Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Growth Rate | 0.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Industrial Air Quality Control Systems Market Analysis by Mordor Intelligence

The Europe Industrial Air Quality Control Systems Market is expected to register a CAGR of 0.6% during the forecast period.

The European industrial landscape continues to undergo significant transformation in its approach to air quality management, with carbon dioxide emissions from energy, flaring, and industrial processes reaching approximately 3,990 million tons in 2021. The power sector remains the most significant contributor, accounting for about 30% of Europe's CO2 emissions, followed by transportation and industrial combustion. This has led to increased adoption of advanced industrial air pollution control systems across industries, particularly in regions with high industrial concentration. The European Union's recent proposal to update the Industrial Emissions Directive, covering approximately 50,000 large industrial installations, demonstrates the region's commitment to achieving zero-pollution targets by 2050.

The chemical and textile industries are witnessing substantial regulatory changes, with over 3,000 chemical and 300 textile industrial plants now required to comply with new environmental norms under the EU Industrial Emissions Directive as of January 2023. These regulations have introduced stricter binding levels for volatile organic compounds (VOCs) and established emission caps for various pollutants. The implementation timeline gives existing installations four years to adapt, while new facilities must comply immediately, driving the demand for advanced industrial air quality control systems across these sectors.

Industrial air pollution remains a critical health concern in Europe, with over 90% of the urban population in the European Union exposed to fine particulate matter levels above WHO guideline levels in 2020. This exposure resulted in more than 230,000 premature deaths in the EU-27 region, highlighting the urgent need for more effective industrial emission control measures. Major industry players are responding to this challenge with innovative solutions, as evidenced by Anguil Environmental Systems' achievement of over 2,200 installations globally, demonstrating the growing adoption of industrial air quality control systems.

The market is experiencing a significant shift in technology adoption, particularly in response to the European Commission's Clean Air Policy Package. Leading companies are introducing advanced solutions, as demonstrated by CTP's launch of the RTO I-SCR system in 2023, capable of breaking down approximately 500 metric tons of nitrous oxide annually. This technological advancement represents a significant step forward in reducing industrial emissions, equivalent to eliminating the climate impact of 150,000 metric tons of CO2. The industry's focus on innovation and efficiency improvements continues to drive the development of more sophisticated industrial emission monitoring systems.

Europe Industrial Air Quality Control Systems Market Trends and Insights

Presence of Stringent Regulation for Air Quality Management

The European Union has implemented comprehensive regulatory frameworks to control industrial emission control and improve air quality across the region. In January 2023, new environmental norms under the EU Industrial Emissions Directive were published for the chemical and textile industries, affecting over 3,000 chemical and 300 textile industrial plants. These facilities must comply with legal norms within four years, while new facilities must comply immediately. The regulations specifically target emission standards for 34 key air pollutants from the chemical industry and include stricter binding levels for volatile organic compounds (VOCs), with particular attention paid to carcinogenic or toxic substances.

The regulatory landscape continues to evolve with significant developments in country-specific initiatives. For instance, in August 2022, the UK Government established a new Best Available Techniques framework to boost industrial emission control standards and reduce air pollution. This framework allows regulators and industry to work together to identify and apply up-to-date, challenging standards for reducing harmful emissions. Similarly, in September 2022, the UK's textile and chemical sectors were required to adopt sustainable best practices under this framework, demonstrating the increasing regulatory pressure on industries to improve their environmental performance. These regulations are particularly significant as power plants are major emission sources, accounting for about 98% of SO2 emissions, 94% of mercury emissions, 86% of NOx emissions, and 83% of fine particulate emissions in the power sector.

The stringent regulations have led to specific industrial requirements and technological adaptations. For example, in 2022, according to the European Environment Agency (EEA), the Mediterranean Sea was designated as an Emission Control Area for sulfur oxides, requiring vessels to use marine fuel with lower sulfur content from May 2025. The permissible limit will be reduced from the current 0.5% to 0.1%, potentially preventing 1,000 premature deaths per year and helping prevent 2,000 cases of child asthma annually. Additionally, the Industrial Emissions Directive (IED) review by the Commission as part of the European Green Deal outlines the use of Best Available Techniques (BAT) to reduce emissions from industrial sources, demonstrating the comprehensive approach to emissions control in the region. This has also led to advancements in industrial air treatment systems and industrial air handling systems to meet these stringent standards.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Type

Electrostatic Precipitators Segment in Europe Industrial Air Quality Control Systems Market

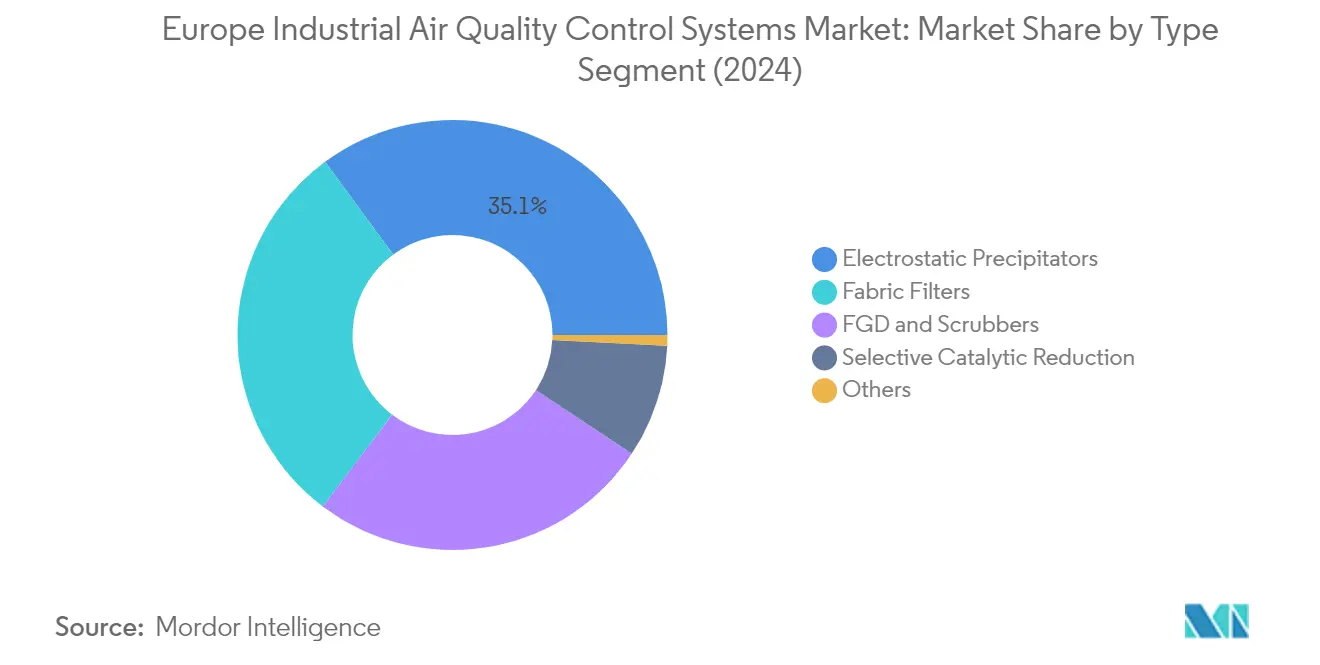

The Electrostatic Precipitators (ESP) segment dominates the European industrial air quality control systems market, holding approximately 35% market share in 2024. This significant market position is attributed to ESP's high collection efficiencies of up to 99.95% for particulate matter and their extensive application across power generation, cement, and industrial sectors. The segment's prominence is further strengthened by its ability to handle very large gas volumes and heavy dust loads with low-pressure drops, along with its capability to handle corrosive materials, wet materials, and high temperatures. The technology's durability and relatively low operating costs have made it particularly attractive for large industrial installations, especially in regions with stringent emission control regulations. Additionally, the use of industrial electrostatic precipitator systems enhances the efficiency of industrial air cleaning systems, making them indispensable in maintaining air quality standards.

Flue Gas Desulfurization Segment in Europe Industrial Air Quality Control Systems Market

The Flue Gas Desulfurization (FGD) and scrubbers segment is projected to exhibit the highest growth rate of approximately 0.8% during the forecast period 2024-2029. This growth is primarily driven by increasing environmental regulations regarding sulfur dioxide emissions across Europe, particularly in the power generation sector. The segment's expansion is further supported by the rising adoption of coal as an alternative energy source in several European countries amid energy security concerns. The technology's ability to achieve SO2 removal efficiencies of over 90% and the growing demand for wet scrubbers in various industrial applications are key factors contributing to its accelerated growth. Additionally, the segment benefits from continuous technological advancements in scrubber designs and increasing investments in retrofit installations across existing industrial facilities. The integration of industrial scrubber technologies is pivotal in meeting these stringent standards.

Remaining Segments in Type

The remaining segments in the market include Selective Catalytic Reduction (SCR), Fabric Filters, and other technologies. Fabric filters have established a strong presence in the market due to their high efficiency in particulate matter removal and flexibility in handling various industrial applications. The SCR segment continues to play a crucial role in nitrogen oxide reduction, particularly in power plants and industrial boilers. Other technologies, while representing a smaller market share, contribute to specialized applications and niche requirements in the industrial air quality control landscape. These segments collectively provide a comprehensive solution portfolio for different industrial emission control needs, complementing the major technologies in addressing specific pollutant removal requirements across various industrial sectors. The role of industrial dust collection systems is also critical in these applications, ensuring compliance with environmental standards.

Segment Analysis: Application

Power Generation Segment in Europe Industrial Air Quality Control Systems Market

The power generation industry dominates the European industrial air quality control systems market, holding approximately 39% market share in 2024. This significant share is primarily driven by the increasing electricity demand and stringent emission control regulations in the region. The sector's dominance is further reinforced by recent geopolitical developments like the Russia-Ukraine conflict, which has led European countries to rely more on coal for energy security, necessitating advanced air quality control systems. Several countries, including Germany, France, and Belgium, have extended or reactivated their coal power plants to maintain energy security, while simultaneously implementing strict emission control measures, driving the demand for air quality control systems in this sector. The integration of industrial gas cleaning technologies is crucial in this context, ensuring compliance with emission standards.

Power Generation Segment in Europe Industrial Air Quality Control Systems Market

The power generation segment is also projected to be the fastest-growing segment during the forecast period 2024-2029. This growth is primarily attributed to the increasing focus on reducing emissions from thermal power plants while maintaining energy security. The segment's growth is further supported by the European Union's recent taxonomy proposal that classifies certain nuclear and natural gas energy projects as "green" investments if they meet specific emission criteria. Additionally, the implementation of new environmental norms under the EU Industrial Emissions Directive and the growing trend of upgrading existing power plants with advanced air quality control systems are expected to drive the segment's growth.

Remaining Segments in Application

The other significant segments in the market include the iron and steel industry, cement industry, chemicals and fertilizers, automotive industry, and oil & gas industry. The iron and steel industry represents the second-largest segment, driven by stringent emission regulations and the industry's shift toward cleaner production methods. The cement industry maintains a substantial market share due to its high emission intensity and ongoing modernization efforts. The chemicals and fertilizers segment is influenced by the growing chemical industry and increasing environmental regulations. The automotive segment is gradually transitioning toward electric vehicle manufacturing, while the oil & gas industry's demand is primarily driven by emission control requirements in refineries and processing facilities.

Segment Analysis: Emissions

Nitrogen Oxides (NOx) Segment in Europe Industrial Air Quality Control Systems Market

Nitrogen oxides (NOx) emissions represent the dominant segment in the European industrial air quality control systems market, driven by extensive regulations and widespread industrial applications. The segment's prominence is attributed to NOx being one of the most common and heavily-regulated pollutants across various industries, including power generation, cement manufacturing, and automotive sectors. The control of NOx emissions has become particularly critical in urban and industrialized regions where the concentration of these pollutants poses significant health and environmental risks. The implementation of stringent emission standards by European countries, particularly for thermal power plants and industrial boilers, has led to increased adoption of NOx control technologies such as Selective Catalytic Reduction (SCR) and Selective Non-Catalytic Reduction (SNCR) systems. The segment's growth is further supported by the European Union's commitment to reducing NOx emissions by 65% compared to 2005 levels by 2030, driving continuous investments in NOx control technologies across industrial facilities.

Sulfur Oxides (SOx) Segment in Europe Industrial Air Quality Control Systems Market

The Sulfur Oxides (SOx) segment is experiencing rapid growth in the European industrial air quality control systems market, driven by intensifying environmental regulations and technological advancements in control systems. The segment's growth is particularly evident in countries like Serbia, Bulgaria, and other Eastern European nations where coal-fired power plants are still operational and require significant SOx emission reductions. The implementation of the Industrial Emissions Directive (IED) and its Best Available Techniques (BAT) requirements has created a strong demand for advanced SOx control technologies, particularly in the power generation and industrial sectors. The maritime sector's adoption of SOx scrubbers, following the IMO 2020 regulations limiting sulfur content in marine fuels, has further accelerated the segment's growth. The development of more efficient and cost-effective desulfurization technologies, combined with increasing pressure to meet environmental standards, continues to drive innovation and investment in SOx control systems across Europe.

Remaining Segments in Emissions

The Particulate Matter (PM) segment plays a crucial role in the European industrial air quality control systems market, addressing both PM10 and PM2.5 emissions that pose significant health risks in urban and industrial areas. This segment is particularly important in countries like Poland, France, and Turkey, where industrial activities and domestic heating contribute significantly to particulate matter pollution. The control of PM emissions involves various technologies, including electrostatic precipitators, fabric filters, and wet scrubbers, each serving specific industrial applications. The segment's importance is underscored by the WHO's revised air quality guidelines, which have set more stringent limits for PM concentrations, driving the adoption of more sophisticated control technologies. The integration of PM control systems with other emission control technologies has become increasingly common, reflecting a holistic approach to air quality management in industrial settings.

Europe Industrial Air Quality Control Systems Market Geography Segment Analysis

Industrial Air Quality Control Systems Market in Germany

Germany represents the largest market for industrial air filtration and industrial ventilation systems in Europe, accounting for approximately 12% of the total market value in 2024. The country's significant market position is driven by its robust industrial base, particularly in power generation, chemical manufacturing, and automotive sectors. The German government's commitment to reaching climate neutrality by 2045 and reducing greenhouse gas emissions by at least 65% by 2030 compared to 1990 levels continues to drive demand for air quality control systems. While the country is transitioning toward renewable energy, coal and natural gas remain significant contributors to the power generation mix, necessitating advanced air quality control systems. The chemical industry, being the third-largest industrial sector after automotive and mechanical engineering, further strengthens the market despite recent challenges in European demand. Additionally, Germany's position as a hub for electric vehicle manufacturing, with significant investments from companies like Volkswagen, Tesla, and BYD, is creating new opportunities for industrial air purification systems in the automotive sector.

Industrial Air Quality Control Systems Market in France

France is emerging as the most dynamic market in the European region, with a projected growth rate of approximately 2% during 2024-2029. The country's market is characterized by its diverse industrial landscape, with particular strength in nuclear power generation, chemical manufacturing, and automotive production. France's chemical industry plays a central role in the modern chemicals sector, manufacturing a wide range of products from basics to specialties and fine chemicals for pharmaceuticals. The country's commitment to environmental protection and stringent emissions regulations continues to drive the adoption of air quality control systems. The automotive sector's transformation, particularly the shift toward electric vehicle production, is creating new demands for advanced industrial fume extraction solutions. The food and beverage industry, being the second-largest in terms of turnover in Europe, also contributes significantly to market growth. Recent investments in modernizing cement plants and other industrial facilities with low-carbon technologies are further driving the demand for sophisticated air quality control systems.

Industrial Air Quality Control Systems Market in United Kingdom

The United Kingdom maintains a significant position in the European industrial air quality control systems market, driven by its comprehensive environmental regulations and industrial diversity. The country's chemical industry, being one of the global leaders, remains active in all key areas including basic inorganics, petrochemicals, polymers, and specialties. Despite Brexit-related challenges, the UK continues to implement stringent air quality standards, particularly through the Air Quality Standards Regulations and the National Emissions Ceiling Regulations. The country's extended operation of coal-based power plants, necessitated by energy security concerns, has sustained the demand for air quality control systems in the power sector. The UK's commitment to reducing emissions, particularly through initiatives like the Best Available Techniques framework launched in 2022, continues to drive innovation and adoption of advanced air quality control technologies across various industrial sectors.

Industrial Air Quality Control Systems Market in Other European Countries

The industrial air quality control systems market across other European countries demonstrates diverse dynamics and opportunities. Countries like Italy, Belgium, and other European nations maintain significant market presence through their industrial activities and environmental commitments. Italy's position as the third-largest chemical industry in Europe and its growing exports of processed food and beverages create substantial demand for air quality control systems. Belgium's chemical industry has shown remarkable growth, with increasing investments in new chemical plants driving market expansion. The market is further shaped by various national and EU-level environmental regulations, technological advancements, and industrial modernization efforts. Countries like Spain, the Netherlands, and the Nordic nations also contribute significantly to the market through their industrial activities and environmental protection initiatives. The collective focus on reducing emissions and improving air quality across these nations continues to drive innovation and adoption of advanced air quality control technologies.

Competitive Landscape

Top Companies in Europe Industrial Air Quality Control Systems Market

The European industrial air quality control systems market is characterized by established players like John Wood Group PLC, Andritz AG, John Cockerill Group, and Fives Group leading the innovation landscape. Companies are focusing on expanding their technological capabilities through strategic acquisitions and partnerships, particularly in areas like electrostatic precipitators, scrubbers, and advanced filtration systems. The market demonstrates a strong emphasis on developing comprehensive end-to-end solutions, from design and engineering to maintenance services. Industry leaders are increasingly investing in research and development to create more efficient and environmentally sustainable industrial air quality control systems, while simultaneously expanding their geographical presence across Europe through strategic facility establishments and service network expansion.

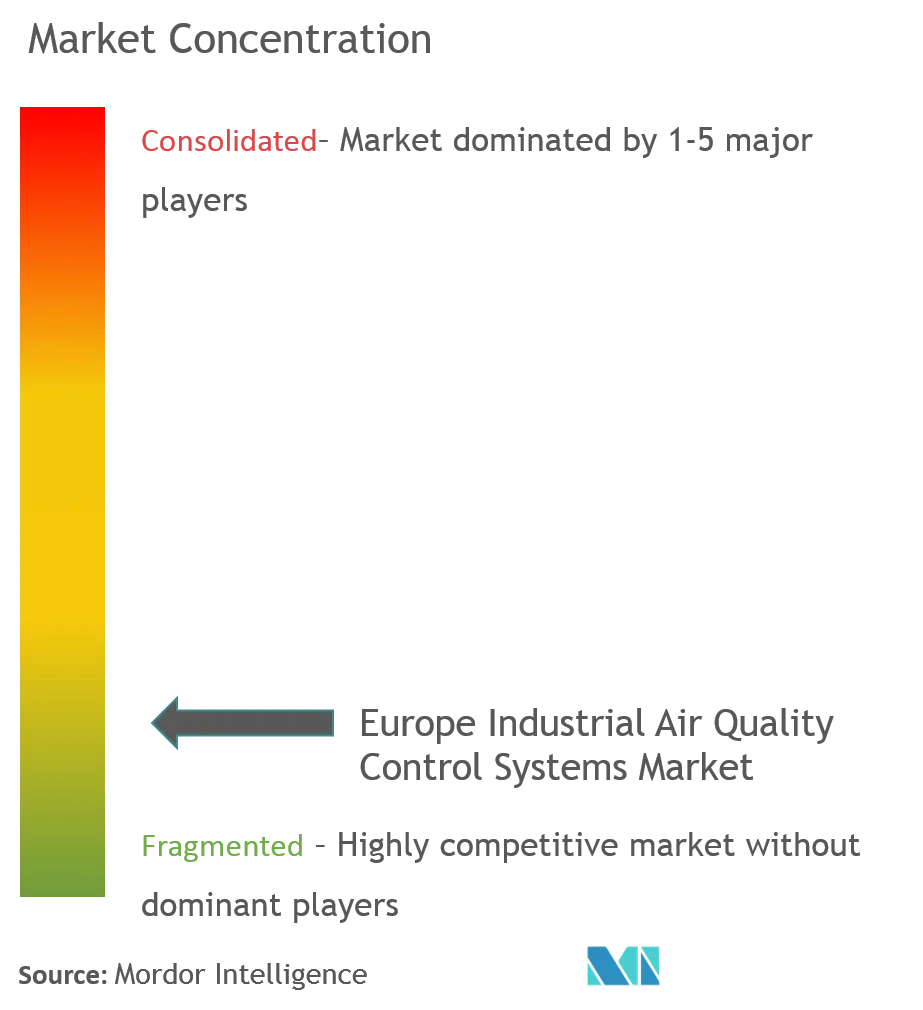

Consolidated Market with Strong M&A Activity

The European industrial air quality control systems market exhibits a moderately consolidated structure dominated by multinational conglomerates with diverse industrial portfolios. These major players leverage their extensive research capabilities, established distribution networks, and strong financial positions to maintain market leadership. The market is characterized by a mix of large-scale integrated solution providers and specialized technology firms, with regional players maintaining strong positions in specific geographic markets or specialized applications.

The industry has witnessed significant merger and acquisition activities, particularly focused on technology acquisition and market expansion. Companies are actively pursuing strategic acquisitions to enhance their product portfolios, gain access to new technologies, and strengthen their presence in key European markets. This consolidation trend is driven by the need to achieve economies of scale, expand service capabilities, and meet increasingly stringent environmental regulations across different industrial sectors.

Innovation and Compliance Drive Market Success

Success in the European industrial air pollution control systems market increasingly depends on companies' ability to offer innovative, energy-efficient solutions while maintaining compliance with evolving environmental regulations. Market leaders are focusing on developing integrated solutions that combine traditional air quality control technologies with advanced digital monitoring and control systems. Companies are also emphasizing the importance of after-sales services, preventive maintenance, and customer support to build long-term relationships with industrial clients.

For new entrants and smaller players, specialization in specific industrial applications or regional markets presents opportunities for growth. The market's high entry barriers, including significant capital requirements and technical expertise, necessitate strategic partnerships or niche market positioning. Companies must also consider the increasing end-user focus on total cost of ownership, energy efficiency, and environmental compliance when developing their market strategies. The ability to provide customized solutions for specific industrial applications while maintaining cost competitiveness will be crucial for long-term success.

Europe Industrial Air Quality Control Systems Industry Leaders

John Wood Group PLC

Andritz AG

John Cockerill Group

Operational Group Limited

Munstermann GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2022: In the European Green Deal, the Commission recommended stricter regulations for sewage treatment from cities, surface and groundwater pollution, and ambient air quality. In ten years, the new regulations will prevent more than 75% of deaths brought on by levels of the major pollutant PM2.5 above WHO recommendations.

- September 2022: Breathe Warsaw announced to employ the city's 165 air sensors, the largest network in Europe, to create an air quality database that will help authorities better identify the sources of pollution. The plan will establish a low-emission zone by 2024 and offer technological help to phase out coal heating.

Europe Industrial Air Quality Control Systems Market Report Scope

Air Quality Control Systems (AQCS) include control systems that reduce the proportion of pollutants from flue gases emitted from exhausts of power plants and other industries majorly fuelled by fossil fuels.

The Europe industrial air quality control systems market is segmented by type, application, emissions (Qualitative Analysis only), and geography. By type, the market is segmented into Electrostatic Precipitators (ESP), Flue Gas Desulfurization (FGD) and Scrubbers, Selective Catalytic Reduction (SCR), Fabric Filters, Others. By application, the market is segmented into Power Generation Industry, Cement Industry, Chemicals and Fertilizers, Iron and Steel Industry, Automotive Industry, Oil & Gas Industry, and Other Applications. By emissions (Qualitative Analysis only), the market is segmented into Nitrogen Oxides (NOx), Sulphur Oxides (SO2), Particulate Matter (PM). The report also covers the market size and forecasts for Europe industrial air quality control systems market across major countries. For each segment, the market sizing and forecasts have been done based on revenue (value in USD).

Type

| Electrostatic Precipitators (ESP) |

| Flue Gas Desulfurization (FGD) and Scrubbers |

| Selective Catalytic Reduction (SCR) |

| Fabric Filters |

| Others |

Application

| Power Generation Industry |

| Cement Industry |

| Chemicals and Fertilizers |

| Iron and Steel Industry |

| Automotive Industry |

| Oil & Gas Industry |

| Other Applications |

Emissions (Qualitative Analysis only)

| Nitrogen Oxides (NOx) |

| Sulphur Oxides (SO2) |

| Particulate Matter (PM) |

Geography

| Germany |

| France |

| United Kingdom |

| Rest of Europe |

| Type | Electrostatic Precipitators (ESP) |

| Flue Gas Desulfurization (FGD) and Scrubbers | |

| Selective Catalytic Reduction (SCR) | |

| Fabric Filters | |

| Others | |

| Application | Power Generation Industry |

| Cement Industry | |

| Chemicals and Fertilizers | |

| Iron and Steel Industry | |

| Automotive Industry | |

| Oil & Gas Industry | |

| Other Applications | |

| Emissions (Qualitative Analysis only) | Nitrogen Oxides (NOx) |

| Sulphur Oxides (SO2) | |

| Particulate Matter (PM) | |

| Geography | Germany |

| France | |

| United Kingdom | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current Europe Industrial Air Quality Control Systems Market size?

The Europe Industrial Air Quality Control Systems Market is projected to register a CAGR of 0.6% during the forecast period (2025-2030)

Who are the key players in Europe Industrial Air Quality Control Systems Market?

John Wood Group PLC, Andritz AG, John Cockerill Group, Operational Group Limited and Munstermann GmbH & Co. KG are the major companies operating in the Europe Industrial Air Quality Control Systems Market.

What years does this Europe Industrial Air Quality Control Systems Market cover?

The report covers the Europe Industrial Air Quality Control Systems Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Industrial Air Quality Control Systems Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: