Europe Biodegradable Cups Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

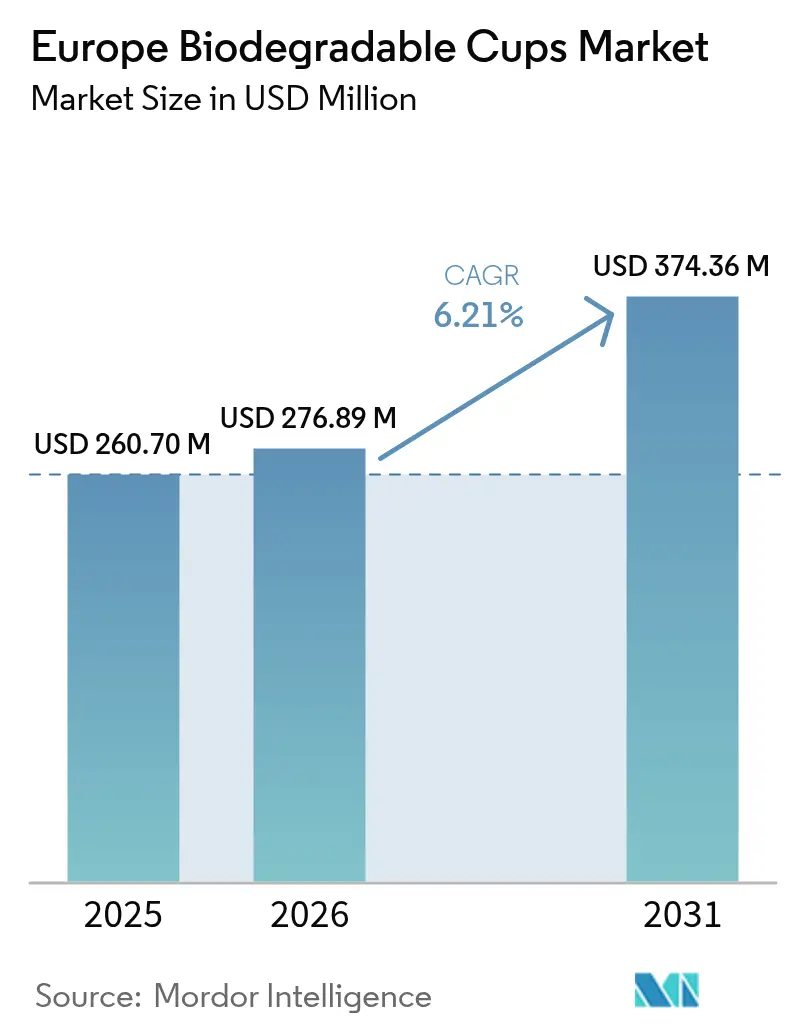

| Base Year Market Size (2025) | USD 260.7 Million |

| Market Size (2026) | USD 276.89 Million |

| Market Size (2031) | USD 374.36 Million |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

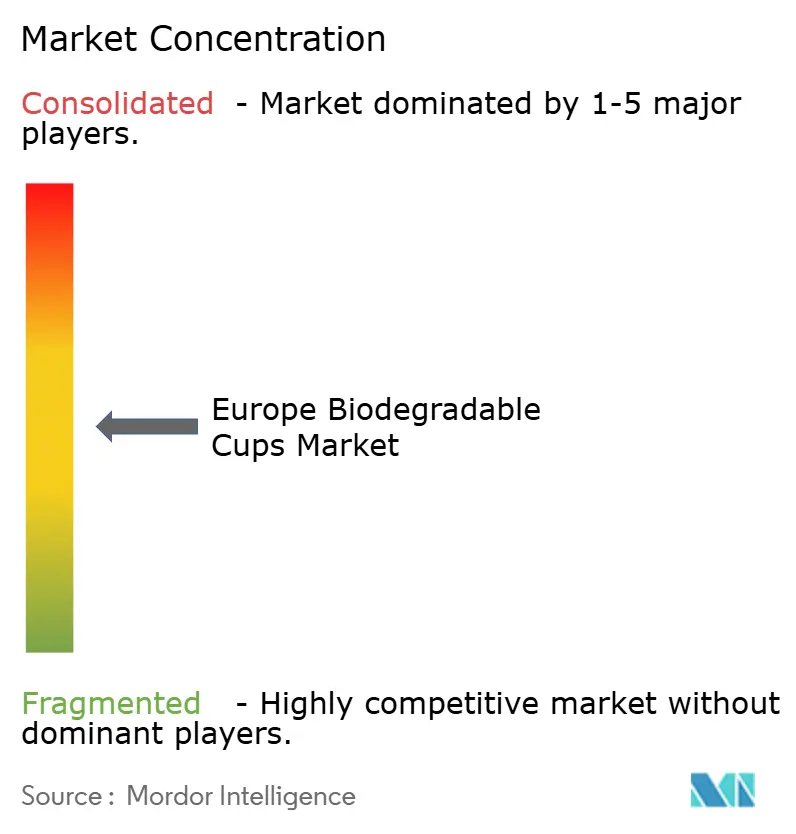

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Biodegradable Cups Market Analysis by Mordor Intelligence

The Europe biodegradable cups market size is expected to grow from USD 260.7 million in 2025 to USD 276.89 million in 2026 and is forecast to reach USD 374.36 million by 2031 at 6.21% CAGR over 2026-2031. Growth is driven by sweeping single-use plastic bans, falling polylactic acid (PLA) resin prices, and brand-level procurement mandates, while headwinds arise from deposit-return schemes and inadequate composting infrastructure. Paper-based cups held a 38.56% share of the Europe biodegradable cups market in 2024, but bio-plastics are expanding faster as the PLA oversupply narrows their cost premium. Beverages remain the anchor application; yet, institutional buyers, such as malls, offices, and universities, now outpace cafés because public tenders increasingly specify certified compostable packaging. Spain delivers the fastest country growth as regional bans bite, whereas Germany’s Mehrwegpflicht law caps single-use demand despite its advanced composting network. Competitive rivalry stays high: integrated fiber leaders defend volumes, pure-play specialists monetize certification niches, and e-commerce distributors scale online access to sustainable SKUs.

Key Report Takeaways

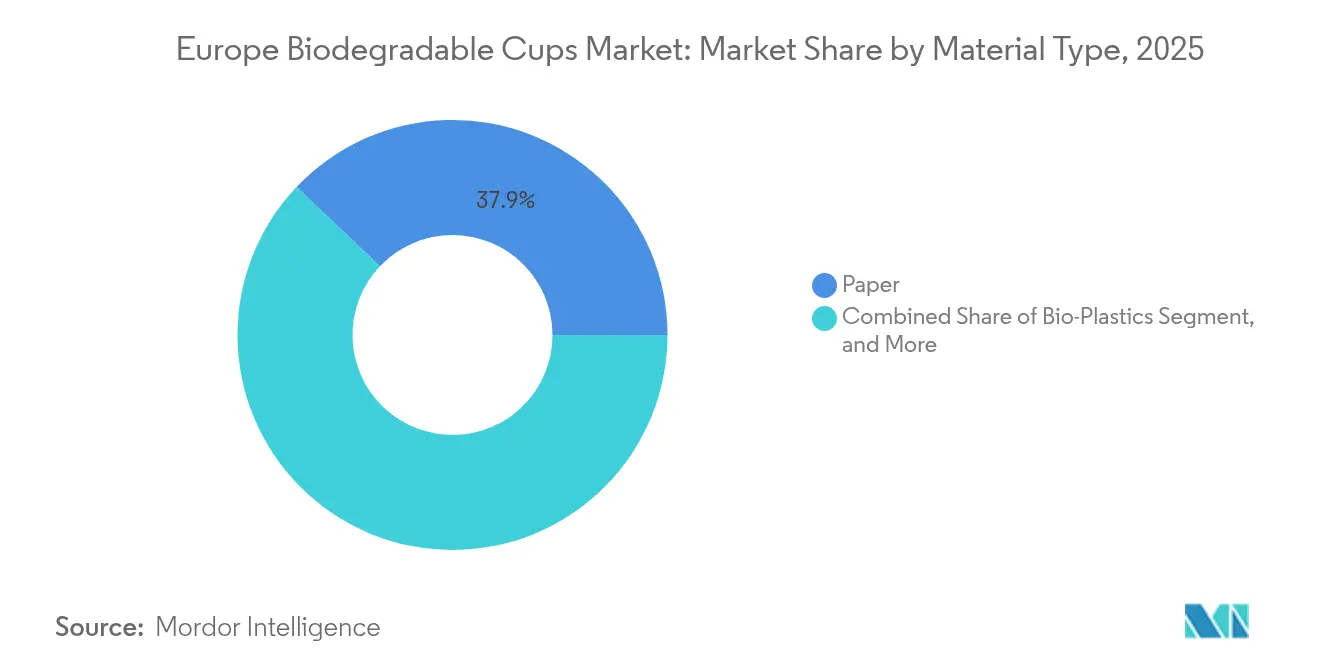

- By material type, paper captured 37.92% of the Europe biodegradable cups market share in 2025, while bio-plastics are projected to expand at an 8.02% CAGR between 2026 and 2031.

- By application, beverages accounted for a 70.12% share of the Europe biodegradable cups market size in 2025 and are forecast to grow at a 7.05% CAGR through 2031.

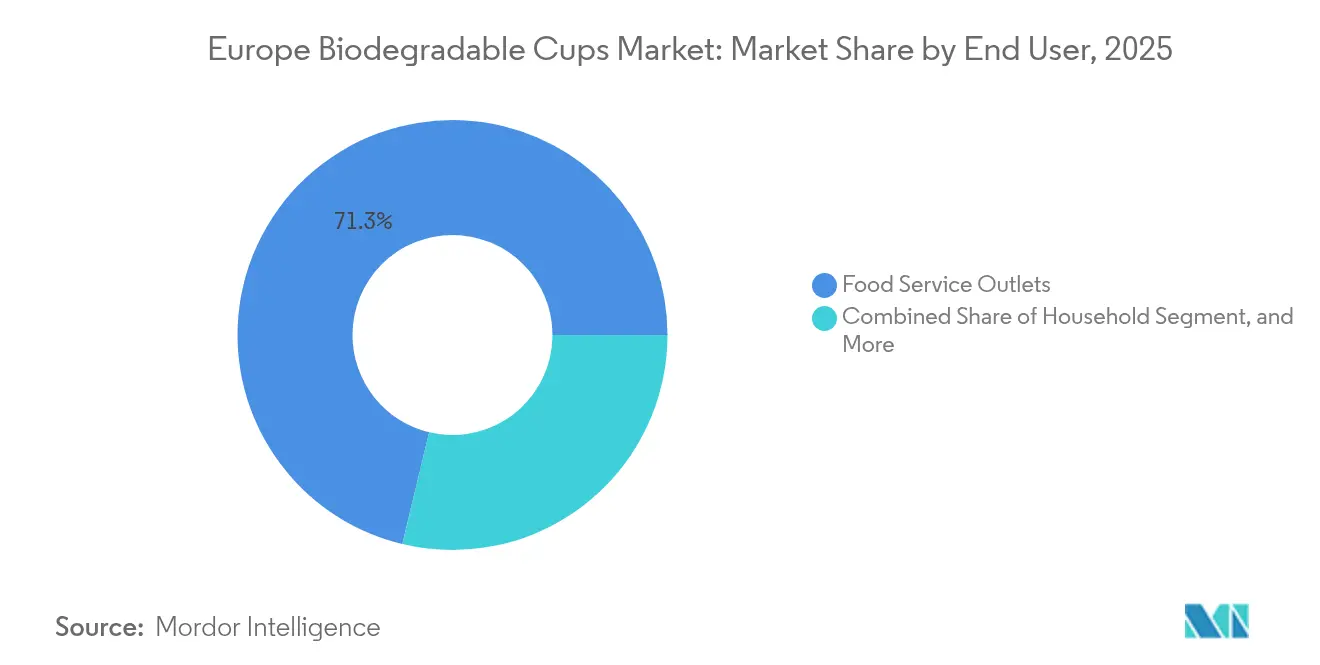

- By end user, food service outlets held a 71.25% share of the Europe biodegradable cups market size in 2025, whereas the institutional segment is poised for the quickest growth at a 7.54% CAGR to 2031.

- By distribution channel, offline sales accounted for a 67.88% share of the Europe biodegradable cups market size in 2025; however, online platforms are expected to log the highest 7.28% CAGR over 2026-2031.

- By country, the United Kingdom commanded a 21.55% share of regional revenue in 2025, while Spain is expected to register the fastest growth rate of 7.98% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Biodegradable Cups Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Sustainable Foodservice Packaging | +1.8% | UK and Benelux strongest | Medium term (2-4 years) |

| Stringent EU Single-Use Plastics Regulations | +2.1% | EU-wide, peak in Spain and France | Short term (≤ 2 years) |

| Coffee Chain Commitments to 100% Compostable Cups | +1.3% | UK, Germany, France | Short term (≤ 2 years) |

| Excess PLA Production Capacity Drives Price Cuts | +1.2% | All European markets | Medium term (2-4 years) |

| Retailer-Led Private-Label Eco-Packaging Race | +0.9% | UK, Germany, France | Medium term (2-4 years) |

| AI-Optimised Coating Lines Reduce Scrap Rates | +0.6% | Germany, UK | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable Foodservice Packaging

European consumers are showing a growing intolerance for single-use plastics. A 2024 Eurobarometer survey reported that 78% now factor sustainability into venue choice.[1]Eurobarometer, “Special Eurobarometer 523: Attitudes of Europeans Towards Waste Management and the Circular Economy,” europa.eu Contract caterers and quick-service chains translate sentiment into procurement policies, as evidenced by Compass Group shifting 62% of cup purchases to compostable materials across 2,000 sites. McDonald’s committed in February 2025 to fiber cups with water-based coatings for every UK and Ireland outlet, eliminating polyethylene liners. EU regulations reinforce preference, mandating that all packaging be recyclable or compostable by 2030. Willingness to pay varies—Swedish patrons accept price increases of up to 12%, while operators in price-sensitive Italy and Spain demand cost parity before switching.

Stringent EU Single-Use Plastics Regulations

Member states are expected to reach full enforcement of the Single-Use Plastics Directive in 2024, closing loopholes and expanding bans. Spain prohibited the use of non-compostable cups in hospitality venues as of January 2024, with fines of up to EUR 600,000.[2]Boletín Oficial del Estado, “Real Decreto 1055/2022,” boe.es France’s AGEC law set a 2025 target for 20% reusable packaging but simultaneously banned Oxo-degradable plastics, boosting short-run demand for certified compostable cups. Italy now requires single-use cups to contain at least 40% bio-based content, essentially reserving shelf space for PLA-lined or fiber alternatives. Extended producer responsibility fees on non-recyclable cups in Germany and the Netherlands raise the relative cost of traditional plastics, accelerating the adoption of biodegradable cups in Europe.

Excess PLA Production Capacity Drives Price Cuts

Capacity expansions by NatureWorks and TotalEnergies Corbion created a PLA surplus, which pushed spot prices down by about 15% between Q1 2024 and Q1 2025.[3]ICIS, “Polylactic Acid (PLA) Pricing Data Q1 2024 – Q1 2025,” icis.com European converters captured the benefit: Vegware reported a 3.2-percentage-point decline in raw-material costs, allowing it to hold prices while widening its margins. As PLA premiums over polyethylene shrink to roughly 18%, bioplastic cups gain ground in high-volume beverage chains, cementing their appeal in the Europe biodegradable cups market.

Coffee Chain Commitments to 100% Compostable Cups

Starbucks achieved 94% penetration of compostable cups across 3,000 European stores by September 2024 and aims to reach 100% by December 2025. Costa Coffee completed a PLA-lined cup rollout in March 2024, affecting 200 million units annually. Pret A Manger plans to drop plastic lids by June 2025. These large buyers impose sustainability benchmarks on smaller chains, compounding demand for certified compostable cups across the Europe biodegradable cups market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Premium Versus Conventional Paper and Plastic Cups | -1.4% | Italy, Spain, Rest of Europe | Medium term (2-4 years) |

| Patchy Industrial Composting Infrastructure | -1.1% | France, Italy, Rest of Europe | Long term (≥ 4 years) |

| Rising Pulp Prices and Supply Volatility | -0.8% | EU-wide | Short term (≤ 2 years) |

| Reusable Cup Deposit Systems Cannibalise Demand | -1.0% | Germany, France, Benelux | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Premium Versus Conventional Paper and Plastic Cups

In Q1 2025, a 12-ounce PLA-lined cup sold for EUR 0.09-0.12, compared to EUR 0.07-0.09 for polyethylene-coated units, resulting in a 15-25% premium that margin-constrained cafés struggle to absorb. Independent operators, especially in Southern Europe, exhibit high price elasticity: 54% would postpone switching if unit costs rise more than EUR 0.03. While EPR fees reduce the penalty on certified cups in Germany and France, similar offsets remain minimal in Italy or Central Europe, tempering volume conversion in the Europe biodegradable cups market.

Patchy Industrial Composting Infrastructure

Industrial composting coverage spans 75% of residents in Germany, but only 55% in France and under 40% in Italy. Cups discarded in regions without high-temperature facilities often end up in landfills or incineration, eroding environmental claims and exposing brands to accusations of greenwashing. Building a new plant costs EUR 5-15 million and takes up to two years for permitting, an investment many municipalities defer. The disposal gap creates operational friction for small foodservice outlets that must segregate waste, slowing end-user adoption of biodegradable cups across the European market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bio-Plastics Narrow the Cost Gap with Paper

Bio-plastics represent the fastest-growing material class, forecast to rise at 8.02% CAGR as oversupply trims PLA resin prices and spurs substitution away from polyethylene liners. PBAT blends captured an additional 18% share, thanks to their improved heat resistance for hot drinks. Emerging polyhydroxyalkanoates attract coastal operators because marine degradability eases litter liability. Paper retains the largest slice at 37.92% but expands more slowly, partly because fiber cups still underperform PLA in high-temperature service. Elevated pulp costs, with European kraft pulp averaging EUR 1,420 per ton (USD 1,562) in Q1 2025, also weigh on converter margins. Bagasse and wheat-straw substrates draw policy support under EU agricultural-waste valorization schemes, yet remain niche due to limited forming capacity. The traction of bioplastics underlines a broader pivot: as material parity improves, the Europe biodegradable cups market growth increasingly flows to resins that deliver high barrier performance without compromising compostability.

The paper’s durability issues with steaming liquids and its reliance on water-based coatings constrain its long-term outlook. Nonetheless, its ubiquity in converter lines and consumer familiarity keep it the entry-level sustainable option for price-sensitive buyers. In contrast, bio-plastics now command greater attention in requests for quotation issued by institutional buyers, signaling that procurement teams value certifications and heat performance over legacy supply relationships. This mix shift ensures that bio-plastics’ unit volumes will close in on paper by the end of the decade, even if the latter maintains a legacy footprint in the cold-drink service. Europe biodegradable cups market players, able to flex between fiber- and resin-lined cups, stand to secure the widest customer base.

By Application: Beverages Remain, King While Food Gains Share

In 2025, beverages held a dominant 70.12% share of the Europe biodegradable cups market, with projections indicating a robust 7.05% CAGR growth rate extending through 2031. Hot drinks drive most demand, yet iced beverages deliver incremental summer spikes that reward converters with agile scheduling. Beverage operators prize tight dimensional tolerances for automated lid fit, nudging them toward higher-spec PLA or dual-layer fiber cups.

The food segment, encompassing soups, noodles, and desserts, is projected to grow at a rate of approximately 6.55% CAGR, driven by the expansion of quick-service chains into hot-food-to-go menus. Larger cup formats push average selling prices higher than those of drinks, thereby cushioning converter margins. However, variable fill temperatures and oil content necessitate multilayer construction, which raises costs and limits uptake in smaller cafés. Europe biodegradable cups market share in food applications grows slowly but steadily because institutional buyers value closed-loop waste contracts that include food residues plus cup composting. As these contracts proliferate, food cups gain a firmer beachhead alongside beverages.

By End User: Institutional Buyers Accelerate

Food service outlets held a 71.25% share of the European biodegradable cups market size in 2025, whereas Institutional procurement, encompassing offices, malls, hospitals, and universities, experiences a 7.54% CAGR as EU green purchasing guidelines shift from voluntary to mandatory. The Europe biodegradable cups market size for institutional channels reached approximately USD 107.54 million in 2026 and is expected to reach USD 154.73 million by 2031. Public agencies and corporate landlords now specify EN 13432 certification in catering contracts, tilting demand toward suppliers with third-party audit trails.

Foodservice outlets still account for more than half of unit volumes, although their growth moderates to near 6.5% as deposit-return schemes shave single-use sales in Germany and France. Independent cafés in Italy and Spain remain price-conscious, prolonging mixed inventories of conventional and compostable cups. Household retail remains the smallest end-user slice but benefits from e-commerce bundling of eco-friendly partyware kits that drive impulse purchases. The widening institutional share reinforces the resilience of the Europe biodegradable cups market because contract terms often lock in multi-year volumes, sheltering suppliers from consumer footfall volatility.

By Distribution Channel: Online Platforms Democratize Access

In 2025, offline sales accounted for 67.88% of total revenue, but online platforms are poised to achieve the highest growth rate, with a projected CAGR of 7.28% from 2026 to 2031. B2B marketplaces list granular SKU data, live inventory, and carbon footprint metrics, allowing small cafés to sidestep minimum-order hurdles that once deterred sustainable packaging. Amazon Business’s next-day delivery compresses lead times and pressures legacy distributors to match service levels.

Offline channels preserve an edge with high-volume chains that negotiate annual tenders bundled with other consumables. In Southern and Eastern Europe, offline penetration holds because digital adoption lags and last-mile logistics remain fragmented. However, even traditional distributors are digitizing; Bunzl reported that e-sales rose to 34% of European revenue in 2024. This hybrid future suggests that suppliers must integrate seamlessly with electronic data interchange while retaining field sales for consultative pitches, a duality that defines winning go-to-market strategies in the Europe biodegradable cups market.

Geography Analysis

The United Kingdom held a 21.55% share in 2025 and is expected to advance at a 6.52% CAGR through 2031, driven by coffee-chain mandates and a Plastic Packaging Tax that adds GBP 0.02 (USD 0.025) per conventional cup, narrowing the cost gap with certified compostables. Composting infrastructure covers approximately 70% of residents, providing brands with confidence in their end-of-life claims. Near-term upside is moderated as reusable pilot programs gain media traction in large cities, but institutional procurement maintains baseline demand stability.

Germany owned roughly 23.65% of the Europe biodegradable cups market share in 2025, but will trail the regional average at 5.55% CAGR because Mehrwegpflicht forces outlets above 80 square meters to offer reusable options, reducing single-use volumes by up to one-tenth. Nevertheless, its 1,200 composting sites, strong certification culture, and corporate sustainability agendas prevent outright contraction.

Spain posts the fastest 7.98% CAGR, driven by bans in Catalonia and Valencia and a rebound in tourist arrivals, which are expected to exceed 85 million in 2024. Coastal hospitality clusters with limited space for dishwashing equipment often find compostable disposables to be the only feasible single-use option. Limited composting coverage outside major metropolitan areas tempers the upside but does not derail momentum where regional governments provide dedicated organic waste collection.

France and Italy ride mid-tier growth at roughly 6.33% and 6.05% CAGR, respectively. France’s AGEC law mandates 20% reusable packaging by 2025, which slows growth in Paris and Lyon, while the lack of nationwide cup deposit schemes still leaves room for compostables. Italy’s 40% bio-based-content rule channels buyers toward PLA and fiber, yet fragmented cafés resist switching until premiums narrow further.

Benelux markets benefit from dense composting networks and EPR fee differentials, but contribute modest volumes due to their small population base. Nordic and Central European countries deliver mixed results. Sweden leans heavily into reusables, whereas Poland’s quick-service boom boosts demand for certified compostables.

Competitive Landscape

Five suppliers captured around 45-50% of 2024 volumes, giving the Europe biodegradable cups market a moderately concentrated structure. Huhtamaki and Stora Enso utilize integrated fiber-to-cup operations, enabling them to hedge against pulp inflation and provide chain-of-custody documentation to multinational coffee clients. Huhtamaki commissioned a EUR 28 million (USD 30.8 million) molded-fiber line in Northern Ireland in March 2025, boosting capacity by 400 million units with AI-enabled defect detection that cuts scrap below 2%. Stora Enso has locked in a five-year PLA feedstock deal at prices 10% below the Q4 2024 spot, stabilizing offers to institutional buyers.

Specialists such as Vegware and Bio Futura monetize premium niches by stacking certifications—EN 13432, TÜV Austria OK Compost, and BPI —while offering custom printing that commands 8-12% price increases. Vegware hedged demand risk by partnering with Recup to supply compostable backup cups for reusable schemes in 6,000 German outlets. Digital-native distributors like Packhelp leverage online price transparency by bundling carbon-footprint calculators that resonate with small cafés under pressure from CSRD reporting.

Technology is increasingly differentiating players. Dart Container’s AI-optimized coating patent trims scrap and saves EUR 0.008 per cup, signaling a new efficiency race. Material innovators, such as Notpla, have rolled out seaweed-coated fiber cups that degrade in home compost, sidestepping infrastructure gaps in Southern Europe. Competitive intensity will remain acute as PLA cost deflation lowers entry barriers and online platforms ease market access for disruptive brands, yet incumbents retain volume defense through direct chain contracts and scale economies in certification audits.

Europe Biodegradable Cups Industry Leaders

Huhtamaki Oyj

Vegware Ltd.

Dart Container Corporation

Benders Paper Cups Ltd.

Genpak LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Huhtamaki Oyj completed the commissioning of a EUR 28 million (USD 31.6 million) molded-fiber cup production line at its Lurgan, Northern Ireland facility, expanding annual capacity by 400 million units and positioning the company to capture incremental volumes from UK coffee chains' compostable-cup commitments, with the new line featuring AI-driven quality control that reduces scrap rates to below 2.0 percent.

- February 2025: Stora Enso Oyj announced a five-year supply agreement with NatureWorks LLC to procure polylactic acid resin at fixed pricing approximately 10 percent below Q4 2024 spot rates, insulating the company from feedstock volatility and enabling it to offer stable pricing to institutional buyers through 2029, a strategic move disclosed in the company's Capital Markets Day presentation.

- February 2025: McDonald's Corporation announced in February 2025 that all UK and Ireland locations would exclusively use fiber-based cups with water-based coatings, eliminating polyethylene liners.

- January 2025: Vegware Ltd. entered a partnership with Recup GmbH, Germany's largest reusable-cup deposit-scheme operator, to supply compostable "backup" cups for customers who forget reusable containers, creating a hybrid model that hedges single-use volume cannibalization while maintaining brand presence in over 6,000 German foodservice outlets.

Europe Biodegradable Cups Market Report Scope

The Europe Biodegradable Cups Market refers to the market for cups made from biodegradable materials that decompose naturally in the environment, reducing waste and environmental impact. These cups are increasingly used as a sustainable alternative to conventional plastic cups in various applications.

The Europe Biodegradable Cups Market is Segmented by Material Type (Bio-Plastics, Paper, Bagasse and Plant Fibre), Application (Beverages, Food), End User (Food Service Outlets, Institutional, Household), Distribution Channel (Offline, Online), and Geography (United Kingdom, Germany, France, Italy, Spain, Benelux, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

| Bio-Plastics | Polylactic Acid (PLA) |

| Poly(Butylene Adipate-co-Terephthalate) (PBAT) | |

| Polybutylene Succinate (PBS) | |

| Polyhydroxyalkanoates (PHA) | |

| Other Bio-Plastics | |

| Paper | |

| Bagasse and Plant Fibre |

| Beverages |

| Food |

| Food Service Outlets (Cafés and Hotels) |

| Institutional (Malls and Commercial Establishments) |

| Household |

| Offline |

| Online |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Benelux |

| Rest of Europe |

| By Material Type | Bio-Plastics | Polylactic Acid (PLA) |

| Poly(Butylene Adipate-co-Terephthalate) (PBAT) | ||

| Polybutylene Succinate (PBS) | ||

| Polyhydroxyalkanoates (PHA) | ||

| Other Bio-Plastics | ||

| Paper | ||

| Bagasse and Plant Fibre | ||

| By Application | Beverages | |

| Food | ||

| By End User | Food Service Outlets (Cafés and Hotels) | |

| Institutional (Malls and Commercial Establishments) | ||

| Household | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Benelux | ||

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe biodegradable cups market in monetary terms?

The market generated USD 276.89 million in revenue during 2026 and is projected to reach USD 374.36 million by 2031.

What growth rate is forecast for biodegradable cups across Europe?

Market revenue is anticipated to expand at a 6.21% compound annual growth rate between 2026 and 2031.

Which material type is growing fastest?

Bio-plastic cups, mainly PLA-lined formats, are forecast to increase at 8.02% CAGR through 2031, the quickest among material categories.

Why is Spain the fastest-growing national market?

Regional single-use plastic bans that took effect in 2024 and a rebound in tourism drive Spain’s 7.98% CAGR outlook to 2031.

How are online distributors influencing procurement?

B2B e-commerce platforms now feature instant pricing and carbon-footprint data, enabling small cafés to order certified compostable cups with next-day delivery, which fuels a 7.28% CAGR for online channels.

What challenges limit wider adoption of biodegradable cups?

Premium prices over conventional cups and uneven industrial composting coverage restrict growth, particularly in Southern and Eastern Europe.

Page last updated on: