Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 1.32 Billion |

| Market Size (2030) | USD 1.60 Billion |

| Growth Rate (2025 - 2030) | 3.94% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Forage Seed Market Analysis by Mordor Intelligence

The Europe forage seed market size stands at USD 1.32 billion in 2025 and is forecast to reach USD 1.60 billion by 2030, reflecting a 3.94% CAGR over the forecast period. Structural demand created by Common Agricultural Policy (CAP) eco-schemes, rising livestock protein requirements, and accelerating climate-adaptation measures underpin this steady trajectory. Hybrid breeding continues to dominate as farmers seek yield stability that offsets escalating input costs. Cover-crop mandates are enlarging seeding windows, while digital agronomy bundles shorten replacement cycles by pairing genetics with real-time decision tools. Conversely, prolonged GMO and NGT approval timelines, volatile farmgate milk prices, and higher seed-quality testing fees create a drag on short-term spending, nudging growers toward value-oriented choices during market downturns.[1]Source: OECD, “Seed Schemes,” oecd.org

Key Report Takeaways

- By breeding technology, hybrids held 88.2% of the Europe forage seed market share in 2024 and are advancing at a 3.97% CAGR through 2030.

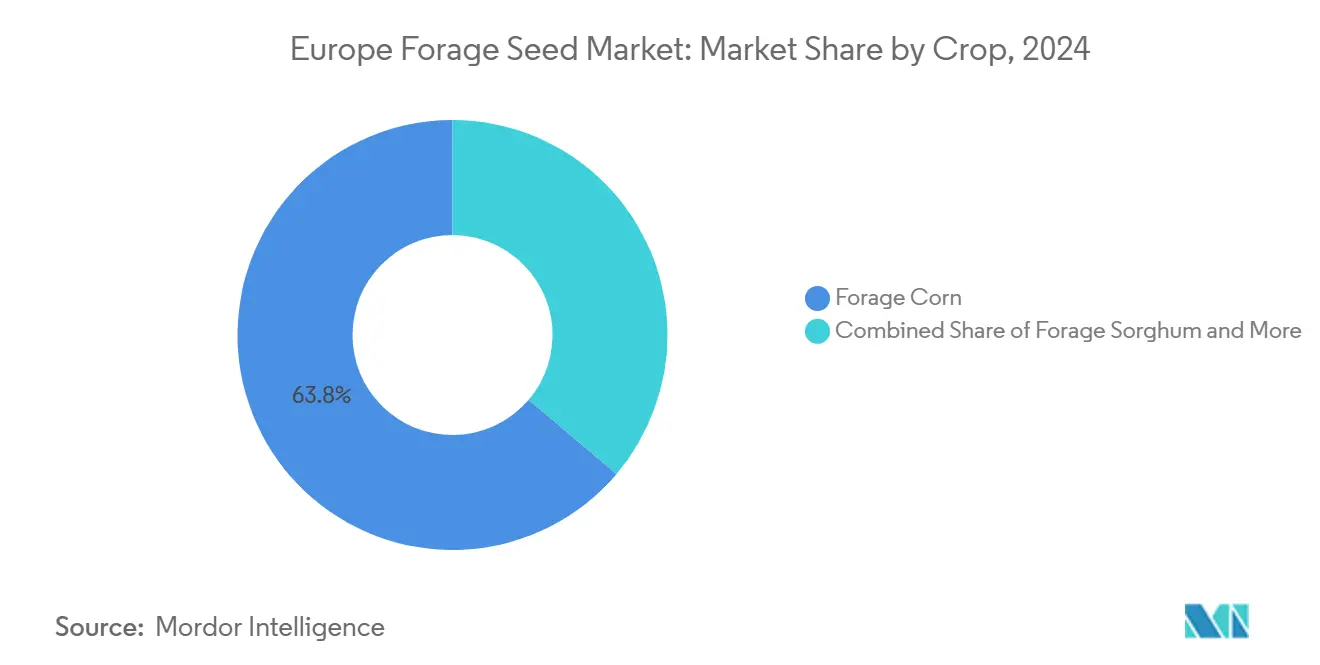

- By crop, forage corn is expected to account for 63.8% of the Europe forage seed market size in 2024, while forage sorghum is projected to grow at a CAGR of 7.07% between 2025 and 2030.

- By country, France led with 29% revenue share in 2024, while the United Kingdom is forecast to grow at a 6.0% CAGR through 2030.

- Royal Barenbrug Group, InVivo, Euralis Semences, Advanta Seeds, and RAGT Group together commanded 30% of the Europe forage seed market size in 2024.

Europe Forage Seed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Union livestock protein demand rebound (post-CAP eco-schemes) | +0.8% | EU-wide, strongest in France, Netherlands, and Denmark | Medium term (2-4 years) |

| Mandatory cover-crop adoption under Common Agricultural Policy (CAP) eco-schemes | +1.2% | EU-wide, particularly Germany, Poland, and Eastern Europe | Long term (≥ 4 years) |

| Surge in drought-tolerant forage hybrids registrations | +0.6% | Mediterranean Europe, expanding to Central Europe | Medium term (2-4 years) |

| Expansion of organic dairy driving non-Genetically Modified Organism(GMO) seed demand | +0.4% | Germany, Netherlands, Austria, and Scandinavia | Long term (≥ 4 years) |

| Digital agronomy bundles boosting seed replacement rates | +0.5% | Western Europe and gradually Eastern Europe | Short term (≤ 2 years) |

| Ukraine war–driven feed-grain deficit shifting acres to forage | +0.7% | Poland, Romania, Baltic States, and Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

European Union livestock protein demand rebound (post-CAP eco-schemes)

Revised Common Agricultural Policy (CAP) eco-schemes channel income support toward protein self-sufficiency, pushing forage seed purchases beyond normal replacement cycles.[2]Source: European Commission, “The Common Agricultural Policy at a Glance,” agriculture.ec.europa.eu Farmers use nitrogen-fixing legumes to satisfy 4% non-productive land rules yet still feed herds, creating a dual benefit that justifies premium seed outlays. France alone unlocked EUR 2.1 billion (USD 2.3 billion) for sustainable practices in 2024, effectively subsidizing seed upgrades. Demand concentrates in high-livestock-density zones where environmental pressure is greatest, sustaining the driver through the medium term. As livestock units align with carbon metrics, protein-rich alfalfa and clover varieties remain central to compliance strategies

Mandatory Cover-Crop Adoption Under Common Agricultural Policy (CAP) Eco-Schemes

Requiring cover crops on at least 3% of European Union arable land translates into roughly 2.4 million new hectares cultivated annually, with Germany adding 400,000 hectares. Farmers leverage regulatory flexibility by choosing forage mixtures that qualify both as cover and feed, letting environmental payments offset seed costs. Larger companies able to amortize EUR 150–200(USD 174-232) per-lot testing fees under International Safe Transit Association (ISTA) and Organisation for Economic Co-operation and Development (OECD) standards gain scale advantages. Over multiple seasons, soil-structure benefits compound, embedding cover rotations permanently and creating long-run seed demand rather than cyclical spikes. The timeline extends beyond 2029 as soil-health incentives deepen.

Surge in Drought-Tolerant Forage Hybrid Registrations

National variety offices processed 47% more drought-tolerant forage applications in 2024 than in 2023, led by perennial ryegrass lines from DLF Seeds and Barenbrug. Three consecutive extreme-weather years shifted breeding targets toward climate resilience. Hybrids, priced 20–30% above open-pollinated seed, offer higher economic returns when stress events strike. Genomic selection accelerates these pipelines, cutting typical release cycles to two seasons. Approval backlogs are easing as authorities prioritize climate traits, indicating a steady flow of new resilient cultivars to market.

Expansion of Organic Dairy Driving Non-Genetically Modified Organism (GMO) Seed Demand

Organic dairy now supplies more than 15% of milk output in Germany, the Netherlands, and Austria, pulling non-Genetically Modified Organism (GMO) seed through the channel. European Union Regulation 2018/848 and private labels such as Naturland enforce strict provenance, prompting seed firms to develop identity-preserved lines. Premiums of 10–15% compensate for additional traceability investments. Digital batch-level certification simplifies audits and builds consumer trust. The trend exhibits a long-term horizon as organic uptake aligns with Farm-to-Fork targets for 25% organic farmland by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Genetically Modified Organism (GMO) or New Genomic Techniques (NGTs) Approval Timelines | -0.8% | EU-wide, especially France, Germany, and Austria | Long term (≥ 4 years) |

| Volatile farmgate milk prices dampening seed budgets | -0.7% | France, Germany, Poland, and UK | Short term (≤ 2 years) |

| Rising seed-quality testing costs (ISTA and OECD) | -0.4% | EU-wide, especially Western Europe | Medium term (2-4 years) |

| Intensifying competition from imported hay and compound feed | -0.6% | Southern Europe, Spain, Italy, and Greece | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict Genetically Modified Organism (GMO) or New Genomic Techniques (NGTs) Approval Timelines

Average European Union approval spans 5–7 years, versus 2–3 years in the Americas, curbing the commercial rollout of advanced traits.[3]Source: European Commission, “GMO Authorisation Process,” agriculture.ec.europa.eu Fragmented national rules create additional uncertainty, diverting R&D toward conventional breeding despite escalating climate threats. Global firms funnel biotech resources to other regions, leaving Europe reliant on slower marker-assisted methods. The delay restrains genetic innovation, narrowing the toolbox available to tackle abiotic stress.

Volatile Farmgate Milk Prices Dampening Seed Budgets

European Union milk prices fell 9% in 2024, squeezing cash flow for dairy farms and lengthening seed replacement cycles. Smaller cooperatives lack reserves to absorb price swings, deferring purchases of higher-priced hybrids. Suppliers offer deferred payment and bundled financing, yet risk aversion persists. Because dairy accounts for significant acreage in France and Germany, price shocks translate quickly into reduced seed orders during down cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Anchor Market Dominance

Hybrids command an 88.2% market share in 2024, reflecting a clear farmer preference for yield stability and stress resilience in the face of climate volatility. The adoption of hybrid forage corn and sorghum varieties is underpinned by their superior performance in both drought and high-input systems, allowing producers to hedge against weather-driven yield risks. Open-pollinated varieties and hybrid derivatives, while still relevant for low-input and organic systems, are increasingly confined to niche applications. Notably, the hybrid segment's forecast CAGR of 3.9% through 2030 signals ongoing investment in breeding programs and technology transfer, with digital agronomy platforms accelerating on-farm adoption.

Hybrid innovation cycles are now synchronized with digital phenotyping and AI-driven selection tools, reducing time-to-market for new varieties and enabling rapid response to emerging agronomic threats. Regulatory compliance with International Safe Transit Association (ISTA) and Organisation for Economic Co-operation and Development (OECD) standards is a prerequisite for market access, and companies with advanced testing infrastructure can move new products through the approval pipeline more efficiently. The interplay between breeding technology and digital agronomy is creating a feedback loop that continuously raises the performance bar for commercial seed offerings, reinforcing the dominance of hybrids in European forage seed systems.

By Crop: Forage Corn and Sorghum Define Growth Poles

Forage corn remains the backbone of the European forage seed market, accounting for 63.8% share in 2024. Its dominance is rooted in high energy density, compatibility with intensive livestock systems, and established agronomic support networks. Forage sorghum is emerging as the fastest-growing crop segment, with a CAGR of 7.07% during the forecast period, driven by its drought tolerance and adaptability to marginal soils. Alfalfa continues to hold the largest share among legume forages, benefiting from Common Agricultural Policy (CAP) eco-scheme incentives and its dual role in protein supply and soil fertility enhancement.

Other forage crops, including ryegrass and clover mixtures, are gaining traction in regions with strong organic and regenerative agriculture movements. The diversification of crop portfolios is both a risk mitigation strategy and a response to evolving regulatory frameworks that incentivize biodiversity and ecosystem services. The emergence of climate-resilient varieties across all crop types is reshaping competitive dynamics, as forage seed companies race to deliver solutions that address both productivity and sustainability imperatives.

Geography Analysis

France, Germany, and the Netherlands together accounted for more than half of Europe's forage seed market demand in 2024, anchored by intensive dairy and mixed-livestock systems. France alone captured 29% of revenue, buoyed by a vertically integrated seed industry and strong Common Agricultural Policy (CAP) support. German growers adopt precision seeding and digital agronomy at scale, enlarging the addressable market for premium hybrids. The Netherlands prioritizes sustainable intensification, pushing demand for traceable, high-value mixtures that meet nutrient-management ceilings.

The United Kingdom is projected to register a 6.0% CAGR through 2030 as post-Brexit policy shifts favor domestic feed security and local breeding investments. Grant structures encourage UK farmers to adopt multi-species leys and forage legumes, reducing reliance on imported soybean meal. Spain and Italy confront water scarcity, steering adoption toward sorghum and drought-resistant ryegrass blends. Regional programs co-fund irrigation upgrades and cultivar trials, smoothing the transition to water-efficient forages.

Eastern Europe shows the fastest acreage expansion as Poland, Romania, and the Baltic States pivot from imported grain to domestic forage after Ukraine supply disruptions. Harmonized European Union seed-quality standards simplify cross-border trade, enabling Western breeders to license germplasm while local multipliers ramp production. Ukraine’s own seed supply uncertainty redirects regional sourcing toward EU-based producers, locking in new customer relationships.

Competitive Landscape

The European forage seed market remains fragmented; the top five companies control only 30% of revenue in 2024. Royal Barenbrug Group leads the market share, followed closely by InVivo, while Euralis Semences, Advanta Seeds, and RAGT Group maintain significant positions. Regional cooperatives and family-owned multipliers thrive by offering locally adapted varieties and direct agronomy support.

Strategic investments focus on climate-resilient germplasm and digital differentiation. KWS opened a new climate-controlled high-bay warehouse in 2025, boosting processing by 70,000 storage spots while lowering energy use. MAS Seeds modernized its Haut-Mauco plant with biosourced treatments to lift industrial performance 25% by 2030. Seed majors bundle software, while startups supply AI disease-forecasting and blockchain traceability, allowing smaller breeders to compete on service rather than scale.

Collaborative Research and Development consortia such as Breeding European Legumes for Increased Sustainability (BELIS) and Innovation, Visions & Technologies (INVITE) pool multi-location data, accelerating stress-trait validation and reducing individual trial costs. Patent filings at the Dutch Raad voor Plantenrassen signal a healthy pipeline, with 2024 registrations featuring new perennial ryegrass and red fescue cultivars. Regulatory mastery rapid ISTA testing and OECD labeling remains a decisive edge, as delays directly translate into missed seasonal windows.

Europe Forage Seed Industry Leaders

InVivo

RAGT Group

Euralis Semences

Advanta Seeds (UPL Ltd.)

Royal Barenbrug Group BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Advancements in European Legume Breeding Enhance Competitiveness in the Seed Market and Support Sustainable Protein Production. The European Legume Breeding Initiative focuses on improving legume varieties such as peas, beans, and clovers to increase sustainable protein production and enhance Europe's seed market position. The project, led by INRAE, includes 22 partners from 10 countries and emphasizes breeding innovation, market adaptation, and climate resilience.

- June 2025: Advanta Seeds acquired corn assets from K-Adriatica, specifically designed for silage and forage corn production systems, to strengthen its operations in Europe, particularly in Italy and Spain. This acquisition improves the availability of high-yielding corn varieties suited to regional livestock feed markets.

- April 2025: RAGT Group has completed the acquisition of Deleplanque Group, thereby enhancing its seed portfolio and expanding its European market reach. This strategic move strengthens RAGT’s capabilities in forage and protein crops through expanded breeding and distribution networks.

Europe Forage Seed Market Report Scope

Hybrids, Open Pollinated Varieties & Hybrid Derivatives are covered as segments by Breeding Technology. Alfalfa, Forage Corn, Forage Sorghum are covered as segments by Crop. France, Germany, Italy, Netherlands, Poland, Romania, Russia, Spain, Turkey, Ukraine, United Kingdom are covered as segments by Country.Breeding Technology

| Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives |

Crop

| Alfalfa |

| Forage Corn |

| Forage Sorghum |

| Other Forage Crops |

Country

| France |

| Germany |

| Italy |

| Netherlands |

| Poland |

| Romania |

| Russia |

| Spain |

| Turkey |

| Ukraine |

| United Kingdom |

| Rest of Europe |

| Breeding Technology | Hybrids |

| Open Pollinated Varieties and Hybrid Derivatives | |

| Crop | Alfalfa |

| Forage Corn | |

| Forage Sorghum | |

| Other Forage Crops | |

| Country | France |

| Germany | |

| Italy | |

| Netherlands | |

| Poland | |

| Romania | |

| Russia | |

| Spain | |

| Turkey | |

| Ukraine | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms