Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

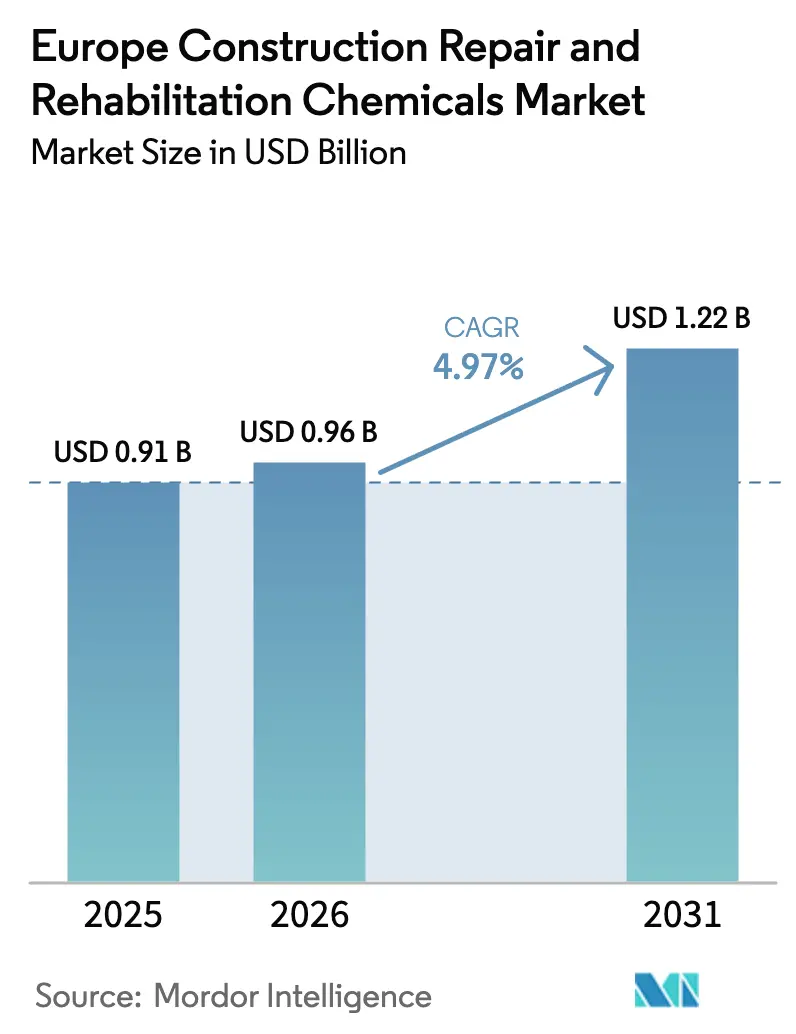

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.22 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Construction Repair And Rehabilitation Chemicals Market Analysis by Mordor Intelligence

The European Construction Repair and Rehabilitation Chemicals market size is expected to grow from USD 0.91 billion in 2025 to USD 0.96 billion in 2026 and is forecast to reach USD 1.22 billion by 2031 at 4.97% CAGR over 2026-2031. Robust public-sector funding, stringent efficiency codes, and widespread infrastructure modernization underpin this trajectory, while manufacturers simultaneously reengineer their product portfolios to meet low-carbon and long-life performance criteria. Parallel policy convergence—chiefly the NextGenerationEU facility—continues to accelerate renovation projects and channel capital toward climate-resilient asset renewal[1]European Commission, “NextGenerationEU Recovery Plan,” EUROPA.EU . Rising feedstock volatility and labor shortages temper short-term momentum, yet sustained adoption of self-healing mortars, polymer-modified grouts, and flame-retardant formulations keeps the European Construction Repair and Rehabilitation Chemicals market firmly on its midterm growth path. Competitive intensity is set to rise as scale players and agile specialists allocate their research and development resources to value-added, EN 13501-1-compliant systems that promise measurable life-cycle savings for asset owners.

Key Report Takeaways

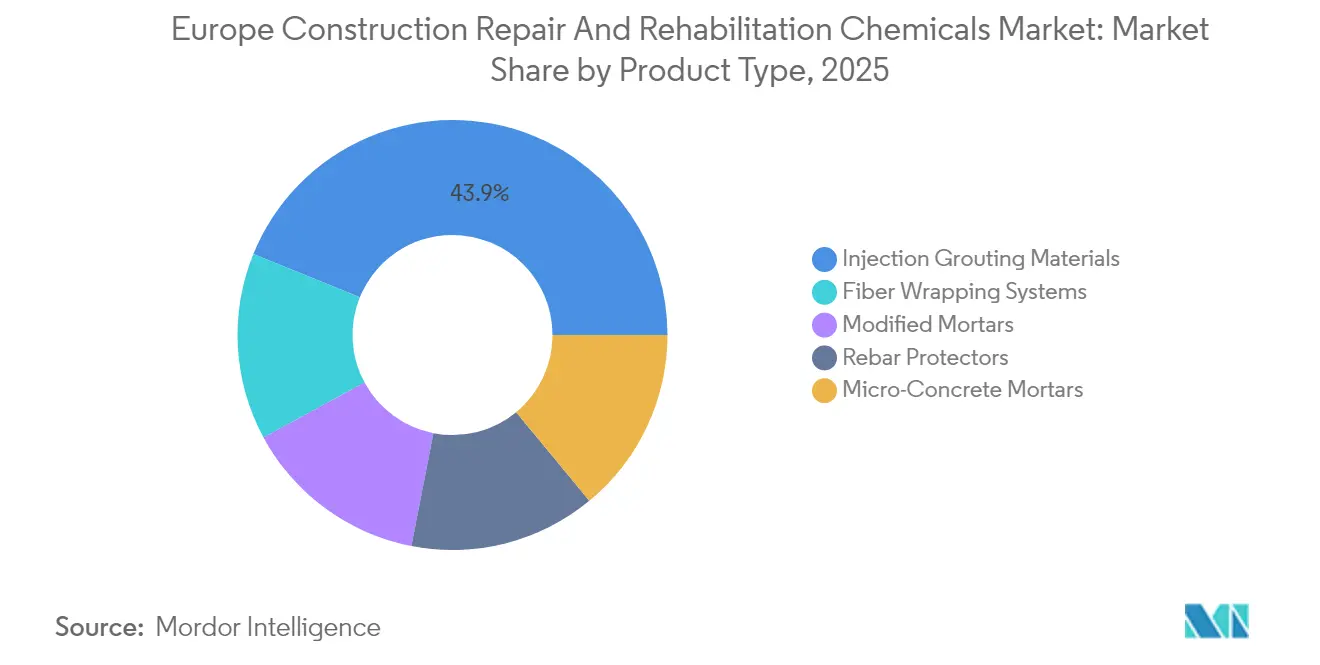

- By product type, injection grouting materials led with a 43.85% share of the European Construction Repair and Rehabilitation Chemicals market in 2025. Additionally, injection grouting materials are projected to grow at the fastest CAGR of 5.43% during the forecast period.

