Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

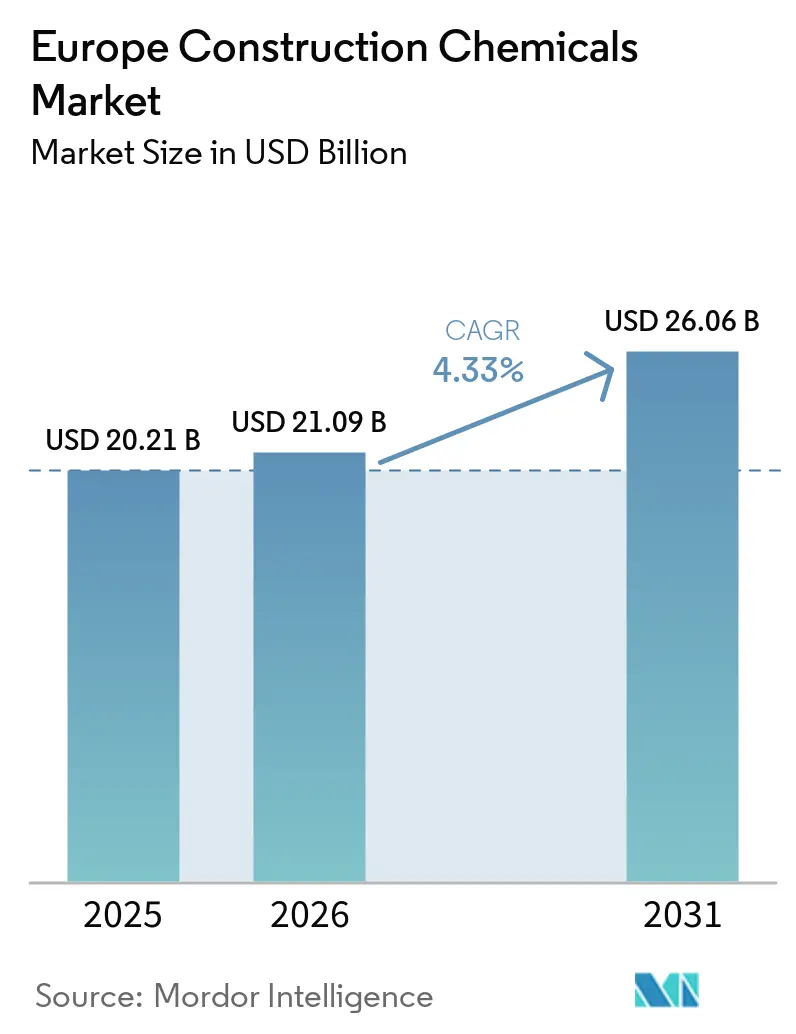

| Base Year Market Size (2025) | USD 20.21 Billion |

| Market Size (2026) | USD 21.09 Billion |

| Market Size (2031) | USD 26.06 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Construction Chemicals Market Analysis by Mordor Intelligence

The Europe Construction Chemicals Market size is expected to increase from USD 20.21 billion in 2025 to USD 21.09 billion in 2026 and reach USD 26.06 billion by 2031, growing at a CAGR of 4.33% over 2026-2031. Robust trans-border infrastructure outlays under the Connecting Europe Facility, zero-emission building rules stemming from the recast Energy Performance of Buildings Directive, and carbon-pricing pressures on cement feed sustained demand for specialty admixtures, waterproofing membranes, and low-VOC (Volatile Organic Compound) sealants. Suppliers with pan-regional logistics networks capture the procurement cycles compressed by European Union (EU) co-financing, while patent momentum in bio-based polyurethanes and graphene-enhanced epoxies signals a shift toward circular-economy compliant chemistries. Nonetheless, phased PFAS (per- and polyfluoroalkyl substances) and VOC prohibitions, carbon-border levies on clinker, and chronic labor shortages in qualified applicators temper near-term volume expansion.

Key Report Takeaways

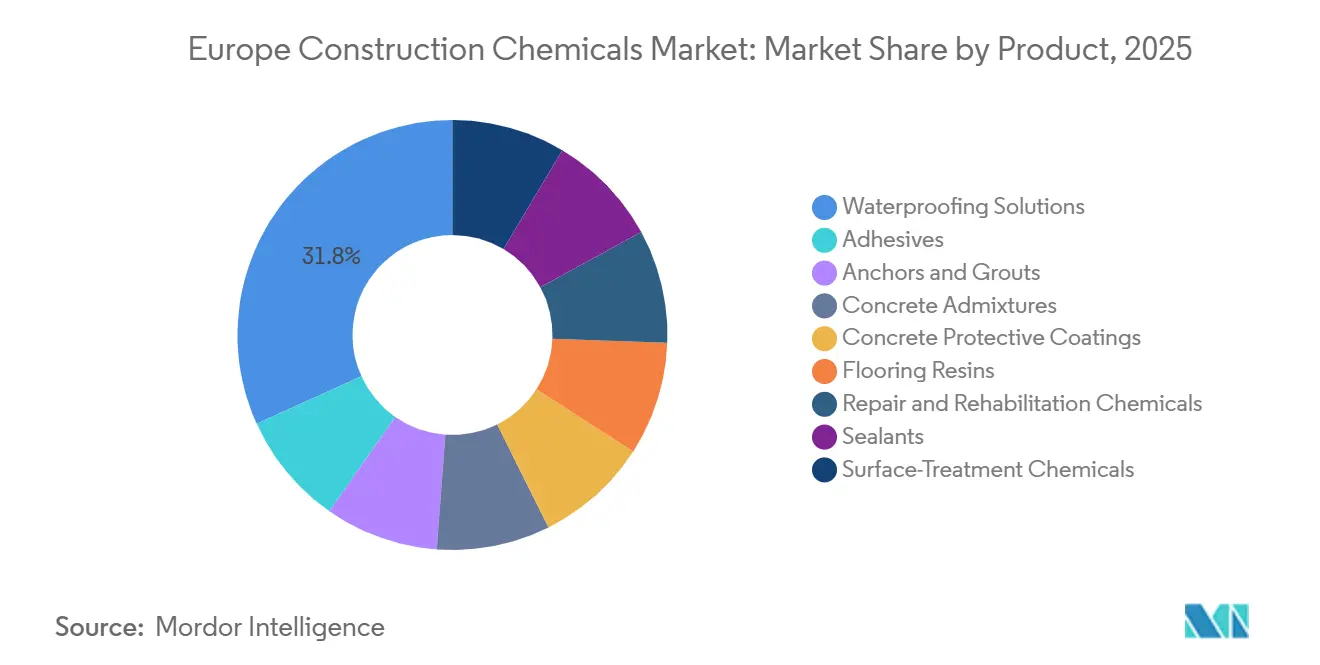

- By product category, waterproofing solutions held 31.78% of the Europe Construction Chemicals market share in 2025. However, the market share of concrete admixtures is expected to increase with the fastest CAGR of 5.12% during the forecast period (2026-2031).

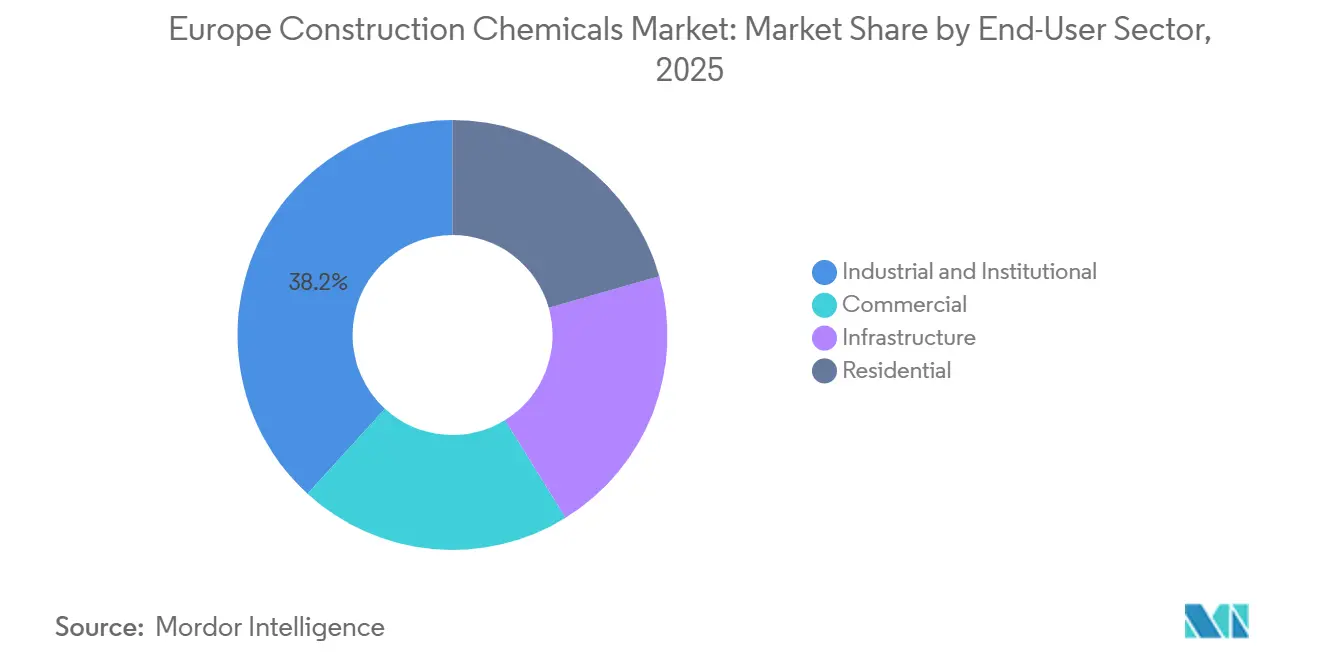

- By end-user sector, industrial and institutional applications accounted for 38.22% of the Europe Construction Chemicals market size in 2025, whereas infrastructure is projected to expand at a 6.68% CAGR during the forecast period (2026-2031).

- By geography, Germany led with a 15.11% share of the Europe Construction Chemicals market in 2025. However, Italy is expected to record the fastest 4.92% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Construction Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Connecting Europe Facility boosts trans-border infrastructure spend | +0.9% | Core EU-27; strongest in Poland, Baltic states, Iberia rail corridors | Medium term (2-4 years) |

| Stricter EPBD 2025 energy-efficiency codes lift high-performance admixture demand | +1.1% | EU-27 with early enforcement in Netherlands, Denmark, Germany | Short term (≤ 2 years) |

| Renovation Wave retrofits push low-VOC sealants and coatings adoption | +0.8% | Western Europe, spill-over to Central Europe | Medium term (2-4 years) |

| Carbon-neutral concrete mandates spur supplementary cementitious materials | +0.7% | Nordic countries, Germany, France; pilot programs in Italy | Long term (≥ 4 years) |

| Growth of green-hydrogen mega-plants drives cryogenic-grade specialty grouts | +0.5% | North Sea coastal zones, Iberia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Connecting Europe Facility Boosts Trans-Border Infrastructure Spend

Peak 2025 allocations under the EUR 33.71 billion program accelerated works such as Rail Baltica and the Lyon-Turin base tunnel, elevating demand for cryogenic-grade epoxy grouts that carry 30-40% price premiums over commodity variants. Poland’s CPK hub already tendered EUR 1.2 billion in concrete-repair contracts specifying ISO 19338-compliant fiber wraps, while Spain’s Mediterranean Corridor consumed 18,000 tons of shrinkage-reducing admixtures in 2025 and is set to double volumes by 2029. CEF (Connecting Europe Facility) co-financing of up to 50% compresses procurement cycles, advantaging suppliers with multi-country depots and mobile technical teams.

Stricter EPBD 2025 Energy-Efficiency Codes Lift High-Performance Admixture Demand

The directive mandates zero-emission status for all new buildings by 2030, and EPC (Energy Performance Certificate) class D retrofits for existing stock by 2033, displacing solvent-borne adhesives with water-borne systems emitting less than 10 g/L VOC. Early adoption in the Netherlands spurred a 34% surge in polyurethane-foam adhesive imports, while Germany’s KfW (Kreditanstalt für Wiederaufbau) disbursed EUR 9.8 billion in retrofit subsidies in 2025, 62% for façade insulation that relies on air-entraining admixtures to offset freeze-thaw cycles. Airtightness thresholds of 0.6 ACH (Air Changes per Hour) in Denmark further popularized acrylic-hybrid sealants capable of -40°C elasticity.

Renovation Wave Retrofits Push Low-VOC Sealants and Coatings Adoption

EUR 72.2 billion in Recovery and Resilience Facility grants underwrite national schemes like France’s MaPrimeRénov, which deployed EUR 2.4 billion in 2025 to replace single-glazed windows using silicone sealants below 5 g/L VOC. Belgian public-building rules capped coating VOC at 30 g/L, banning alkyd lines and lifting water-borne acrylic demand 41% year-on-year. Deep-retrofit targets of 60% energy savings necessitate multi-layer façades where hybrid polymer sealants prevent plasticizer migration across dissimilar substrates.

Carbon-Neutral Concrete Mandates Spur Supplementary Cementitious Materials

From January 2026, concrete must carry Environmental Product Declarations and meet 150 kg CO₂/m³ limits by 2030, tightening from today’s 240 kg CO₂/m³ baseline. Compliance centers on 40-60% SCM (Supplementary Cementitious Materials) replacement mixes activated by polycarboxylate-ether super-plasticizers. Germany posted a 19% uptake in SCM (Supplementary Cementitious Materials) volumes in 2025, while France’s RE2020 code forces whole-life carbon ceilings to be hit only by geopolymer binders paired with viscosity-modifying admixtures. Nordic trials of carbon-capture concrete demand retarding agents to extend set times for full carbonation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and PFAS phase-out rules restrict solvent-borne chemistries | -0.6% | EU-27; strictest in Nordic countries and Germany | Short term (≤ 2 years) |

| Shortage of certified applicators for advanced flooring and repair systems | -0.4% | Germany, Netherlands, Austria; emerging in France | Medium term (2-4 years) |

| Cement CO₂-pricing accelerates shift toward alternative structural materials | -0.3% | EU-27; most acute in Sweden, Finland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and PFAS Phase-Out Rules Restrict Solvent-Borne Chemistries

REACH Annex XVII banned PFAS in construction sealants from January 2025, granting essential-use exemptions to <8% of applicants[1]European Chemicals Agency, “PFAS Restriction under REACH,” echa.europa.eu. The ruling erased fluoropolymer-modified epoxies from wastewater facilities, forcing silane-terminated alternatives with 15-20% lower abrasion resistance. Germany’s TA Luft dropped to 20 mg/m³ VOC on sites, shifting contractors to water-borne sealants needing 48-hour cure cycles, extending project timelines 8-12%. France’s Grenelle II procurement filter excluded 34% of legacy adhesive SKUs (stock keeping units), while Nordic Swan caps of 1 g/L VOC inflated hybrid polymer costs by 25-30%.

Shortage of Certified Applicators for Advanced Flooring and Repair Systems

A 17% deficit in certified polyaspartic and epoxy flooring installers was recorded in Germany in 2025, with 42% of the workforce above 50. Polyaspartics require exact 100:50 mix ratios and 15-25°C ambient windows; deviations void warranties, deterring uptake despite 30% faster completion. The Netherlands’ SBB issued 23% fewer KOMO (Quality Declarations of Maintenance and Environment in Construction) certificates in 2025, while Austria’s mandatory 80-hour epoxy-injection curriculum reached only 41% completion. France’s Qualibat scheme for fiber-reinforced wrapping counts just 1,840 qualified firms against 4,200 annual bridge projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Waterproofing Dominates, Admixtures Accelerate

Waterproofing solutions accounted for 31.78% of the Europe Construction Chemicals market share in 2025, as 48% of the region’s housing stock predates 1970 and confronts rising precipitation[2]European Environment Agency, “Climate Trends and Precipitation Data,” eea.europa.eu. Concrete admixtures, supported by carbon-neutral mandates, are forecast to post a 5.12% CAGR during the forecast period (2026-2031) and command a growing portion of the market size. Adhesives diverge, with water-borne lines up 29% after PFAS bans clipped fluorinated hot-melts, while reactive polyurethanes cut cross-laminated timber press cycles to 90 minutes. Sealants captured 11% of revenue, silicone grades remaining preferred in curtain-wall glazing for -60°C elasticity.

Unit costs of cryogenic-grade epoxy grouts exceed EUR 4,500/t, triple cementitious grades, but volumes rise with hydrogen and CO₂ (Carbon dioxide) pipelines. Concrete protective coatings, especially bridge-deck epoxies exhibiting 0.02% chloride permeability after 28 days, defend aging infrastructure. Polyaspartic flooring resins doubled to 18% share of pharmaceutical cleanrooms as GMP (Good Manufacturing Practices) audits tightened. Fiber-wrapping systems restore 85% flexural capacity in bridges, securing EU-funded retrofit budgets, while silicone mold-release agents cut façade-panel rework 34%.

By End-User Sector: Infrastructure Outpaces Industrial Growth

Industrial and Institutional sites maintained a 38.22% revenue share in 2025, led by data centers and GMP (Good Manufacturing Practices) cleanrooms that demand antimicrobial coatings. Infrastructure is projected to rise at a 6.68% CAGR during the forecast period (2026-2031), supported by the Connecting Europe Facility and a EUR 1.5 trillion rehabilitation backlog that lifts demand for epoxy-injection grouts and fiber wraps. Commercial projects slowed on hybrid-work trends, with office absorption down 22% in major metros, while residential uptake depends on Renovation Wave subsidies offsetting 3.75% ECB (European Central Bank) policy rates.

Bridge aging dynamics create a USD component of the Europe construction chemicals market size, where fiber wraps extend service life 20-25 years at one-third replacement cost. Hydrogen projects import cryogenic-grade grouts at EUR 4,500/t, sustaining niche margins. Industrial cleanrooms specify polyaspartic floors at EUR 85-110/m², double warehouse epoxy, because FDA (Food and Drug Administration) and EMA (European Medicines Agency) validations prioritize 2-hour cure and 80°C thermal-shock resistance.

Geography Analysis

Germany retained 15.11% of regional revenue in 2025, anchored by a EUR 270 billion federal infrastructure plan prioritizing bridge repair and Autobahn expansion that consumes fiber-reinforced mortars and high-modulus epoxies. Italy is the fastest-growing major market at a 4.92% CAGR from 2026, aided by EUR 25.4 billion for energy-efficient retrofits and seismic upgrades under its National Recovery and Resilience Plan. France’s decelerated as fiscal limits deferred the Grand Paris Express and trimmed MaPrimeRénov payouts by 18%.

The United Kingdom has grappled with a contraction in construction employment since 2019 and new UKCA (UK Conformity Assessed) marking hurdles. Spain benefits from 4.2 GW of 2025 solar-thermal parks that specify 85% albedo protective coatings. Russia remains technologically isolated; domestic admixtures trail Western formulations by 5-7 years. Nordic countries boast per-capita spend of EUR 42, double the EU average, owing to stringent energy codes and timber prefabrication glued with sub-1 g/L VOC adhesives.

Competitive Landscape

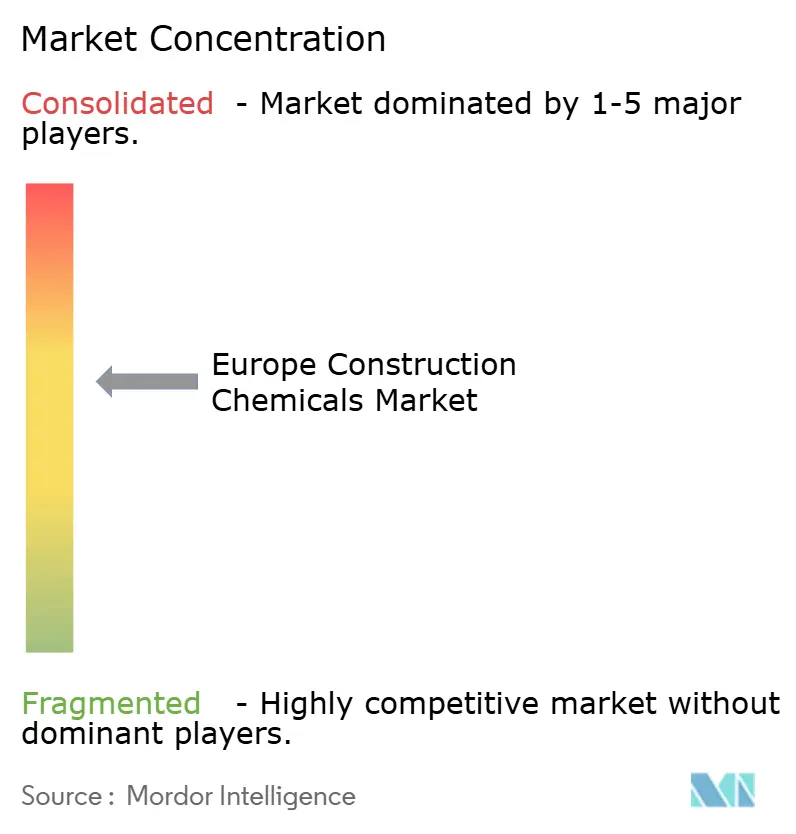

The Europe Construction Chemicals market is moderately consolidated. Commodity super-plasticizer prices fell 6% on Southern European overcapacity, but ISO 14001-certified low-emission lines command 12-18% public-procurement premiums. Saint-Gobain leverages vertically integrated gypsum and insulation assets for bundled façades, whereas Schomburg concentrates on heritage-restoration mortars meeting EN 459 lime standards in a EUR 680 million Italian-French niche.

Europe Construction Chemicals Industry Leaders

Sika AG

Mapei S.p.A.

Saint-Gobain

Arkema

RPM International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Greek coatings manufacturer Vitex completed the acquisition of Microfill, a company specializing in calcium carbonate-based fillers. Microfill, headquartered in Corinth, Greece, was recognized for its high-quality raw materials, including calcium carbonate sourced from its proprietary deposit.

- August 2025: Sika AG launched SikaTile-150 Moisture Guard Fabric Membrane and SikaTile-250 Fracture Guard UCM globally. SikaTile-150 Moisture Guard Fabric Membrane is a dependable solution for waterproofing showers, tub surrounds, walls, and wet areas.

Europe Construction Chemicals Market Report Scope

Construction chemicals, including admixtures, sealants, and coatings, are mixed with materials like concrete and mortar to boost durability, strength, and workability. These chemicals not only enhance performance and expedite construction but also shield structures from environmental wear. Key types encompass waterproofing agents, concrete admixtures, flooring solutions, repair compounds, and adhesives.

The Europe Construction Chemicals market report is segmented by product, end-use sector, and geography. By product, the market is segmented into adhesives, anchors and grouts, concrete admixtures, concrete protective coatings, flooring resins, repair and rehabilitation chemicals, sealants, surface-treatment chemicals, and waterproofing solutions. By end-use sector, the market is segmented into commercial, industrial and institutional, infrastructure, and residential. The report also covers the market size and forecasts for the Europe Construction Chemicals market in 6 countries across Europe. For each segment, market sizing and forecasts have been done based on value (USD).

By Product

| Adhesives | Hot-Melt |

| Reactive | |

| Solvent-borne | |

| Water-borne | |

| Anchors and Grouts | Cementitious Fixing |

| Resin Fixing | |

| Concrete Admixtures | Accelerator |

| Air-Entraining | |

| Super-plasticizer | |

| Retarder | |

| Shrinkage-Reducer | |

| Viscosity-Modifier | |

| Plasticizer | |

| Other Types | |

| Concrete Protective Coatings | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyurethane | |

| Other Resins | |

| Flooring Resins | Acrylic |

| Epoxy | |

| Polyaspartic | |

| Polyurethane | |

| Other Resins | |

| Repair and Rehabilitation Chemicals | Fiber-Wrapping Systems |

| Injection Grouting | |

| Micro-concrete Mortars | |

| Modified Mortars | |

| Rebar Protectors | |

| Sealants | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| Surface-Treatment Chemicals | Curing Compounds |

| Mold-Release Agents | |

| Other Types | |

| Waterproofing Solutions | Chemicals |

| Membranes |

By End-User Sector

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

By Geography

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By Product | Adhesives | Hot-Melt |

| Reactive | ||

| Solvent-borne | ||

| Water-borne | ||

| Anchors and Grouts | Cementitious Fixing | |

| Resin Fixing | ||

| Concrete Admixtures | Accelerator | |

| Air-Entraining | ||

| Super-plasticizer | ||

| Retarder | ||

| Shrinkage-Reducer | ||

| Viscosity-Modifier | ||

| Plasticizer | ||

| Other Types | ||

| Concrete Protective Coatings | Acrylic | |

| Alkyd | ||

| Epoxy | ||

| Polyurethane | ||

| Other Resins | ||

| Flooring Resins | Acrylic | |

| Epoxy | ||

| Polyaspartic | ||

| Polyurethane | ||

| Other Resins | ||

| Repair and Rehabilitation Chemicals | Fiber-Wrapping Systems | |

| Injection Grouting | ||

| Micro-concrete Mortars | ||

| Modified Mortars | ||

| Rebar Protectors | ||

| Sealants | Acrylic | |

| Epoxy | ||

| Polyurethane | ||

| Silicone | ||

| Other Resins | ||

| Surface-Treatment Chemicals | Curing Compounds | |

| Mold-Release Agents | ||

| Other Types | ||

| Waterproofing Solutions | Chemicals | |

| Membranes | ||

| By End-User Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

| By Geography | France | |

| Germany | ||

| Italy | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

Market Definition

- END-USE SECTOR - Construction chemicals consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of construction chemical products such as concrete admixtures, repair and rehabilitation chemicals, flooring resins, waterproofing solutions, anchors and grouts, adhesives and sealants, and surface treatment chemicals is considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms