Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

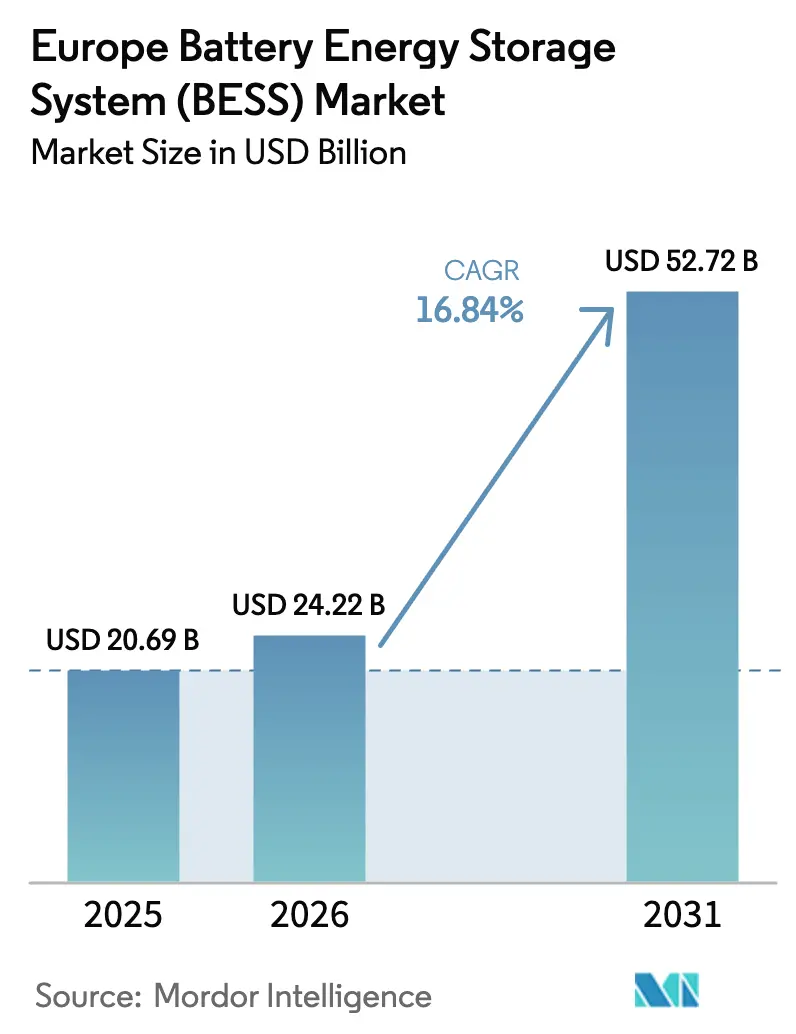

| Base Year Market Size (2025) | USD 20.69 Billion |

| Market Size (2026) | USD 24.22 Billion |

| Market Size (2031) | USD 52.72 Billion |

| Growth Rate (2026 - 2031) | 16.84% CAGR |

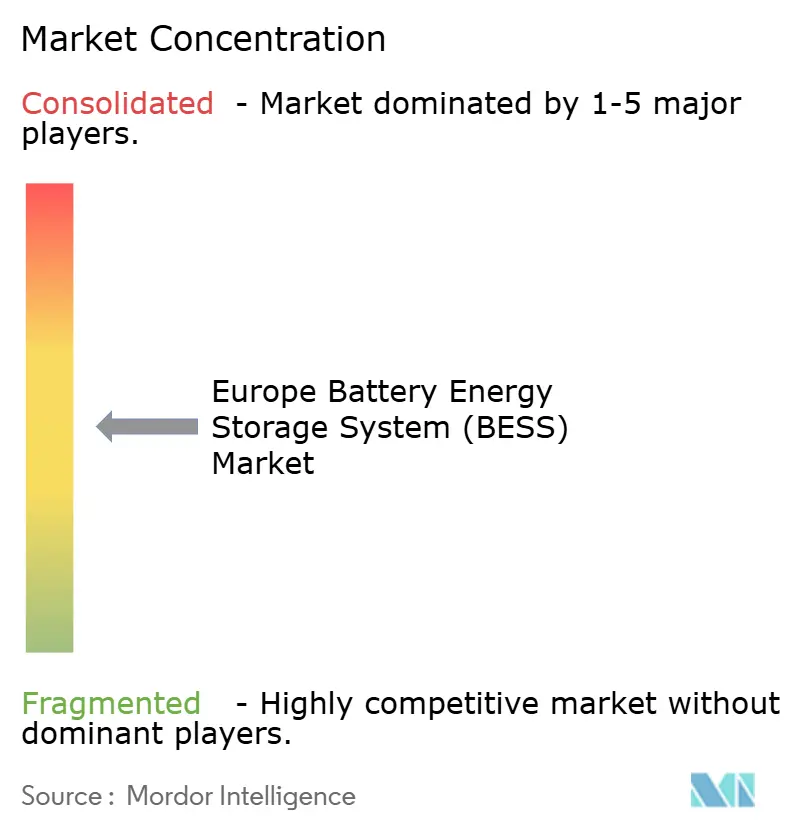

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Battery Energy Storage System (BESS) Market Analysis by Mordor Intelligence

The Europe Battery Energy Storage System (BESS) market size is projected to expand from USD 20.69 billion in 2025 and USD 24.22 billion in 2026 to USD 52.72 billion by 2031, reflecting a 16.84% CAGR and confirming investor confidence in long-duration grid flexibility solutions. This growth curve aligns with the European Commission mandate that 30% of balancing reserves must come from non-fossil assets by 2030, encouraging utilities to substitute gas peakers with batteries.[1]: European Commission, “Revised Electricity Market Regulation,” ec.europa.eu Revenue certainty has improved as competitive capacity and fast-reserve auctions in the United Kingdom and Italy compress payback periods below seven years, drawing pension funds and infrastructure specialists into the European Battery Energy Storage Systems market. Technology mix continues to favor lithium-iron-phosphate cells thanks to cycle-life advantages, although flow chemistries are gaining traction where duration exceeds four hours. Industrial clusters in Germany, Spain, and the Nordic countries are deploying hybrid solar-plus-storage projects to hedge against grid-connection delays that now average 36 months, while residential prosumers monetize time-of-use spreads that widened to EUR 0.26–0.36 per kWh in late 2025.

Key Report Takeaways

- By battery type, lithium-ion commanded 87.8% of the European Battery Energy Storage Systems market share in 2025; flow batteries are forecast to expand at a 28.3% CAGR through 2031.

- By connection type, on-grid installations accounted for 85.5% of the European Battery Energy Storage Systems market size in 2025, while off-grid systems are projected to grow at 28.9% to 2031.

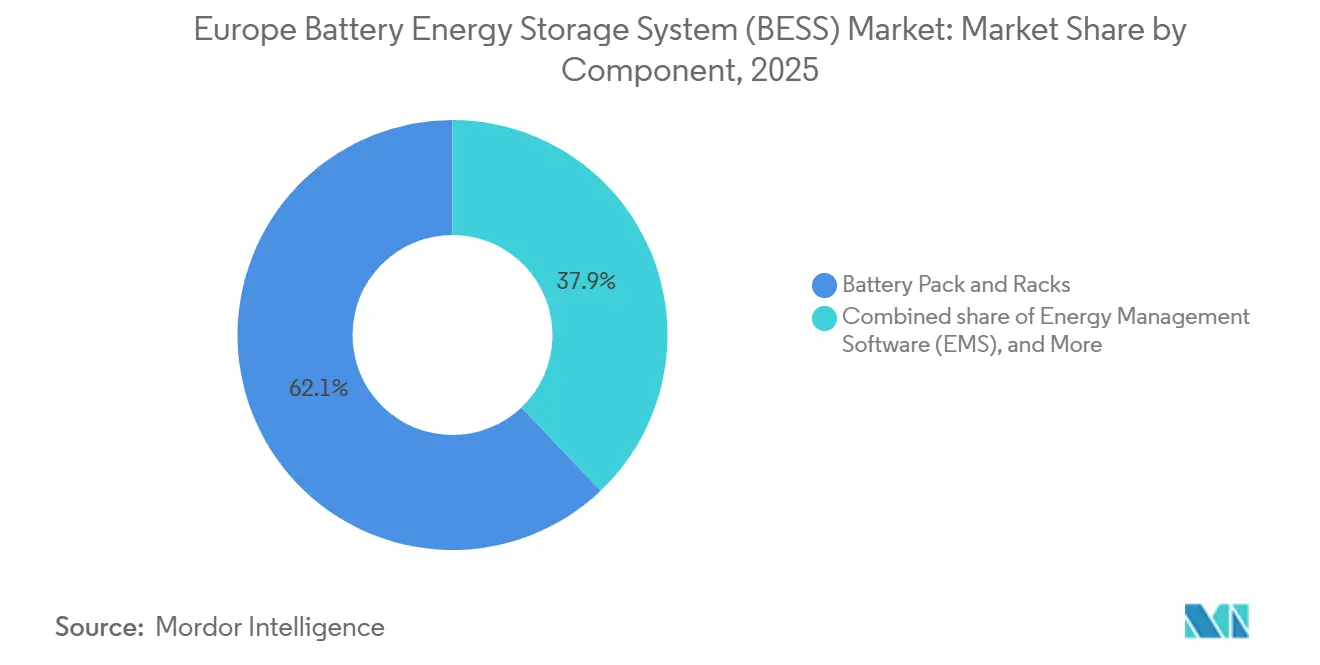

- By component, battery packs and racks represented 62.1% of total system value in 2025; energy-management software is advancing at a 31.4% CAGR through 2031.

- By energy capacity, systems in the 10–100 MWh band held 47.3% of deployments in 2025, whereas projects above 500 MWh will expand at a 30.1% CAGR through 2031.

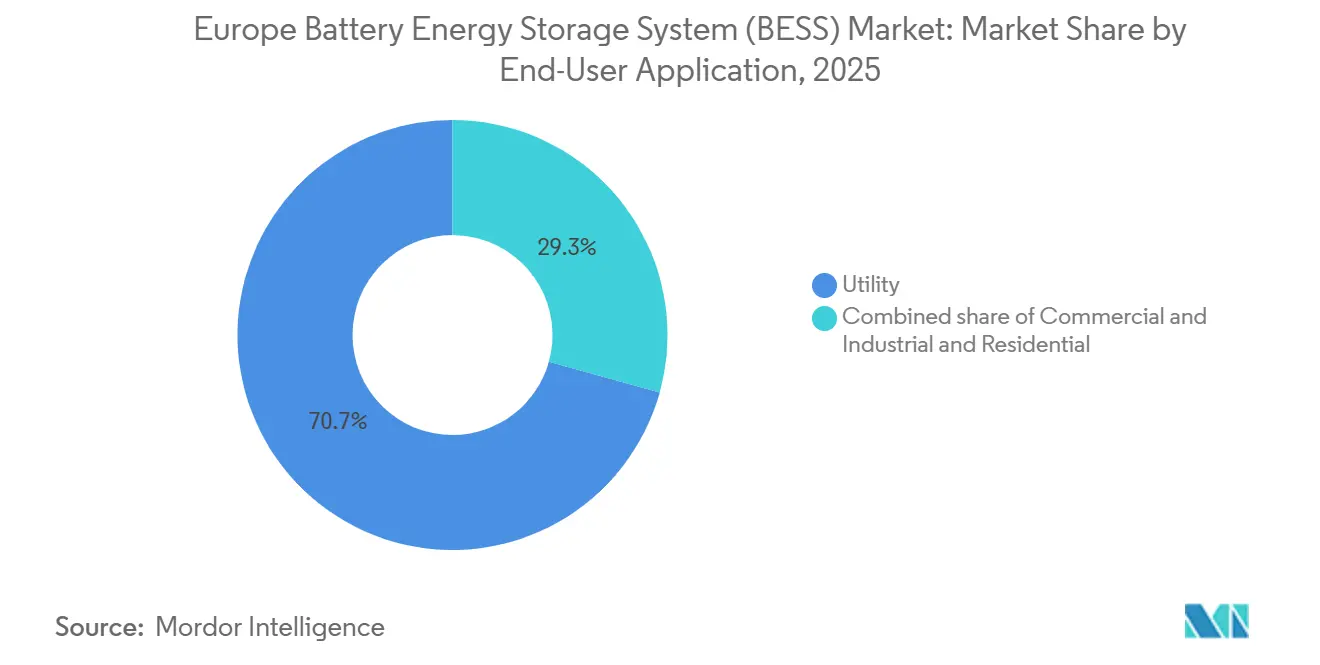

- By end-user, utilities captured 70.7% of demand in 2025; commercial and industrial users are forecast to post a 29.5% CAGR to 2031.

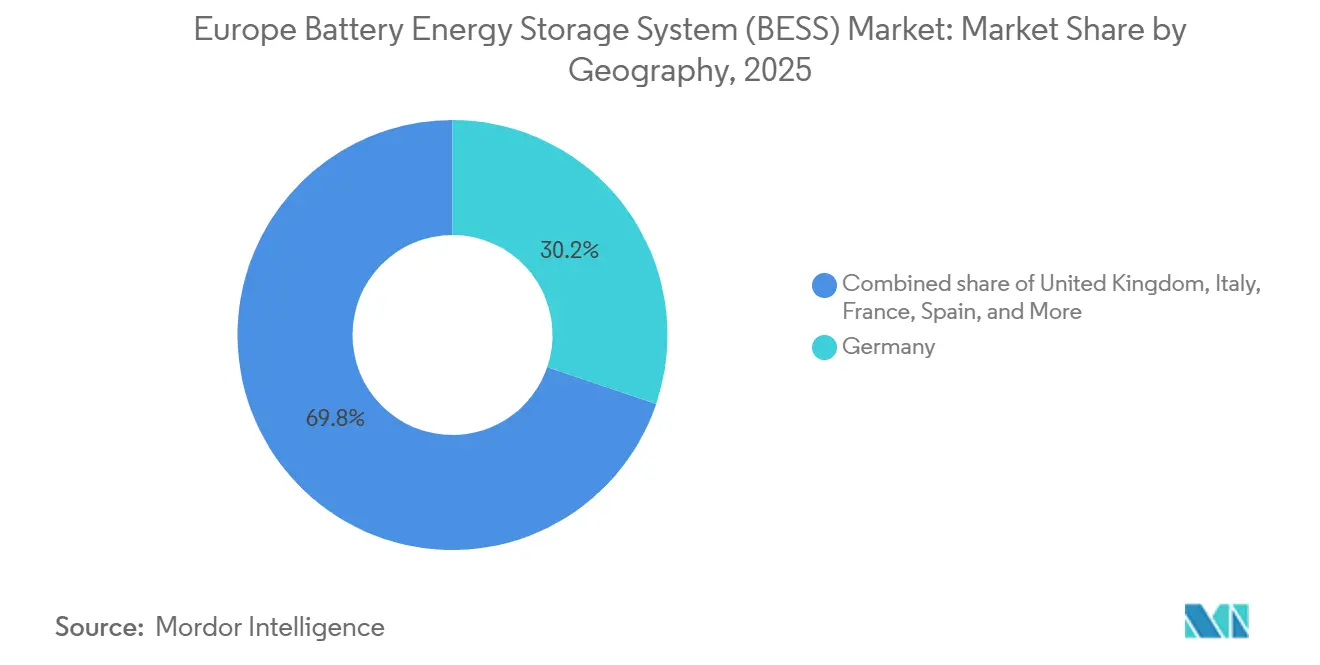

- By geography, Germany led with a 30.2% share of the European Battery Energy Storage Systems market in 2025, while the United Kingdom is expected to grow at a 22.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Battery Energy Storage System (BESS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-wide Fit-for-55 Flexibility Mandates Accelerating BESS Procurement | 3.2% | EU-wide, strongest in Germany, Netherlands, Belgium | Medium term (2-4 years) |

| Residential Prosumer Tariff-Arbitrage Amid Record-High Retail Prices | 2.8% | Germany, Denmark, Belgium, Ireland | Short term (≤ 2 years) |

| National Capacity & Fast-Reserve Auctions Creating Bankable Revenue Stacks | 3.5% | United Kingdom, Italy, France | Medium term (2-4 years) |

| Germany's Smart-Meter Roll-out Unlocking Behind-the-Meter Aggregation | 2.1% | Germany, with spillover to Austria, Switzerland | Long term (≥ 4 years) |

| Corporate PPA Boom Driving Co-located BESS with Utility-Scale Renewables | 2.9% | Spain, Nordic countries, Poland | Medium term (2-4 years) |

| Accelerated De-Risking of Li-ion Supply via EU Battery Passport & Critical-Mineral Acts | 1.9% | EU-wide, manufacturing hubs in France, Germany, Sweden | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-Wide Fit-for-55 Flexibility Mandates Accelerating BESS Procurement

The directive requires each member state to source at least 30% of balancing reserves from non-fossil resources by 2030, providing a structural demand floor for the European Battery Energy Storage Systems market. Battery projects now pre-qualify for automatic frequency restoration tenders that formerly went to hydro and gas assets, shortening payback periods below seven years in Germany and the Netherlands.[2]European Commission, “Fit-for-55 Legislative Package,” ec.europa.eu Developers are racing to secure connection agreements ahead of expected queue reforms, while transmission operators add interim targets that further pull forward investment decisions.

Residential Prosumer Tariff-Arbitrage Amid Record-High Retail Prices

Retail electricity prices averaged EUR 0.41 per kWh in late 2025 in Germany, creating a spread of EUR 0.26–0.36 versus day-ahead wholesale prices.[3]Eurostat Analysts, “Electricity Price Statistics 2025,” eurostat.ec.europa.eu This margin underpins eight-to-ten-year payback periods for 10 kWh home systems even without feed-in tariffs. More than 60% of German residential batteries now use algorithms that charge during negative-price hours, which occurred 300 times in 2025, and discharge during evening peaks.

National Capacity & Fast-Reserve Auctions Creating Bankable Revenue Stacks

The February 2025 U.K. Capacity Market awarded 1.8 GW of battery contracts at GBP 63 per kW per year, while National Grid committed to 4.5 GW of exclusive battery fast-reserve procurement by 2028.[4]U.K. Government, “Capacity Market Auction Results 2025,” gov.uk Italy and France introduced similar mechanisms, enabling lenders to underwrite 12% blended IRRs on multi-layered revenue stacks.

Germany’s Smart-Meter Roll-out Unlocking Aggregation of Behind-the-Meter Storage

Mandatory smart meters for high-consumption households allow aggregators to pool residential batteries into virtual power plants, providing real-time telemetry that meets market participation rules. Platforms operated by Next Kraftwerke and Sonnen already offer over 50,000 aggregated batteries to day-ahead and balancing markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Connection Queues and Limited Interconnection Capacity | -2.7% | Germany, Spain, United Kingdom | Short term (≤ 2 years) |

| Volatile Ancillary-Service Prices Undermining Project IRRs | -1.9% | Germany, Netherlands, Nordic countries | Medium term (2-4 years) |

| Fire-Safety & Urban-Zoning Rules Raising Capex for Dense Cities | -1.4% | Germany, United Kingdom, France (urban cores) | Long term (≥ 4 years) |

| Reliance on Chinese Cell Imports Exposing Projects to FX & Trade-Policy Risk | -1.6% | EU-wide, acute in Southern and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Queues and Limited Interconnection Capacity

Germany’s queue exceeded 100 GW by end-2025, stretching wait times to 36 months and eroding project NPVs by up to 20%. Spain and the United Kingdom face similar constraints, prompting the U.K. grid operator to adopt a first-ready approach that favors shovel-ready applications.

Volatile Ancillary-Service Prices Undermining Project IRRs

Germany’s frequency containment reserve prices fell from EUR 8,500 per MW per month in early 2024 to EUR 3,200 by mid-2025 as 3 GW of new batteries saturated a 600 MW market. Comparable swings in the Netherlands and Nordic zones force developers to hedge revenues with more complex contracts, raising transaction costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Flow Chemistries Gain Duration Edge

Lithium-ion held 87.8% of installed capacity in 2025, giving the segment the dominant Europe Battery Energy Storage Systems market share. Flow batteries, expanding at a 28.3% CAGR, appeal to grid operators that need 6–10 hour discharge profiles and wish to avoid lithium cost escalations. Sodium-ion and lithium titanate technologies are entering pilot phases for specific resilience or temperature-tolerant applications. Overall, chemistry diversification is likely to cap lithium’s share below 80% by 2031, even as absolute lithium volume continues to rise.

The European Battery Energy Storage Systems market size for flow chemistries is expected to surpass USD 4 billion by 2031, supported by vendor-financed warranties exceeding 20 years. Utility preference for multi-hour assets aligns with interconnection upgrades that favor fewer, longer-duration systems, while corporate buyers value the environmental credentials embedded in vanadium recycling chains.

By Connection Type: Off-Grid Surge Offsets On-Grid Dominance

On-grid assets accounted for 85.5% of capacity in 2025, reflecting mature grid-service revenue models. Off-grid and hybrid microgrids will advance at a 28.9% CAGR, carving new demand pools inside industrial campuses and island communities. The European Battery Energy Storage Systems market size tied to off-grid mining operations already exceeds USD 1 billion, highlighted by Wärtsilä’s 10 MW Swedish microgrid that delivered 40% savings in 2025.

As grid queues lengthen, data-center operators and chemical producers are securing off-grid permits that bypass transmission interconnection. Hybrid plants capable of islanding during outages support resilience mandates and reduce network charges that can reach EUR 150 per kW yearly in Germany.

By Component: Software Emerges as Value Driver

Battery packs captured 62.1% of system cost in 2025, yet price competition among Asian cell makers is squeezing margins and shifting value toward control software. Energy-management platforms are growing at 31.4% as asset owners seek to optimize hourly bids across multiple markets, lifting revenue by as much as 25% relative to static dispatch. The European Battery Energy Storage Systems market share attributable to software and analytics is poised to double by 2031.

Fire-safety and HVAC subsystems now add EUR 50–80 per kWh in dense urban jobs because of Germany’s VDE-AR-E 2510-50 and the United Kingdom’s BS 5839-1 standards. Vendors that can integrate these requirements into factory-built enclosures gain schedule and cost advantages.

By Energy Capacity Range: Bigger Blocks, Lower Unit Cost

Systems between 10 and 100 MWh held a 47.3% share in 2025, favored for permitting agility. However, assets above 500 MWh will expand at 30.1% through 2031 as transmission operators prefer fewer interconnection nodes that simplify grid-code compliance. Fluence’s 500 MWh Schleswig-Holstein plant illustrates how large-scale systems can stack frequency, capacity, and arbitrage income under a single grid agreement.

In contrast, sub-10 MWh residential and small-commercial units will keep growing where retail-wholesale spreads exceed 3:1. This bifurcation creates unique service niches for integrators specializing either in distributed fleets or in giga-scale turnkey projects.

By End-User Application: C&I Momentum Builds

Utilities dominated demand with a 70.7% share in 2025, but commercial and industrial buyers are growing at 29.5% on the back of Scope 2 reporting rules and demand-charge pressures. The Europe Battery Energy Storage Systems market size linked to data centers will climb sharply as Amazon and other hyperscalers commit to 24/7 carbon-free energy targets.

Industrial companies in chemicals, steel, and cement deploy behind-the-meter batteries to shave peak-network fees and participate in demand response. Residential uptake remains strongest in Germany, Belgium, and Denmark, where time-of-use tariffs favor daily cycling.

Geography Analysis

Germany held a 30.2% share of the European Battery Energy Storage Systems market in 2025, underpinned by EUR 0.41 per kWh retail tariffs and a 2 GW annual auction schedule that provides long-term revenue visibility. Smart-meter mandates enable aggregators to pull household batteries into wholesale and balancing markets, yet grid-connection queues above 100 GW extend commissioning times beyond three years, eroding returns.

The United Kingdom is the fastest expanding market with a 22.2% forecast CAGR to 2031, powered by 15-year Capacity Market contracts and National Grid’s 4.5 GW battery fast-reserve target. Italy follows as Terna reserves 2 GW of ultra-fast frequency response for storage, offering EUR 12,000 per MW per month payments that layer onto wholesale arbitrage.

France and Spain scale deployments alongside solar and wind pipelines. Spain’s 8 GW solar-storage queue is concentrated in Extremadura and Andalusia, where corporate PPAs pre-contract the majority of output, mitigating merchant risk. Nordic countries adopt hybrid wind-battery assets that lower balancing costs by 40% and suit cold-weather sodium-ion trials, while Poland emerges with a 3 GW pipeline aimed at manufacturing off-takers.

Competitive Landscape

The top five integrators, Fluence, Tesla, Wärtsilä, BYD, and Hitachi Energy, controlled roughly 48% of contracted gigawatt-hours in 2025, positioning the European Battery Energy Storage Systems market at moderate concentration. Fluence leverages its Mosaic optimizer to raise asset revenues by up to 25%, embedding long-term service agreements that stabilize cash flow. Tesla benefits from vertically integrated Megapack manufacturing at its Berlin-Brandenburg site, lowering capex and pairing Autobidder software with lithium-iron-phosphate cells.

Wärtsilä competes in off-grid mining and island microgrids, offering black-start capability that commands premium pricing. BYD opened a Rotterdam hub in 2025 to ship 5 GWh annually under 15-year warranties, while Hitachi Energy integrates digital twins for grid-forming inverters. Niche providers such as Invinity focus on durations beyond six hours using vanadium flow technology, and aggregators like Next Kraftwerke monetize residential fleets without owning hardware.

Price pressure intensifies as Chinese cell suppliers move downstream into turnkey EPC, while new European gigafactories from Northvolt and ACC supply low-carbon cells that qualify projects for sustainable finance. Patent filings around thermal-management and fire-suppression modules are rising, reflecting tougher urban safety rules that add EUR 50–80 per kWh in dense city projects.

Europe Battery Energy Storage System (BESS) Industry Leaders

Fluence Energy Inc.

Tesla Inc.

BYD Co. Ltd.

LG Energy Solution Ltd.

Wärtsilä Oyj Abp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Switzerland authorised an 800 MW/1,600 MWh redox-flow plant in Laufenburg, setting a global record for the technology and enhancing continental grid resilience.

- May 2025: Northvolt revealed plans to curtail Swedish battery production, highlighting the competitiveness challenge posed by Asian suppliers.

- April 2025: BW ESS and Nordea Bank closed the largest Nordic storage financing package, backing multi-gigawatt deployment.

- March 2025: LG Energy Solution signed a USD 384 million supply deal with PGE for Poland’s 900 MWh BESS, leveraging its Wrocław facility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European battery energy storage system market as all stationary, grid-connected systems that use rechargeable electrochemical batteries, associated management hardware, and software for power shifting, frequency regulation, or backup across front- and behind-the-meter applications.

Scope exclusion: mobile traction batteries and pumped-hydro storage fall outside this assessment.

Segmentation Overview

- By Battery Type

- Lithium-ion (Lithium Iron Phosphate (LFP), Nickel-Manganese-Cobalt (NMC), Lithium Titanate (LTO))

- Lead-acid

- Flow Battery (Vanadium Redox, Zinc-Bromine)

- Sodium-ion

- Other Battery Technologies (NiCd, Hybrid Super-capacitors)

- By Connection Type

- On-Grid (Utility Interconnected)

- Off-Grid (Micro-Grid, Hybrid)

- By Component

- Battery Pack and Racks

- Power Conversion System (PCS)

- Energy Management Software (EMS)

- Balance-of-Plant and Services

- By Energy Capacity Range

- Below 10 MWh

- 10 to 100 MWh

- 100 to 500 MWh

- Above 500 MWh

- By End-user Application

- Utility

- Commercial and Industrial

- Residential

- By Geography

- Germany

- United Kingdom

- Italy

- France

- Spain

- Nordic Countries (Norway, Sweden, Denmark, Finland)

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed utility planners, battery integrators, and residential-solar installers across Germany, Italy, the United Kingdom, the Nordics, and Iberia. These conversations clarified typical system costs, evolving revenue stacks, and country-specific policy timelines, which we then mapped against secondary datapoints to close information gaps and validate model assumptions.

Desk Research

We drew on open datasets from Eurostat, ENTSO-E, and national transmission system operators for historical power flows and renewable curtailment levels, while studies by SolarPower Europe and the European Association for Storage of Energy provided installation statistics and policy trackers. Company 10-Ks, EPC tender documents, and regulator consultations offered price signals and pipeline visibility. Select paid collections, such as D&B Hoovers for supplier revenues and Dow Jones Factiva for deal flow, rounded out the evidence base. The sources named are illustrative, and many additional public and subscription materials were reviewed.

Market-Sizing & Forecasting

A top-down build began with annual installed power (MW) reported by TSOs, which we converted to energy (MWh) using average duration hours, and then to revenue through sampled ASPs gathered during interviews. Results were cross-checked with a bottom-up slice of supplier shipments and project announcements to refine totals. Key model drivers include lithium-ion cost curves, renewable penetration targets, balancing service prices, residential PV adoption, and interconnection queue attrition. Forecasts employ multivariate regression coupled with scenario analysis to project these drivers to 2030, after which sensitivity tests adjust for policy or supply-chain shocks.

Data Validation & Update Cycle

Outputs pass variance checks against historical capacity additions, exchange-rate movements, and inflation benchmarks. Senior analysts review anomalies before sign-off. The dataset is refreshed each year, with interim updates triggered by material events such as major capacity auctions or battery price swings, ensuring clients always access the latest view.

Why Mordor's Europe Battery Energy Storage System Baseline Earns Trust

Published market values often diverge; differing technology scopes, ASP assumptions, and update cadences typically sit at the heart of the gap.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.54 B (2025) | Mordor Intelligence | - |

| USD 18.10 B (2024) | Global Consultancy A | Includes non-battery technologies and uses global ASP averages |

| USD 11.80 B (2024) | Industry Research B | Excludes front-of-the-meter projects below 1 MW |

| USD 16.50 B (2023) | Trade Analytics C | Uses euro values without consistent currency conversion and older base year |

The comparison shows that once scopes and price bases are aligned, Mordor's balanced 2025 baseline sits midway between expansive and conservative estimates, giving decision-makers a dependable anchor built on clearly traceable variables and repeatable steps.

Key Questions Answered in the Report

How large is the Europe Battery Energy Storage Systems market in 2026?

The market is valued at USD 24.22 billion in 2026 and is forecast to reach USD 52.72 billion by 2031.

What CAGR is expected for battery storage deployments in Europe to 2031?

The market is projected to grow at a 16.84% CAGR over the 2026-2031 period.

Which battery chemistry leads European deployments?

Lithium-ion dominates with 87.8% installed share in 2025, though flow batteries are the fastest growing.

Why are corporate PPAs important for storage growth?

35% of European corporate PPAs now require co-located batteries to guarantee minimum delivery factors and manage imbalance risk.

What challenges do developers face when connecting new projects?

Grid-connection queues above 100 GW in major markets and evolving safety standards add delays and extra capex.

Which country is the fastest growing European battery market?

The United Kingdom is projected to expand at 22.2% through 2031, driven by long-term capacity and fast-reserve contracts.

Page last updated on: