Europe Organic Fertilizer Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 4.52 Billion |

| Market Size (2030) | USD 6.62 Billion |

| Growth Rate (2025 - 2030) | 7.95% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Organic Fertilizer Market Analysis by Mordor Intelligence

The Europe Organic Fertilizer Market size is estimated at 4.52 billion USD in 2025, and is expected to reach 6.62 billion USD by 2030, growing at a CAGR of 7.95% during the forecast period (2025-2030).

The European organic fertilizer industry is undergoing a significant transformation, driven by the European Union's commitment to sustainable agriculture and environmental protection. The European Commission is currently implementing a comprehensive revision of its fertilizer regulations for the first time since 2003, aimed at streamlining the entry of new fertilizing products, particularly those derived from biowaste and secondary raw materials. This regulatory overhaul is establishing stringent safety and quality standards for fertilizing products across all EU member states, fostering innovation in sustainable fertilizer practices. The region's dominant position in the global organic fertilizer landscape is evident, as Europe accounted for 41.7% of the global organic fertilizer market in 2022, highlighting its leadership in sustainable agricultural practices.

The production landscape of organic fertilizers in Europe is characterized by a diverse range of products and manufacturing processes, with a particular emphasis on circular economy principles. Meal-based fertilizers, derived from meat processing industry byproducts, have emerged as the primary product category, valued for their rich nutrient content, including nitrogen, phosphorus, potassium, and calcium. The industry has witnessed significant technological advancements in processing methods, particularly in the conversion of meat and bone meal into effective fertilizers, which simultaneously addresses waste management challenges and agricultural needs. This approach aligns perfectly with the EU's circular economy objectives, as it transforms what would otherwise be waste material into valuable agricultural inputs, including organic waste fertilizer.

Supply chain optimization and distribution networks have become increasingly sophisticated, with manufacturers focusing on regional sourcing and local distribution to minimize environmental impact. The European Union's emphasis on reducing carbon emissions has prompted fertilizer producers to adopt more sustainable production and distribution practices. Companies are investing in advanced processing facilities and developing innovative formulations that maximize nutrient availability while minimizing environmental impact. The industry has also seen a rise in partnerships between fertilizer manufacturers and waste management companies, creating more efficient resource utilization systems.

Looking ahead, the European organic fertilizer market is positioned for substantial growth, supported by the EU's ambitious environmental targets and changing agricultural practices. The European Commission's objective of increasing organic agriculture to a minimum of 25% of the EU's agricultural land by 2030 is driving significant investments in biological fertilizer production and distribution infrastructure. This transition is accompanied by increasing research and development activities focused on improving product efficiency and reducing production costs. The industry is witnessing a shift towards more integrated approaches, where natural fertilizer production is becoming part of larger sustainable agriculture ecosystems, incorporating advanced technologies for nutrient management and soil health optimization.

Europe Organic Fertilizer Market Trends and Insights

European Green Deal is majorly contributing for increasing organic cultivation.

- European countries are increasingly promoting organic farming, and the amount of land categorized as organic has increased significantly over the last decade. In March 2021, the European Commission launched an organic action plan to achieve the European Green Deal target of ensuring that 25% of agricultural land is under organic farming by 2030. Austria, Italy, Spain, and Germany are among the leading countries for organic agriculture in the European region. In Italy, 15.0% of the agriculture area is under organic farming, which is higher than the EU average of 7.5%.

- In 2021, there were 14.7 million hectares of organic land in the European Union (EU). The agricultural production area is divided into three main types of use: arable land crops (mainly cereals, root crops, and fresh vegetables), permanent grassland, and permanent crops (fruit trees and berries, olive groves, and vineyards). The area of organic arable land was 6.5 million hectares in 2021, the equivalent of 46% of the EU's total organic agricultural area.

- The organic areas of cereals, oilseeds, protein crops, and pulses in the European Union increased by 32.6% between 2017 and 2021, reaching more than 1.6 million hectares. With 1.3 million hectares under cultivation, perennial crops like Olives, grapes, almonds, and citrus fruits accounted for 15% of the organic land in the region in 2020. Spain, Italy, and Greece are major growers of organic olive trees, with an area of 256,507, 208,212, and 56,507 hectares, respectively, in 2021. Both olives and grapes are crucial for the European economy as they can be turned into specialty products that generate demand locally and internationally. The growing organic acreage in the region is expected to further strengthen the European organic cultivation industry.

Growing demand for organic food, rising the per capita spending, will have a positive effect over organic fertilizer market

- Consumers in Europe are purchasing more goods made using natural materials and methods. Even though organic food only makes up a small fraction of the total EU agricultural production, it is no longer a niche industry. The European Union represents the second-largest single market for organic goods internationally, with an average per capita spending of USD 74.8 annually. The per capita spending on organic food in Europe has doubled in the last decade. In 2020, Swiss and Danish consumers spent the most on organic food (USD 494.09 and USD 453.90 per capita, respectively).

- Germany is the largest organic food market in the European region and the second largest in the world after the United States, with a market size of USD 6.3 billion and a per capita consumption of USD 75.6 in 2021, as per Global Organic Trade data. The country accounted for 10.0% of the global organic food demand, with its share estimated to record a CAGR of 2.7% between 2021 and 2026.

- The French organic food market witnessed strong growth, with a 12.6% rise in retail sales in 2021. The country's per capita spending on organic food was recorded at USD 88.8 in 2021, as per Global Organic Trade data. In 2018, as recorded by the Agence BIO/Spirit Insight Barometer, 88% of French people declared having consumed organic products. Preserving health, environment, and animal welfare are the primary justifications for consumers of organic foods in France. The organic food industry has begun to grow in several other nations, including Spain, the Netherlands, and Sweden, with the opening of organic stores. The growth in organic sales was triggered during and after the COVID-19 pandemic, as consumers began paying more attention to health issues and becoming aware of the adverse effects of conventionally grown food.

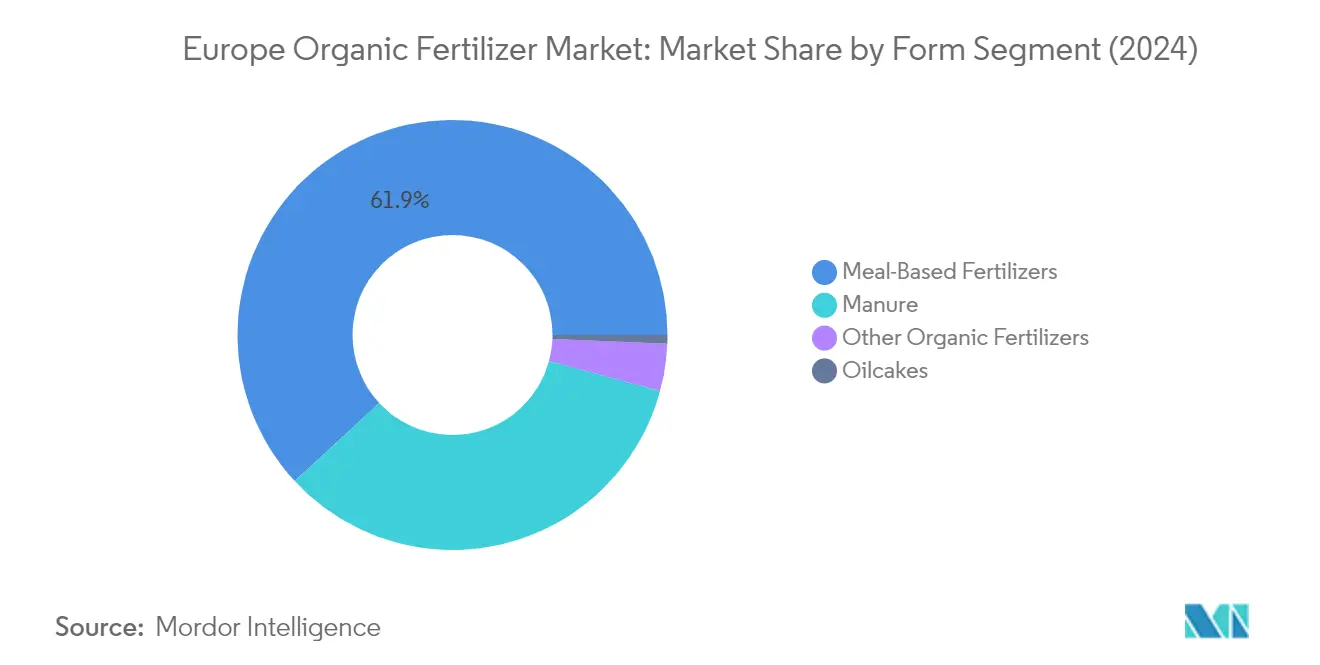

Segment Analysis: Form

Meal-Based Fertilizers Segment in Europe Organic Fertilizer Market

Meal-based fertilizers dominate the European organic fertilizer market, accounting for approximately 62% of the total market value in 2024. These fertilizers, which are byproducts of the meat processing industry, have gained significant traction due to their rich nutrient content, including nitrogen, phosphorus, potassium, and calcium, making them highly beneficial for agricultural crops. Row crops represent the primary consumers of meal-based fertilizers, with a share of about 78% among all crop types, followed by horticultural crops at 22%. The segment's prominence is particularly notable in France, which leads the European market with an 11.5% share. The popularity of meal-based fertilizers is further enhanced by their dual benefits not only do they provide essential nutrients for crop growth, but they also offer an environmentally friendly solution for disposing of meat processing waste, aligning with Europe's growing focus on sustainable agricultural practices.

Manure Segment in Europe Organic Fertilizer Market

The manure fertilizer segment is projected to exhibit the strongest growth in the European organic fertilizers market between 2024 and 2029, with an expected growth rate of approximately 8%. This robust growth is primarily driven by the significant amount of animal farming in the region, with the European Soil Data Center reporting substantial manure generation that is increasingly being utilized for agricultural purposes. The segment's growth is further supported by rising input costs for farmers, making livestock manure fertilizer an increasingly attractive option for reducing expenses and decreasing the region's dependence on non-EU nations for fertilizers. The Joint Research Centre's proposal for the safe use of processed manure as a chemical fertilizer alternative is expected to further accelerate adoption, particularly as it aligns with Europe's circular economy objectives and sustainable agricultural practices.

Remaining Segments in Form Segmentation

The oilcakes and other organic fertilizers segments complete the market landscape, each offering unique benefits to the agricultural sector. Oilcakes, derived from oilseed processing, are valued for their high nutrient content and effectiveness against soil-borne diseases and plant parasitic nematodes. While traditionally used as animal feed, they are gaining recognition as valuable organic fertilizers, particularly in horticultural and cash crop cultivation. The other organic fertilizers segment, which includes products like fish guano, bat guano, fish emulsion, vermicompost, and molasses, provides farmers with diverse options for sustainable soil enrichment. These segments, though smaller in market share, play crucial roles in offering farmers varied choices for different crop needs and soil conditions.

Segment Analysis: Crop Type

Row Crops Segment in Europe Organic Fertilizer Market

Row crops dominate the European organic fertilizers market, commanding approximately 78% of the total market value in 2024. This significant market share can be attributed to the region's extensive cultivation area for row crops, which accounts for about 82% of the total European organic crop cultivation area. Cereals are the primary row crops produced in Europe, representing nearly 69% of all organic row crop land. The segment's dominance is further strengthened by the widespread use of meal-based fertilizers, which are particularly effective at supplementing nitrogen requirements in row crops. France leads the European market in this segment, followed by Spain, reflecting these countries' strong agricultural sectors and commitment to organic farming practices.

Cash Crops Segment in Europe Organic Fertilizer Market

The cash crops segment is projected to experience the most rapid growth in the European organic fertilizers market between 2024 and 2029, with an expected growth rate of approximately 9%. This growth is primarily driven by the increasing adoption of organic farming practices for high-value crops such as coffee, tea, cocoa, sugar, and non-food crops like tobacco and cotton. Meal-based fertilizers and manure fertilizer are commonly used for cash crop production, with meal-based fertilizers accounting for about 66% of organic fertilizer consumption in this segment. Tea emerges as the dominant cash crop, representing approximately 88% of the total organic agricultural land dedicated to cash crops. The segment's growth is further supported by the proven effectiveness of organic fertilizers in improving soil health and increasing crop yields on marginal lands.

Remaining Segments in Crop Type

The horticultural crops segment plays a vital role in the European organic fertilizers market, focusing on fruits, vegetables, and specialty crops. This segment benefits from the increasing consumer demand for organic fruits and vegetables, particularly in countries like Spain and Italy, which are major producers of organic horticultural products. The segment utilizes a diverse range of organic fertilizers, with meal-based fertilizers and manures being the most commonly used products. The growth in this segment is supported by various European initiatives promoting organic farming practices and sustainable agriculture, particularly in the Mediterranean region where horticultural crop production is a significant agricultural activity.

Europe Organic Fertilizer Market Geography Segment Analysis

Europe Organic Fertilizer Market in France

France has established itself as the dominant force in the European organic fertilizers market, driven by its robust agricultural sector and strong government support for organic farming practices. The country's leadership position is evidenced by its approximately 12% market share in 2024. The French government's implementation of 'eco-schemes' has been instrumental in promoting organic agriculture by providing additional funding to farmers who adopt environmentally friendly practices. The country's diverse agricultural landscape, encompassing major crops like wheat, barley, corn, potatoes, and sugar beet, has created a substantial demand for organic fertilizer. Manure fertilizers are particularly popular among French farmers, owing to their cost-effectiveness, accessibility, and proven ability to enhance soil biodiversity. The country's commitment to sustainable agriculture is further reinforced by initiatives like the French National Federation of Organic Farming's "eau et bio" program, which facilitates large-scale organic agriculture development through collaborations with local organizations.

Europe Organic Fertilizer Market in Germany

Germany's organic fertilizer market is experiencing remarkable growth, with projections indicating an impressive growth rate of approximately 9% between 2024 and 2029. As the second-largest organic food market globally, Germany has set an ambitious target of converting 30% of its agricultural land into organic farms. The country's strategic approach includes initiatives to reduce distribution and logistics costs, making organic products more accessible to end consumers. Despite the significant increase in organic farming area, domestic production still struggles to meet the growing demand for organic food, creating substantial opportunities for local farmers. The country's new organic food production, packaging, and labeling rules have created barriers for exporters, further benefiting domestic producers. The combination of high organic food prices and attractive returns continues to motivate more farmers to transition to organic farming practices, particularly in the cultivation of cereals such as wheat, barley, corn, and rape.

Europe Organic Fertilizer Market in Spain

Spain has positioned itself as a major player in the European organic fertilizers market, ranking among the top three organic farming countries globally after Australia and Argentina. The nation's organic farming sector encompasses a diverse range of crops, including olive groves, cereals, nuts, vineyards, green plants, and pulses. Row crops dominate the organic fertilizer consumption, reflecting the country's extensive cultivation area. The Spanish organic farming industry has shown remarkable progress in expanding organic olive grove cultivation, which has become the country's primary organic crop. The government's commitment to sustainable agriculture is demonstrated through initiatives like the Ministry of Agriculture, Fisheries, and Food's support for organic farming practices. This comprehensive approach to organic agriculture has helped Spain maintain its position as a key contributor to Europe's organic farming landscape.

Europe Organic Fertilizer Market in Italy

Italy has emerged as a significant force in the European organic fertilizers market, supported by its robust organic food production infrastructure comprising 60,000 organic-producing companies. The country's organic agriculture industry is particularly strong in crops such as olive groves, vineyards, and cereals. The Italian government has demonstrated its commitment to organic farming through various initiatives, including funding for organic farming research and programs to encourage new organic producers. The country's approach to organic agriculture is characterized by a strong focus on quality and sustainability, with strict adherence to organic farming principles. The Italian organic food market's impressive growth trajectory has been supported by increasing consumer awareness and demand for organic products, making it an integral part of the European organic farming landscape.

Europe Organic Fertilizer Market in Other Countries

The organic fertilizer market in other European countries, including the Netherlands, Russia, Turkey, and the United Kingdom, demonstrates varying levels of development and growth potential. The Netherlands, with its advanced agricultural technology and strong focus on sustainable farming practices, has established itself as an important player in the organic fertilizer sector. Russia's emerging organic farming sector shows significant potential for growth, supported by government initiatives to identify suitable locations for organic agriculture development. Turkey's favorable climate and geographic location have made it a key supplier of organic fertilizers to Europe, while the United Kingdom's sustainable farming incentive scheme continues to drive the adoption of organic farming practices. These countries collectively contribute to the diverse and dynamic nature of the European organic fertilizer market, each bringing unique strengths and opportunities to the sector.

Competitive Landscape

Top Companies in Europe Organic Fertilizer Market

The European organic fertilizer market is characterized by companies focusing on sustainable and innovative product development to meet the growing demand for organic farming solutions. Manufacturers are increasingly investing in research and development to create enhanced formulations using novel raw materials like meat processing waste and seafood residues. Companies are expanding their distribution networks across the region while also pursuing strategic partnerships with agricultural universities and research institutions to strengthen their technical capabilities. Many players are adopting circular economy principles in their production processes, with some implementing standardized composting systems and others focusing on waste valorization. The industry is seeing increased collaboration between established players and local agricultural cooperatives to improve market penetration and farmer adoption of organic fertilizers.

Fragmented Market with Regional Leaders Emerging

The European organic fertilizers market exhibits a highly fragmented structure, with the top five players accounting for a relatively small portion of the total market share, while numerous small and medium-sized enterprises operate at regional and local levels. The market is characterized by a mix of large agricultural input companies diversifying into bio fertilizers and specialized manufacturers focused exclusively on organic and biological solutions. Local players often maintain strong positions in their respective regions through a deep understanding of soil conditions and crop requirements specific to their areas.

The industry is witnessing gradual consolidation through strategic acquisitions and partnerships, though this trend remains moderate compared to the conventional fertilizer sector. Companies with established distribution networks are increasingly partnering with or acquiring smaller innovative players to expand their organic product portfolios. Regional players are strengthening their positions through vertical integration, establishing direct relationships with raw material suppliers, and building strong connections with farming communities.

Innovation and Sustainability Drive Future Growth

Success in the European organic fertilizer market increasingly depends on companies' ability to develop innovative products while maintaining cost competitiveness. Manufacturers need to focus on establishing efficient supply chains for organic raw materials and implementing advanced processing technologies to improve product quality and consistency. Building strong relationships with organic farmers and agricultural cooperatives while providing comprehensive technical support and education about the benefits of biological fertilizers is becoming crucial for market success.

Future growth opportunities lie in developing specialized products for different crop segments and soil conditions while ensuring compliance with evolving European regulations. Companies need to invest in sustainable packaging solutions and efficient logistics networks to reduce environmental impact and operating costs. The ability to demonstrate product efficacy through field trials and scientific validation while maintaining transparent communication about sourcing and manufacturing processes will become increasingly important for market success. Players must also prepare for potential regulatory changes regarding organic farming practices and fertilizer composition standards. Additionally, the development of organic soil enhancers tailored to specific agricultural needs can offer a competitive edge in the market.

Europe Organic Fertilizer Industry Leaders

Agribios Italiana s.r.l.

Coromandel International Ltd.

HELLO NATURE ITALIA srl

ORGANAZOTO FERTILIZZANTI SPA

Suståne Natural Fertilizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2022: The company approved the merger between Liberty Pesticides and Fertilizers Limited (LPFL) and Coromandel SQM (India) Private Limited (CSQM) (wholly-owned subsidiaries), which came into effect on April 1, 2021. This merger is anticipated to expand the company's product portfolio, including its organic fertilizers, in the long run.

- May 2021: The company launched 'Godavari BhuBhagya,' a bio-enriched organic manure.

Europe Organic Fertilizer Market Report Scope

Manure, Meal Based Fertilizers, Oilcakes are covered as segments by Form. Cash Crops, Horticultural Crops, Row Crops are covered as segments by Crop Type. France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom are covered as segments by Country.| Manure |

| Meal Based Fertilizers |

| Oilcakes |

| Other Organic Fertilizers |

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| France |

| Germany |

| Italy |

| Netherlands |

| Russia |

| Spain |

| Turkey |

| United Kingdom |

| Rest of Europe |

| Form | Manure |

| Meal Based Fertilizers | |

| Oilcakes | |

| Other Organic Fertilizers | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops | |

| Country | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of organic fertilizers applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The crop nutrition function of agricultural biological consists of various products that provide essential plant nutrients and enhance soil quality.

- TYPE - Organic fertilizers are applied to provide essential crop nutrients and enhance the soil quality.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.