Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

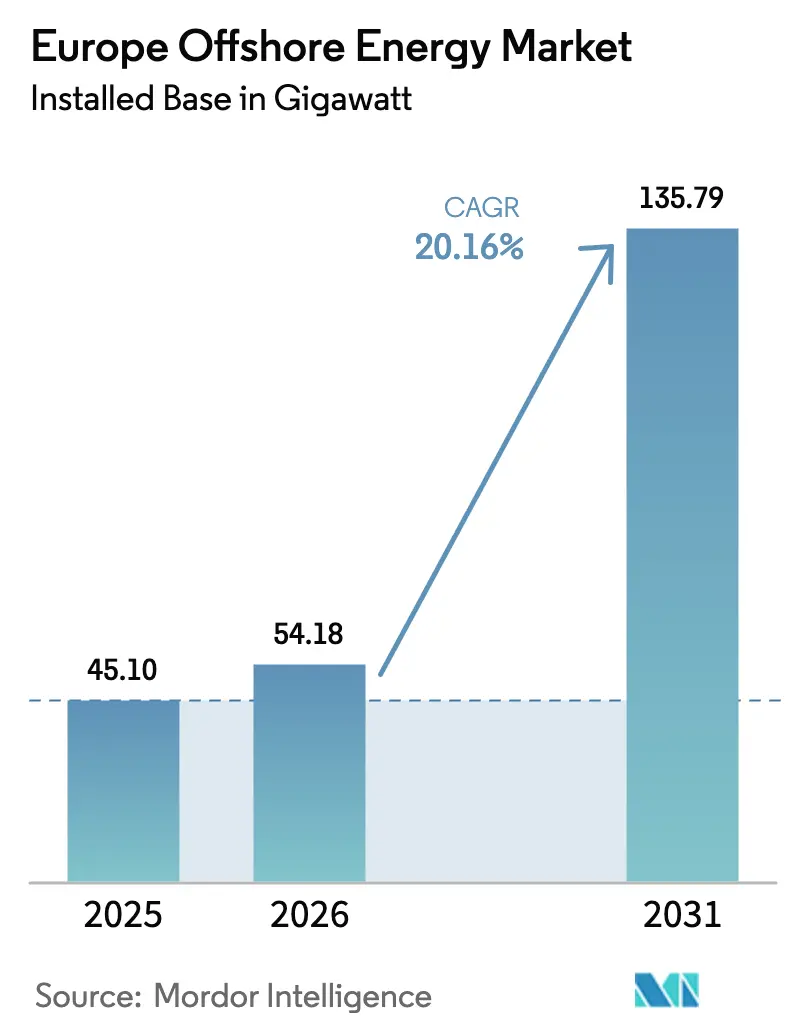

| Base Year Market Size (2025) | 45.10 gigawatt |

| Market Volume (2026) | 54.18 gigawatt |

| Market Volume (2031) | 135.79 gigawatt |

| Growth Rate (2026 - 2031) | 20.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Offshore Energy Market Analysis by Mordor Intelligence

Europe Offshore Energy Market size in 2026 is estimated at 54.18 gigawatt, growing from 2025 value of 45.10 gigawatt with 2031 projections showing 135.79 gigawatt, growing at 20.16% CAGR over 2026-2031.

This growth trajectory mirrors the European Union’s sharpened Green Deal ambitions, unprecedented policy visibility, and accelerating deployment of next-generation 15–20 MW turbines that compress development timelines and unlock deeper-water sites. Record additions of 4.2 GW in 2023 pushed wind’s contribution to 19% of the EU’s electricity mix, with a stated 35% target for 2030; policy mechanisms such as contracts for difference (CfDs) and expedited maritime spatial planning increase developer confidence, spur supply-chain investments, and lower the cost of capital. Developers also benefit from the REPowerEU program’s push for energy security, which has shifted offshore wind from 14% to 19% of Europe’s electricity mix in only two years and lifted output from 375 TWh to 466 TWh, while the Ostend Declaration commits nine North Sea states to 120 GW by 2030 and 300 GW by 2050. Technology momentum is equally striking: 5–10 MW turbines still dominate the water, but >15 MW units already anchor commercial orders such as Vestas’ 1,020 MW Nordlicht 1, positioning the European offshore energy market for scale-driven cost compression and higher capacity factors.

Key Report Takeaways

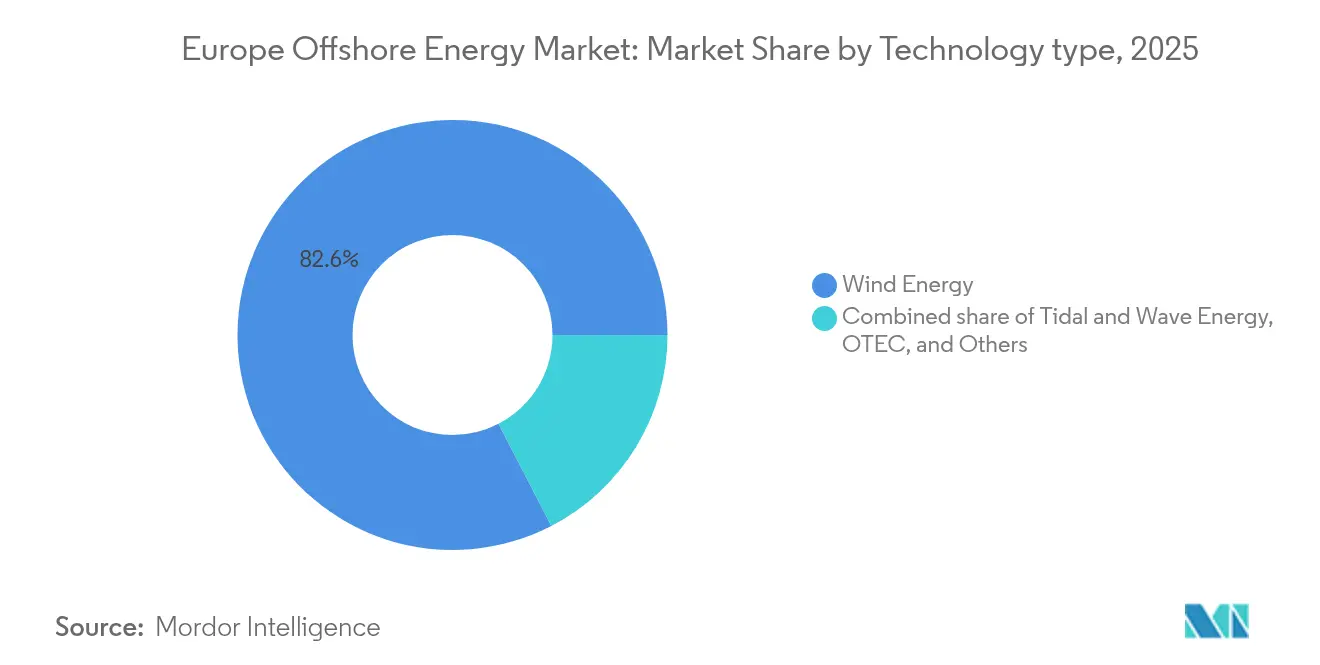

- By technology, wind energy led with 82.60% of the European offshore energy market share in 2025; its 21.34% CAGR keeps it the fastest-growing technology through 2031.

- By water depth, deep-water sites (Above 60 m) held 66.20% revenue share in 2025, while transitional 30 to 60 m zones are projected to expand at a 31.62% CAGR to 2031.

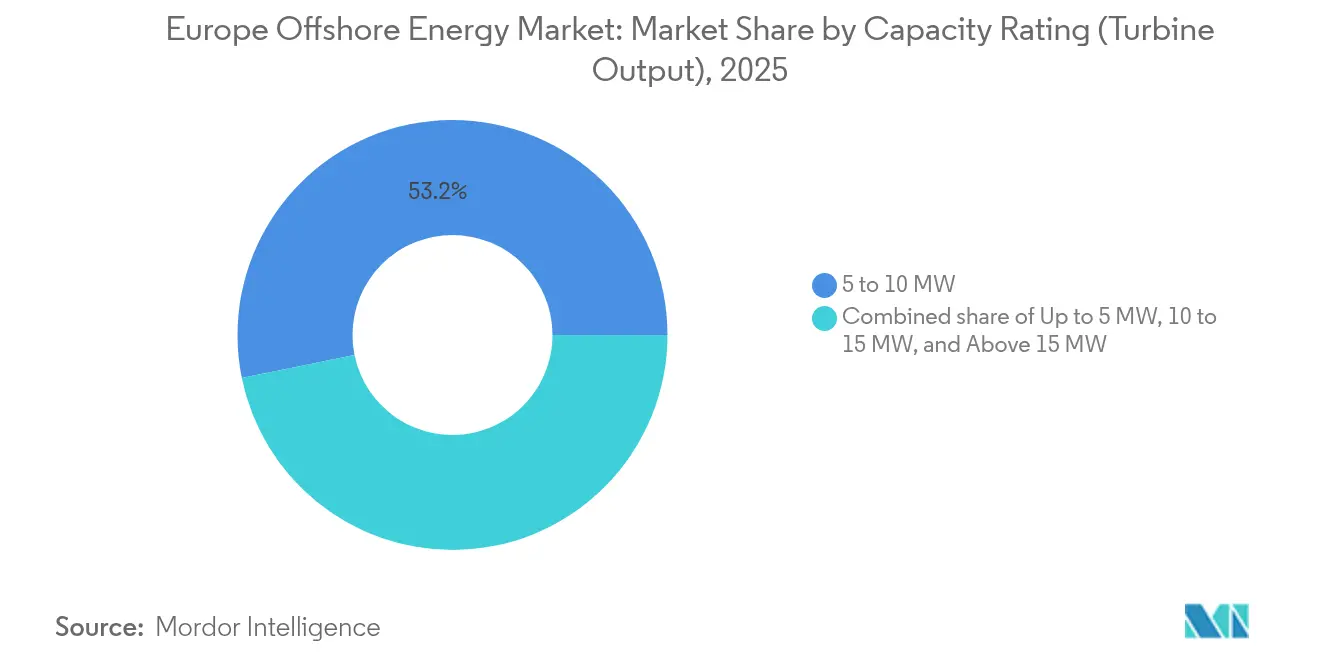

- By capacity rating, 5 to 10 MW turbines accounted for 53.20% of the European offshore energy market size in 2025; Above 15 MW units post the highest growth at 28.65% CAGR.

- By geography, the United Kingdom captured 44.30% of the European offshore energy market share in 2025, whereas Spain shows the fastest 23.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Offshore Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal-Driven Capacity Targets & National Offshore Auctions | +5.20% | Global, with primary focus on North Sea countries | Medium term (2-4 years) |

| Rapid Cost Declines in >15 MW Turbines Enabling Deep-Water Projects | +4.80% | North Sea, Atlantic, Mediterranean regions | Long term (≥ 4 years) |

| Green Hydrogen (Power-to-X) Demand for Offshore Wind Integration | +3.10% | Germany, Netherlands, Denmark, Sweden | Medium term (2-4 years) |

| Commercialisation of Floating Wind Unlocking Atlantic & Med Sites | +2.90% | Spain, France, Portugal, Italy | Long term (≥ 4 years) |

| Offshore Grid Interconnection & OFTO/HVDC Tender Pipeline | +2.70% | North Sea countries, Baltic region | Medium term (2-4 years) |

| Oil & Gas Platform Electrification & Decarbonisation Mandates | +2.10% | North Sea, primarily UK, Netherlands, Norway | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Green Deal-Driven Capacity Targets & National Offshore Auctions

Binding Green Deal legislation has set an 86–89 GW offshore target for 2030 and 356–366 GW for 2050, triggering a pan-European cascade of national auction calendars that give developers long-range visibility into seabed leases, CfD strike prices, and grid connections. France plans 10 GW of tenders by 2035, while Denmark’s latest round could power the nation’s electricity demand. Hornsea 3 in UK waters secured a GBP 37.35/MWh inflation-indexed CfD, demonstrating how policy certainty compresses financing costs and lowers bid pricing. Coupled with the REPowerEU “Accele-RES” digital permitting platform and the European Wind Charter signed by 26 countries, administrative bottlenecks are easing, evidenced by more than 20 competitive auctions across Europe in 2024 that collectively allocated over 55 GW of capacity.(1)European Commission, “REPowerEU: Planning and permitting reforms,” europa.eu

Rapid Cost Declines in Above 15 MW Turbines Enabling Deep-Water Projects

Commercial orders for 15 MW platforms, such as Vestas’ nod for Germany’s Nordlicht 1, illustrate that turbine scaling has crossed from prototype to bankable product class. These machines push capacity factors toward 70% in steady North Sea wind regimes and reduce foundation counts by up to 40% compared with 8 MW layouts, cutting installed cost per megawatt even after factoring recent steel volatility. Forward pipelines already feature 20 MW prototypes from European and Asian OEMs, indicating an entrenched trend. The remaining friction point lies with installation logistics: only a handful of jack-ups can manage nacelles weighing more than 1,200 tons, so shipbuilders must accelerate newbuild cycles over the next three years to prevent execution lags.

Green Hydrogen (Power-to-X) Demand for Offshore Wind Integration

Germany’s permitting of a 100 MW electrolyzer linked to RWE offshore capacity and Sweden’s Neptunus hub proposal reaffirm that green hydrogen is moving from concept to contract. The EU seeks 20 million tons of renewable hydrogen by 2030; offshore generation offers superior capacity factors and circumvents onshore grid congestion, with modular 500 MW “factory-in-a-box” concepts now standard in North Sea project feasibility studies. Offshore-to-hydrogen also aligns with industrial clusters requiring shipping-grade ammonia and green steel feedstock, opening a demand corridor that back-stops long-term power-purchase agreements for gigawatt-scale arrays.

Commercialisation of Floating Wind Unlocking Atlantic & Med Sites

Floating foundations open an estimated 4,000 GW of European offshore potential. Spain’s maritime plan reserves 19 zones for up to 3 GW by 2030; France awarded Europe’s first commercial-scale floating tender in the Mediterranean in 2024, and Ocean Winds’ 250 MW project signals private-sector conviction(2)Ocean Winds, “250 MW Mediterranean floating award,” oceanwinds.com. With levelized energy costs in Spain’s Canary Islands at 100–135 EUR/MWh, floating is already cost-competitive in high-resource sites that fixed monopiles cannot reach. Platform standardisation, industrialised hull fabrication, and hybrid mooring systems are expected to trim costs by another 30% by 2035, bringing floating on par with shallow-water monopiles even before carbon pricing adjustments.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Heavy-Lift Vessel Availability for Next-Gen Turbines | -3.70% | Global, with acute impact on North Sea and emerging markets | Short term (≤ 2 years) |

| Supply-Chain Inflation in Steel & Rare-Earth Components | -2.40% | Europe-wide, with particular impact on manufacturing hubs | Medium term (2-4 years) |

| Lengthy Permitting & Coastal Visual-Impact Opposition | -2.10% | Coastal regions across Europe, particularly Germany and UK | Medium term (2-4 years) |

| Offshore Grid Congestion & Limited On-shore Landing Points | -1.80% | North Sea countries, Baltic region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Heavy-Lift Vessel Availability for Next-Gen Turbines

Only 15–20 heavy-lift units worldwide can erect above 15 MW turbines, and day rates jumped 75% between 2022 and 2024, echoing the tight LNG carrier market a decade ago. Developers with legacy charters—Ørsted, RWE, Vattenfall—have locked in multiyear slots, leaving newer entrants to scramble or delay. Financing a newbuild costs USD 400 million and can take three years; cumulative capex of USD 14.8 billion is needed to bridge the fleet gap. Until then, schedule slips risk eroding auction bid economics, especially in emerging markets like Spain, where floating pilots hinge on vessel availability.

Supply-Chain Inflation in Steel & Rare-Earth Components

Escalating costs for critical offshore wind components, particularly steel foundations and rare-earth permanent magnets, have driven project investment costs to USD 3,523/kW in early 2024 while threatening the economic viability of projects awarded under previous auction price assumptions. Steel price volatility significantly affects monopile foundations, with specialized heavy plate steel for offshore applications commanding premium pricing due to quality requirements and a limited supplier base. Ørsted's memorandum of understanding with Dillinger for lower-emission steel demonstrates industry efforts to secure supply while meeting decarbonization criteria, though the transition to green steel production methods initially increases costs by 55-60% compared to conventional processes. Rare-earth elements essential for permanent magnet generators face supply concentration risks, with China controlling 80% of global processing capacity and export restrictions potentially disrupting European turbine manufacturing. The Netherlands' projected failure to meet offshore wind targets stems partly from supply chain constraints, while Germany's North Sea output declined 9% in 2023 due to grid infrastructure limitations exacerbating component delivery delays. Industry responses include vertical integration strategies, regional supplier development programs, and alternative material research, yet near-term cost pressures persist as demand growth outpaces supply chain expansion capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Wind Energy Dominates Renewable Transition

Wind energy accounted for 82.60% of the European offshore energy market size in 2025 and is pacing a 21.34% CAGR through 2031, far outstripping tidal and wave pilots that remain pre-commercial. Despite recent input inflation, its installed base benefits from two decades of learning curves, bankable performance histories, and fully amortised supply chains that drive down per-unit costs. The wider policy ecosystem anchors its lead: North Sea states align seabed grants with dedicated grid build-outs, while developers secure CfDs at sub-40 EUR/MWh prices that keep merchant exposure low. Though technically promising in Atlantic gateways, tidal and wave technology still confront higher levelized costs and limited OEM competition; demonstration units such as Magallanes Renovables’ floating tidal platform post 45% capacity factors but lack the multi-sourcing that de-risks procurement. Ocean Thermal Energy Conversion projects remain confined to warmer equatorial waters, leaving European waters outside their economically viable envelope. Consequently, the European offshore energy market continues to channel the vast majority of capital toward wind build-outs, cementing its prominence through 2031.

The spread of technology also reveals an accelerating pivot to floating sub-segments within wind. Spain, France, and Portugal are aligning industrial roadmaps with floating prototypes that marry serial hull fabrication techniques to modular topside assemblies, aiming at sub-100 EUR/MWh price points by mid-decade. These cost curves rely on standardised anchor systems and lightweight composite blades that mitigate port draft constraints. Wave and tidal advocates nonetheless draw policy attention for grid-balancing attributes: multiple governments now include technology-neutral innovation pots in auction designs, offering floor revenues that could lift niche renewables to 5% market share after 2030. Until then, wind remains the default investment choice, supported by mature O&M contracting structures and insurance products that protect lenders from weather-related downtime.

By Water Depth: Transitional Zone Drives Fastest Expansion

Installations anchored in more than 60 m of water captured 66.20% of the European offshore energy market 2025 as multi-GW projects such as Dogger Bank leveraged rich wind seams far offshore. Yet the 30-60 m transitional band is projected to log a 31.62% CAGR to 2031, acting as the sweet spot where fixed-bottom economics intersect with improved wind yield. Developers exploit this window to deploy new 15 MW turbines while avoiding the cost and technical leap required for floating foundations. Transitional-depth projects also benefit from existing vessel capability: conventional jack-ups can still install foundations without the keel clearance challenges faced in deep water. Moreover, grid interconnection distances remain manageable, containing cable expenditure and reducing transmission losses.

Policy designs amplify this trend. Several North Sea lease rounds explicitly segment sites at 40-55 m depths to synchronise auctioned acreage with current vessel capacity and OEM supply limits, creating a pipeline that eases the industry’s learning curve toward deeper water. Shallow sites under 30 m, once the prime real estate for early offshore wind, now face pushback from coastal stakeholders who cite visual intrusion and tourism impacts. As those areas approach saturation, repowering becomes their main growth lever, using taller towers on existing monopiles. Deep-water prospects beyond 60 m will regain momentum once floating substructures reach industrial maturity, but until then, the transitional band remains the European offshore energy market’s volume star.

By Capacity Rating: Turbine Scaling Accelerates Market Evolution

Turbines rated 5-10 MW represented 53.20% of the European offshore energy market in 2025, reflecting their proven deployment economics and compatibility with today’s jack-up fleets. However, machines exceeding 15 MW are poised for a 28.65% CAGR and will dominate new FIDs by 2027 as OEM roadmaps and financing norms converge around fewer, larger rotors. A 15 MW turbine can displace two 8 MW units, trimming array cable length, foundations, and O&M visits; levelized cost reductions of 25-30% are already documented in comparative project models. Direct-drive architectures also eliminate gearbox maintenance, extending design life toward 30 years.

OEM competition feeds this leap. Vestas, Siemens Gamesa, and GE Vernova each have 15-17 MW prototypes moving through type certification, while Chinese entrants accelerate to 18-20 MW to win export share. Yet supersized hardware drives secondary challenges: rotor diameters exceeding 250 m demand blades longer than football pitches, necessitating new logistic corridors and factory footprints. Port upgrades across the North Sea and Baltic form an invisible but essential part of the capacity-rating shift, and public-sector grants have begun underwriting quayside reinforcements to preserve regional manufacturing competitiveness. Despite the hype, the 10-15 MW class offers a comfort zone for financiers wary of unproven mechanical loads in above 15 MW machines. Developers hedging technology risk often pair a tranche of mid-range turbines with a smaller batch of flagships, sweetening lenders’ risk appetites while capturing some scale efficiencies. Over time, experience curves will normalise above 15 MW reliability metrics, after which that rating band is expected to become the European offshore energy market’s default specification.

Geography Analysis

The United Kingdom remained the epicentre of the European offshore energy market in 2025, holding 44.30% market share on the back of 11 GW operational capacity and a 100 GW pipeline that spans fixed and floating archetypes. Projects such as the 2.9 GW Hornsea 3 and the multistage Dogger Bank complex demonstrate how phased development strategies smooth supply-chain peaks and sustain local manufacturing jobs. Germany, the Netherlands, and Denmark collectively add another 35.40% through coordinated North Sea Energy Cooperation targets, though grid congestion shaved 9% off German output in 2023, highlighting the parallel need for offshore backbone upgrades. Norway leverages its oil-and-gas pedigree for floating ventures like Equinor’s Hywind Tampen, the world’s largest floating array feeding petroleum platforms directly, offering a template for decarbonising hard-to-abate sectors.

Southern Europe provides the breakout narrative. Spain posts the fastest 23.08% CAGR through 2031 as Maritime Spatial Planning earmarks 19 floating zones, and the first competitive auction slated for 2025 paves the regulatory road. Atlantic wind speeds, deep-water shelf edges, and fewer fishing-ground conflicts give Spain’s floating pipeline cost advantages over crowded North Sea shallows. France likewise accelerates, with 10 GW of tenders locked into a multi-annual schedule that has already awarded both fixed-bottom and floating concessions in the Mediterranean. Italy and Portugal follow, using hybrid solar-wind zones to de-risk port upgrades and stimulate local steel fabrication clusters.

The Baltic Sea is transforming from fringe theatre to a growth pole. Poland, Sweden, and Finland push combined gigawatt-scale projects such as Ørsted-PGE’s 1.5 GW Baltica 2 and Vattenfall’s 2.5 GW Korsnäs concept, driven by net-zero mandates and energy-security priorities in the wake of geopolitical tensions. Further east, emerging Adriatic markets like Croatia tender their first blocks, offering early entrants preferential grid quotas and streamlined licensing. This geographical diversification underpins the wider European offshore energy market by spreading weather risk, reducing single-basin dependency, and fostering competition among ports and yard facilities.

Competitive Landscape

Market structure skews toward a tiered hierarchy. Ørsted, RWE, Equinor, and Vattenfall anchor the top tier with vertically integrated portfolios exceeding 40 GW at operational, construction, or consented stages, giving them procurement muscle and vessel access advantages. Their strategies increasingly hinge on supply-chain integration: Ørsted’s steel offtake pact with Dillinger secures low-carbon heavy plate, while RWE’s joint venture with Norges Bank Investment Management unlocks patient capital aligned with sovereign decarbonisation goals(5)Energy Global, “RWE–NBIM joint venture announcement,” energyglobal.com. Equinor extends hydrocarbon know-how into floating wind moorings, and Vattenfall uses integrated onshore-to-offshore PPA offerings to bundle power with green-hydrogen contracts.

Mid-tier players—TotalEnergies, Shell, Iberdrola, SSE Renewables, and Statkraft—leverage balance-sheet heft but balance renewables against legacy businesses. They often partner with infrastructure funds or pension capital seeking long-dated cash flows; for example, Ørsted carved out a 12.45% slice of four UK wind farms to Brookfield for GBP 1.745 billion in 2024, recycling capital into new growth. Floating specialists such as Ocean Winds and Principle Power carve niches with proprietary platforms they license into developer consortia, while regional independents like Parkwind ride public-private alliances to secure local content advantages.

Competitive intensity rises in vessel procurement, blade manufacturing, and HVDC export systems. Aker Solutions and Siemens Energy secured full notice to proceed on the 2.8 GW Norfolk Vanguard build-out in early 2025, underscoring EPC contractors’ role in derisking mega-projects. Meanwhile, the merger between Saipem and Subsea7 into “Saipem7” adds a EUR 43 billion backlog to the installation arena, potentially lowering per-day vessel rates through fleet pooling economies. Overall, the European offshore energy market rewards scale, technology partnerships, and early spatial-planning engagement, while entrants lacking vessel slots or turbine supply agreements face steep barriers.

Europe Offshore Energy Industry Leaders

Siemens Gamesa Renewable Energy SA

Vestas Wind Systems AS

Hydroquest

Ørsted AS

E.ON SE.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vattenfall has made the final investment decision to build the Nordlicht 1 and 2 offshore wind farms in the German North Sea, with Nordlicht 1 set to become the largest offshore wind project in Germany.

- March 2025: RWE and Norges Bank Investment Management (NBIM) have finalized a transaction where NBIM acquired a 49% stake in RWE's Nordseecluster and Thor offshore wind projects for approximately EUR 1.4 billion.

- February 2025: Saipem and Subsea7 have agreed to merge, creating a new entity named Saipem7 with a combined backlog of EUR 43 billion. This merger aims to establish a global leader in the energy services sector, combining their expertise and resources.

- January 2025: Aker Solutions and Siemens Energy have received full notice to proceed with the 2.8 GW Norfolk Vanguard offshore wind farm project, following a limited notice received in November 2023. This project is part of RWE's Norfolk offshore wind zone, which will be capable of powering over 4 million households.

Europe Offshore Energy Market Report Scope

Offshore renewable energy is defined as the electricity generated from ocean-based resources, such as wind turbines located offshore in the oceans and Great Lakes, along with marine energy sources, such as waves, tides, salinity, and thermal properties. Projects utilizing ocean resources are considered offshore. For example, a tidal generator located at a river's mouth is considered offshore since it utilizes ocean tides to generate electricity.

The European Offshore Energy Market is Segmented by Technology (Wind Energy, Wave Energy, Tidal Stream, Ocean Thermal Energy Conversion (OTEC), and Other Technology Types) and Geography (United Kingdom, Germany, Netherlands, Denmark, Norway, and Rest of Europe). The report offers the installed capacity and forecasts in capacity (GW) for all the above segments.

By Technology

| Wind Energy |

| Tidal and Wave Energy |

| Ocean Thermal Energy Conversion (OTEC) |

| Other Technologies |

By Water Depth

| 0 to 30 m (Shallow) |

| 30 to 60 m (Transitional) |

| Above 60 m (Deep-water) |

By Installation Type (Qualitative analysis only)

| Fixed Foundation (includes Monopile, Jacket, Gravity-based) |

| Floating Platform (Semi-submersible, Spar-Buoy, Tension-Leg Platform) |

By Component (Qualitative analysis only)

| Turbine |

| Substructure and Foundation |

| Electrical Infrastructure |

| Sub-sea Cables |

| Mooring and Anchoring Systems |

| Control and Monitoring |

By Capacity Rating (Turbine Output)

| Up to 5 MW |

| 5 to 10 MW |

| 10 to 15 MW |

| Above 15 MW |

By Geography

| United Kingdom |

| Germany |

| Netherlands |

| Denmark |

| Norway |

| France |

| Belgium |

| Sweden |

| Ireland |

| Rest of Europe |

| By Technology | Wind Energy |

| Tidal and Wave Energy | |

| Ocean Thermal Energy Conversion (OTEC) | |

| Other Technologies | |

| By Water Depth | 0 to 30 m (Shallow) |

| 30 to 60 m (Transitional) | |

| Above 60 m (Deep-water) | |

| By Installation Type (Qualitative analysis only) | Fixed Foundation (includes Monopile, Jacket, Gravity-based) |

| Floating Platform (Semi-submersible, Spar-Buoy, Tension-Leg Platform) | |

| By Component (Qualitative analysis only) | Turbine |

| Substructure and Foundation | |

| Electrical Infrastructure | |

| Sub-sea Cables | |

| Mooring and Anchoring Systems | |

| Control and Monitoring | |

| By Capacity Rating (Turbine Output) | Up to 5 MW |

| 5 to 10 MW | |

| 10 to 15 MW | |

| Above 15 MW | |

| By Geography | United Kingdom |

| Germany | |

| Netherlands | |

| Denmark | |

| Norway | |

| France | |

| Belgium | |

| Sweden | |

| Ireland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected size of the Europe offshore energy market by 2031?

The Europe offshore energy market size is forecast to reach 135.79 GW by 2031, expanding at a 20.16% CAGR during the forecast period (2026-2031).

Which country currently holds the largest share of installed offshore capacity in Europe?

The United Kingdom led with 44.30% of the Europe offshore energy market share in 2025, reflecting more than 11 GW in operation.

Why are above 15 MW turbines considered game-changers for offshore wind economics?

Larger turbines cut the number of foundations and electrical hookups per megawatt, pushing capacity factors toward 70% and lowering levelized costs by up to 30% versus 8 MW models.

How will floating wind technology influence future European installations?

Floating foundations unlock deep Atlantic and Mediterranean waters, adding an estimated 4,000 GW of potential and are expected to achieve cost parity with fixed-bottom solutions by 2035.

What are the main constraints facing near-term offshore build-out?

Limited heavy-lift vessels for next-generation turbines and inflation in steel and rare-earth materials are the two most immediate bottlenecks, together shaving roughly 6% off projected CAGR.

Page last updated on: