Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

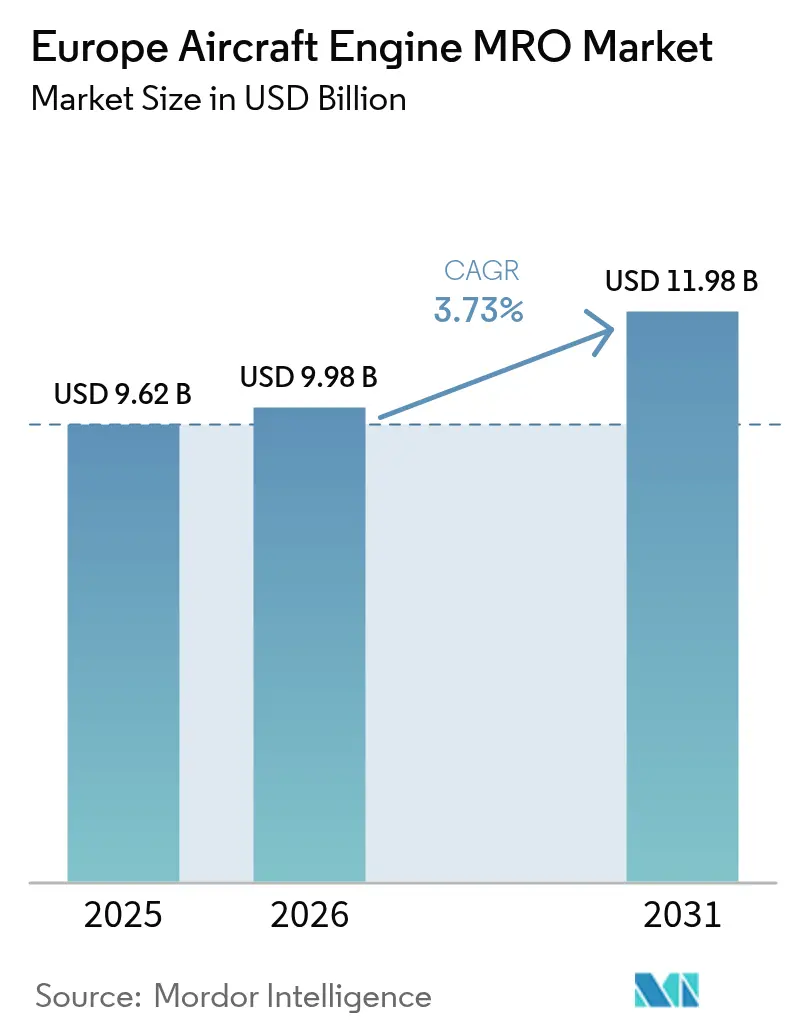

| Base Year Market Size (2025) | USD 9.62 Billion |

| Market Size (2026) | USD 9.98 Billion |

| Market Size (2031) | USD 11.98 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aircraft Engine MRO Market Analysis by Mordor Intelligence

Europe aircraft engine MRO market size in 2026 is estimated at USD 9.98 billion, growing from 2025 value of USD 9.62 billion with 2031 projections showing USD 11.98 billion, growing at 3.73% CAGR over 2026-2031. Growth is shaped by high leasing penetration, which tightens shop-visit intervals, sustained delivery backlogs that keep older engines in service, and the broader adoption of predictive maintenance, which compresses turnaround times. Independent providers are capitalizing on flexible time-and-materials contracts while OEM-affiliated shops expand capacity through licensing agreements and proprietary health-monitoring data. Spare engine lease rates are rising, signaling an operator's willingness to pay premiums to avoid aircraft-on-ground events, and EU funding for emissions retrofits is de-risking investment in next-generation propulsion maintenance. At the same time, labor shortages and life-limited part bottlenecks temper the overall expansion of the Europe aircraft engine MRO market.

Key Report Takeaways

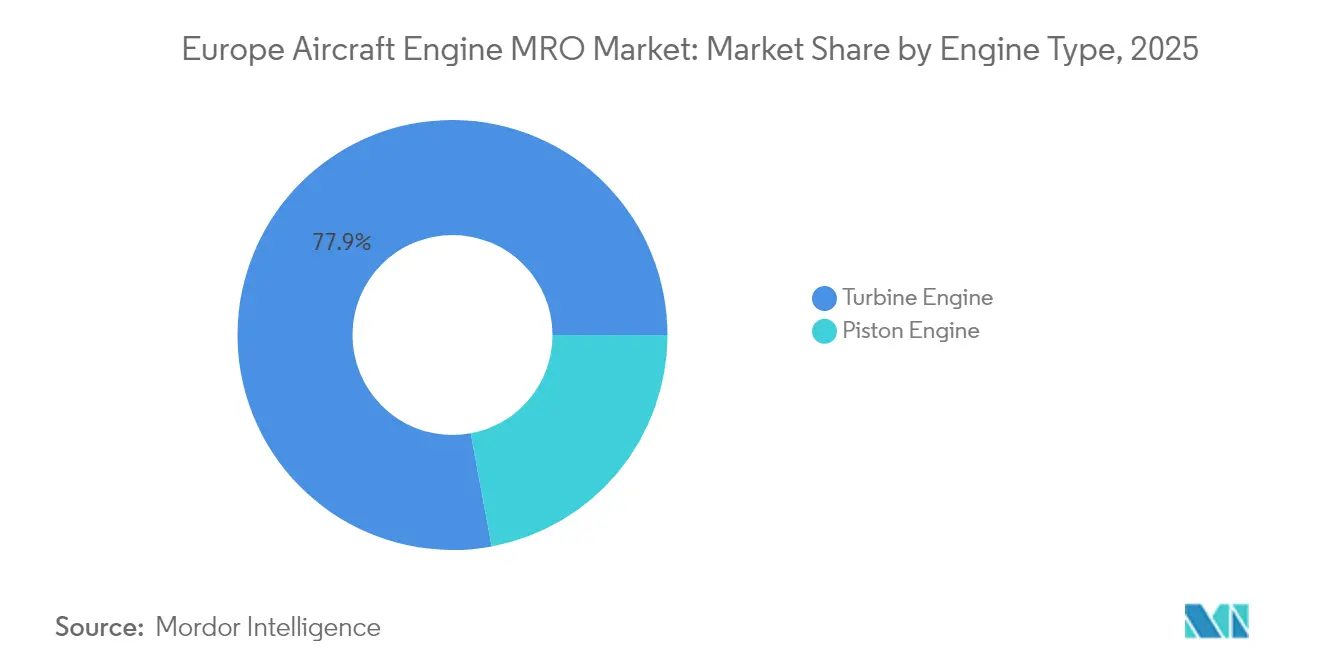

- By engine type, turbine engines held 77.92% of the Europe aircraft engine MRO market share in 2025, while the segment is expected to advance at a 4.39% CAGR through 2031.

- By aviation segment, commercial aviation accounted for 66.95% of the Europe aircraft engine MRO market size in 2025, whereas UAVs led growth at a 6.93% CAGR from 2026 to 2031.

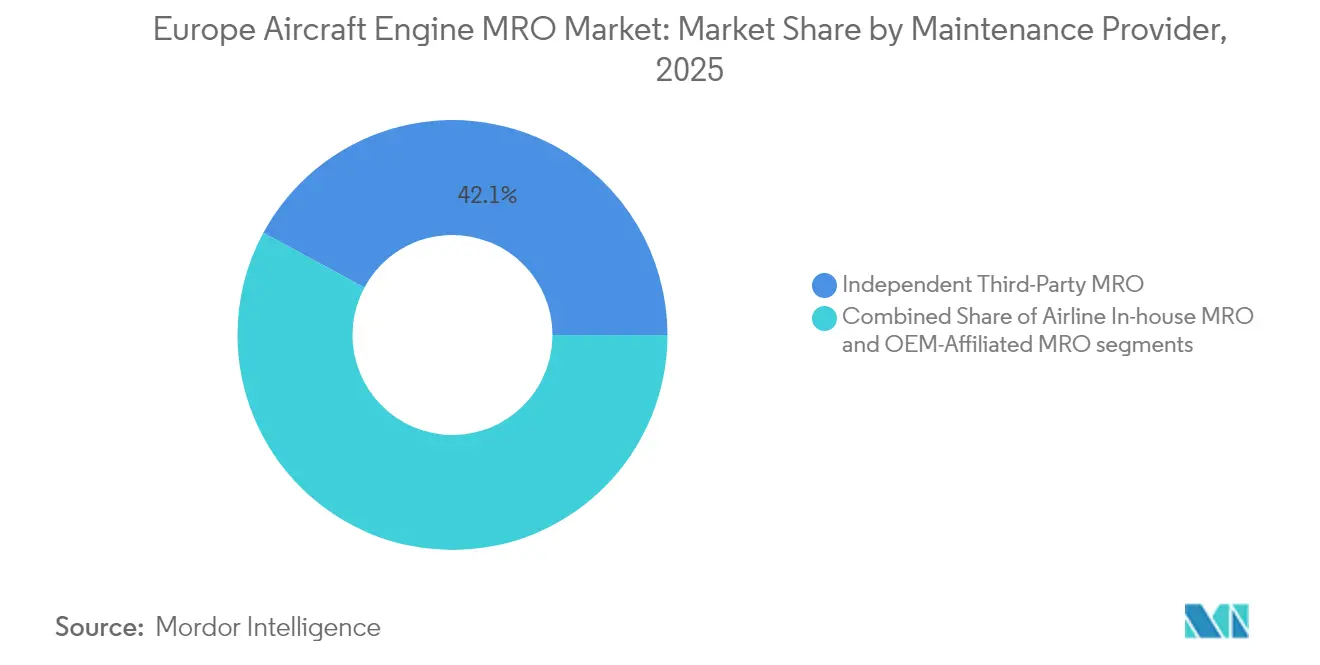

- By maintenance provider, independent third-party MROs captured a 42.12% share of the Europe aircraft engine MRO market in 2025; however, OEM-affiliated facilities are projected to record the highest CAGR at 4.96% through 2031.

- By geography, the United Kingdom led with 21.10% revenue share in 2025, while Spain posted the fastest regional CAGR at 5.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Aircraft Engine MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovery in flight hours and delivery backlogs increasing engine utilization | +1.2% | UK, Germany, France | Short term (≤ 2 years) |

| Ageing European aircraft fleets extending engine maintenance cycles | +0.9% | UK, Germany, France, Italy | Medium term (2-4 years) |

| Adoption of predictive maintenance and engine health monitoring systems | +0.6% | Frankfurt, Amsterdam, Paris hubs | Medium term (2-4 years) |

| EU funding programs supporting engine efficiency and emissions retrofits | +0.4% | EU | Long term (≥ 4 years) |

| Open-access LEAP and GTF MRO licensing expanding independent MRO capacity | +0.8% | Spain, Poland, Turkey | Short term (≤ 2 years) |

| Growing aircraft leasing and fleet transitions increasing shop visit frequency | +1.0% | Dublin, Amsterdam, Zurich | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recovery in Flight Hours and Delivery Backlogs Increasing Engine Utilization

Daily traffic across European airspace rebounded to 31,000 to 34,000 flights in 2024, representing 95% of the 2019 levels, and pushing engines to accumulate cycles faster than pandemic-era forecasts had anticipated. IBA projects that regional shop visits will increase from 2,500 in 2024 to more than 3,500 in 2025, a 40% rise that strains available capacity. Delivery backlogs exceeding 14,000 aircraft worldwide keep older engines, such as the CFM56-7B, in service, while early LEAP-1A fleets enter their first performance-restoration events. Spare-engine lease rates for CFM56-7B rose to USD 100,000 per month in 2024, signaling operators’ willingness to pay premiums to avoid aircraft-on-ground events.[1]Willis Lease Finance Corporation, “European Engine Market Analysis and Shop Visit Forecasts,” willislease.com

Ageing European Aircraft Fleets Extending Engine Maintenance Cycles

A large share of A320ceo and B737NG aircraft operating in Europe has exceeded 15 years of service, and nearly half of the installed CFM56 base had not yet reached a first shop visit as of early 2024. Rolls-Royce forecasts 1,100 to 1,200 large-engine shop visits annually through the mid-term, sustaining demand despite the introduction of new-generation deliveries. Older engines also suffer more unscheduled removals, illustrated by Lufthansa Technik’s 2025 uptick in surprise inductions, which further loads independent shops. Operators increasingly run end-of-lease assets to failure, transferring maintenance liability to lessors, who then source faster, lower-cost solutions.

Adoption of Predictive Maintenance and Engine Health-Monitoring Systems

GE Aerospace’s AI borescope tool cut inspection time from three hours to 90 minutes in 2024, allowing faster on-wing assessments and fewer precautionary removals. Lufthansa Technik’s AVIATAR now aggregates real-time data from over 100 operators, enabling the prediction of component failures up to 60 days in advance. The DLR-led PREDICT program, launched in 2025, focuses on non-destructive on-wing inspection for hydrogen and hybrid-electric engines. Meanwhile, MTU partnered with Teledyne to stream engine data via GroundLink Comm+. Condition-based interventions can extend time-on-wing 20 to 40%, yet when anomalies appear, they compress visit windows, creating lumpy demand patterns.

EU Funding Programs Supporting Engine Efficiency and Emissions Retrofits

The EU Clean Aviation Joint Undertaking awarded EUR 25 million (USD 29.30 million) in 2024 for next-generation turboshaft research and development, while Horizon Europe funds studies on the compatibility of SAF with in-service engines. NATO’s Defence Fund backed a modular 3,000-shp turboshaft concept that promises 30% lower maintenance labor. France’s DGA co-finances Safran’s new turboshaft family, with ground testing slated for 2026. Although focused on development, these programs accelerate the adoption of digital twins, additive repairs, and advanced coatings, which quickly migrate into MRO processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled EASA-certified maintenance personnel | −0.5% | Germany, UK, France | Medium term (2-4 years) |

| Supply-chain constraints in life-limited parts and forged components | −0.7% | France, UK | Short term (≤ 2 years) |

| Uncertainty around SAF certification and retrofit costs for legacy engines | −0.3% | EU | Long term (≥ 4 years) |

| High energy and utility costs increasing MRO operating expenses | −0.4% | Germany, UK, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled EASA-Certified Maintenance Personnel

EASA Part-66 licensure demands thousands of practical hours and multiple exams, creating a talent pipeline that cannot scale rapidly. Airbus forecasts that Europe will need 640,000 new technicians over the next 20 years.[2]Airbus, “Global Market Forecast and Technician Demand,” airbus.com MTU is spending EUR 150 million (USD 175.99 million) to automate processes and expand apprenticeships in Germany, yet still warns of throughput limits. StandardAero built an in-house mechanic academy in San Antonio, a model that European shops now emulate. High-pressure turbine blade repair and non-destructive testing roles remain the hardest to fill.

Supply Chain Constraints in Life-Limited Parts and Forged Components

Rolls-Royce booked GBP 410 million (USD 549.17 million) in 2023 contract-loss provisions tied to delays in titanium forgings for turbine disks and compressor blades. GE’s FLIGHT DECK initiative increased supplier on-time delivery above 90% in 2024; however, lead times for certain LEAP and GTF nozzles remain 18 to 24 months. OEMs are prioritizing new-engine production, forcing MRO shops to cannibalize used serviceable material or extend turnaround times. The constraint removes 0.7 percentage points from forecast growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Turbine Engines Anchor Aftermarket Revenue

Turbine engines generated 77.92% of Europe aircraft engine MRO market revenue in 2025 and are forecast to expand at a 4.39% CAGR through 2031, overtaking piston activity in absolute growth terms. Turbofans power the majority of narrowbody and widebody fleets, and LEAP shop visits are expected to triple by 2030. Hot and harsh operations compress on-wing life, further boosting demand. Safran and GE Aerospace are competing for next-generation turboshaft awards that will direct future MRO work to European hubs. Turbojet engines form a declining niche, while turboprops receive support from Avio Aero’s Catalyst program. OEM-affiliated shops specialize in high-margin performance-restoration work, whereas independents compete on price and faster turnaround times. Rolls-Royce recorded an 11.6% operating margin on GBP 7.3 billion (USD 9.77 billion) civil revenue in 2023, underscoring the advantage of scale in turbine aftermarket economics.

A residual 22.08% share comes from piston engines, which serve fragmented general aviation fleets and record limited growth. Their maintenance activity remains distributed among small regional shops and does not materially alter aggregate forecasts for the Europe aircraft engine MRO market. However, hybrid-electric projects currently under EU research funding could revive interest in small-displacement piston designs configured as range extenders, potentially opening up longer-term specialization opportunities.

By Aviation: Commercial Aviation Dominates, UAVs Scale Fastest

Commercial operators accounted for 66.95% of Europe aircraft engine MRO market value in 2025, driven by an installed base of more than 10,000 active aircraft. Narrowbody engines average higher daily utilization than widebodies, yet widebody shop visits deliver greater revenue per event, with Trent XWB overhauls exceeding USD 3 million. Regional jets powered by CF34-10 engines benefit from ITP Aero’s localized repair capabilities introduced in 2025. Military fleets, including Eurofighter Typhoon and F-135 engines, ensure steady throughput but slower growth.

UAVs are leading the relative expansion at a 6.93% CAGR, supported by EASA maintenance rules for engines with a mass exceeding 150 kg. Military UAVs, such as the MQ-9 and Eurodrone, require turboprop overhauls similar to those of manned aircraft, while emerging cargo drones collaborate with general aviation shops. The Europe aircraft engine MRO market, therefore, widens its scope to new propulsion classes and security-cleared facilities.

By Maintenance Provider Type: Independent Share Holds, OEM-Affiliated Capacity Accelerates

Independent providers retained a 42.12% share of the Europe aircraft engine MRO market sales in 2025, due to their multi-OEM capabilities and price flexibility. Still, OEM-affiliated shops advance at a 4.96% CAGR as manufacturers leverage proprietary data and service agreements to secure higher-margin work. GE Aerospace generated 70% of its USD 35 billion in 2024 turnover from aftermarket services, and Rolls-Royce TotalCare invoiced GBP 4.60 billion (USD 6.16 billion) in flying-hour receipts that same year. Airline in-house units face capital constraints and are increasingly outsourcing heavy maintenance visits while retaining line maintenance. StandardAero will ramp up LEAP capacity at its San Antonio site to meet demand from European carriers, signaling cross-regional service models that reinforce competition in the Europe aircraft engine MRO market.

Geography Analysis

The United Kingdom generated 21.10% of Europe's aircraft engine MRO market turnover in 2025, anchored by Rolls-Royce Derby and Dahlewitz, as well as GE Aerospace Wales. Rolls-Royce invested GBP 55 million (USD 73.63 million) in 2024 to expand Trent XWB assembly, and AerFin doubled quick-turn capacity at its new South Wales site in 2025. British providers benefit from regulatory expertise and closer proximity, but they face higher labor costs than those in Eastern Europe.

Spain represents the fastest-growing national segment at a 5.18% CAGR through 2031. ITP Aero posted EUR 1.61 billion (USD 1.89 billion) in revenue in 2024 and joined GE’s CF34-10 repair network in 2025, while Iberia Maintenance aligned with Honeywell on accessory repair. Italy, Switzerland, Turkey, and the Rest of Europe complete the regional landscape, with SR Technics, Turkish Technic, and Magnetic MRO scaling LEAP and Trent capabilities. Expansion trends confirm a multi-hub structure that disperses growth across the Europe aircraft engine MRO market.

Competitive Landscape

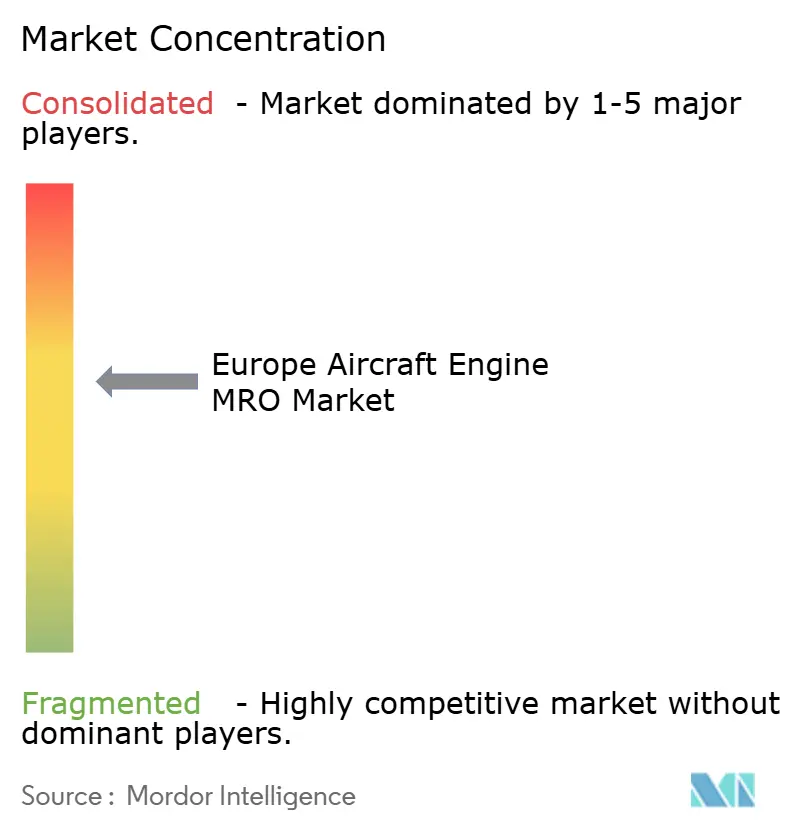

Five leading groups, Lufthansa Technik AG, Rolls-Royce Holdings plc, Pratt & Whitney (RTX Corporation), GE Aerospace (General Electric Company), and Safran SA, control the majority of the European aircraft engine MRO market revenue, indicating moderate concentration. OEMs leverage data platforms such as GE FLIGHT DECK, Rolls-Royce TotalCare, and AVIATAR to bind customers into long-term service agreements. Independent providers respond with aggressive test-cell investment, industrialized component repairs, and alliances that pool licensing rights. ST Engineering opened new LEAP lines in Singapore in 2025, and StandardAero is accelerating capacity to secure European contracts.

White-space opportunities lie in additive manufacturing, on-wing repairs, and hydrogen-ready maintenance. The DLR PREDICT program aims to cut shop-visit frequency by 30% through advanced inspection, while GE Additive deploys multi-laser printing for turbine parts. Digital marketplaces for spare engines, illustrated by Shannon Engine Support’s USD 875 million LEAP financing in 2024, enhance asset utilization and disrupt traditional slot-allocation models. Competitive intensity therefore rises, yet the Europe aircraft engine MRO market rewards scale, proprietary data, and diversified licensing portfolios.

Europe Aircraft Engine MRO Industry Leaders

Lufthansa Technik AG

Pratt & Whitney (RTX Corporation)

GE Aerospace (General Electric Company)

Safran SA

Rolls-Royce Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Swiss MRO provider SR Technics signed a long-term agreement with Safran Aircraft Engines for comprehensive overhaul and testing services of CFM International Leap-1A engines, ensuring operational reliability and performance.

- May 2025: Rolls-Royce secured a five-year contract with the UK MoD for EJ200 engine maintenance, ensuring the operational readiness of the Royal Air Force's Typhoon aircraft through comprehensive servicing and technical support.

- June 2023: TEISAS and GE Aerospace agreed to extend TEISAS's license to provide F110 depot-level maintenance services for several countries operating F16 and F15 fighter aircraft. The collaboration will further strengthen the relationship between TEI and its long-term partner, GE Aerospace, in the field of military engine services. TEI and GE Aerospace have successfully collaborated for many years and are now poised to play a critical role in supporting the F110 engine globally.

Europe Aircraft Engine MRO Market Report Scope

Maintenance, repair, and overhaul (MRO) is one of the key activities in an aircraft's and its engines' lifecycle. The typically long operational lifetimes of aircraft necessitate performing MRO activities to maintain their longevity in the long run. Engine maintenance, repair, and overhaul (MRO) involves the repair, servicing, or inspection of engines to ensure the safety and airworthiness of the aircraft in accordance with international standards.

The Europe aircraft engine MRO market is segmented based on engine type, aviation, maintenance provider type, and geography. The market is segmented by engine type into turbine engines and piston engines. By aviation, the market is classified into commercial aviation, military aviation, general aviation, and unmanned aerial vehicles (UAVs). The scope of the study for the UAVs is limited to military applications only. By maintenance provider type, the market is categorized into airline in-house MRO, independent third-party MRO, and OEM-affiliated MRO. By country, the market is segmented into the United Kingdom, Germany, France, Italy, Spain, Switzerland, and the Rest of Europe. The market sizing and forecasts have been provided in value (USD) for all the above segments.

By Engine Type

| Turbine Engine | Turboprop Engine |

| Turbofan Engine | |

| Turboshaft Engine | |

| Turbojet Engine | |

| Piston Engine |

By Aviation

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Vehicles (UAVs) |

By Maintenance Provider Type

| Airline In-house MRO |

| Independent Third-Party MRO |

| OEM-Affiliated MRO |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Switzerland |

| Rest of Europe |

| By Engine Type | Turbine Engine | Turboprop Engine |

| Turbofan Engine | ||

| Turboshaft Engine | ||

| Turbojet Engine | ||

| Piston Engine | ||

| By Aviation | Commercial Aviation | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military Aviation | Combat | |

| Transport | ||

| Special Mission | ||

| Helicopters | ||

| General Aviation | Business Jets | |

| Commercial Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| By Maintenance Provider Type | Airline In-house MRO | |

| Independent Third-Party MRO | ||

| OEM-Affiliated MRO | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Switzerland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe aircraft engine MRO market?

The Europe aircraft engine MRO market is valued at USD 9.98 billion for 2026 and is forecasted to reach USD 11.98 billion by 2031.

Which engine segment brings the most revenue?

Turbine engines generate 77.92% of market revenue and are growing at a 4.39% CAGR.

Which aviation category is expanding fastest?

UAVs lead growth at a 6.93% CAGR through 2031.

Why are OEM-affiliated MRO shops gaining share?

OEMs leverage proprietary health-monitoring data and licensing to win high-margin service agreements, driving a 4.96% CAGR for their facilities.

Which European country shows the highest growth rate?

Spain posts the fastest national expansion at a 5.18% CAGR, supported by ITP Aero and Iberia Maintenance investments.

What is the biggest restraint facing providers?

Shortages of EASA-certified technicians and persistent supply-chain delays in life-limited parts combine to reduce forecast CAGR by more than one percentage point.

Page last updated on: