Embroidery Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.7 Billion |

| Growth Rate (2026 - 2031) | 6.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

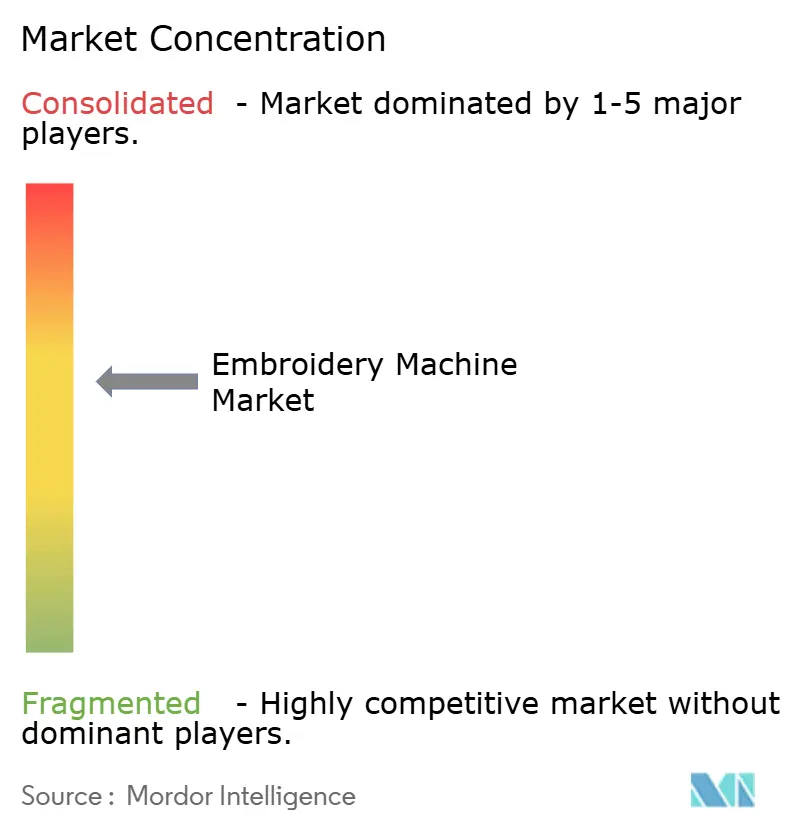

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embroidery Machine Market Analysis by Mordor Intelligence

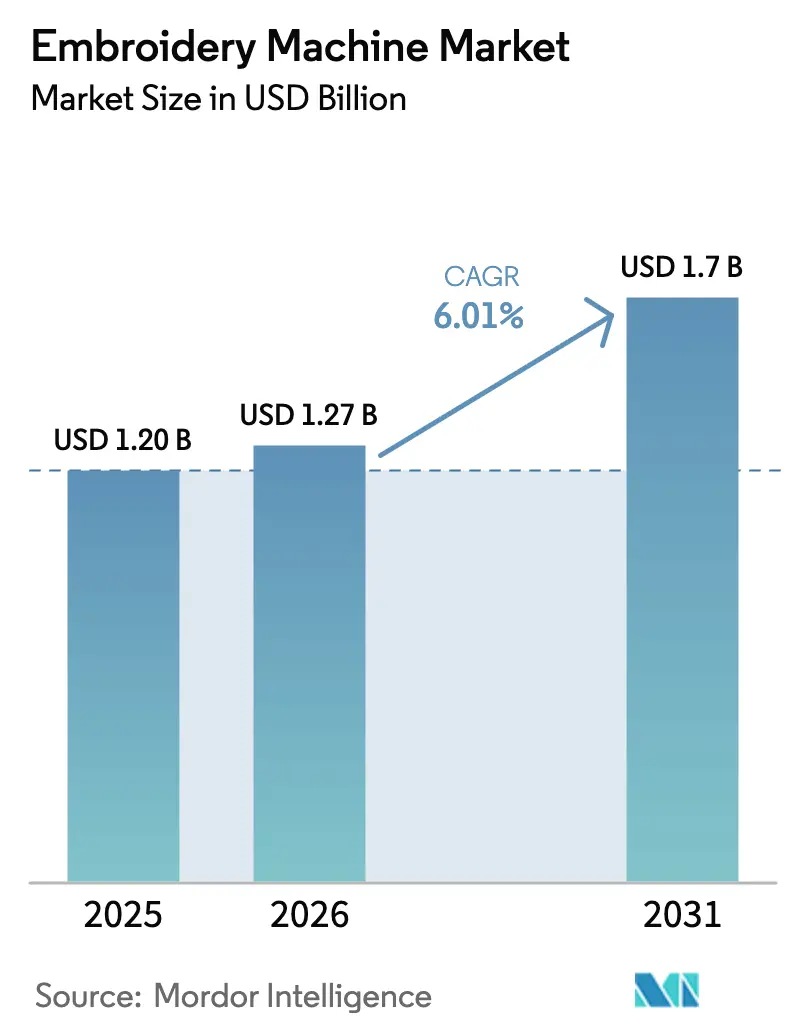

The Embroidery Machine Market size is expected to increase from USD 1.20 billion in 2025 to USD 1.27 billion in 2026 and reach USD 1.7 billion by 2030, growing at a CAGR of 6.01% over 2026-2030.

Generative-AI auto-digitizing compresses design lead-times, EU carbon-tariff rules redirect decorators from screen-printing to thread-based logos, and IIoT-enabled uptime guarantees shorten automation payback periods, so both high-throughput multi-head systems and agile single-head units find addressable demand. North American fan-merch operators choose 10-needle machines to monetize new Name, Image, and Likeness (NIL) opportunities, while Asia-Pacific contract factories deploy lights-out floors that keep stitchers running overnight without human supervision. Government green-equipment rebates covering IE4/IE5 servo motors lower operating costs in Japan and South Korea, and OEMs increasingly bundle evergreen firmware to ease small-business fears of controller obsolescence. Collectively, these forces provide a balanced demand mix that insulates the embroidery machine market from cyclical apparel swings.

Key Report Takeaways

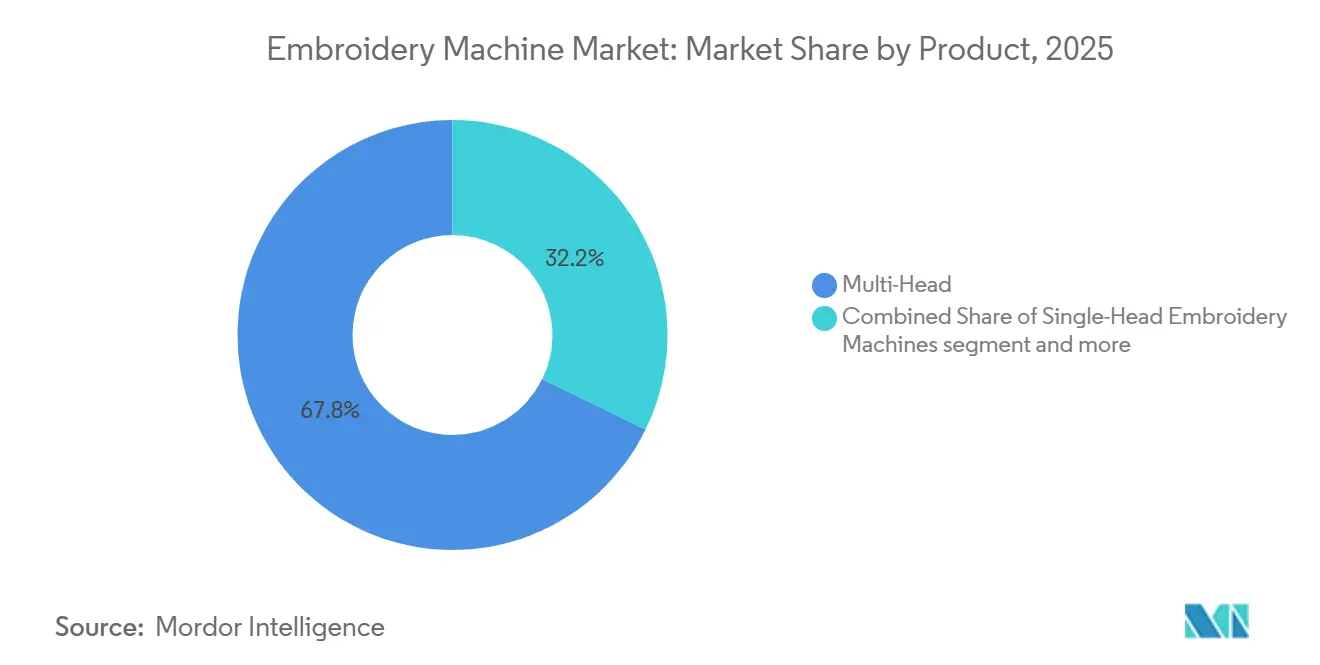

- By product type, multi-head machines led with 67.75% of the embroidery machine market share in 2025, and single-head machines are the fastest-growing product type at an 8.25% CAGR through 2031.

- By technology, computerized technology commanded 64.65% of the embroidery machine market size in 2025, and is set to advance at a 7.75% CAGR during 2026-2031.

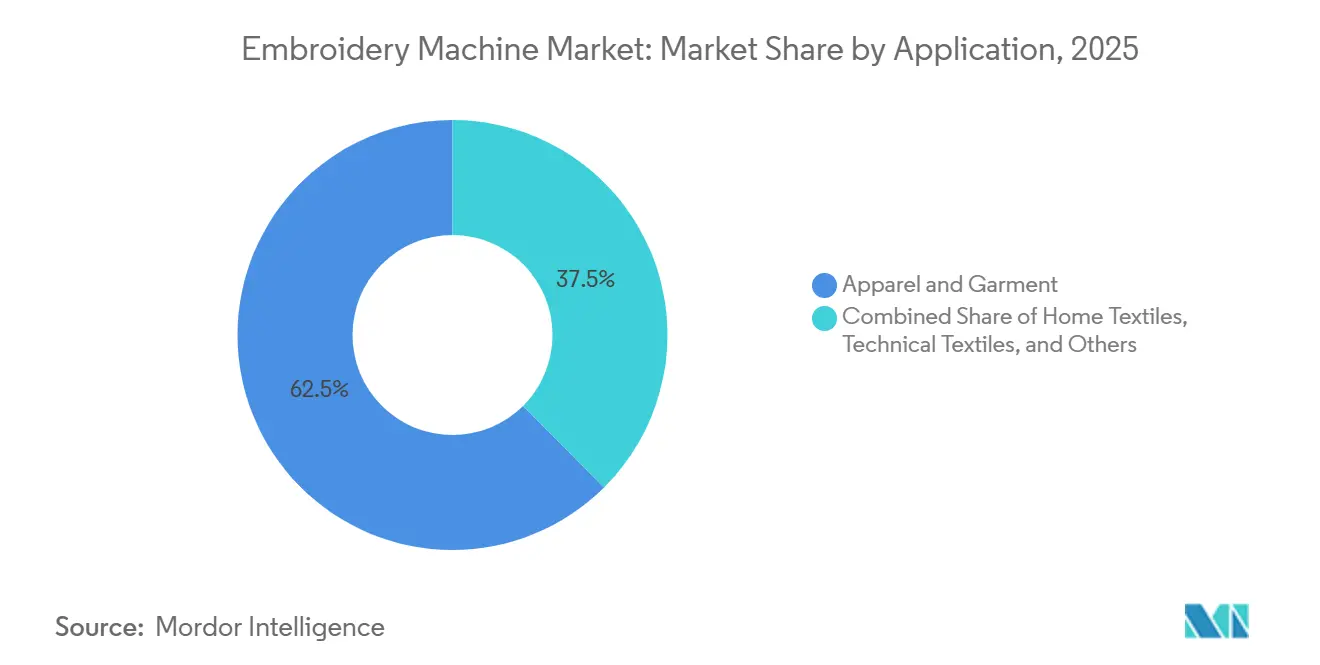

- By application, apparel and garments maintained 62.45% of the embroidery machine market size in 2025; technical textiles posted the highest forecast growth at 9.2% CAGR to 2031.

- By end-user, industrial users delivered 65.55% of the embroidery machine market share in 2025, whereas home and hobbyist buyers will expand at a 7.05% CAGR during 2026-2031.

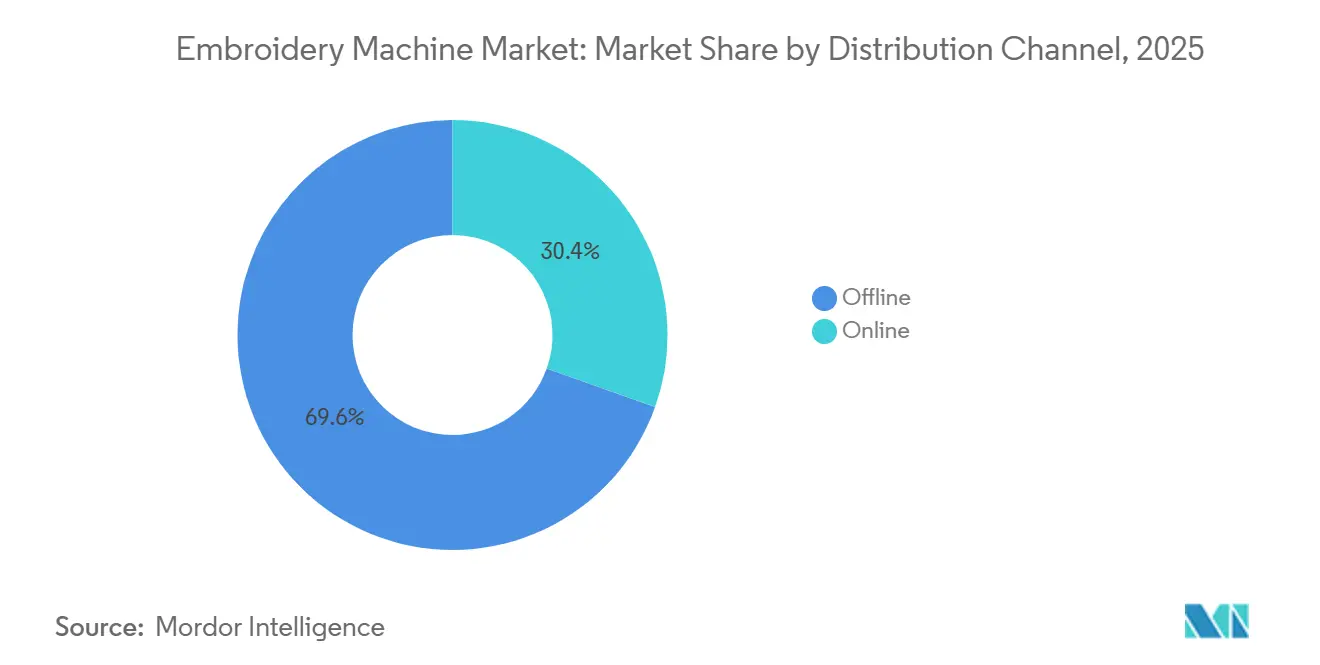

- By distribution channel, offline delivered 69.55% of the embroidery machine market share in 2025, whereas online will expand at a 7.25% CAGR during 2026-2031.

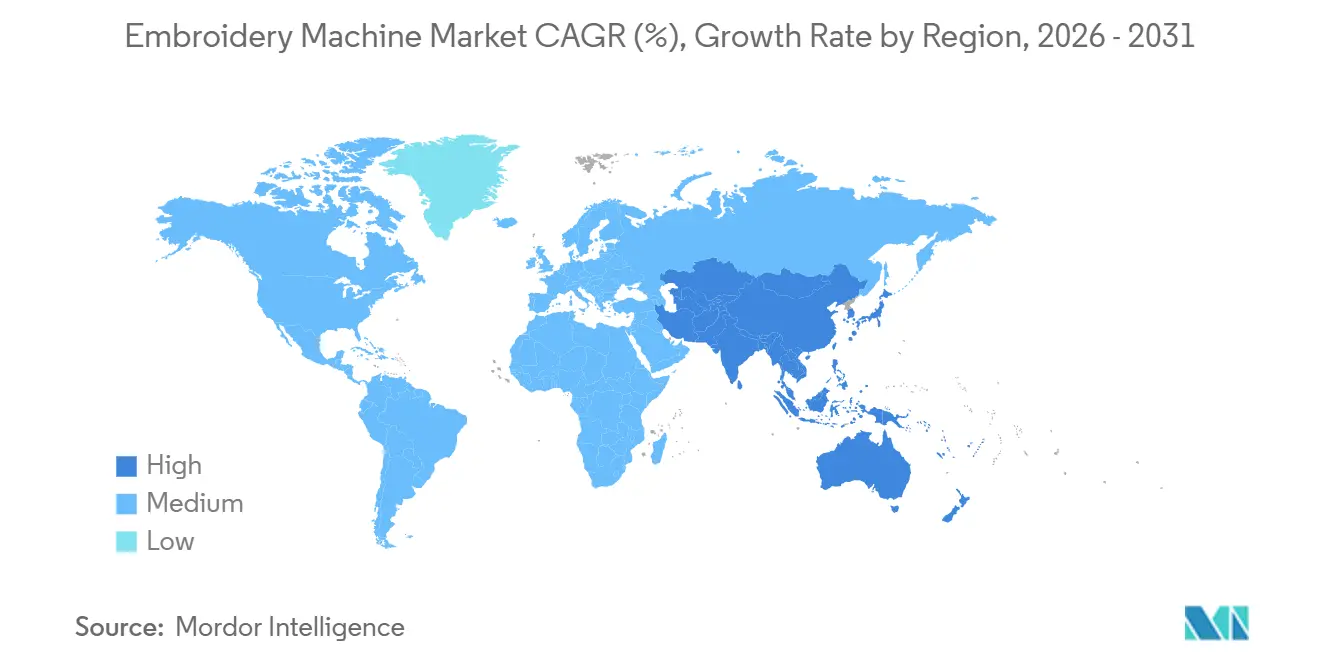

- By geography, Asia-Pacific captured 62.55% of the embroidery machine market size in 2025, and is expected to grow at a 7.45% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Embroidery Machine Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI auto-digitizing cuts design time for custom DTC brands | +1.3% | North America & EU | Short term (≤ 2 years) |

| Indian e-commerce real-time personalization spikes single-head shipments | +1.1% | India, with early adoption in Southeast Asia | Short term (≤ 2 years) |

| EU CBAM carbon tariffs shift decorators from screen-print to thread logos | +0.9% | EU core, spill-over to UK & EFTA | Medium term (2-4 years) |

| IIoT predictive maintenance lowers downtime in Chinese contract factories | +0.8% | China, expanding to Vietnam & Bangladesh | Medium term (2-4 years) |

| US NIL expansion to high-school sports boosts fan-merch 10-needle demand | +0.7% | United States, regional concentration in Texas & California | Short term (≤ 2 years) |

| Government green-equipment rebates for high-efficiency servo motors | +0.6% | Japan & South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generative-AI Auto-Digitizing Cuts Design Time for Custom DTC Brands

Generative models now translate customer artwork into optimized stitch files in minutes, replacing the 2-4-hour manual workflow that once bottlenecked small apparel houses. Early field data show 87% design-match accuracy and up to 30% lower rework, which supports the 48-hour order-to-ship promises that differentiate direct-to-consumer sellers. Rapid design iteration also lets brands bundle personalization without charging a premium, lifting average order value by roughly one-fifth. As software moves to subscription models, OEMs collect recurring revenue and continuously improve algorithms, adding a cloud moat that discourages price-based churn. Near-term buyers cite AI digitizing as a top three purchase criterion, overtaking needle count and field size.

Indian E-Commerce Real-Time Personalization Spikes Single-Head Shipments

Indian marketplaces introduced real-time preview engines that let shoppers upload photos and generate mock-ups before checkout, collapsing batching economics and making single-head flexibility indispensable. GST incentives that classify embroidery at a 12% tax rate widen the margin compared with screen-printed goods, allowing micro-entrepreneurs to break even in under nine months. Unit imports priced below USD 5,000 surged throughout 2025, representing the fastest expansion in the embroidery machine market.[1]Ministry of Trade, Industry and Energy, “Energy Efficiency Standards,” MOTIE.GO.KR Software localization in Hindi, Tamil, and Bengali further lowers adoption barriers, while same-day courier networks in Tier 2 cities supply threads and stabilizers within 24 hours. Early adopters report daily volumes of 20 to 25 bespoke orders, proving the cash-flow logic for the segment.

EU CBAM Carbon Tariffs Shift Decorators from Screen-Print to Thread Logos

Full CBAM enforcement in 2028 will tax high-carbon decoration methods, raising the delivered cost of PVC-ink screen prints by 8-12% versus embroidery’s lower emission profile.[2]European Commission, “Carbon Border Adjustment Mechanism,” EUROPA.EU European uniform and hospitality buyers already embed Scope 3 clauses in contracts, so decorators must pivot or forfeit orders. Finance teams model a 24-month payback on multi-head units when carbon credits are included, which shortens the investment hurdle for small firms. Machine vendors respond by publishing third-party life-cycle assessments that quantify CO₂ savings, giving procurement departments auditable evidence to justify capex. Over time, embroidery’s regulatory advantage is expected to narrow the cost gap with print alternatives, especially on large batch runs.

IIoT Predictive Maintenance Lowers Downtime in Chinese Contract Factories

Sensor kits that track needle temperature and vibration stream data to cloud dashboards where AI flags anomalies 72 hours before failure, trimming unplanned stoppages by nearly half. Contract manufacturers running 18-hour shifts convert every hour gained directly into billable output, so ROI on IIoT retrofits falls below one year. Global buyers now request overall equipment effectiveness (OEE) logs during supplier audits, rewarding plants that maintain more than 80% OEE with bonus volumes. Chinese OEMs embed the analytics layer at factory gate pricing, eroding the service-contract premium long held by Japanese rivals. As uptake spreads to Vietnam and Bangladesh, IIoT readiness will likely emerge as a supplier qualification norm.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid DTF printers cannibalize promo-product embroidery in APAC | -0.9% | APAC, concentrated in China & Southeast Asia | Medium term (2-4 years) |

| EU apparel spending slowdown delays capex refresh cycles | -0.7% | EU core, with spillover to UK | Short term (≤ 2 years) |

| Skilled-operator shortage persists across NA & EU despite upskilling grants | -0.6% | North America & EU | Long term (≥ 4 years) |

| Rapid controller-software obsolescence raises perceived investment risk for SMEs | -0.5% | Global, acute in markets with fragmented vendor support | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid DTF Printers Cannibalize Promo-Product Embroidery in APAC

As Direct-to-Film consumable costs drop, APAC promo suppliers shift roughly one-third of volume to hybrid printers that transfer full-color graphics at USD 0.65 per logo versus USD 1.80 for thread. Entry-level embroidery shops lacking scale struggle to defend share where tactile quality is less valued, particularly on caps, totes, and conference giveaways. Machine makers respond by introducing combo heads that embroider and print in one pass, but adoption is nascent due to higher ticket prices.[3]JUKI Corporation, “G-Series Hybrid Embroidery Machines,” JUKI.CO.JP Over the medium horizon, embroidery must reposition as a premium finish for high-value or technical items to avoid further share erosion.

EU Apparel Spending Slowdown Delays Capex Refresh Cycles

Inflation-adjusted apparel spend contracted 2.3% in 2025, pushing machine replacement from a seven-year norm toward a decade. Cash-strapped decorators choose patch repairs over new purchases, which tempers near-term unit growth yet inflates demand for spare parts and field service. Leasing penetration below 20% in Southern Europe leaves buyers reliant on self-financed capex, magnifying deferral incentives. OEMs address the gap by marketing trade-in programs with deferred first payments, but take-up remains limited. Unless consumer confidence rebounds quickly, European shipments may lag global averages through 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Single-Head Machines Capture Micro-Batch Momentum

Despite accounting for only a small fraction of 2025's revenue, single-head machines are projected to achieve the highest growth rate among all product classes, with an anticipated CAGR of 8.25%. Micro-batch economics favor their sub-5-minute setup times, eliminating the idle windows that penalize multi-head gear on one-off orders. A single-head unit processing 20 daily jobs often yields higher ROA than a 6-head station locked into three long runs. Brother’s PR1055X camera-guided alignment feature trims material waste by up to 15%. Multi-head platforms remain indispensable for 500-unit contract runs, so the embroidery machine market balances efficiency at both volume extremes.

Chenille and sequin machines remain niche, enticing varsity-jacket and luxury-textile producers seeking tactile differentiation. Laser appliqué hybrids occupy bespoke decor where mixed-media techniques can justify 30% price premiums. Product diversity therefore enables OEMs to hedge against fashion cyclicality, helping stabilize the embroidery machine industry despite demand swings in any single segment.

By Technology: Computerized Systems Extend Their Lead

Fully automatic equipment owned 64.65% of the 2025 turnover and should widen its share as computer-vision sensors and AI path planners shave downtime. Lights-out Chinese floors run unattended graveyard shifts at up to 1,000 stitches per minute, proving the throughput upside. Retrofit kits costing USD 2,500 convert semi-automatic lines to partial autonomy, a stopgap for cost-sensitive buyers. Manual machines continue in haute-couture ateliers where human imperfection signals artisanal luxury to end consumers.

Semi-automatic gear makes sense in wage-advantaged markets such as Bangladesh, while computerized lines dominate regions where labor averages USD 10/hour or more. Because automation savings compound each year, computerized shipments are projected to grow 7.75% annually, outstripping the broader embroidery machine market size expansion.

By Application: Technical Textiles Accelerate on Lightweight Mandates

Apparel drove 62.45% of revenue in 2025, yet carbon-fiber preforms, medical sutures, and airbag reinforcements give technical textiles a 9.2% growth runway. Automotive OEMs replace woven inserts with embroidered stitches that save 200-300 g per vehicle, supporting emissions targets. Aerospace composite firms cite 18-22% tensile-strength gains from oriented thread layups. Higher complexity demands machines priced USD 40,000-80,000 multiples of apparel-grade units lifting average selling price and bolstering the embroidery machine market size.

Home textiles and promotional goods grow steadily but face substitution risk from hybrid DTF print. Corporate uniforms and hospitality linens benefit from CBAM, encouraging screen-print replacements. The shifting mix toward technical work raises skill requirements, nudging OEMs to bundle advanced training with each sale.

By End-User: Hobbyists Democratize Stitching

Industrial plants still accounted for 65.55% of global shipments in 2025, but hobbyists and side-hustlers buying sub-USD 1,000 equipment expand at a 7.05% CAGR. USB connectivity and cloud pattern libraries mirror 3-D printing’s learning curve collapse, letting weekend operators earn USD 500-800 monthly via Etsy or local fairs. Commercial shops with fewer than 10 heads act as a bridge, servicing school and small-business accounts with four-day turnarounds. Some hobby operators graduate to commercial-grade multi-heads, showing mobility across tiers that complicates discrete segmentation.

Technical schools and maker spaces add incremental demand by incorporating embroidery modules into broader digital-fabrication curricula. As firmware updates arrive over Wi-Fi, even casual owners stay current without costly board swaps, lowering lifetime ownership anxiety.

By Distribution Channel: Online Direct Sales Gain Ground

Dealers and specialty stores captured 69.55% of 2025 spend thanks to installation and service packages. Yet OEM web-shops grow 7.25% per year by bundling AR configurators and software subscriptions, keeping 28-32% margin versus 18-22% through resellers. Amazon and Alibaba list thousands of SKUs, eroding price opacity but commoditizing mid-tier models. Big-box retailers still move seasonal bulk 12,000-plus entry units each holiday period in North America alone, suggesting physical display remains relevant at lower price points.

Manufacturers walk a tightrope between owning the customer relationship and preserving partner goodwill. Hybrid channel policies directed at enterprise accounts, dealers for SMEs, are becoming the norm, though conflicts persist when discounting online undercut showroom pricing.

Geography Analysis

Asia-Pacific anchored 62.55% of 2025 turnover and should grow at a 7.45% CAGR, led by China’s 180,000-unit installed base and India’s single-head boom. Guangdong, Zhejiang, and Jiangsu clusters exploit co-located suppliers that shrink turnaround to 72 hours. IIoT penetration rose sharply post-2024, with OEE gains of 13 percentage points convincing buyers to standardize on sensor-ready machines. India differs: real-time personalization converts small orders into immediate dispatch, so single-head share tops 55% of domestic sales. Government rebates on IE4 motors in Japan and South Korea accelerate replacement rather than incremental units, while Australia remains niche, focused on sports customization.

North America relies on NIL-driven high-school merch to sustain growth. Texas and California alone captured nearly 40% of 2025 U.S. demand; Canada sells mainly into resource-sector uniforms that specify flame-resistant logos. Mexico’s maquiladoras enjoy USMCA tariff relief that pulls embroidery closer to U.S. retail shelves, albeit at lower margins.

Europe remains bifurcated. Western Europe pursues replacement anchored to CBAM compliance, making multi-head upgrades attractive for corporate-uniform suppliers. Eastern Europe expands net capacity, leveraging lower labor aboard EU duty-free access. Southern regions struggle with soft apparel spend, lengthening machine life cycles to as much as 10 years. Nordic buyers need reflective thread for safety wear, a small but steady niche. Middle East growth centers on luxury linens for new hotels, whereas Africa’s penetration stays low outside South Africa and Nigeria.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

The embroidery machine market is moderately concentrated. Brother, Tajima, Barudan, and JUKI draw on decades-long installed bases and lucrative consumables streams. German stalwarts ZSK and PFAFF price at 40-50% premiums for sub-millimeter accuracy required in technical textiles. Chinese challengers such as Zhejiang Lejia and Shanghai Feiyue undercut established brands by 25-30% while reaching 80-85% of performance ratings, pressing mid-tier Japanese players. Swiss and U.S. names Bernina, Ricoma, and Melco target prosumers, offering bundled webinars and design libraries that flatten the learning curve.

Strategically, vendors emphasize automation, AI path planning, smart hoops, vision-based tension control, servitization, predictive-maintenance subscriptions, and evergreen firmware; and vertical integration, thread, software, and e-commerce storefronts. Patent activity clusters around hybrid DTF-plus-embroidery heads and RFID hoops that auto-pull prior setups, signaling future convergence of decoration technologies. As retrofit kits stretch machine life, OEMs must balance retrofit revenue against cannibalized new-unit sales.

Embroidery Machine Industry Leaders

Brother Industries, Ltd

Bernina International AG

Janome Sewing Machine Co., Ltd.:

Tajima Industries Ltd.

ZSK Stickmaschinen GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Brother Industries debuted the PR1100e multi-needle model featuring an AI design assistant that slashes digitizing time to under 10 minutes

- December 2025: Barudan secured ISO 14001 certification for its Ogaki factory, aligning with EU Scope 3 supplier requirements.

- November 2025: ZSK Stickmaschinen and Siemens integrated MindSphere IIoT analytics into RACER machines for predictive maintenance.

- October 2025: Melco introduced the Amaya Bravo 16-needle line with vision-guided placement to cut fabric waste 15% .

Global Embroidery Machine Market Report Scope

An embroidering machine is a machine used to create decorative designs or patterns on fabric using different types of stitches and colors of thread. Embroidery machines are often used to add intricate and individualized details to clothing, linens, and other fabrics.

The report provides a comprehensive background analysis of the embroidery machine market, covering current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. Additionally, the COVID-19 impact has been incorporated and considered during the study.

The embroidery machine market is segmented by type (free motion embroidery machine, Cornely hand-guided embroidery machine, computerized embroidery machine (single-head embroidery machine, multi-head embroidery machine, Schiffli embroidery machine), end user (residential, commercial), distribution channel (online and offline), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America).

The report offers market size and forecasts for the embroidery machine market in value (USD) for all the above segments.

| Single-Head Embroidery Machines |

| Multi-Head Embroidery Machines |

| Chenille Embroidery Machines |

| Others (Sequin, Laser, Cap/Flat, etc.) |

| Manual Embroidery Machines |

| Semi-Automatic Machines |

| Fully Automatic/Computerized Machines |

| Apparel & Garments |

| Home Textiles |

| Technical Textiles (Auto, Medical, Aero) |

| Others (Fashion Accessories, Corporate Branding & Uniforms, Promotional Products, etc,) |

| Home/Personal Use (Residential / Hobbyist) |

| Commercial/Small Business Use (less than 10 machines) |

| Industrial Use (≥10 machines) |

| Others (vocational training, Fashion/ design schools) |

| Offline (Direct, Dealers, Specialty, Big-Box) |

| Online (OEM Direct, E-commerce) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product | Single-Head Embroidery Machines | |

| Multi-Head Embroidery Machines | ||

| Chenille Embroidery Machines | ||

| Others (Sequin, Laser, Cap/Flat, etc.) | ||

| By Technology | Manual Embroidery Machines | |

| Semi-Automatic Machines | ||

| Fully Automatic/Computerized Machines | ||

| By Application | Apparel & Garments | |

| Home Textiles | ||

| Technical Textiles (Auto, Medical, Aero) | ||

| Others (Fashion Accessories, Corporate Branding & Uniforms, Promotional Products, etc,) | ||

| By End-User | Home/Personal Use (Residential / Hobbyist) | |

| Commercial/Small Business Use (less than 10 machines) | ||

| Industrial Use (≥10 machines) | ||

| Others (vocational training, Fashion/ design schools) | ||

| By Distribution Channel | Offline (Direct, Dealers, Specialty, Big-Box) | |

| Online (OEM Direct, E-commerce) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the embroidery machine market be in 2031?

The embroidery machine market size is forecast to reach USD 1.70 billion by 2031, growing at a 6.01% CAGR from 2026.

Which product type is growing the fastest?

Single-head units post the strongest outlook at an 8.25% CAGR because they excel at one-off, personalized orders.

Why is Asia-Pacific so dominant?

The region holds over 60% share due to China’s lights-out factories and India’s e-commerce personalization surge, both of which require large machine volumes.

What technology trend most influences new purchases?

Fully computerized systems with AI-driven digitizing and IIoT sensors are displacing semi-automatic models thanks to higher throughput and lower downtime.

How do EU carbon tariffs affect demand?

CBAM raises the cost of screen-printed imports, pushing European decorators toward embroidery to avoid 8-12% margin erosion.

Are hobbyist buyers significant?

Yes, sub-USD 1,000 entry machines enable side-hustlers to monetize customized designs, expanding the buyer base beyond traditional factories.

Page last updated on: