Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 26.6 Billion |

| Market Size (2026) | USD 31.15 Billion |

| Market Size (2031) | USD 68.45 Billion |

| Growth Rate (2026 - 2031) | 17.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Green Data Center Market Analysis by Mordor Intelligence

The Europe green data center market size was valued at USD 26.6 billion in 2025 and estimated to grow from USD 31.15 billion in 2026 to reach USD 68.45 billion by 2031, at a CAGR of 17.09% during the forecast period (2026-2031). Heightened regulatory ambition under the EU Green Deal, hyperscale investments in next-generation AI infrastructure, and enterprise-wide digitization are reinforcing a sustained demand curve that supports both capacity growth and sustainability innovation. Operators are steering capital toward ultra-efficient power and cooling technologies as the Energy Efficiency Directive requires facilities above 500 kW to report energy metrics and meet renewable-energy thresholds. Nordic incentives for power-purchase agreements (PPAs) ensure low-carbon electricity and enable operators to post power-usage-effectiveness (PUE) ratios close to the physical minimum, while FLAP-D hubs remain attractive for interconnection density despite grid backlogs. Service providers that bundle monitoring, lifecycle management, and compliance reporting are expanding faster than hardware-centric peers, reflecting the shift from one-off builds to continuous optimization. Vendors able to align Scope 3 reporting support with high-density liquid cooling stand to capture the strongest upside.

Key Report Takeaways

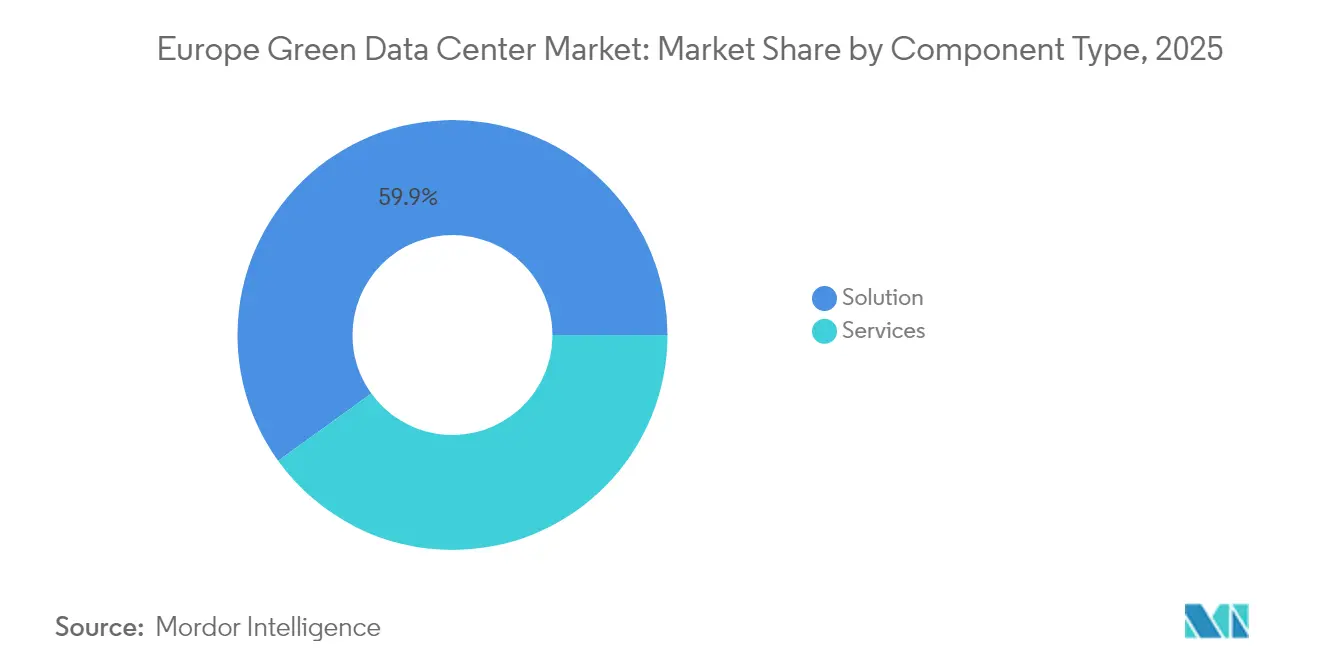

- By component, solutions captured 59.94% revenue share in 2025; services are projected to climb at a 21.66% CAGR to 2031.

- By data center type, hyperscalers/cloud service providers held 34.85% of the Europe green data center market share in 2025 and are advancing at a 23.79% CAGR through 2031.

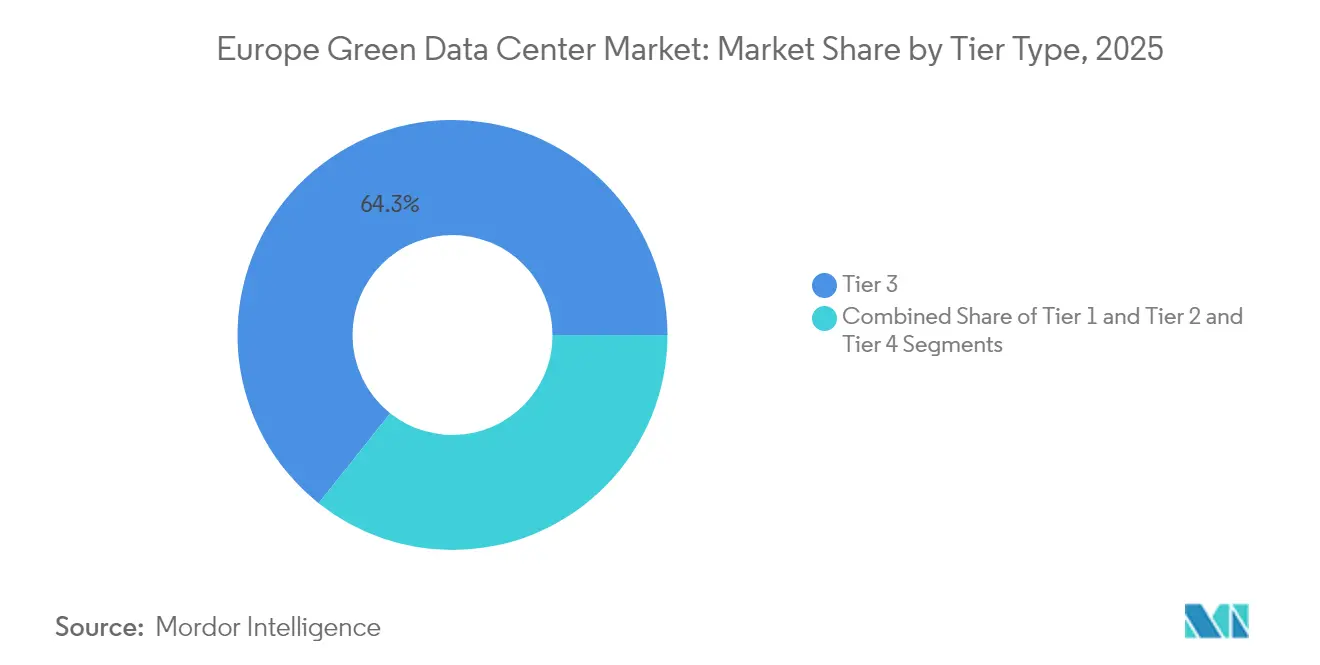

- By tier type, Tier 3 facilities accounted for 64.30% of the Europe green data center market size in 2025, while Tier 4 leads growth at a 23.07% CAGR to 2031.

- By industry vertical, telecom & IT held 27.85% of the Europe green data center market size in 2025; government deployments are growing fastest at 24.25% CAGR.

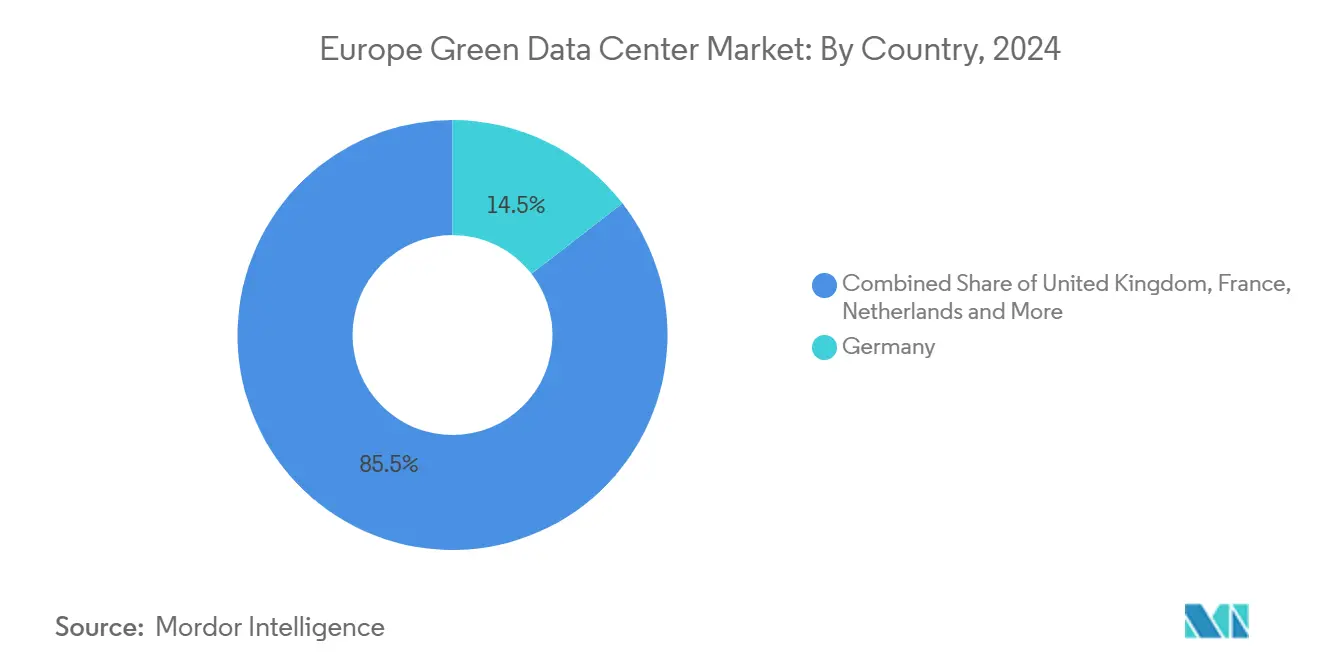

- By country, Germany led with 14.35% market share in 2025; Ireland is the fastest-growing geography at 18.75% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Green Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud and Big-Data Workload Surge | +4.2% | Global, concentrated in FLAP-D markets | Short term (≤ 2 years) |

| EU Green Deal and Fit-for-55 Mandates | +3.8% | EU-wide, strongest in Germany and Nordic countries | Medium term (2-4 years) |

| Hyperscale and Edge Build-outs in FLAP-D Hubs | +3.1% | Frankfurt, London, Amsterdam, Paris, Dublin | Medium term (2-4 years) |

| Nordic PPAs Enabling Ultra-Low PUE | +2.4% | Sweden, Norway, Denmark, Finland | Long term (≥ 4 years) |

| District-Heating Waste-Heat Subsidies | +1.8% | Germany, Denmark, Netherlands | Long term (≥ 4 years) |

| Scope-3-Focused Green SLAs Demand | +1.3% | EU-wide, led by multinational enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud & Big-Data Workload Surge

AI and machine-learning tasks consumed 8% of data-center electricity in Europe during 2024 and may hit 20% by 2028, prompting rapid adoption of liquid cooling that removes heat 15–25 times faster than air.[1]Ericsson, “AI Energy Demand Outlook 2024,” ericsson.com Microsoft earmarked USD 2.5 billion for an AI-focused campus in Leeds hosting more than 20,000 GPUs by 2026, signalling how hyperscalers reshape facility architecture around high-density racks. Smaller inference workloads at the edge are spawning distributed micro-sites tethered to central training clusters, reducing latency while sustaining renewable-energy targets. Enterprise cloud strategies now include quantitative sustainability metrics; 38% of European operators invested in greener facilities in 2024 to balance AI growth with carbon-reduction pledges. Liquid-ready designs and rack-level heat reuse deliver both performance and compliance benefits that reinforce the driver’s position in near-term demand formation.

EU Green Deal & Fit-for-55 Mandates

The Energy Efficiency Directive obliges data centers above 500 kW to publish annual resource metrics and to cut energy consumption by 11.7% by 2030. Germany’s Energy Efficiency Act sets a PUE ceiling of 1.2 for new builds from July 2026 and a 100% renewable-electricity mandate by 2027.[2]Linklaters, “Germany Passes Energy Efficiency Act,” linklaters.com A pan-EU sustainability-rating framework entering force in September 2024 enables operators to benchmark performance and secure procurement preference from corporates bound by the Corporate Sustainability Reporting Directive. Compliance spending is unlocking product innovation: Equinix is piloting waste-heat networks that warm neighboring homes while lowering facility PUE.[3]Computer Weekly, “Equinix Tests District-Heat Export in Frankfurt,” computerweekly.com Operators able to evidence transparent metrics gain a competitive edge in enterprise RFPs, intensifying adoption of automated monitoring and lifecycle-carbon accounting platforms.

Hyperscale & Edge Build-outs in FLAP-D Hubs

Frankfurt, London, Amsterdam, Paris, and Dublin host the densest interconnection fabrics in Europe, attracting disproportionate hyperscale capital. Digital Realty’s USD 8.4 billion integration of Interxion enlarged an already expansive European estate to 112 facilities, consolidating sustainability know-how and cross-market power-procurement leverage. Equinix financed expansion through EUR 1.15 billion in green bonds in 2024, lifting its cumulative sustainable-debt tally to USD 6.9 billion. Although grid queues are lengthening, operators are pivoting toward second-tier cities like Madrid and Milan, while edge nodes inside urban cores provide ultra-low-latency compute. Interconnection density in FLAP-D helps to minimize duplicate capacity, cutting energy per transaction and underscoring the hubs’ structural advantage.

Nordic PPAs Enabling Ultra-Low PUE

Abundant hydro, wind, and low ambient temperatures position the Nordic cluster as Europe’s energy-efficient stronghold. Amazon committed EUR 700 million to Finnish wind projects totaling 472 MW capacity, the country’s largest private renewable investment, to fuel regional data-center demand. Swedish photovoltaic additions doubled to 1,600.9 MW in 2024, offering new contracting choices for operators. Denmark’s corporate-PPA framework could see 36% of industrial electricity supplied via long-term renewable contracts by 2040. Integrated Nordic power markets permit cross-border renewable swaps, enabling Google to run Finnish data halls on Swedish wind power. Resulting PUE scores near 1.1 strengthen the region’s draw for AI workloads and carbon-neutrality programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for Liquid-Cooling and On-site RE | -2.1% | Global, acute in retrofit scenarios | Short term (≤ 2 years) |

| Grid-Connection Delays in Power-Scarce Hubs | -1.8% | UK, Germany, Netherlands | Medium term (2-4 years) |

| Embodied-Carbon Steel and Concrete Scrutiny | -1.2% | EU-wide, strongest in Germany and Nordic countries | Long term (≥ 4 years) |

| Sustainable-DC Engineering Talent Shortage | -0.9% | FLAP-D markets, spreading to secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Liquid-Cooling & On-site RE

Direct-to-chip and immersion systems cost 20–40% more than air cooling despite life-cycle savings, stretching payback timelines for operators lacking low-cost capital. AI racks topping 20 kW magnify the need for these upgrades, yet retrofit works demand floorplate reconfiguration, electrical refits, and staff reskilling. On-site solar or battery installations face six-month permitting windows, complicating schedules and raising holding costs. Larger multinationals mitigate expense through sustainability-linked loans, but smaller colocation players risk margin compression until financing innovation or partnership models neutralize upfront burdens.

Grid-Connection Delays in Power-Scarce Hubs

German applicants face connection dates extending to 2031, while UK projects report 13-year waits in constrained zones. Ireland’s pause on Dublin-area projects until 2028 underscores how supply-chain digitization collides with national carbon budgets. Regulators such as Germany’s BNetzA are exploring “repartition” capacity auctions to replace first-come, first-served rules. In the interim, operators deploy large battery systems and flexible cooling logic to shave peak loads, yet opportunity losses accumulate as demand shifts to less-congested markets. Grid modernisation pace will heavily influence the Europe green data center market’s geographic redistribution over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Lead Infrastructure Modernization

Solutions revenue reached USD 15.94 billion in 2025, equal to 59.94% of overall expenditure, as operators procured efficient power trains, high-density servers, and advanced cooling to satisfy Directive-driven PUE benchmarks. Europe green data center market size for services registered USD 10.66 billion and is on track for a 21.66% CAGR to 2031, reflecting surging demand for carbon accounting, lifecycle monitoring, and regulatory advisory. Dedicated system-integration practices align liquid and air cooling within retrofit footprints, compressing migration time while raising resource efficiency. Continuous monitoring via data-center-infrastructure-management (DCIM) software automates energy reporting, a mandatory prerequisite for transparency audits under the EU Green Deal. As Scope 3 tracking obligations deepen, professional-services portfolios focused on supplier audits and embodied-carbon assessments capture an incremental share, reaffirming a services-led maturity phase that complements hardware refresh cycles.

By Data Center Type: Hyperscalers Drive Sustainability Innovation

Hyperscalers held 34.85% of 2025 revenue and expand at 23.79% CAGR, capitalizing on balance-sheet strength to lock renewable contracts and trial liquid-cooling at scale. The Europe green data center market size attributed to hyperscale campuses is projected to exceed USD 33.3 billion by 2031, with sustainability clauses embedded in power-purchase agreements anchoring long-term competitiveness. Colocation providers differentiate by bundling renewable credits and waste-heat-reuse schemes that appeal to mid-sized enterprises. Enterprise on-premises footprints continue to shrink, yet firms with latency-sensitive workloads maintain hybrid models that lean on edge nodes outfitted with efficient cooling. Edge providers deploy 250 kW–1 MW modules near population centers, ensuring regulatory compliance through recycled-air economizers and modular battery storage. Larger hyperscalers publicize construction-phase carbon cuts, such as AWS adopting low-carbon steel in Sweden to trim embodied emissions by up to 70%, setting a bar smaller competitors strive to match.

By Tier Type: Tier 4 Growth Reflects Mission-Critical Sustainability

Tier 3 dominated 2025 with 64.30% share, yet Tier 4 growth of 23.07% CAGR to 2031 signals demand for concurrent maintainability alongside strict sustainability targets. The Europe green data center market share for Tier 4 is forecast to reach 18.75% by 2031 as healthcare, financial, and public-sector workloads adopt N+N redundancy and liquid cooling that together lower PUE toward 1.15. Operators classify premium suites as “Green Tier” offerings where uptime and carbon neutrality co-exist, using immersion cooling and heat-recovery chillers to reclaim thermal energy for municipal heating loops. Meanwhile, Tier 1 and 2 sites address cost-sensitive or archival workloads but face retrofit pressure as the Energy Efficiency Directive tightens minimum standards, nudging even modest facilities toward more efficient power architectures.

By Industry Vertical: Government Acceleration Drives Public-Sector Transformation

Telecom & IT retained leadership at 27.85% revenue in 2025, supported by carriers’ need for regional interconnection and compliance with net-zero roadmaps. Deutsche Telekom reduced network energy intensity 20% between 2021 and 2024 by migrating workloads into ultra-efficient regional hubs. Government data-center demand climbs 24.25% CAGR as agencies digitalize citizen services and must certify environmental stewardship. Europe green data center industry adoption across public entities often mandates waste-heat reuse and 100% renewable sourcing, pushing suppliers to secure guarantees of origin. Financial-services operators in Frankfurt and Paris incorporate AI fraud-detection engines that depend on low-latency green compute, while healthcare and life-science tenants reference EU patient-data localization rules that favor domestic, certified facilities. Manufacturing firms intertwine facility procurement with broader industrial electrification plans, occasionally piping server waste heat into process loops that trim fossil-fuel boilers.

Geography Analysis

Germany leads the Europe green data center market with 14.35% share, drawing on strong fiber, central location, and a defined legislative roadmap. Operators in Frankfurt executed pilot district-heat schemes that export server warmth to residential grids, easing local fossil demand and trimming facility PUE toward 1.2. Connection backlogs remain a hurdle, but regulator proposals for capacity auctions could release stranded power blocks and stabilize expansion schedules.

Ireland follows an outsized growth path at 18.75% CAGR to 2031. Although wholesale power constraints triggered a moratorium on new Dublin connections, the existing base of 82 sites continues to scale through efficiency upgrades and renewable PPAs. Data centers contributed roughly 21% of Ireland’s 2024 electricity demand, yet long-term PPA frameworks under discussion aim to align additional capacity with incremental offshore wind projects. Scarcity of new permits elevates the value of licensed footprints, pushing operators to maximize rack density and waste-heat capture.

Nordic countries combine near-carbon-free grids with cool ambient temperatures, giving Sweden, Norway, Denmark, and Finland the continent’s lowest average PUE scores. Microsoft’s USD 3.2 billion Swedish AI cluster relies on 100% renewable energy contracts and commits surplus heat to local district networks. Amazon’s 472 MW Finnish wind program and Google’s cross-border renewable swaps highlight the region’s integrated power markets. Denmark’s CPPA framework and Norway’s waste-heat rules encourage projects that both meet uptime needs and extend climate benefits outside facility walls, solidifying Nordic leadership in green compute exports to mainland Europe.

Competitive Landscape

Europe green data center market is fragmented as vendors adopt inorganic growth strategies such as strategic partnerships and mergers and acquisitions to expand the market foothold. Key players are IBM, Cisco Systems, Inc., Dell Technologies Inc., etc.

In September 2022, A new data center of OVHcloud is being constructed in Limburg, Germany. The new building, which was first announced in April 2022, would have more than 6,000 square meters (64,580 sq ft) of floor space available for 40,000 servers, which OVH stated equates to a storage capacity of 100 exabytes. OVH highlighted the green qualities of the new facility. According to the company, the new data center will get 100 percent of its electricity from renewable sources. Also, OVHcloud will be using its patented water cooling technology, waste heat from the servers will be used for underfloor heating in the adjoining offices, and will have an ecological green roof with plants on the facades and trees on the site.

In July 2022, In Hanu, Germany, a sizable data center park is being planned by European logistics real estate company P3 Logistic Parks. At least eight data center modules will be developed on a building area of about 200,000 square meters (2.1 million square feet) over 10 years, with an electrical supply of 180 megawatts (MW) at the site. Construction will be done in phases. The on-spec campus, according to P3, would be developed and run sustainably, and it will be powered entirely by renewable energy.

Europe Green Data Center Industry Leaders

Equinix, Inc.

Digital Realty Trust, Inc.

NTT Global Data Centers EMEA GmbH

OVH Groupe SAS

Interxion Holding N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TikTok invested EUR 1 billion in a Kouvola, Finland site as part of its EUR 12 billion European data-security program, underscoring Nordic momentum

- June 2025: Apto revealed a EUR 3 billion plan for Italy’s largest campus in Lacchiarella, positioning the country as a rising hyperscale option

- May 2025: CyrusOne opened a 54 MW Milan facility powered entirely by renewable energy, expanding Southern Europe’s green footprint

- April 2025: Equinix posted USD 2.225 billion Q1 revenue and unveiled NVIDIA collaborations for AI-ready halls across its European network.

- February 2025: Vantage Data Centers and MEAG pledged EUR 1.4 billion to Vantage’s EMEA platform, marking a top-tier infrastructure commitment.

- January 2025: PIMCO lifted its European data-center fund target to EUR 1 billion, confirming institutional appetite for sustainability-anchored assets

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe green data center market as revenues generated from live data center facilities whose power, cooling, IT, and monitoring systems are deliberately engineered to minimize carbon emissions through high-efficiency equipment, renewable electricity procurement, waste-heat reuse, and PUE targets of 1.5 or lower.

Scope exclusion: capital outlays for land, shells, or purely construction-phase services are outside this revenue pool.

Segmentation Overview

- By Component

- By Service

- System Integration

- Monitoring Services

- Professional Services

- Other Services

- By Solution

- Power

- Cooling

- Servers

- Networking Equipment

- Management Software

- Other Solutions

- By Service

- By Data Center Type

- Colocation Providers

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Industry Vertical

- Healthcare

- Financial Services

- Government

- Telecom and IT

- Manufacturing

- Media and Entertainment

- Other Verticals

- By Country

- Germany

- United Kingdom

- France

- Netherlands

- Ireland

- Norway

- Sweden

- Denmark

- Spain

- Italy

- Russia

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

We interview data-center operators, renewable-energy traders, facility engineers, and equipment vendors across Germany, the Nordics, the United Kingdom, and Southern Europe. These discussions validate effective PUE ranges, average contract power prices, typical service mark-ups, and timing of capacity additions, letting us close gaps left by desk research and refine scenario bounds.

Desk Research

Mordor analysts first harvest quantitative inputs from public tier-one sources such as Eurostat electricity price series, ENTSO-E grid mix data, the European Environment Agency's energy efficiency indicators, and Cloudscene site counts, which reveal installed IT load and renewable penetration. We enrich those with policy texts (EU Green Deal, Fit-for-55, Climate-Neutral Data Centre Pact), patent trends from Questel, and reported PUE bands in Uptime Institute surveys to frame technology baselines.

Company 10-Ks, power purchase agreement disclosures, investor decks, and Factiva news flows then help our team track hyperscale buildouts, rack-density moves, and liquid-cooling pilots. The sources named are illustrative; many additional publications are consulted to cross-check figures and assumptions.

Market-Sizing & Forecasting

Our model begins with a top-down reconstruction of regional green IT load (MW) using published capacity plus renewable share and average service pricing. Results are tested against sampled bottom-up roll-ups of colocation, cloud, and enterprise campus revenues to spot mismatches. Key drivers embedded include new rack installations, average PUE migration, renewable power premium, district-heat offtake incentives, electricity tariff outlook, and hyperscale capex pipelines. Multivariate regression aligns these variables with historical revenue to project through 2030, while scenario analysis gauges upside from accelerated AI workloads. Where operator financials are silent, we apply benchmark ASP × rack counts adjusted by utilization factors derived from primary calls.

Data Validation & Update Cycle

Outputs undergo variance checks versus independent metrics, analyst peer review, and automated anomaly flags. Our report refreshes annually, with interim revisions triggered by material events such as policy shifts or megawatt-scale PPA signings. A final analyst pass ensures clients receive the latest view.

Why Mordor's Europe Green Data Center Baseline Commands Reliability

Published estimates often differ because firms choose dissimilar component mixes, pricing proxies, and refresh schedules.

Key gap drivers here include whether revenues from efficiency-retrofit services are counted, how non-renewable colocation halls are filtered out, currency conversion timing, and the aggressiveness of AI-workload growth assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 26.60 B (2025) | Mordor Intelligence | - |

| USD 21.80 B (2024) | Regional Consultancy A | Excludes monitoring software and applies 2024 FX without rebasing to 2025 |

| USD 16.14 B (2025) | Global Consultancy B | Omits enterprise-run campuses that self-procure renewables and assumes flat rack-density, understating revenue potential |

The comparison shows that by selecting a clear green eligibility filter, incorporating both service and solution streams, and aligning currencies to the model year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can readily trace and reproduce.

Key Questions Answered in the Report

What is the current value of the Europe green data center market?

The market generated USD 31.15 billion in 2026 and is projected to reach USD 68.45 billion by 2031, reflecting a 17.09% CAGR.

Which segment grows fastest in the Europe green data center market?

Services, encompassing sustainability consulting and monitoring, expand at 21.66% CAGR through 2031.

Why are hyperscalers critical to European green data-center growth?

They hold 34.85% market share, deploy liquid cooling at scale, and lock multi-gigawatt renewable PPAs that accelerate sustainable capacity additions.

How do EU regulations impact data-center design?

The Energy Efficiency Directive and national laws such as Germany’s EnEfG impose strict PUE and renewable quotas, pushing operators toward ultra-efficient power and cooling systems.

Which geography offers the best conditions for low-carbon data centers?

Nordic countries combine near-100% renewable grids, cool climates, and supportive PPA frameworks, enabling PUE scores near 1.1 and attracting major hyperscale projects.

What is the chief barrier slowing deployment in FLAP-D hubs?

Prolonged grid-connection backlogs—in some cases extending to 13 years—delay new builds, forcing operators to pursue alternative sites or interim battery solutions.

Page last updated on: