Circular Knitting Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

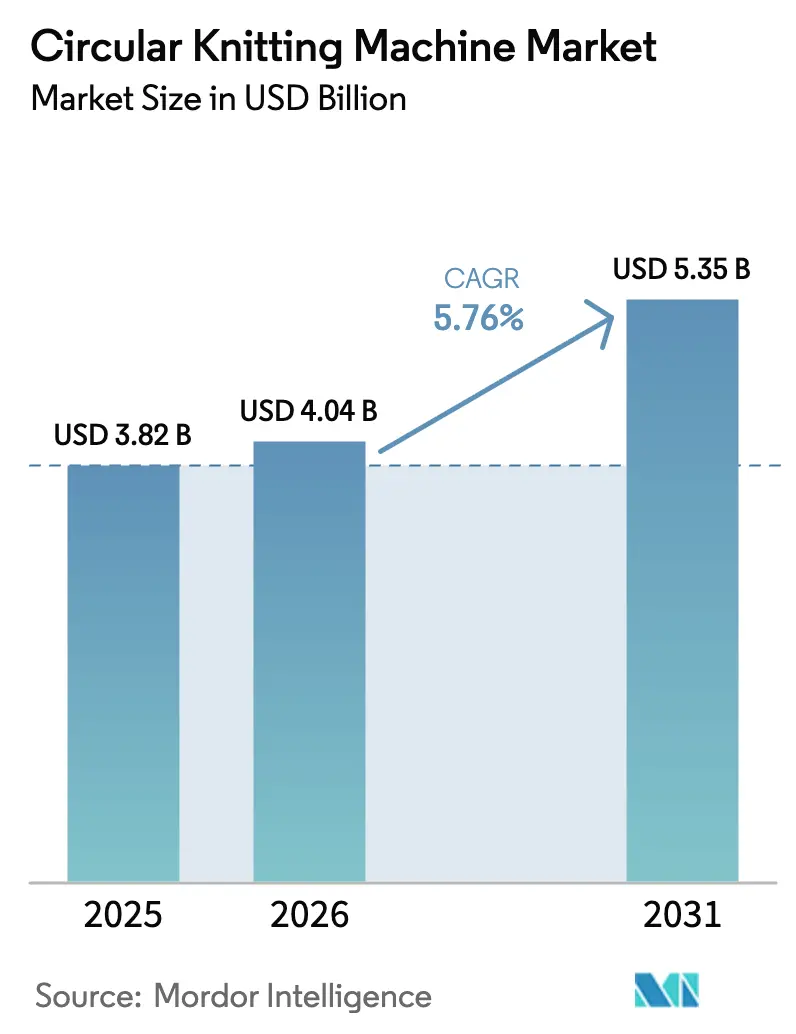

| Market Size (2026) | USD 4.04 Billion |

| Market Size (2031) | USD 5.35 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

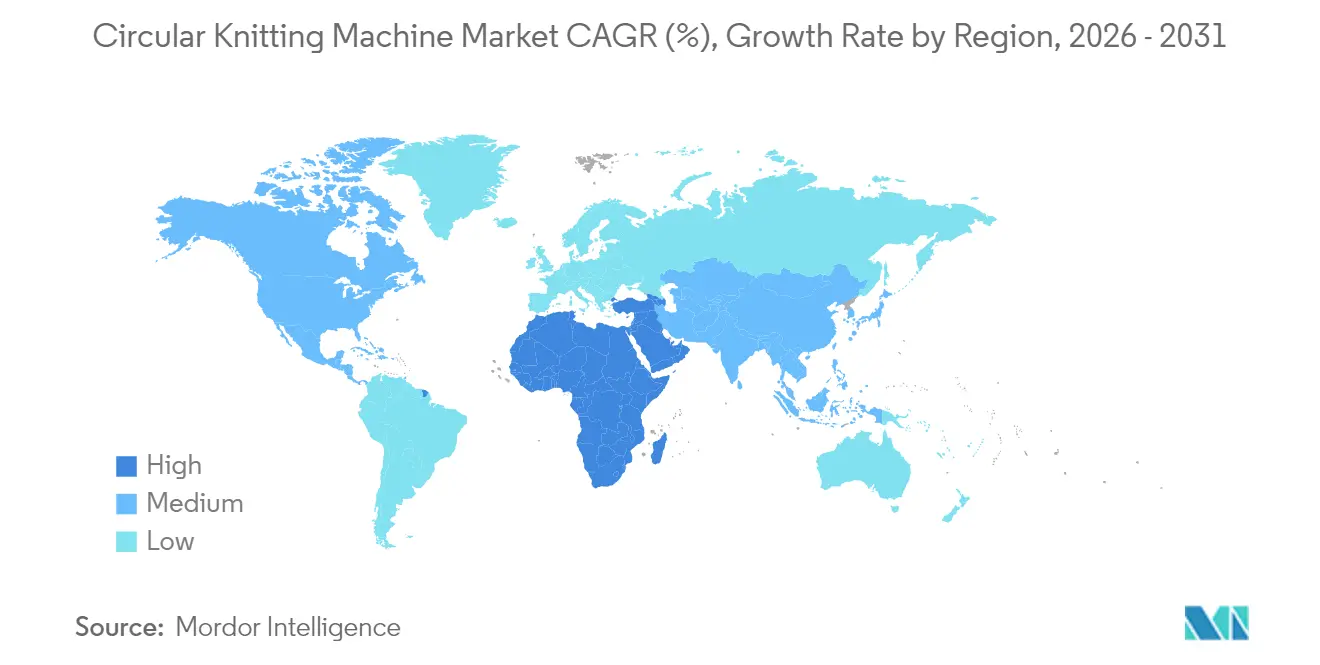

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Circular Knitting Machine Market Analysis by Mordor Intelligence

The circular knitting machines market size is expected to grow from USD 3.82 billion in 2025 to USD 4.04 billion in 2026 and is forecast to reach USD 5.35 billion by 2031 at 5.76% CAGR over 2026-2031. Healthy capital spending by apparel, technical, and medical-textile producers, the steady shift toward Industry 4.0 platforms, and regulatory pressure for recycled yarn compatibility are steering demand. Mid-sized manufacturers are scaling electronic control systems to support seamless fashion cycles, while large groups favor fully integrated, sensor-rich machinery that automates quality, maintenance, and supply-chain hand-offs. Asia-Pacific extends its lead through localized supply chains and RCEP tariff advantages, yet the Middle East and Africa show the fastest unit shipment growth as sovereign wealth funds finance greenfield plants. Competitive pressures remain moderate because know-how, after-sales service, and software ecosystems still differentiate the field even when hardware designs converge.

Key Report Takeaways

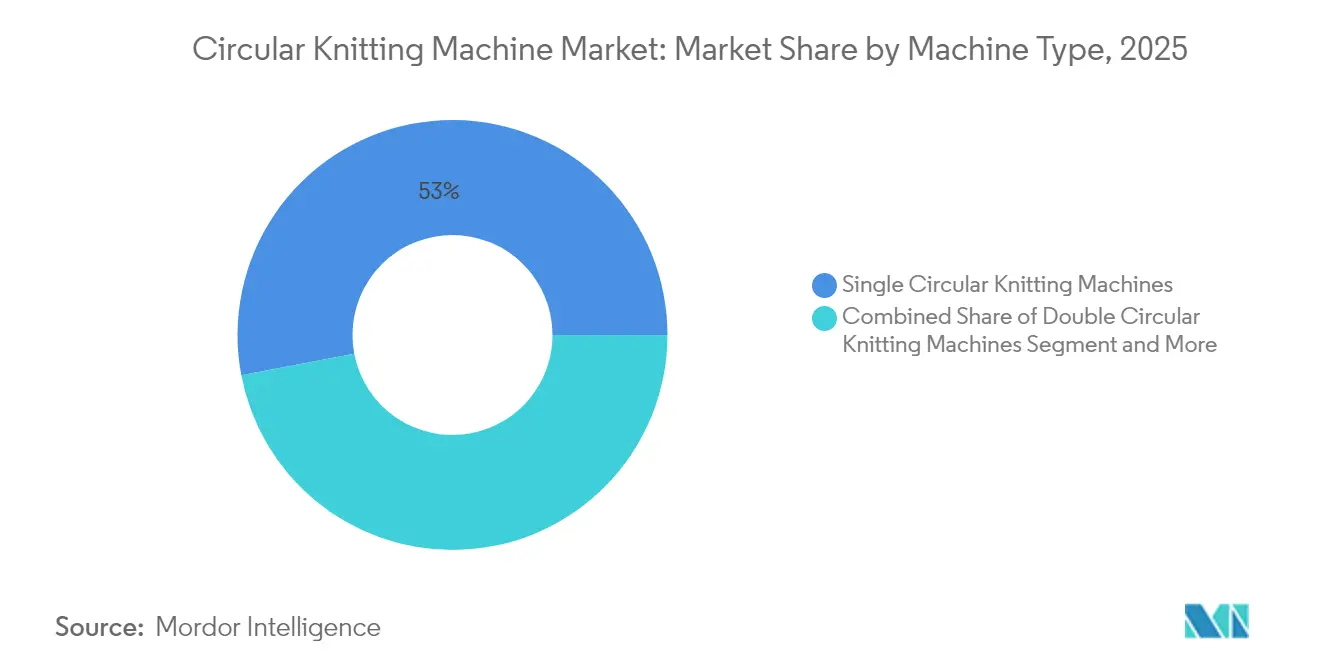

- By machine type, single circular models held 53.00% of the circular knitting machines market share in 2025, whereas specialty jacquard units are set to register the quickest 6.92% CAGR through 2031.

- By gauge, medium-gauge systems captured 47.40% of 2025 revenue, while fine-gauge equipment is forecast to post a 6.02% CAGR to 2031.

- By diameter, mid-diameter machines commanded 41.85% of 2025 sales; small-diameter variants are on track for a 4.58% CAGR during the outlook period.

- By automation level, electronic control platforms accounted for 49.95% share of the circular knitting machines market size in 2025, and Industry 4.0-ready systems should expand at 6.82% CAGR up to 2031.

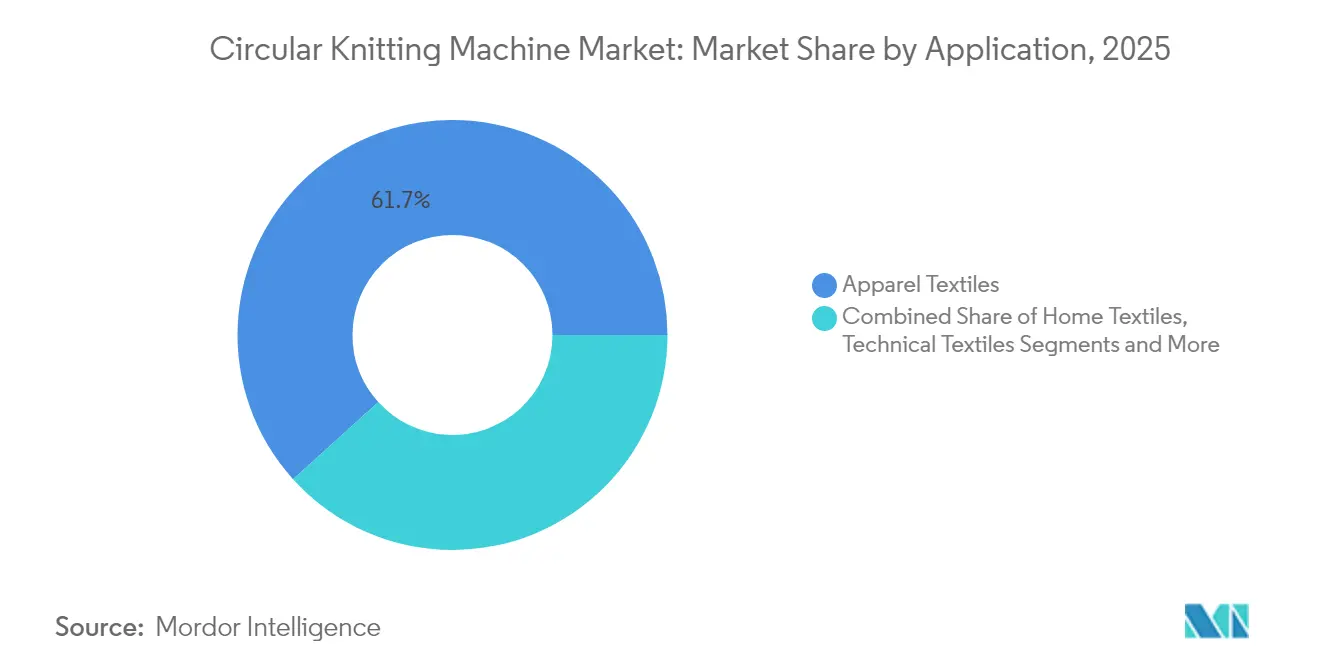

- By application, apparel textiles led with 61.70% revenue share in 2025; technical-textile demand is advancing at an 8.73% CAGR through 2031.

- By yarn type, cotton dominated with a 38.10% share in 2025, yet recycled yarns remain the pace setter at a 7.32% CAGR across the forecast window.

- By geography, Asia-Pacific contributed 47.90% to 2025 shipments, while the Middle East and Africa are projected to deliver the swiftest 5.48% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Circular Knitting Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for seamless/athleisure garments | +1.2% | Global; strongest in North America & Europe | Medium term (2-4 years) |

| Automation & digitization of knitting operations | +1.0% | APAC core; spill-over to North America | Long term (≥ 4 years) |

| Expansion of technical- & medical-textile applications | +0.8% | North America & EU; rising in APAC | Long term (≥ 4 years) |

| Manufacturing migration to cost-efficient Asian clusters | +0.6% | APAC; knock-on to MEA | Medium term (2-4 years) |

| Near-shoring is pressuring flexible, small-lot machinery | +0.5% | North America & EU | Short term (≤ 2 years) |

| Recycled yarn compatibility attracting sustainability capex | +0.4% | Global, led by EU rules | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Seamless/Athleisure Garments

Athleisure’s structural rise is propelling new machinery purchases because seamless technology eliminates cut-and-sew steps that add cost and compromise fit. Santoni’s high-gauge platforms knit compression and ergonomic zones in one pass, creating soft yet durable garments that support premium pricing. Sportswear brands increasingly specify electronic jacquard heads to weave logos and ventilation zones directly into fabric tubes, shrinking lead times for style refreshes. As comfort and performance converge in everyday apparel, fabricators are retrofitting existing bays with multi-gauge cylinders to handle ultrafine yarns. Seamless fashions also trim material waste, bolstering sustainability metrics that retailers track closely in compliance reports.

Automation & Digitization of Knitting Operations

Industry 4.0 integration is rewriting shop-floor management. Pailung’s Manufacturing Execution System records every cam adjustment, enabling exact fabric replication across global plants. IoT sensors feed yarn tension, temperature, and vibration data into cloud analytics that predict faults hours before they stop the line. Digital twins let technicians trial new stitch densities virtually, slashing costly sample loops. Computer vision now flags defects at full speed, so only perfect rolls reach dyeing. With worker shortages in several hubs, autonomous recipe control is no longer optional; it guards uptime and cushions labor risk.

Expansion of Technical- & Medical-Textile Applications

Technical textiles enjoy the fastest adoption curve because circular knitting builds tubes, meshes, and spacer fabrics that weaving cannot replicate. Integer’s micro-diameter equipment knits vascular grafts where pore geometry dictates patient outcomes. Auto makers specify multi-material seat covers that mix polyester face yarns with aramid reinforcements for side-airbag seams, cutting weight and stitching steps. Composite parts for drones and sporting goods emerge from carbon-fiber preforms knitted to net shape, lowering scrap. Hospitals, carmakers, and aerospace OEMs all seek suppliers who can pivot from cotton jerseys to high-modulus synthetics without swapping machines.

Manufacturing Migration to Cost-Efficient Asian Clusters

RCEP has made Vietnam, Bangladesh, and Indonesia magnets for Chinese, Korean, and Japanese groups aiming to hedge labor and tariff exposure. Shared utilities in industrial parks let small knitters access steam and effluent treatment once reserved for giants, spurring pooled orders for mid-range electronic machines. Vendors are rolling out remote-diagnostic dashboards to serve scattered factories with fewer field technicians. As clusters mature, localized spare-part depots shorten downtime, removing a traditional edge held by suppliers located near buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure | -0.8% | Global; SMEs hardest hit | Short term (≤ 2 years) |

| Raw material (yarn) price volatility | -0.6% | Worldwide, cotton belts are acute | Medium term (2-4 years) |

| Skilled machine operator shortage | -0.4% | APAC & North America hubs | Long term (≥ 4 years) |

| Secondary (used-machine) market cannibalization | -0.3% | Emerging, cost-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

A full Industry 4.0 circular knitting line costs USD 15–50 million, covering high-speed cylinders, winding, inspection, and digital backend. Small firms struggle to source that financing, especially where leasing infrastructure lags. Rapid tech cycles magnify risk because equipment can feel dated within five years. Consequently, some buyers postpone upgrades or choose stripped-down models, which slows market acceleration until flexible pay-per-use packages gain traction.

Raw-Material (Yarn) Price Volatility

Cotton futures and polyester feedstock swings squeeze margins when fabric contracts are fixed for seasons. Tax policies in Pakistan that load local cotton with GST highlight how duties distort mill input economics. Recycled yarn premiums fluctuate with collection rates and oil prices, complicating budgeting for eco-labeled programs. Many knitters now stock extra weeks of yarn, raising working-capital needs and warehouse costs[1]Springer, Oluwabusola Dorcas Olagunju, “Investment Decision Modeling for Textile Machinery,” springer.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Single Circular Dominance Faces Jacquard Disruption

Single-cylinder units generated 53.00% of the circular knitting machines market share in 2025 because their straightforward cam architecture delivers high yards per minute for T-shirts, underwear, and sheets. The circular knitting machines market size for specialty jacquard platforms is smaller today, but this niche is on a 6.92% CAGR track as fashion labels chase intricate motifs that lift average selling prices. Modern jacquard heads use micro-step motors for every needle, so patterns change via software rather than hardware plates, trimming setup to minutes. Wellknit’s double computerized jacquard model showcases triple-action knitting, letting mills pivot from plain jerseys at dawn to sculpted relief fabrics by lunch.

Second, double-jersey machinery remains crucial for rib and interlock pieces that demand stretch retention. Although its growth rate trails jacquard, demand holds steady in underwear and sports cuffs. Hybrid platforms now embed removable needle beds, giving operators the choice of single or double knitting without swapping the entire frame. This flexibility appeals to contract manufacturers juggling diverse brand orders under one roof. As a result, the competitive gap between dominant single machines and rising jacquard contenders will narrow through the decade.

By Gauge: Fine Gauge Innovation Drives Premium Applications

Medium gauges (12–24 NPI) owned 47.40% of shipments in 2025 because they balance yarn range, speed, and fabric hand suitable for mass apparel. Fine-gauge models, although costlier, promise a 6.02% CAGR by 2031 as lingerie and athleisure require micro-denier yarns for a second-skin feel. Here, the circular knitting machines market size benefits from technological leaps such as Pailung’s redesigned sinker rings that minimize abrasion at 28 NPI. Ultra-fine cylinders allow seamless hosiery with 200-needle barrels, once exclusive to flat knitting.

Coarse-gauge systems still matter for thermal wear and industrial sleeves, yet face little innovation. The premium differential in yarn weight means coarse fabrics struggle to justify price hikes, capping revenue growth. Consequently, suppliers channel R&D into fine tolerances laser-ground cams, ceramic yarn guides, and oil-mist lubrication to boost speed without compromising needle life.

By Diameter: Small Diameter Growth Reflects Specialized Applications

Mid-diameter machines (15"–30") supplied 41.85% of 2025 revenue, matching common fabric widths for tees and leggings. Small-diameter (<15") cylinders are expanding at a 4.58% CAGR because medical and hosiery demand near-net tubes with minimal seam irritation. Integer’s 8" vascular-graft machine knits implantable polyester sleeves whose uniform wall thickness ensures blood compatibility. Fashion tights benefit, too, since graduated-compression zones are achievable only on tight circumferences.

Large-diameter (>30") frames help terry towel and home-textile makers deliver jumbo rolls, yet plant floor spacing and high power draw limit their adoption. Some mills now adapt modular creels so one large machine feeds several yarn types, maximizing footprint utility. Still, the relative growth edge lies with specialty small-diameter units geared for high-value health and wellness products.

By Automation Level: Industry 4.0 Integration Accelerates

Electronic control held a 49.95% share in 2025 as most mills completed the shift away from purely mechanical cams. Industry 4.0-ready systems, featuring cloud connectivity, digital twins, and AI maintenance, will outpace the base with a 6.82% CAGR. The circular knitting machines market size for computerized platforms rises because sensor-rich cylinders cut defect scrap and unlock predictive uptime. Asian Development Bank studies show Pakistan’s mills expect productivity lifts topping 35% once IoT and analytics mature.

Mechanical rigs persist mainly for entry-level buyers, but component vendors now offer retrofit boards that digitize pattern memory, easing the upgrade path. Still, the step to full smart-factory status is steep: plants must integrate ERP, yarn warehouse, and dye-house data. Vendors that package end-to-end software, not just machines, will capture premium margins.

By Application: Technical Textiles Drive Innovation

Apparel textiles delivered 61.70% of the 2025 turnover owing to global basics consumption. However, technical-textile demand brings the sharpest 8.73% CAGR because automotive, medical, and defense users pay for functionality rather than yards. That pivot enlarges the circular knitting machines market size by inviting higher ASP equipment capable of processing aramid, carbon, and UHMWPE yarns. For instance, Pailung’s spacer-fabric lines knit 3D structures for EV battery insulation where thermal management is critical.

Home textiles remain steady, fed by pandemic-era nesting trends, yet price competition is intense. Niche segments such as filtration sleeves and geotextiles gain traction, but volumes are small. As sustainability metrics harden, brands will prefer mono-material constructions that simplify recycling, pushing mills toward specialized cylinders able to handle stiff technical filaments without needle breakage.

By Yarn Type: Recycled Materials Gain Traction

Cotton kept a 38.10% share thanks to consumer affinity and supply familiarity. Recycled yarns, though, are surging at 7.32% CAGR, elevating the circular knitting machines market share for equipment optimized to handle variable fiber lengths. Mills installing optical yarn evenness testers can knit PET bottle yarn blends at commercial speeds without surge rollers. Research in Polymer Degradation and Stability confirms recycled polyester knit fabrics now match virgin counterparts in pilling and colorfastness after process tweaks.

Synthetic staples such as polyester and nylon still dominate sportswear, and high-tenacity varieties underpin medical and industrial uses. Blends complicate recycling, spurring interest in design-for-disassembly where one polymer rules. Machine suppliers are testing heat-resistant guides to process bio-based PLA filaments that melt at lower temperatures, ensuring future-proof versatility.

Geography Analysis

Asia-Pacific retained 47.90% of 2025 shipments because integrated yarn-to-garment ecosystems, supportive export rebates, and abundant technician pools anchor machinery demand. China leads, yet unit sales migrate to Vietnam and Indonesia as labor costs rise at home and RCEP waives duties on cross-border equipment sales. India’s Production-Linked Incentive scheme fuels fresh orders, though patchy power and zoning rules temper ramp-up speed. Japan’s makers occupy premium niches, supplying micro-diameter lines for medical implants that secure high margins despite modest volume.

North America’s resurgence rests on near-shoring. The United States sees fresh capex as brands value tariff avoidance and carbon-footprint cuts. Shawmut’s North Carolina site demonstrates local investment logic: smart cylinders slash labor reliance while producing specialty fabrics that justify higher wages. Canadian mills, smaller in number, ride the same wave, offering quick-turn knits to e-commerce labels. Mexico absorbs overflow for automotive and protective textiles, helped by USMCA rules of origin.

Europe commands the technology high ground. German and Italian OEMs steer automation breakthroughs and maintain dense service networks. EU Green Deal mandates recycled content, prompting mills in Portugal and Spain to order tension-adaptive machines compatible with reclaimed fibers. The Middle East and Africa register the fastest 5.48% CAGR because Gulf sovereign funds deploy petro-dollars into diversification parks, while Turkey upgrades existing looms to capture EU quick-response orders. Egypt leverages duty-free EU access, yet requires port and energy upgrades to exploit its full potential.

Competitive Landscape

The market remains moderately fragmented: the top five vendors together control just above half of global revenue, leaving room for specialists. Mayer & Cie., Pailung, and Fukuhara headline the tier-1 bracket, leveraging scale for in-house electronics and global service fleets. Chinese challengers, notably Wellknit and Yuanda, undercut on price while closing quality gaps via imported needles and German software modules. Their rapid domestic growth funds foreign expansion, especially into cost-sensitive Africa.

Strategic moves pivot toward platform ecosystems. Pailung bundles IoT dashboards that link creels, knitting heads, and finishing lines, locking clients into proprietary data cycles. Mayer & Cie.’s tie-up with TotalEnergies to co-brand biodegradable machine oil exemplifies value-added consumables that earn annuity margins. Karl Mayer’s acquisition path into tricot broadened its textile architecture reach, hedging against single-technology cyclicality.

Emerging players exploit white spaces. Syre backs recycled-fiber-centric lines, betting regulation will favor its closed-loop narrative. Equipment-as-a-service offers, still nascent, appear in Europe, where banks prefer subscription cash flow over collateral risk. Meanwhile, software houses push retrofit kits that overlay AI defect detection on legacy frames, threatening OEM lock-ins. As cost parity tightens, after-sales uptime guarantees become decisive bid criteria.

Circular Knitting Machine Industry Leaders

-

Baiyuan Machine

-

Mayer & Cie

-

Terrot

-

Santoni

-

Fukuhara

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Syre Group signed a memorandum of understanding with Binh Dinh Province, Vietnam, to develop a USD 1 billion polyester fabric recycling complex with 250,000 t/y capacity, bolstering circular textile infrastructure.

- April 2025: ANDRITZ secured an order from Alear Silk Road New Materials to supply three neXline aXcess spunlace lines in Xinjiang, China, targeting a Q4 2025 start-up.

- April 2025: Chinese Handa Industries committed USD 150 million to Bangladesh for integrated textile and garment operations under a BIDA MoU.

- February 2025: Karl Mayer Group announced a leading circular knitter invested in its tricot machines, signaling warp-knit diversification by cylinder-knit specialists.

Global Circular Knitting Machine Market Report Scope

Circular knitting machines, also known as large circular knitting machines, are devices that generate tubular and seamless fabrics by knitting with circular needles and shaping the fabric by adjusting the tension or length of the knitting stitches. The Global Circular Knitting Machine Market is segmented by Machine Type (Single Circular Knitting Machines, Double Circular Knitting Machines), by Application (Apparel Textiles, Home Textiles, Technical Textiles, Medical Textiles, Others) and by Geography (North America (United States, Mexico and Canada), Asia-Pacific (China, Japan, India, South Korea and Rest of Asia-Pacific), Europe (Germany, France, United Kingdom, Italy, Spain, Benelux and Rest of Europe), Middle East & Africa (South Africa, Saudi Arabia, UAE and Rest of Middle East & Africa) and South America (Brazil and Rest of South America)). The report offers market size and forecasts for transportation infrastructure construction market in value (USD billion) for all above segments.

| Single Circular Knitting Machines |

| Double Circular Knitting Machines |

| Hybrid / Convertible Machines |

| Specialty Jacquard Machines |

| Fine Gauge (Over 24) |

| Medium Gauge (12-24) |

| Coarse Gauge (less than 12) |

| Small (less than 15”) |

| Mid (15”-30”) |

| Large (more than 30”) |

| Mechanical Control |

| Electronic Control |

| Computerized Control |

| Industry-4.0 Integrated |

| Apparel Textiles |

| Home Textiles |

| Technical Textiles |

| Medical Textiles |

| Automotive Textiles |

| Others |

| Cotton |

| Synthetic (Polyester, Nylon) |

| Blends |

| High-Performance Fibers |

| Recycled Yarns |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Machine Type | Single Circular Knitting Machines | |

| Double Circular Knitting Machines | ||

| Hybrid / Convertible Machines | ||

| Specialty Jacquard Machines | ||

| By Gauge | Fine Gauge (Over 24) | |

| Medium Gauge (12-24) | ||

| Coarse Gauge (less than 12) | ||

| By Diameter | Small (less than 15”) | |

| Mid (15”-30”) | ||

| Large (more than 30”) | ||

| By Automation Level | Mechanical Control | |

| Electronic Control | ||

| Computerized Control | ||

| Industry-4.0 Integrated | ||

| By Application | Apparel Textiles | |

| Home Textiles | ||

| Technical Textiles | ||

| Medical Textiles | ||

| Automotive Textiles | ||

| Others | ||

| By Yarn Type | Cotton | |

| Synthetic (Polyester, Nylon) | ||

| Blends | ||

| High-Performance Fibers | ||

| Recycled Yarns | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for circular knitting machinery?

The circular knitting machines market size hit USD 4.04 billion in 2026 and is set to reach USD 5.35 billion by 2031, reflecting a 5.76% CAGR.

Which geographic region leads demand for new circular knitting equipment?

Asia-Pacific accounted for 47.90% of 2025 shipments owing to its integrated textile clusters and trade preferences.

Which machine category is growing the fastest?

Specialty jacquard systems are forecast to expand at 6.92% CAGR because brands seek on-machine patterning and product differentiation.

How are sustainability mandates influencing equipment choices?

Mills are investing in platforms that process recycled polyester and cotton, driving a 7.32% CAGR for recycled-yarn compatible machinery and integrated yarn-quality monitoring systems.

Why are smart, Industry 4.0-ready machines gaining share?

Connected sensors, digital twins and predictive maintenance cut defect rates and labor reliance; such Industry 4.0 platforms are accelerating at a 6.82% CAGR through 2031.

Page last updated on: