Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

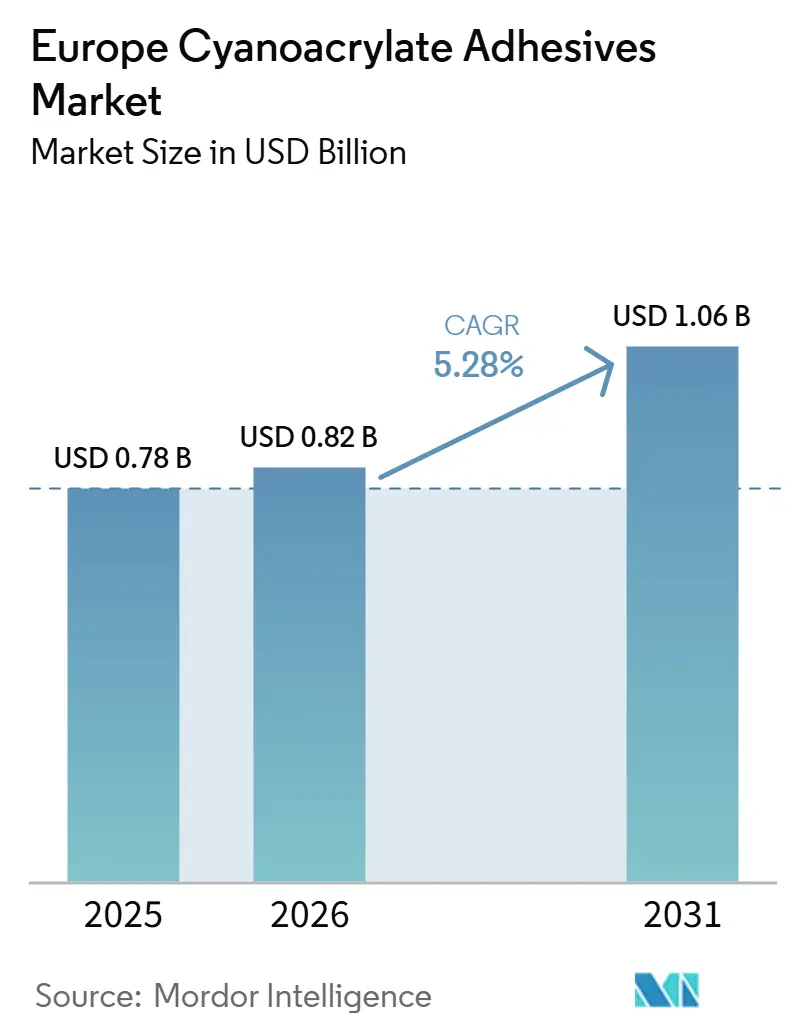

| Base Year Market Size (2025) | USD 0.78 Billion |

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.06 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

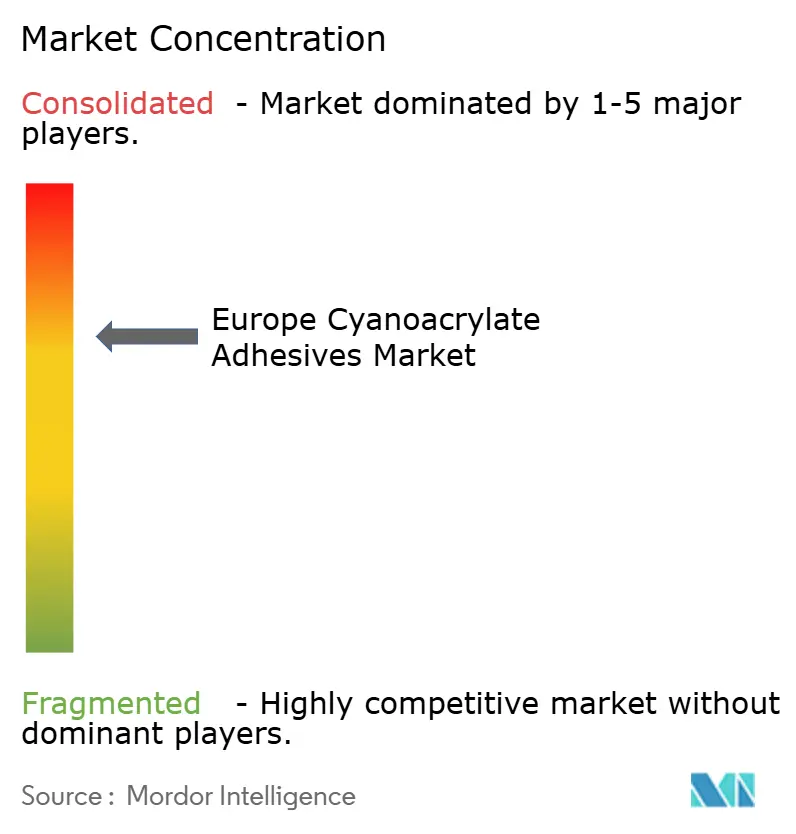

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Cyanoacrylate Adhesives Market Analysis by Mordor Intelligence

The Europe Cyanoacrylate Adhesives Market size is projected to expand from USD 0.78 billion in 2025 to USD 0.82 billion in 2026 and USD 1.06 billion by 2031, registering a CAGR of 5.28% between 2026 and 2031. Demand momentum stems from fast-fixture production on automotive lines, minimally invasive surgery, and culture across Western Europe. Regulatory action on volatile organic compounds (VOCs) is reshaping product portfolios, steering formulators toward low-odor and low-bloom chemistries that command premium prices. Consolidation among global suppliers tightens competitive pressure, while dual-cure and ultraviolet (UV) cure platforms open new windows where cure-on-demand and automated dispensing matter most. Henkel, Sika, Arkema, and H.B. Fuller are using mergers, AI-driven formulation tools, and captive dispensing equipment to embed their brands deeper in end-user production cells.

Key Report Takeaways

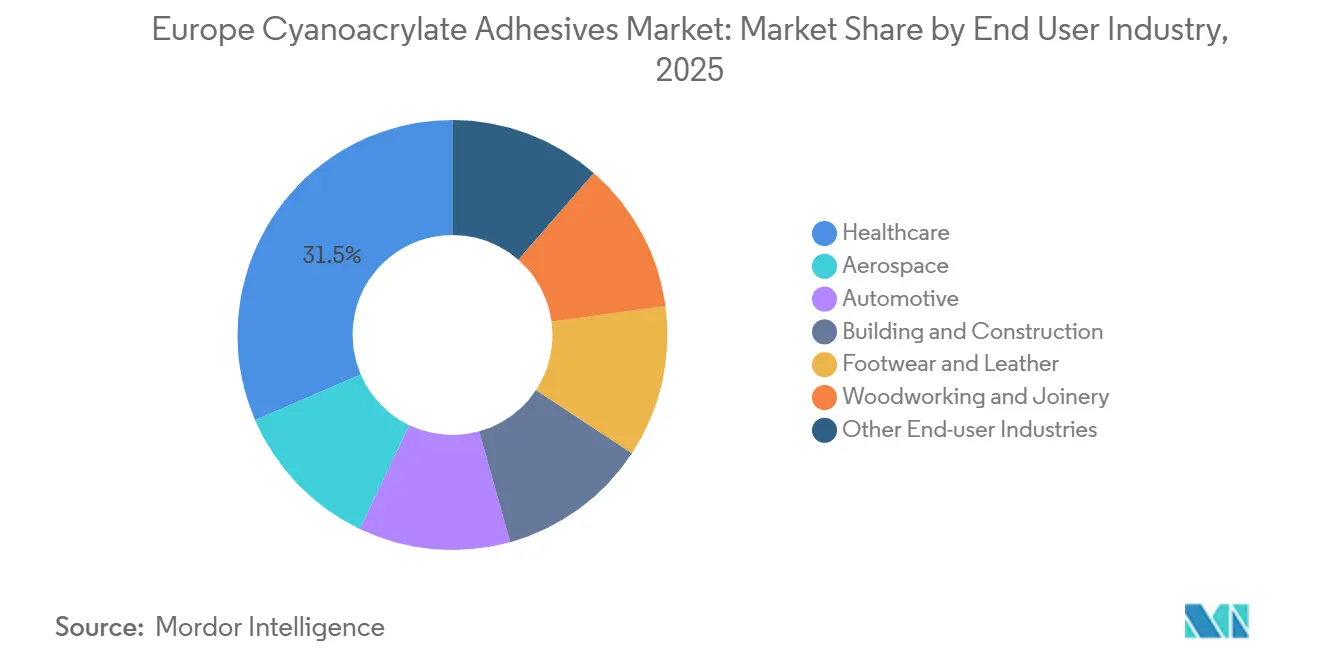

- By end-user industry, healthcare led with 31.48% of the Europe Cyanoacrylate Adhesives Market share in 2025; it is advancing at a 6.04% CAGR through 2026-2031, buoyed by tissue-grade n-butyl-2-cyanoacrylate adoption in laparoscopic procedures.

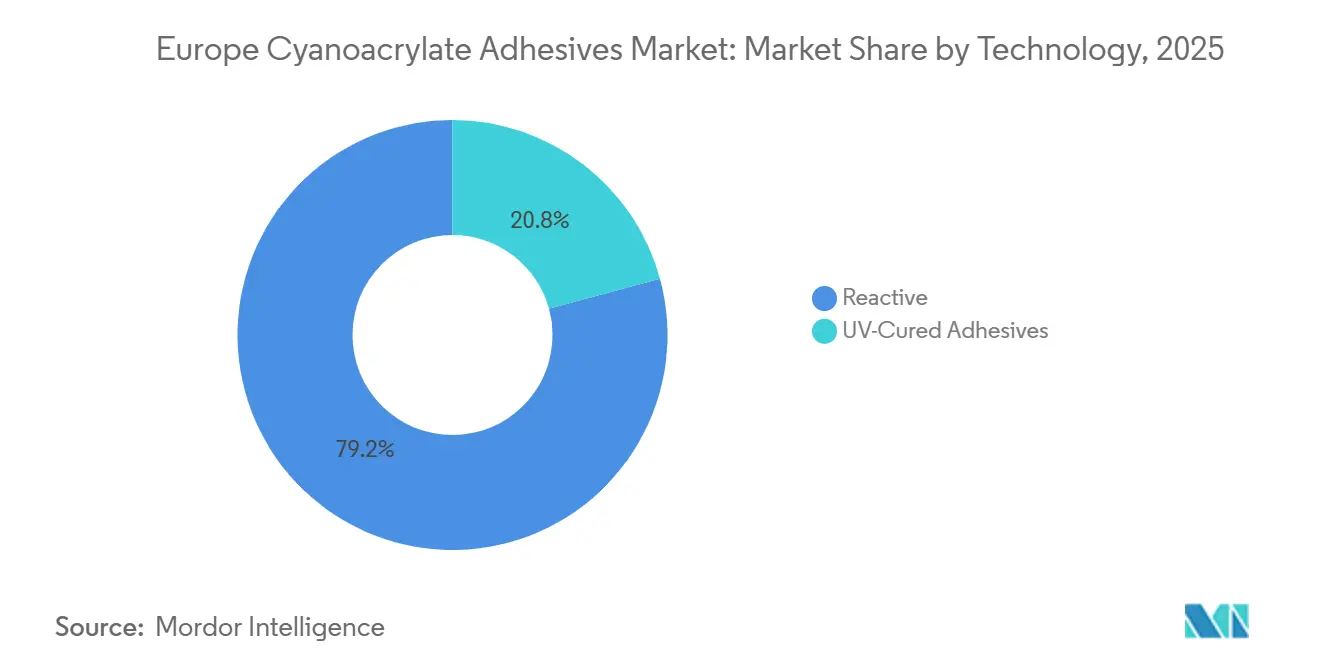

- By technology, reactive led with 79.22% of the Europe Cyanoacrylate Adhesives Market share in 2025; UV-cured grades is forecast to grow at a 6.68% CAGR between 2026 and 2031.

- By geography, Germany commanded 26.13% of the 2025 share and is projected to grow at a 6.34% CAGR between 2026 and 2031, reflecting dense automotive, medical-device, and electronics clusters.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Cyanoacrylate Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating lightweighting initiatives in automotive production | +1.20% | Germany, France, UK, Spain | Medium term (2-4 years) |

| Rapid adoption of tissue-grade cyanoacrylates in minimally invasive surgeries | +1.40% | Germany, France, UK, Italy | Short term (≤ 2 years) |

| Growth of engineered wood and modular furniture manufacturing | +0.90% | Germany, Italy, Spain, Rest of Europe | Long term (≥ 4 years) |

| DIY and home improvement retail boom | +0.70% | UK, Germany, France | Short term (≤ 2 years) |

| Shift to low-odor, low-bloom formulations under stricter volatile organic compound (VOC) rules | +1.10% | EU-wide, strongest in Germany and France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Lightweighting Initiatives in European Automotive Production

European automakers blend aluminum, carbon fiber, and high-strength steel to trim mass without sacrificing crash performance. Adhesive bonding eliminates rivets, raises fatigue life, and permits mixed-material joints. Cyanoacrylates excel in interior trim, sensor housings, and wiring harness strain relief, where sub-30-second fixture times support just-in-time sequencing. Henkel’s early 2026 campaign on its LOCTITE and TEROSON ranges underscores the link between lightweighting, fleet carbon dioxide targets, and rapid production changeovers. The European Union’s circular-design proposals call for reversible bonding; suppliers investing in thermally debondable cyanoacrylates gain first-mover advantage. Electric vehicle battery modules add dielectric and thermal-runaway constraints, nudging formulators toward hybrid or filled grades that dissipate heat while remaining non-structural.

Rapid Adoption of Tissue Grade Cyanoacrylates in Minimally Invasive Surgeries

N-butyl-2- and octyl-2-cyanoacrylate glues now close incisions, fix meshes, and seal varices across laparoscopic specialties. Randomized studies reported 100% mesh fixation success and lower pain scores versus absorbable tacks, while the United Kingdom’s National Institute for Health and Care Excellence (NICE) guidance states clinical equivalence to mechanical fixation with shorter hospital stays[1]National Institute for Health and Care Excellence, “Cyanoacrylate Glue for Hernia Mesh Fixation,” NICE.ORG.UK. The EU Medical Device Regulation classifies these glues as Class III, demanding exhaustive biocompatibility data. Premium pricing reflects sterile single-use applicators and ISO 10993 validation, yet hospitals tolerate higher unit costs thanks to quicker procedure turnover and lower readmission rates.

Growth of Engineered Wood and Modular Furniture Manufacturing

Europe’s particleboard and medium-density fiberboard capacity is pivoting away from formaldehyde-based resins under Horizon Europe’s Sustainable Structural Boards (SUSBOARD) program, which funds bio-based adhesive research targeting 100% fossil-free panels. While structural panel glues move toward lysine-based chemistries, cyanoacrylates retain leadership in miter joint assembly for cabinets and trim, where 10-second fixture times eliminate clamps. Products such as Sika's Everbuild Mitre Fast bond MDF, wood, and plastics under temperature swings from -20°C to 70°C, offering cost-effective speed on crowded factory floors.

Shift to Low-Odor, Low-Bloom Formulations to Meet Stricter VOC Rules

EU-wide VOC ceilings for adhesives, entering into force in 2026, spur audits of legacy solvent systems. Alkoxy-based cyanoacrylates emit fewer irritants and virtually eliminate white blooming, cutting scrap rates in high-gloss consumer goods. Henkel's Born2Bond ULTRA and Performance Adhesives’ Bondloc B403 typify offerings that ship without hazard pictograms, simplify cross-border transport, and earn favorable scores in public-sector tenders. Early adopters enjoy premium price realization, though installers must relearn surface prep and dwell-time techniques.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent occupational safety labeling (H315/H335) | -0.80% | EU-wide, toughest in Germany and Nordic markets | Short term (≤ 2 years) |

| Performance gap vs structural acrylics and epoxies above 120 °C | -1.10% | Germany, France, and Italy are automotive and electronics hubs | Medium term (2-4 years) |

| Feedstock volatility for methyl-2-cyanoacrylate monomer | -0.60% | Global; European pricing linked to Asian acrylonitrile cycles | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Occupational Safety Labeling (H315/H335) Limiting Industrial Throughput

H315/H335 classifications obligate local exhaust, goggles, and polymer-laminate gloves. Manual assembly lines are slow as operators don respirators, raising labor cost per part. Mid-2025 Safety Data Sheet (SDS) updates from 3M and ITW enumerate exposure limits and push customers toward automated dispensing cells that vent fumes and minimize hand contact. Small firms lacking capital may exit, accelerating market consolidation.

Performance Discrepancies Above 120 °C

Standard cyanoacrylates soften near 100°C and lose up to 50% of room-temperature shear strength, whereas novolac epoxies endure 250°C and acrylics such as Permabond TA437 serve at 200°C[2]Permabond, “Epoxy vs Acrylic,” PERMABOND.COM. Electric-vehicle inverters, under-hood sensors, and power electronics therefore default to epoxies or silicones. Suppliers experiment with elastomeric toughening and urethane modifications, yet intrinsic thermoplastic backbones cap heat deflection. The thermal gap curbs penetration into high-stress automotive and renewable energy modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Healthcare Commands Premium Growth

Healthcare’s 31.48% share of 2025 demand reflected operating-room preferences for tissue-grade glues that shorten OR time and reduce postoperative pain. A 6.04% CAGR through 2026-2031 keeps the segment atop the growth league, as European Union Medical Device Regulation (EU-MDR) compliance and ISO 10993 testing become standard procurement prerequisites. Automotive remains a significant segment; however, heat resistance limits applications to interior trim and wire management. Construction, footwear, and woodworking contribute a steady volume in price-sensitive formulations.

A 2026 Journal of Clinical Medicine reviewed across 10 studies spanning six countries found lower infection rates for octyl-2-cyanoacrylate in breast surgery than subcuticular sutures, though wound dehiscence risk rose under high tension. Medical-device firms such as B. Braun, Advanced Medical Solutions, and GEM commercialize single-use applicators that fetch margins above industrial grades. Outside healthcare, aerospace engineers adopt low-outgassing Dymax 9773 for printed circuit board (PCB) staking on satellites and avionics, meeting American Society for Testing and Materials (ASTM) E595 and Military Standard (MIL-STD)-883 benchmarks in seconds, with fast ultraviolet (UV) cure.

By Technology: UV-Cured Variants Outpace Reactive Mainstream

Reactive formulations captured 79.22% of 2025 demand because one-component, moisture-cure simplicity fits broad factory floors. UV-cured grades are forecast to grow at a 6.68% CAGR between 2026 and 2031. Dual-cure products from MXBON and ThreeBond lock exposed surfaces under 365/405 nm LEDs in under 5 seconds, then complete shadow-zone cure via ambient humidity. Electronics assemblers value bloom-free optics and low ionic residue that preserves circuit reliability.

Reactive platforms remain cost winners for metals, rubbers, and porous wood, and low-bloom alkoxy grades reduce white frosting. LED exposure units are now available at a significantly lower cost, reducing the payback period for small and medium enterprises (SMEs). Henkel's AI-driven "virtual adhesives" not only forecast cure kinetics but also reduce the trial-and-error process. This innovation hints at a future where rapid ultraviolet (UV) surface fixation is combined with bulk moisture curing, catering specifically to the needs of medical wearables and optics.

Geography Analysis

Germany anchors the Europe Cyanoacrylate Adhesives Market with 26.13% of 2025 volume, rising at 6.34% CAGR through 2026-2031 as Bavaria’s OEMs, Baden-Württemberg’s medical-device corridor, and Saxony’s electronics fabs expand. Tesa's Offenburg expansion, slated for 2027, adds more than 200 million m² of adhesive-tape capacity, 70% for automotive and electronics. Germany's stringent Technical Rules for Hazardous Substances (TRGS) 401 and REACH enforcement accelerate migration to low-odor formulations.

France and the United Kingdom together absorb a significant share of regional demand. Toulouse aerospace plants and Lyon pharma clusters in France, plus Bristol aircraft assembly and Cambridge med-tech startups in the UK, sustain specialty-grade pull. Post-Brexit, the UK still mirrors EU-REACH, avoiding supply chain splintering. Italy’s Lombardy and Veneto host furniture and footwear hubs that prefer high-viscosity gels for porous leather and MDF, while Spain’s Catalonia vehicle suppliers and Basque composites shops grow mid-single digits.

Rest-of-Europe markets, Poland, the Czech Republic, Romania, and the Baltics, benefit as supply chains shift eastward to manage labor costs. Russia’s participation remains impaired by trade curbs, diverting volume to Central Europe.

Competitive Landscape

The Europe Cyanoacrylate Adhesives Market is moderately consolidated. Mid-tier specialists like Permabond, Dymax, DELO, and ThreeBond have carved out premium niches in the market. They focus on areas such as low-outgassing for aerospace, ultraviolet (UV) dual-cure solutions for electronics, and heat-resistant options for industrial repairs. In May 2025, Dymax introduced a TPO-free UV line, preemptively addressing the EU's upcoming photoinitiator restrictions and ensuring compliance with cytotoxicity standards. Additionally, regional players, including Spain's Afinitica and the UK's Xtraloc, export a significant portion of their output, capitalizing on swift custom formulations and private-label filling services.

Europe Cyanoacrylate Adhesives Industry Leaders

3M

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Henkel AG announced acquiring Stahl Group for USD 2.3 billion, boosting innovation, competition, and specialty adhesives development, driving Europe's cyanoacrylate adhesives market growth.

- February 2026: Sika AG announced plans to acquire Akkim Kimya, strengthening its production and supply capabilities, driving growth, and intensifying competition in Europe's cyanoacrylate adhesives market.

Europe Cyanoacrylate Adhesives Market Report Scope

Cyanoacrylate adhesives, commonly known as super glues, are fast-acting bonding agents that cure rapidly in the presence of moisture. They form strong, rigid joints by polymerizing into a solid plastic upon contact with surfaces. These adhesives bond a wide range of materials such as plastics, metals, ceramics, and rubber. Their quick setting time and high strength make them ideal for household, industrial, and medical applications.

The Europe Cyanoacrylate Adhesives Market is segmented by end-user industry, technology, and country. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, woodworking and joinery, and other end-user industries. By technology, the market is segmented into reactive and UV cured adhesives. The report also covers the market size and forecasts for the Europe Cyanoacrylate Adhesives Market in 6 countries across Europe. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Woodworking and Joinery |

| Other End-user Industries |

By Technology

| Reactive |

| UV-Cured Adhesives |

By Geography

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| By Technology | Reactive |

| UV-Cured Adhesives | |

| By Geography | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the cyanoacrylate adhesives market.

- Product - All cyanoacrylate adhesive products are considered in the market studied

- Resin - Under the scope of the study, cyanoacrylates based on Alkoxy Ethyl, Ethyl Ester, Methyl Ester, and Others are considered

- Technology - For the purpose of this study, Reactive and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms