers paired with digital compliance dashboards, illustrating how policy can compress adoption cycles. Such public spending cements the Europe precision farming market as a policy-anchored arena rather than a purely profit-driven technology market.

Rapid progress in on-farm AI, IoT and 5G connectivity

Autonomous implements now process edge-camera feeds through AI chips and stream findings across low-latency rural 5G corridors. John Deere reports 77% less herbicide on See and Spray Select deployments, and latency-free data sync enables machine swarms to coordinate in real time[2]Source: European 5G Observatory, “Status of 5G Corridor Projects,” 5gobservatory.eu. With 37 cross-border 5G corridors funded in 2024, the Europe precision farming market graduates from post-process analytics to live decision systems. Yet coverage gaps in parts of the UK and the Baltic keep a wedge between early adopters and fringe regions, reinforcing a digital divide inside the Europe precision farming market.

Monetization of carbon credits using machine-generated field data

IoT soil probes and satellite biomass readings create immutable audit trails, allowing farms to verify tonnes of carbon sequestered. Early pilots in Cyprus and Italy average EUR 4,140 per farm in credit revenue, while Bayer-backed initiatives seek a 15% GHG cut by 2025. The shift converts sustainability into hard income, making precision farming a revenue line instead of a cost center and reshaping ROI benchmarks across the Europe precision farming market.

Labor scarcity accelerating demand for autonomous machinery

Growers in Germany and the Netherlands report seasonal-worker deficits of 25-30% in 2024, placing wage bills on a steep incline. Autonomous sprayers and robotic weeders offer a substitution path, trimming labor hours per hectare by up to 40%. Equipment suppliers see this pain point as a prime catalyst, redirecting R and D budgets from horsepower boosts toward unmanned platforms[3]Source: AGCO Corporation, “AGCO Q1 2025 Financial Results,” agcocorp.com. The net effect is a demand spike for autonomy modules in the Europe precision farming market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front hardware and retrofit costs | –2.3% | EU-wide; acute in Eastern Europe, small farms | Short term (≤2 years) |

| Fragmented data-privacy and interoperability rules | –1.8% | EU-wide; varies by member state | Medium term (2-4 years) |

| Patchy last-mile broadband and edge-cloud capacity | –1.4% | Rural districts, notably Eastern Europe, UK | Long term (≥4 years) |

| Digital-skills gap among ageing farmers | –1.1% | EU-wide; high in traditional regions | Long term (≥4 years) |

Source: Mordor Intelligence

High up-front hardware and retrofit costs

A fully-featured VRT sprayer package easily tops EUR 50,000, eclipsing the average annual net farm income in Hungary and Slovakia. The European Investment Fund warns that high interest rates compound the burden, especially for micro-enterprises[4]Source: European Investment Fund, “Small Business Finance Outlook 2024,” eif.org. Low-cost controller boards built on open-source silicon now achieve 97.17% accuracy, yet market penetration remains limited by distribution reach and service capacity. Until lending spreads shrink or pooling models scale, expensive kits will cap the Europe precision farming market’s full potential.

Fragmented EU data-privacy and interoperability regulations

Member-state variances require vendors to customize cloud locations, consent flows, and telemetry standards, inflating cost and elongating deployment timelines. While ISOBUS eased tractor-implement connectivity, cross-platform data exchange still lacks an EU-wide farm-data protocol. This regulatory mosaic slows software ecosystem formation and clips scale advantages inside the Europe precision farming market.

Segment Analysis

By Technology: GPS Dominance Faces VRT Disruption

In 2024, guidance and auto-steer platforms generated 42.5% of Europe's precision farming market revenue, benefiting from multi-satellite compatibility and affordable retrofit kits. However, variable-rate technology is projected to log a 13.4% CAGR to 2030, the strongest lift across the Europe precision farming market, as eco-scheme audits appraise input application maps. New VRT sprayers deliver herbicide savings of up to 97.5% through real-time target recognition, drastically shifting cost curves. Remote sensing—satellite and proximal—holds second-place turnover, underpinning disease mapping, yield forecasts, and insurance underwriting. Drone swarms transition from field photographers to active applicators, while robotic weeders edge from pilot to first commercial fleets. Integration with Galileo and Copernicus' unique assets supplies a sovereign edge, positioning Europe’s developers against US-GPS-centric competitors and reinforcing global differentiation for the European precision farming market.

The Europe precision farming industry sees emerging digital-twin engines roll environmental layers, crop phenology, and machinery logs into predictive simulations. These models run on field-edge compute nodes for latency-free optimization, reinforcing the strategic pivot from mere guidance to decision-support ecosystems. As a consequence, suppliers that historically sold metal now sell algorithms, heralding a margin reallocation that will redefine competitive hierarchies.

Note: Segment shares of all individual segments available upon report purchase

By Component: Software Acceleration Challenges Hardware Dominance

Hardware retained 55% of 2024 turnover yet faces gradual share erosion as analytics subscriptions scale. AI advice engines and compliance report builders commanding recurring fees. The Europe precision farming market size for software is on track to exceed USD 3.2 billion by 2030, mirroring SaaS trajectories in adjacent industrial verticals. Services—from sensor calibration to agronomic coaching—sit at the smallest base but show pronounced elasticity: once connectivity stabilizes, managed-service layers offer low-capital pathways for small farms. Edge-cloud hybrids emerge to reconcile bandwidth bottlenecks, sending compressed insights rather than raw data, ensuring GDPR conformity without latency trade-offs.

The hardware remains crucial yet commoditized as suppliers replicate sensor arrays and GNSS chips. Value migrates towards integrated operating systems able to orchestrate multi-brand fleets, verify carbon metrics, and synchronise with government portals for subsidy validation. OEMs thus partner with cloud hyperscalers and space-data firms in a bid to secure longitudinal data flows critical to customer lock-in.

By Application: Yield Monitoring Leadership Threatened by Pest Detection Innovation

Yield monitors captured 31% of 2024 income thanks to instant payback visibility and machine-integrated sensors. Yet AI-driven pest detection climbs fastest at 11.2% CAGR, stacking root-zone imaging, spectral vegetation indices, and canopy thermography to catch infestations seven days sooner than legacy scouting. As a result, insecticide volumes fall by 60% without yield drag, further aligning with Green Deal targets. Variable-rate application, although originally nutrient-focused, now extends to seed and bio-stimulant dosing, rounding out the application portfolio. Soil-health dashboards leverage electro-conductivity probes and in-situ fluorescence for predictive fertilizer advice, while business-management modules ensure audit-ready documentation. Such digital paperwork responds to the CAP’s heightened traceability conditions and accelerates payment cycles, driving another wedge of demand.

The Europe precision farming market continually widens its application bandwidth, with methane-emission tracking for livestock integration and water-stress decision engines for drought-exposed orchards appearing on the near horizon. As each module plugs into a common platform, incremental ROI compounds, smoothing upgrade justification and elevating cross-sell velocity for vendors.

By Crop Type: Precision Viticulture Emerges as Premium Growth Driver

Cereals and grains constitute 50.8% of revenue, aligned with Europe’s broadacre heritage. Yet vineyards and other specialty crops clock an 11.6% CAGR, the fastest within the Europe precision farming market, thanks to high produce-value density and branding pressure for sustainability labels. Site-specific irrigation loops save water stress for Mediterranean vineyards; canopy sensors inform micro-parcel harvest scheduling to boost phenolic profiles. Meanwhile, orchard operators deploy robotic pickers guided by lidar maps, blending labor substitution with fruit-quality consistency. Oilseeds, pulses, and open-field vegetables maintain steady yet modest growth, while greenhouse tomatoes and peppers integrate sensor-laden climate loops, illustrating precision beyond open fields.

Premium segments set performance benchmarks later adopted in high-volume commodities, positioning viticulture and horticulture as R and D sandboxes whose best practices cascade into barley or maize operations, ultimately amplifying the Europe precision farming market’s knowledge spillover effects.

Note: Segment shares of all individual segments available upon report purchase

By Farm Size: Small Farm Digitization Accelerates Despite Large Farm Dominance

Estates above 500 ha represented 64% of deployments in 2024, leveraging scale economies and internal IT staff. Yet small farms under 100 ha post a 14% adoption CAGR, becoming the dynamo for diffusion in the Europe precision farming market. Subscription models eliminate capex shocks, while machinery co-operatives let members rent high-spec sprayers by the hour. Simplified user experiences, local-language onboarding, and preset agronomy templates lower cognitive load, broadening the addressable base. Medium-sized farms stand as pivotal swing buyers—large enough for individual capex, agile enough for fast pivots—forming the testing ground for bundle innovations.

Public-sector nudges such as startup incubators, young farmer bonuses, and voucher schemes sustain momentum. These policies ensure that the Europe precision farming market will not plateau in a large-farm enclave but diffuse into fragmented plots across Mediterranean terraces and Alpine valleys alike.

Geography Analysis

Germany heads the Europe precision farming market, underpinned by EUR 6.2 billion of CAP-backed digital allocations and a near-ubiquitous broadband footprint. With OEM clusters from Lower Saxony to Baden-Württemberg, machine builders collaborate closely with agronomic institutes, compressing prototype-to-field cycles to under 12 months. The national mix spans broadacre grains, sugar beets, and dairy forages, providing ample testbeds for multi-crop algorithm training.

Italy is the momentum hotspot, slated for a 14% CAGR through 2030 as EUR 450 million of Recovery Fund grants offset capital barriers and severe labor shortages force mechanization. Precision viticulture roll-outs in Veneto and Piedmont demonstrate 33.4% greenhouse gas cuts at scale.

France follows with strong public-private R and D consortia linking input majors and digital agritech startups. The Netherlands concentrates on greenhouse automation, while Spain leverages satellite-based water-stress indices for high-value horticulture. Poland and Romania, recipients of significant structural funds, are fast-tracking farm-machinery upgrades yet still wrestle with last-mile fiber gaps that curb real-time analytics. Collectively, these patterns confirm that subsidy design, crop portfolio, and connectivity maturity, and not farm size alone, determine precision adoption rates across Europe.

Competitive Landscape

The Europe precision farming market exhibits moderate concentration. The top five suppliers capture 57.8% of aggregate revenue, yet no single brand exceeds a one-fifth hold, preserving room for challengers. John Deere posted USD 520 million in European precision revenue during 2024, equal to 17.0% of the market. AGCO’s PTx Trimble follows at USD 410 million (13.4%), leveraging combined guidance-software stacks, while CNH Industrial rounds out the top three with USD 340 million (11.1%).

Strategic alliances trump outright acquisitions. AGCO’s USD 2 billion JV with Trimble seeks USD 2 billion in revenue by 2028, offering a mixed-fleet cockpit that unites telemetry across brands. John Deere fast-tracks autonomy roll-outs, partnering with Wiedenmann to widen sales channels in the UK and Ireland. Syngenta renews a satellite imagery collaboration with Planet to fuse crop-growth maps into scouting apps. Start-ups such as Ecorobotix bring laser-guided spot sprayers to tackle herbicide resistance, while senseFly, now under Parrot, extends fixed-wing drone analytics tailored to European parcel sizes.

Corporate venture funds from Corteva and BASF funnel minority stakes into early-stage AI agrotech, seeding a pipeline of disruptive IP without diluting incumbent market sway. Space-tech providers, Airbus Intelligence, ESA spinoffs, forge data partnerships, embedding Earth-observation products into farm dashboards. Meanwhile, white space persists in regulatory compliance SaaS, multi-brand equipment orchestration, and low-cost carbon-audit toolkits, areas, where incumbents lack speed and start-ups, lack scale, setting the scene for future consolidation waves.

Europe Precision Farming Industry Leaders

-

Deere & Company

-

AGCO (PTx Trimble JV)

-

CNH Industrial (Raven)

-

Topcon Positioning Systems

-

CLAAS KGaA mbH

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: AGCO reported Q1 2025 net sales of USD 2.1 billion, down 30% YoY, but reiterated long-term growth through PTx Trimble, targeting USD 2 billion in revenue by 2028.

- May 2025: Syngenta and Planet renewed a satellite-imagery agreement to enhance European crop monitoring solutions.

- March 2025: Agmatix and BASF launched AI tools for early soybean cyst nematode detection across EU trials.

- January 2025: John Deere showcased autonomous machinery at CES 2025 and signed a marketing pact with Wiedenmann for broader European distribution.

Europe Precision Farming Market Report Scope

Precision farming is the adoption of a highly precise set of practices that uses technology to cater to the needs of individual plots and crops. It is a farming management concept based on observing, measuring, and responding to inter and intra-field variability in crops.

The market is segmented by Technology(Guidance systems, Remote sensing, Variable Rate Technology, Drones and UAVs, and Other technologies), Components(Hardware, Software, and Services), Application(Yield monitoring, Variable Rate Application, Field Mapping, Soil Monitoring, Crop Scouting, Other Application), and Geography (Germany, United Kingdom, Italy, France, and the Rest of Europe). The market size and estimation will be provided in terms of value (USD) for the above-mentioned segments.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe precision farming market?

The market stands at USD 4.2 billion in 2025 and is projected to reach USD 7.6 billion by 2030.

Which technology segment is expanding fastest?

Variable-rate technology shows the highest growth, advancing at a 13.4% CAGR to 2030.

How do EU policies influence adoption?

CAP eco-schemes mandate precision tools for subsidy eligibility, while Green Deal fertilizer ceilings turn VRT into a compliance requirement.

What are the main barriers to small-farm uptake?

High initial hardware costs, patchy rural broadband, and a persistent digital-skills gap limit rapid adoption among holdings below 100 ha.

Which companies are shaping the competitive landscape?

AGCO, John Deere, Topcon Positioning Systems, CLAAS KGaA mbH, and a wave of AI-driven start-ups are leading through joint ventures, autonomous machinery, and data-centric platforms.

Page last updated on: July 4, 2025