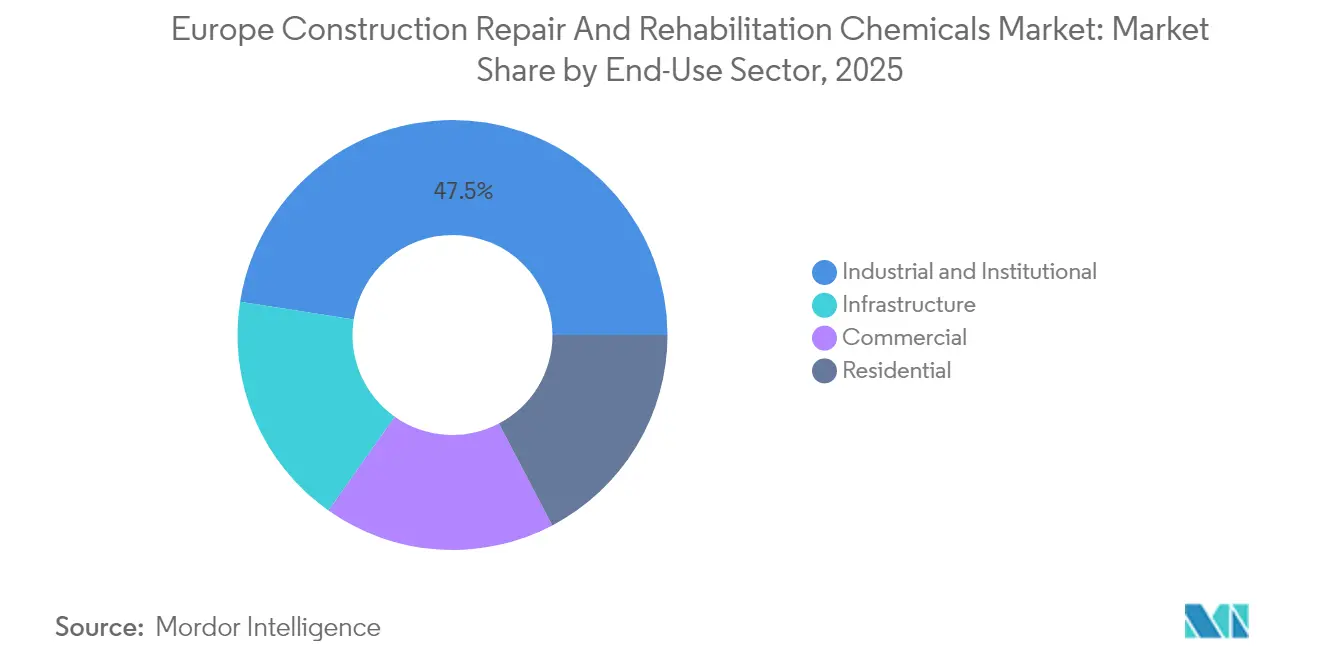

- By end-use sector, the industrial and institutional segment accounted for 47.52% of the European Construction Repair and Rehabilitation Chemicals market size in 2025. However, infrastructure is expected to record the highest projected CAGR at 5.78% through 2031.

- By geography, Germany held 14.41% revenue share in 2025, while Italy is expected to register the fastest growth at a 5.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Construction Repair And Rehabilitation Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated renovation demand under EU Green Deal and “Renovation Wave” | +1.8% | Core EU markets, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Ageing transport and building stock requiring life-extension solutions | +1.2% | Western Europe | Long term (≥ 4 years) |

| Tightening energy-efficiency codes | +1.0% | EU core, early adoption in Nordics | Medium term (2-4 years) |

| Infrastructure resilience funds | +0.9% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Uptake of self-healing micro-capsulated mortars | +0.4% | Germany, UK, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Renovation Demand under EU Green Deal and “Renovation Wave”

The EU Renovation Wave guidelines require member states to significantly increase their annual renovation rates by 2030. This push has led to a surge in deep retrofit projects, necessitating advanced sealing and strengthening chemistries. Through the Recovery and Resilience Facility, substantial funding is allocated to subsidize upgrades, achieving a significant reduction in building energy use. Germany and France dominate this demand, evidenced by a notable rise in subsidy applications in 2024. In response, suppliers are ramping up production of low-viscosity, high-bond grouts and airtightness mortars. With carbon pricing tightening the cost disparity between new builds and existing ones, the momentum for Europe's Construction, Repair, and Rehabilitation Chemicals market strengthens. As renovation mandates grow, contractors enhance their technical skills, and product preferences shift towards premium, certification-ready systems, a positive feedback loop emerges.

Ageing Transport and Building Stock Requiring Life-Extension Solutions

More than three-quarters of Europe’s residential units are energy-inefficient, while bridges and tunnels average over five decades in service life[2]European Investment Bank, “Infrastructure Investment Report 2025,” EIB.ORG. Asset owners now prioritize rehabilitation strategies that add 25–30 years of performance, catalyzing uptake of polymer-modified mortars and corrosion-inhibiting admixtures. Western European rail and highway operators report cost savings over replacement by deploying fiber-reinforced polymer wraps and micro-fine cement grouts. Life-cycle costing frameworks embedded in public procurement amplify this demand, reinforcing market expansion even amid raw-material inflation. Innovation centers on hybrid mortar systems that deliver both structural recovery and energy performance gains, making them particularly attractive for industrial facilities where downtime incurs high revenue penalties.

Tightening Energy-Efficiency Codes

The revised Energy Performance of Buildings Directive 2024 imposes EPC class E thresholds by 2030 and class D by 2033, prompting owners of older stock to undertake envelope upgrades at an increasingly rapid pace. High-performance injection grouts and thermal bridge repair systems become essential, especially in masonry structures common across historic urban centers. Nordic member states lead early adoption; Sweden documented a spike in orders for advanced repair mortars during 2024 retrofit cycles. Fiscal incentives, including accelerated depreciation for deep renovations, offset premium product pricing, sustaining demand for EN 1504-certified chemistries that merge structural repair with airtightness enhancement.

Infrastructure Resilience Funds Unlocking Rehab Budgets

By 2030, the Connecting Europe Facility and Cohesion Fund will focus on climate-resilient upgrades to road, rail, and water assets. Italy stands out, driving demand for specialized products such as corrosion-protected mortars and hydrophobic coatings, which are especially suited to its Mediterranean climate. Contracts based on performance typically emphasize durability of 20–25 years, leading to a heightened demand for premium products, such as self-healing additives and low-permeability grouts. While Southern and Eastern Europe have historically lagged in asset maintenance investments, they are now emerging as pivotal growth centers in the European Construction Repair and Rehabilitation Chemicals market. Suppliers that leverage concrete life-cycle models and offer compliance assistance are carving out a competitive edge in the procurement process.

Restraints Impact Analysis*

| Restraints | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile epoxy and PU feedstock prices | -0.8% | Manufacturing-intensive regions | Short term (≤ 2 years) |

| Skilled labor shortages | -0.6% | Western Europe, spreading eastward | Medium term (2-4 years) |

| Tunnel-fire regulations limiting certain polymer grouts | -0.3% | Germany, France, Italy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Epoxy and PU Feedstock Prices

Epoxy resin prices surged in 2024 amid global petrochemical supply chain disruptions, while polyurethane precursors also increased, compressing contractor margins and prompting quarterly price adjustment clauses. The reliance on Asian intermediates magnifies exposure, and downstream project budgets now incorporate contingency premiums. Producers respond by pursuing backward integration and piloting bio-based epoxies, though commercialization remains three years away. In the meantime, value engineering intensifies, encouraging substitution toward cementitious or hybrid systems where technical performance allows. Persistent volatility restrains short-term spending, shaving 0.8 percentage points off the projected CAGR for the Europe Construction Repair and Rehabilitation Chemicals market.

Skilled Labor Shortages

In 2024, the EU faces a significant shortfall of construction workers, with Germany being one of the most affected. This deficit is causing delays in specialized repair projects. Techniques like injection-grouting and fiber-wrapping demand certified operatives, a talent pool that won't easily arise from traditional labor sources without significant reskilling. Compounding the issue is an aging workforce; the average age of a certified technician is relatively high. Despite contractors raising wages and implementing on-site training, project timelines continue to stretch, impacting suppliers' immediate revenue. While robotics and ready-mix cartridges offer some relief, their adoption remains limited compared to the broader market demands.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Injection Grouting Materials Reinforce Market Dominance

Injection grouting materials command the largest share of the European Construction Repair and Rehabilitation Chemicals market, with a 43.85% revenue share. Their superior crack-penetration capability underpins explosive uptake in heritage retrofits and energy upgrades, where structural interphases must seal without disassembling façade elements. The segment’s 5.43% CAGR to 2031 outpaces all peers as suppliers integrate micro-fine cement technology and self-leveling polyurethane hybrids that tackle both load-bearing and thermal-bridge functions. Specification frameworks under EN 1504 increasingly prioritize grouting solutions that can demonstrate bond strength above 25 MPa and permeability below 10^-16 m/s, standards that next-generation products already exceed.

Alternative product classes trail yet carve defensible niches. Fiber-wrapping systems are gaining momentum in seismic retrofits across Italy and Greece, utilizing carbon fabrics to increase flexural capacity. Micro-concrete mortars meet the precision-repair demands of industrial slabs exposed to chemical spills, whereas modified mortars address harsh agro-industrial settings. Rebar protectors are likely to increase in demand as coastal infrastructure owners intensify their efforts to prevent corrosion. Collectively, product innovation fuels a resilient pipeline that underpins the European Construction Repair and Rehabilitation Chemicals market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-Use Sector: Infrastructure Ascends as Fastest-Growth Vertical

The industrial and institutional sector continued to dominate the European Construction Repair and Rehabilitation Chemicals market share, accounting for 47.52% in 2025, supported by proactive plant maintenance cultures and safety-critical operating regimes. Petrochemical complexes, food plants, and data centers prefer premium repair chemistries to trim shutdowns; micro-fine cement grouts capable of one-hour compressive strength gain resonate strongly. Nonetheless, infrastructure emerges as the momentum leader, notching a 5.78% CAGR to 2031, driven by EU resilience funds. Asset managers shift from reactive patching to predictive maintenance, demanding sensor-embedded mortars and corrosion-monitoring coatings to lengthen inspection intervals.

Commercial real estate gains tailwinds from EPC-driven façade upgrades, while residential renovation momentum spreads beyond early-adopter Germany and France into Spain and Poland via incentive schemes such as MaPrimeRénov and KfW 261 loans. Cross-sector convergence around sustainability and durability narrows the performance gap, encouraging supply chains to harmonize formulation platforms across diverse end-use applications. This convergence secures mid-term volume expansion for the European Construction, Repair, and Rehabilitation Chemicals market, despite cyclical swings in construction.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Germany, leveraging an annual renovation ecosystem bolstered by federal KfW grants and Länder tax rebates, commands a 14.41% share of the 2025 revenue. With an eye on energy-neutrality targets, Germany is witnessing a surge in retrofitting manufacturing plants and housing stock. This push has intensified the demand for injection grouts that meet the Passivhaus standard. While market developers enjoy the advantages of a dense network of certified applicators, a looming wave of retirements poses a challenge. Without swift vocational programs to replenish the skilled workforce, growth may be stunted.

Italy is experiencing rapid growth, boasting the title of the fastest-growing nation, with a strong projected growth rate of 5.65% from 2026 to 2031. The National Recovery and Resilience Plan has earmarked substantial funding for transport infrastructure enhancements. Simultaneously, the Superbonus 110% tax incentive is driving private housing retrofits, especially where seismic and energy efficiency standards converge. Suppliers of dual-function mortars, which offer both shear-wall reinforcement and insulation, are witnessing heightened interest from early adopters. Notably, regional disparities emerge: northern industrial hubs prioritize minimizing production line stops, while southern regions emphasize bolstering resilience against seismic and flooding challenges.

France, Spain, and the UK each tap into lucrative opportunities. France’s MaPrimeRénov initiative targets significant housing upgrades annually. Spain is channeling EU funds to revamp its national highways. Meanwhile, the UK, in response to the Grenfell inquiry, is directing investments through its National Infrastructure Strategy, with a spotlight on fire-safe composite materials. Eastern European nations, categorized under the Rest of Europe, are adeptly converting EU structural funds into tangible projects. However, the pace of adopting high specifications is tempered by the region's still-maturing procurement frameworks. These geographically tailored policy initiatives collectively bolster a diversified demand landscape, shielding the European Construction Repair and Rehabilitation Chemicals market from the vulnerabilities of single-country dependencies.

Competitive Landscape

The European Construction Repair and Rehabilitation Chemicals Market is moderately fragmented. MAPEI, Sika, and Holcim leverage their extensive continental manufacturing footprints and research and development budgets to continuously develop sustainable formulations, such as carbon-negative mortars and micro-capsulated crack sealants. Saint-Gobain Weber and MC-Bauchemie differentiate via bio-based binders and digital dosage apps that shorten onsite cycle times. Regulatory pull from EN 1504 and EU taxonomy reporting accentuates the competitive premium on traceable, low-carbon, and high-durability products, reshaping strategic roadmaps across the European Construction Repair and Rehabilitation Chemicals market.

Europe Construction Repair And Rehabilitation Chemicals Industry Leaders

MAPEI S.p.A.

Saint-Gobain

Sika AG

RPM International Inc.

HOLCIM

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Responding to customer demand for convenience and reduced waste on smaller jobs, Setcrete Ltd. launched a new half-size, 2.5kg sack of its popular Rapid Set Repair Mortar in the United Kingdom.

- January 2025: Imerys launched Fondag Aerospace, a concrete engineered to withstand the punishing conditions of rocket launches in Europe and the rest of the world. Fondag Aerospace has been established to meet the demanding requirements of the aerospace industry.

Europe Construction Repair And Rehabilitation Chemicals Market Report Scope

Specialized chemical compounds, known as construction, repair, and rehabilitation chemicals, restore and enhance existing structures. These chemicals address damages such as cracks and spalls, bolster load-bearing capacities, and shield against environmental factors, all aimed at prolonging a structure's lifespan.

The European construction repair and rehabilitation chemicals market is segmented by product type, end-use sector, and geography. By product type, the market is segmented into fiber wrapping systems, injection grouting materials, micro-concrete mortars, modified mortars, and rebar protectors. By end-use sector, the market is segmented into commercial, industrial and institutional, infrastructure, and residential. The report also covers the market size and forecasts for the construction, repair, and rehabilitation chemicals market in 6 countries across the European region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Product type

| Fiber Wrapping Systems |

| Injection Grouting Materials |

| Micro-Concrete Mortars |

| Modified Mortars |

| Rebar Protectors |

By End-Use Sector

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

By Country

| France |

| Germany |

| Italy |

| Russia |

| Spain |

| United Kingdom |

| Rest of Europe |

| By Product type | Fiber Wrapping Systems |

| Injection Grouting Materials | |

| Micro-Concrete Mortars | |

| Modified Mortars | |

| Rebar Protectors | |

| By End-Use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential | |

| By Country | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe construction repair and rehabilitation chemicals market?

The Europe construction repair and rehabilitation chemicals market size is expected to reach USD 0.96 billion by 2026.

What value does the Europe construction repair and rehabilitation chemicals market reach by 2031?

Forecasts indicate USD 1.22 billion by 2031, reflecting a 4.97% CAGR.

Which product category leads demand in Europe for construction repair chemicals?

Injection grouting materials held 43.85% share in 2025 due to versatility in structural and energy-efficiency retrofits.

Why is Italy the fastest-growing national market?

Italy benefits from EUR 15.6 billion in resilience funding and generous tax incentives that support seismic and energy upgrades.

What main challenge could slow near-term growth?

Volatile epoxy and polyurethane feedstock prices inflate project budgets and may defer some rehabilitation schedules.