Europe LFP Battery Pack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

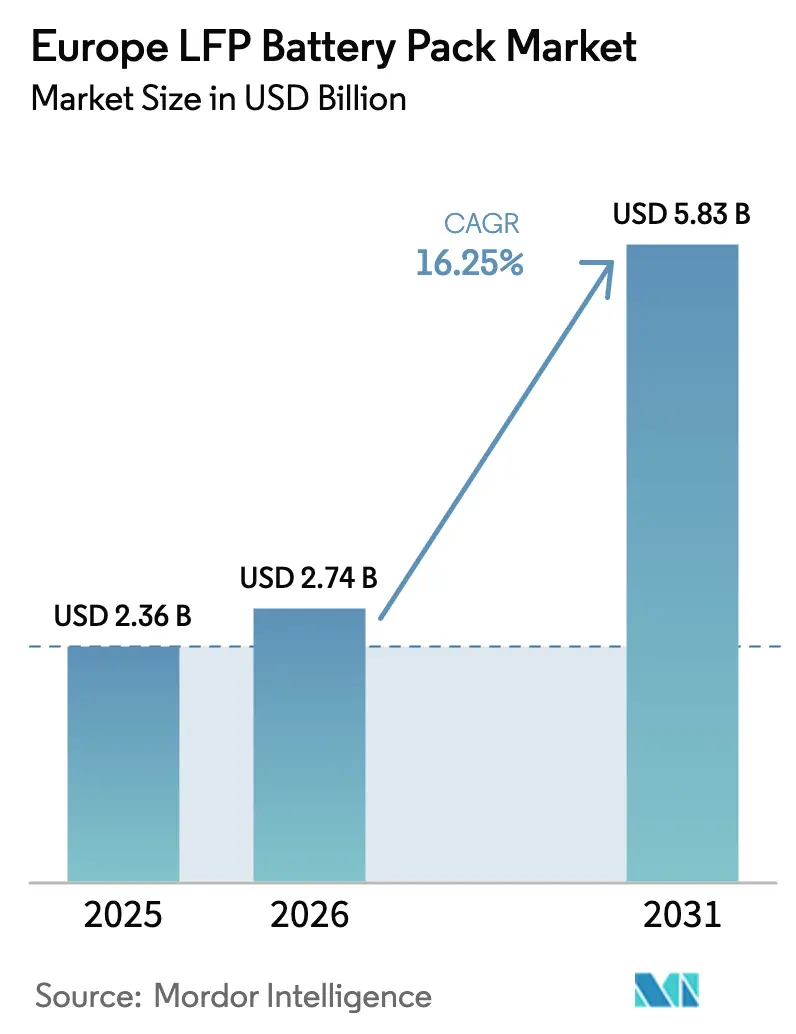

| Base Year Market Size (2025) | USD 2.36 Billion |

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 5.83 Billion |

| Growth Rate (2026 - 2031) | 16.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe LFP Battery Pack Market Analysis by Mordor Intelligence

The Europe LFP battery pack market size was valued at USD 2.36 billion in 2025 and estimated to grow from USD 2.74 billion in 2026 to reach USD 5.83 billion by 2031, at a CAGR of 16.25% during the forecast period (2026-2031). This expansion aligns with EU-wide carbon-reduction rules, tighter battery-passport requirements, and a shift by automakers toward chemistries that minimize exposure to nickel and cobalt price swings. Poland and Hungary have become production magnets as incentives lower the upfront cost of gigafactory projects, while a growing roster of passenger-car and commercial-vehicle programs locks in multi-year offtake agreements. Suppliers also benefit from the fire-safety head-room of LFP cathodes, a feature that has proved decisive in urban bus tenders across Germany, Sweden, and the Netherlands. At the technical level, rapid adoption of cell-to-pack (CTP) architecture, improved cylindrical-cell energy density, and 400–600 V power-train standardization reinforce near-term cost leadership.

Key Report Takeaways

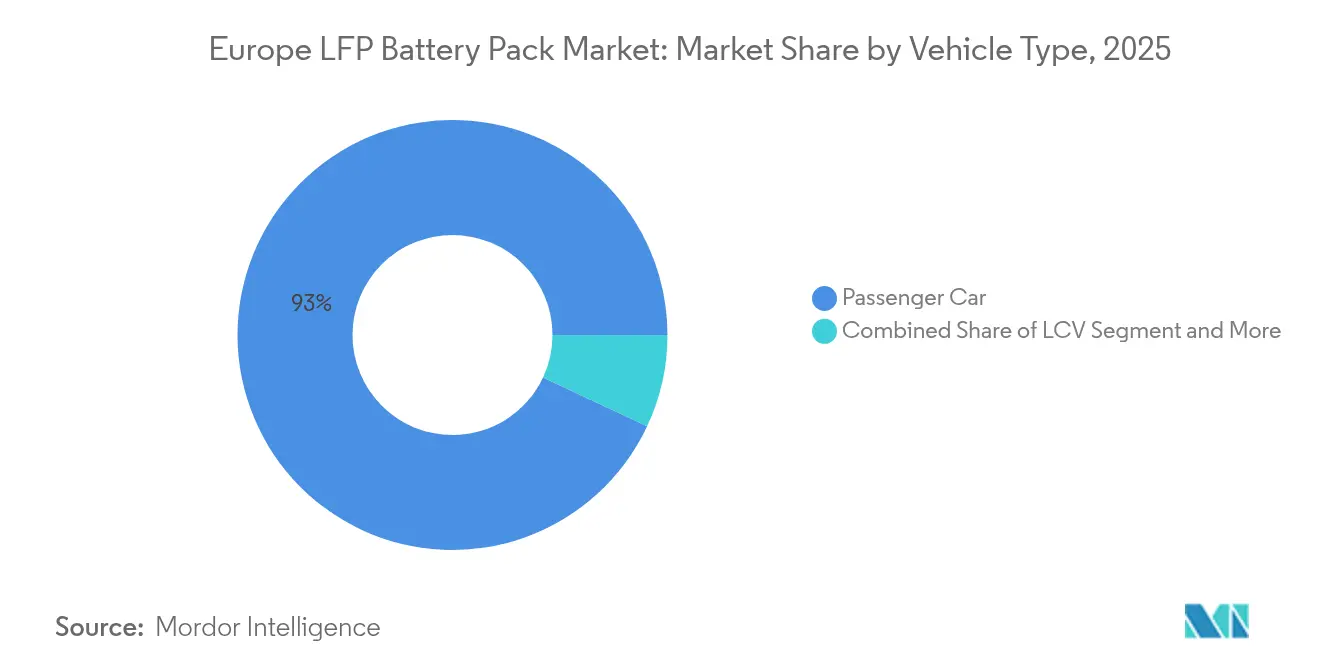

- By vehicle type, passenger cars held 93.02% revenue share in 2025, yet medium and heavy-duty trucks are expanding at a 16.62% CAGR through 2031.

- By propulsion type, battery-electric vehicles commanded 86.35% share, whereas plug-in hybrids are projected to surge at a 19.88% CAGR.

- By capacity, the 60–80 kWh bracket accounted for 28.74% of the Europe LFP battery pack market size in 2025; packs above 150 kWh are forecast to advance at an 17.54% CAGR.

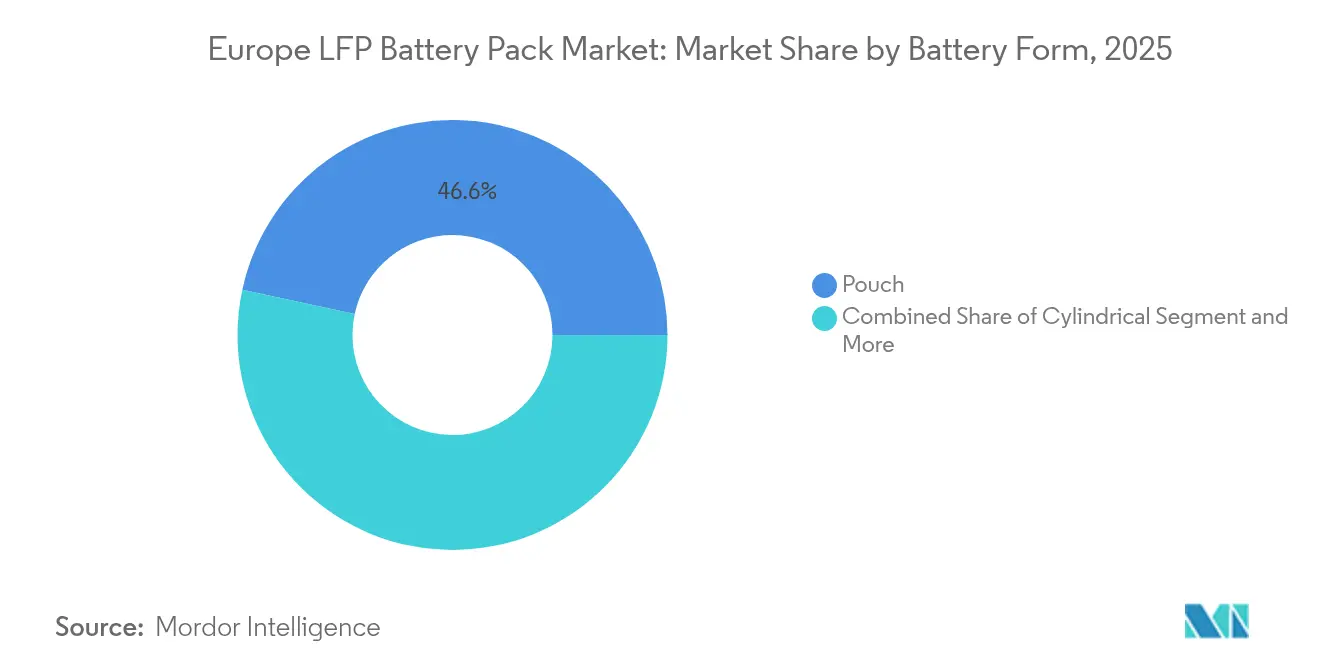

- By battery form, pouch cells captured 46.62% share, while cylindrical cells exhibit a 18.92% CAGR through 2031.

- By voltage class, 400–600 V systems represented 47.75% of installations in 2025, but above-800 V designs lead growth at 19.57% CAGR.

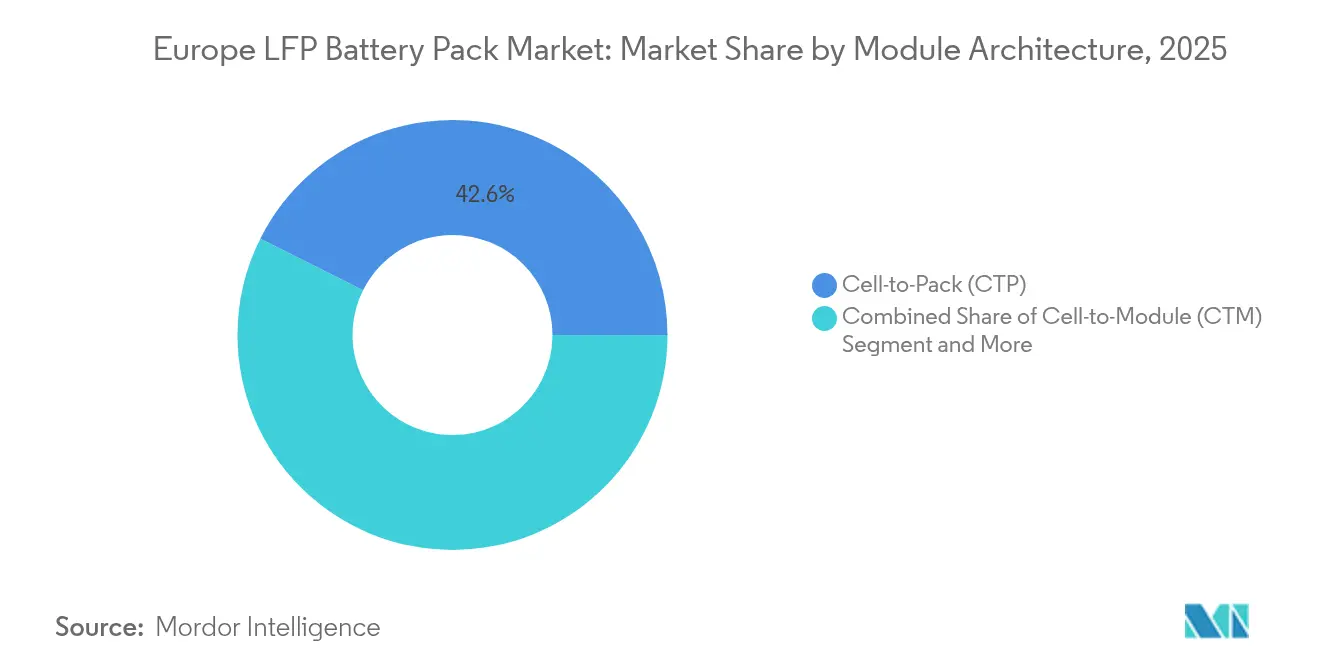

- By module architecture, cell-to-pack designs held 42.61% share and are set to expand at an 18.05% CAGR.

- By component, cathode led with 49.81% of the Europe LFP battery pack market share in 2025, while separator will record the fastest 17.21% CAGR to 2031.

- By country, Poland led with 34.74% of the Europe LFP battery pack market share in 2025, while Hungary recorded the fastest 21.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe LFP Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy-Fueled E-Mobility Targets | +3.2% | Germany, France, Netherlands | Medium term (2-4 years) |

| Leap-In Cell-To-Pack Design | +2.8% | Hungary, Poland hubs | Short term (≤ 2 years) |

| Nickel Volatility Pushes LFP | +2.5% | Germany premium OEMs | Medium term (2-4 years) |

| EU Battery-Passport Mandates | +2.1% | EU-wide | Short term (≤ 2 years) |

| Fire-Safety Unlocks Tenders | +1.9% | Scandinavia, Germany | Long term (≥ 4 years) |

| Sodium-Ion Pilot Lines Scale | +1.7% | France, Sweden | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subsidy-Fueled E-Mobility Targets (EU Fit-for-55, REPowerEU)

Member states, under the Fit-for-55 and REPowerEU initiatives, have allocated significant funding to support battery manufacturing incentives, with a focus extending to the year 2030 [1]“Fit for 55 Package,” European Commission, europa.eu. Germany allocated significant investment in 2024, narrowing the capital gap for gigafactory construction. Building a typical 20 GWh LFP plant requires substantial investment, where incentive stacking can significantly reduce the equity outlay. Investors also gain first-mover access to the digital battery passport regime that becomes mandatory in 2027. Compliance with carbon footprint and recycled content metrics enhances tender eligibility for EU fleet contracts.

Leap-in Cell-to-Pack Design Cost Cuts

Eliminating modules reduces pack materials, minimizes interconnect losses, and increases volumetric energy density. The design choice lets LFP compete head-to-head with NMC in 40–80 kWh passenger packs. Tesla’s Berlin Gigafactory demonstrates added gains from marrying CTP with structural battery integration, though EU type-approval still lengthens time-to-market for fully load-bearing packs. European suppliers now tool new lines around CTP as the default, making legacy module formats an exception.

High-Nickel Cost Volatility Pushes OEMs to LFP

In 2024, nickel prices experienced significant fluctuations, introducing a considerable cost risk for NMC cathodes. Volkswagen Group reacted by targeting an increase in LFP sourcing in the coming years. Stellantis followed by fast-tracking LFP qualification across its C-segment platforms, citing notable savings. The strategy also hedges geopolitical exposure, given nickel mining’s concentration in Russia and Indonesia. Chinese cell majors capitalize on this pivot, locking in multi-billion-dollar offtake deals with BMW and Mercedes-Benz for European supply.

Inter-EU Battery-Passport Mandate Favors Local Packs

From 2027, every traction pack sold in Europe must carry verifiable CO₂ Footprint, origin, and recycled content data. CATL responded by establishing a full-pack assembly facility in Hungary, earmarking additional investment for compliance, IT, and logistics. OEMs are already demanding pre-compliant packs for model-year 2026 launches, thereby funneling volume toward local plants and away from imported assemblies. Suppliers able to document localized value add a scoring edge in competitive RFQs, reinforcing on-shoring momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gigafactories Shrink Outsourcing | –2.8% | Germany, France, Sweden | Medium term (2-4 years) |

| Slow 800V Adoption Limits LFP | –2.1% | Germany, United Kingdom | Long term (≥ 4 years) |

| Graphite and Lithium Bottlenecks | –1.9% | EU-wide | Short term (≤ 2 years) |

| Recycling Lag for LFP | –1.4% | EU-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

In-house OEM Gigafactories Shrink Outsourcing Pool

Volkswagen's PowerCo program is leading significant investments by European automakers in captive battery plants, aiming to achieve substantial annual capacity by the end of the decade [2]“Cell Manufacturing Roadmap,” Volkswagen PowerCo, powerco.de. Mercedes-Benz and BMW have similar carve-outs via joint ventures, siphoning volume from independent cell makers. Fragmentation raises fixed-cost hurdles because each closed-loop plant operates at a sub-economy scale. As captive output rises, the addressable pool for stand-alone suppliers shrinks, tempering the growth runway for the European LFP battery pack market. Smaller producers may pivot to niches such as buses, stationary storage, and micromobility rather than compete head-on with OEM gigafactories.

Slow 800 V Adoption Limits LFP in Premium BEVs

Porsche’s 800 V Taycan achieves 270 kW peak charge rates on silicon-NMC packs; LFP tops out near 200 kW under similar conditions [3]“800 V Platform Fast-Charge Study,” Porsche Engineering, porsche.com. As IONITY upgrades to 400 kW cabinets, premium OEMs view ultra-fast charging as a table stake. Audi and BMW, therefore, retain NMC for halo models despite LFP cost wins. The European LFP battery pack industry thus cedes high-margin premium volume until higher-voltage-tolerant LFP variants mature. Suppliers are pursuing doped-graphite or lithium-manganese-iron-phosphate tweaks, but commercial timelines extend beyond 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Demand Accelerates Despite Passenger-Car Dominance

Passenger cars generated 93.02% of the revenue in 2025, giving them the largest market share in the Europe LFP battery pack market. The segment benefits from stable model cycles, multi-year supply agreements, and consumer acceptance of 60–80 kWh packs, which provide a real-world range of 280–300 km. Tesla’s Model 3 and Model Y variants have demonstrated that LFP chemistry can meet daily-use patterns while reducing the bill of materials relative to NMC packs. Fleet managers for ride-hailing and subscription services also value LFP’s 6,000-cycle life, which helps maintain resilient residual values. In contrast, medium and heavy-duty trucks post the fastest 16.62% CAGR because total-cost-of-ownership calculations favor cycle life over gravimetric energy density. Volvo’s FH Electric and Mercedes-Benz eActros feature 300 kWh-plus LFP packs that achieve parity with diesel drivelines, narrowing the payback gap for long-haul freight.

Light commercial vans and city buses offer a steady upside as urban-delivery platforms and municipal transit agencies transition from NMC to LFP for enhanced fire-safety headroom. Hamburg’s 2024 tender required LFP batteries exclusively, triggering a surge in orders for e-bus range. Combined, these trends keep the Europe LFP battery pack market on a volume trajectory that widens beyond passenger cars toward commercial duty cycles that demand durability and simplified thermal management.

By Propulsion Type: Plug-In Hybrids Post Strongest Growth

Battery-electric vehicles commanded 86.35% demand in 2025, supported by EU fleet CO₂ mandates and falling pack prices. Total BEV volumes expand alongside entry-level hatchbacks and C-segment crossovers that adopt 400–600V platforms optimized for 60–80kWh LFP packs. Yet plug-in hybrids book the highest 19.88% CAGR as automakers exploit LFP’s thermal robustness to deliver compact 25–30 kWh packs without costly cooling loops. BMW’s X5 xDrive45e and Mercedes-Benz GLE 350de each save significantly per unit by moving to LFP cells, a margin lift that offsets rising power-train electronics costs.

Policy design also fuels PHEV momentum: France’s bonus-malus scheme and Germany’s company-car tax break reward vehicles with an electric range of at least 80 km, a target easily met by LFP at modest pack sizes. The configuration bridges charging infrastructure gaps in rural areas, providing buyers with combustion backup while still qualifying for low company car tax brackets. As a result, the Europe LFP battery pack market size attached to PHEVs is projected to expand between 2026 and 2031, gradually narrowing the capacity gap with BEVs.

By Capacity: High-Energy Packs Lead Innovation Curve

The 60–80 kWh bracket held 28.74% of the Europe LFP battery pack market size in 2025, mirroring mainstream C-segment vehicle requirements. Automakers lock these packs into modular skateboard designs, securing scale economies on both cell and enclosure tooling. Above-150 kWh packs, however, clock an 17.54% CAGR, driven by the electrification of heavy trucks and premium SUVs that require towing capability or long-distance duty cycles. Mercedes-Benz’s eTruck prototypes run 300 kWh LFP packs, cutting diesel operating costs over years of service periods. The surge forces suppliers to upgrade thermal-interface materials and high-voltage busbars that can handle multi-hundred-kilowatt continuous outputs.

Below-40 kWh volumes remain niche, covering urban delivery micro-vans and select e-quadricycles. Cycle-life economics in this band favor LFP even more strongly, yet absolute material demand lags due to limited energy content. Overall, capacity stratification illustrates that the Europe LFP battery pack market can extend from compact run-abouts to long-haul Class 8 trucks without major chemistry changes—only packaging and cooling tweaks.

By Battery Form: Cylindrical Cells Close on Pouch Leadership

Pouch cells retained a 46.62% share in 2025, thanks to investments in legacy lines made by LG Energy Solution and Northvolt. The format’s flexible footprint accommodates diverse floor plan geometries, a plus for multi-platform OEM programs. Cylindrical designs are now growing at a 18.92% CAGR after Tesla’s structural battery work validated 4680-form-factor LFP cells, which achieved 255 Wh/kg. Automated winding and tableless architectures bring throughput gains that reduce conversion costs, making cylindrical the low-cost frontrunner for future high-volume BEVs.

Prismatic cells maintain stable demand in commercial vehicles, where rigid casings serve as both structural members and load-bearing components. Recycling considerations slightly favor cylindrical units because automated disassembly lines already exist in European pilot plants, a factor that aligns with the rollout of the battery passport. Collectively, format convergence pushes the Europe LFP battery pack market toward manufacturing templates that promise sub-USD 80 per kWh at the pack level over the coming years.

By Voltage Class: Transition to 800 V Gains Pace

Systems in the 400–600 V range accounted for 47.75% of installations in 2025, as most C-segment BEVs and light vans operate comfortably within these voltages. Above-800 V architectures, though, race ahead with a 19.57% CAGR as Porsche’s Taycan benchmark reshapes charging-time expectations. OEMs are eyeing 350 kW public chargers rolling out via the IONITY upgrade plan, a path that compresses charging time to a few minutes for large-battery sedans.

LFP’s flat discharge curve helps moderate heat spikes during high-current phases, but its lower nominal voltage pushes pack-string counts higher, nudging cost up. Suppliers respond with advanced battery-management ICs that support cell-balancing accuracy, thereby minimizing the risk of overcharging at high pack voltages. The Europe LFP battery pack market share captured by 800 V platforms is expected to increase once doped-graphite anodes raise voltage limits sufficiently to meet 350 kW charge protocols without exceeding 50 °C core temperatures.

By Module Architecture: Cell-to-Pack Becomes New Default

Cell-to-pack designs accounted for 42.61% of shipments in 2025 and are projected to grow at an 18.05% CAGR. Eliminating module housings removes up to 20 kg of structural content in a typical 75 kWh pack, freeing volume that lifts usable energy. Northvolt and ACC designed their Hungarian and French gigafactories around CTP tooling from the outset, thereby accelerating their learning curves compared to retrofits.

Module-to-pack retains a place in service-critical fleets such as postal vans or ride-share sedans, where hot-swap capability limits downtime. However, cost pressure from mainstream passenger-car programs drives OEMs toward CTP as the baseline architecture. Ongoing EU end-of-life directives may tilt the balance again if recyclers find module-level disassembly more economical than pack-level shredding. For now, CTP underpins the next efficiency jump in the Europe LFP battery pack market.

By Component: Cathode Commands Highest Value Capture

Cathode materials accounted for 49.81% of the bill-of-materials value in 2025, underscoring their significant influence on performance and cost. European producers focus on nano-coating and particle-size tuning to cut internal resistance and raise power density. Separator technology follows with a 17.21% CAGR as ceramic-coated films extend thermal stability envelopes needed for fast-charge duty cycles.

Graphite anodes undergo silicon-doping trials that target a significant energy-density uplift without jeopardizing cycle life—necessary for long-haul logistics fleets chasing payload parity. Electrolyte blends are shifting toward localized solvent sourcing to mitigate supply-risk exposure. Component segmentation signals new revenue pools for the Europe LFP battery pack industry as tier-two suppliers scale up functional coatings and specialty salts.

Geography Analysis

Poland heads the region with 34.74% Europe LFP battery pack market share in 2025. The country’s Wrocław-based LG Energy Solution plant, and CATL plans a second 100 GWh site by 2028. A significant incentive package covering land, tax, and training reduces the effective capital expenditure per gigawatt-hour (GWh), making Poland the cost leader for greenfield builds. Supply-chain depth around stamped enclosures, harnesses, and power electronics further anchors local value creation.

Hungary posts the fastest 21.28% CAGR to 2031 after CATL’s Debrecen mega-project locked in 100 GWh output by 2027. Mercedes-Benz, BMW, and Audi's final assembly sites are located within 250 km of each other, reducing logistics lead times. The nation’s flat corporate tax rate, combined with EU structural fund co-financing, amplifies capital returns. Samsung SDI and SK On expansions round out a cluster effect that pools vendor bases for separator film and electrolyte.

Germany remains pivotal, despite higher labor costs, as it hosts premium-segment programs that demand advanced battery management integration. Northvolt’s Schleswig-Holstein plant, set for 60 GWh by 2029, leans on abundant wind power to meet CO₂-footprint caps embedded in the battery passport. France, Italy, and Sweden contribute specialized niche output—urban-mobility packs, marine propulsion modules, and grid-storage racks—while the United Kingdom lags amid post-Brexit regulatory uncertainty. Collectively, these dynamics ensure the Europe LFP battery pack market maintains production redundancy across multiple jurisdictions, buffering political-risk exposure.

Competitive Landscape

The Europe LFP battery pack market shows moderate concentration. CATL and BYD anchor the leaderboard by co-locating cell and pack assembly inside the EU customs zone, a hedge against potential anti-dumping duties. LG Energy Solution and Samsung SDI defend their share via legacy OEM deals, as well as incremental improvements—such as heat-resistant separators and high-precision stacking—that enhance energy density on pouch lines. Northvolt and ACC pursue vertical integration, touting renewable-energy footprints and closed-loop recycling as differentiators for premium German brands.

Technology race themes focus on manufacturing scale, localized supply chains, and compliance IT rather than outright chemistry breakthroughs. CATL’s Qilin cylindrical cell signals a path to sub-USD 70 per kWh packs, while LG Energy Solution pilots dry-electrode coating that can shave energy consumption in calendaring. BYD leverages its in-house bus division to capture municipal tenders that specify LFP for safety, giving it a captive demand base independent of passenger-car cycles.

Strategic alliances tighten. Stellantis inked a EUR 4.1 billion (~USD 4.7 billion) 50-50 venture with CATL for a Zaragoza plant targeting 50 GWh by 2026, safeguarding mid-range passenger-car supply [4]“Joint Venture Press Release 2024,” Stellantis, stellantis.com. Tesla’s Berlin Gigafactory sources cylindrical LFP cells mainly from its own Nevada output while tapping third-party cathode powder from BASF’s Harjavalta refinery in Finland. The likely outcome is a consolidation toward three or four full-line suppliers plus a ring of niche specialists in marine, grid, and off-highway segments, maintaining a balanced yet competitive Europe LFP battery pack market.

Europe LFP Battery Pack Industry Leaders

Contemporary Amperex Technology Co., Limited (CATL)

BYD Company Ltd.

LG Energy Solution, Ltd.

Samsung SDI Co., Ltd.

CALB Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: CATL unveiled Shenxing Pro, an LFP cell claimed to remain free of flame and smoke during thermal runaway, aimed at Europe-bound EVs.

- December 2024: Stellantis and CATL agreed to spend up to EUR 4.1 billion (~USD 4.7 billion) on a 50 GWh LFP battery plant in Zaragoza, Spain, with production slated for late 2026.

Europe LFP Battery Pack Market Report Scope

Bus, LCV, M&HDT, Passenger Car are covered as segments by Body Type. BEV, PHEV are covered as segments by Propulsion Type. 15 kWh to 40 kWh, 40 kWh to 80 kWh, Above 80 kWh, Less than 15 kWh are covered as segments by Capacity. Cylindrical, Pouch, Prismatic are covered as segments by Battery Form. Laser, Wire are covered as segments by Method. Anode, Cathode, Electrolyte, Separator are covered as segments by Component. Cobalt, Lithium, Manganese, Natural Graphite, Nickel are covered as segments by Material Type. France, Germany, Hungary, Italy, Poland, Sweden, UK, Rest-of-Europe are covered as segments by Country.| Passenger Car |

| LCV |

| M&HDT |

| Bus |

| BEV |

| PHEV |

| Below 15 kWh |

| 15-40 kWh |

| 40-60 kWh |

| 60-80 kWh |

| 80-100 kWh |

| 100-150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Below 400 V (48-350 V) |

| 400-600 V |

| 600-800 V |

| Above 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| France |

| Germany |

| Hungary |

| Italy |

| Poland |

| Sweden |

| United Kingdom |

| Rest of Europe |

| By Vehicle Type | Passenger Car |

| LCV | |

| M&HDT | |

| Bus | |

| By Propulsion Type | BEV |

| PHEV | |

| By Capacity | Below 15 kWh |

| 15-40 kWh | |

| 40-60 kWh | |

| 60-80 kWh | |

| 80-100 kWh | |

| 100-150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Below 400 V (48-350 V) |

| 400-600 V | |

| 600-800 V | |

| Above 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator | |

| By Country | France |

| Germany | |

| Hungary | |

| Italy | |

| Poland | |

| Sweden | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- Battery Chemistry - LFP battery type is considred under the scope of battery chemistry.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, passenger cars, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 4

- Vehicle Type - Vehicle type considered under this segment include passenger vehicles, and commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms