Elevator Control Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.59 Billion |

| Market Size (2031) | USD 12.19 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Elevator Control Market Analysis by Mordor Intelligence

The elevator control market size is expected to grow from USD 9.14 billion in 2025 to USD 9.59 billion in 2026 and is forecast to reach USD 12.19 billion by 2031 at 4.93% CAGR over 2026-2031. The elevator control market is benefiting from the rapid migration away from relay-based logic toward IoT-enabled controllers that embed predictive maintenance, destination dispatch, and energy-optimization algorithms. Accelerating high-rise construction, especially in Asia–Pacific megacities, is spurring fresh installations, while tightening safety and accessibility codes are pushing building owners in North America and Europe to modernize aging units. Semiconductor shortages that plagued 2024 have eased, allowing manufacturers to clear backlogs and replenish inventories, yet lingering supply-chain risk keeps lead times above pre-pandemic levels. Rising cybersecurity scrutiny is nudging operators to invest in encrypted communication protocols and secure firmware updates, a trend that turns software maintenance into a recurring revenue stream for leading OEMs. Competitive differentiation is therefore moving beyond hardware toward data analytics, remote diagnostics, and service bundling, reshaping the elevator control market’s growth trajectory.

Key Report Takeaways

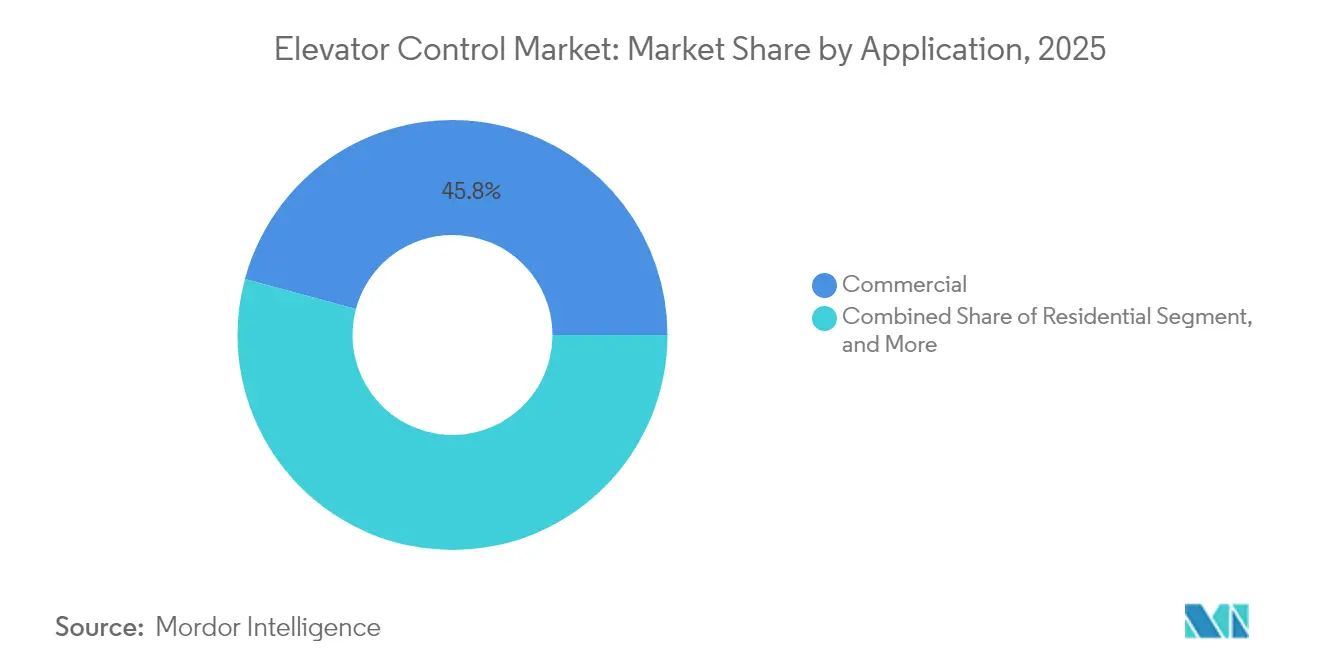

- By application, commercial buildings led with 45.80% of the elevator control market share in 2025, while industrial and logistics applications are forecast to expand at a 6.05% CAGR through 2031.

- By component, controllers accounted for 38.20% of the elevator control market size in 2025, whereas software and connectivity platforms are projected to post the fastest growth at a 6.25% CAGR.

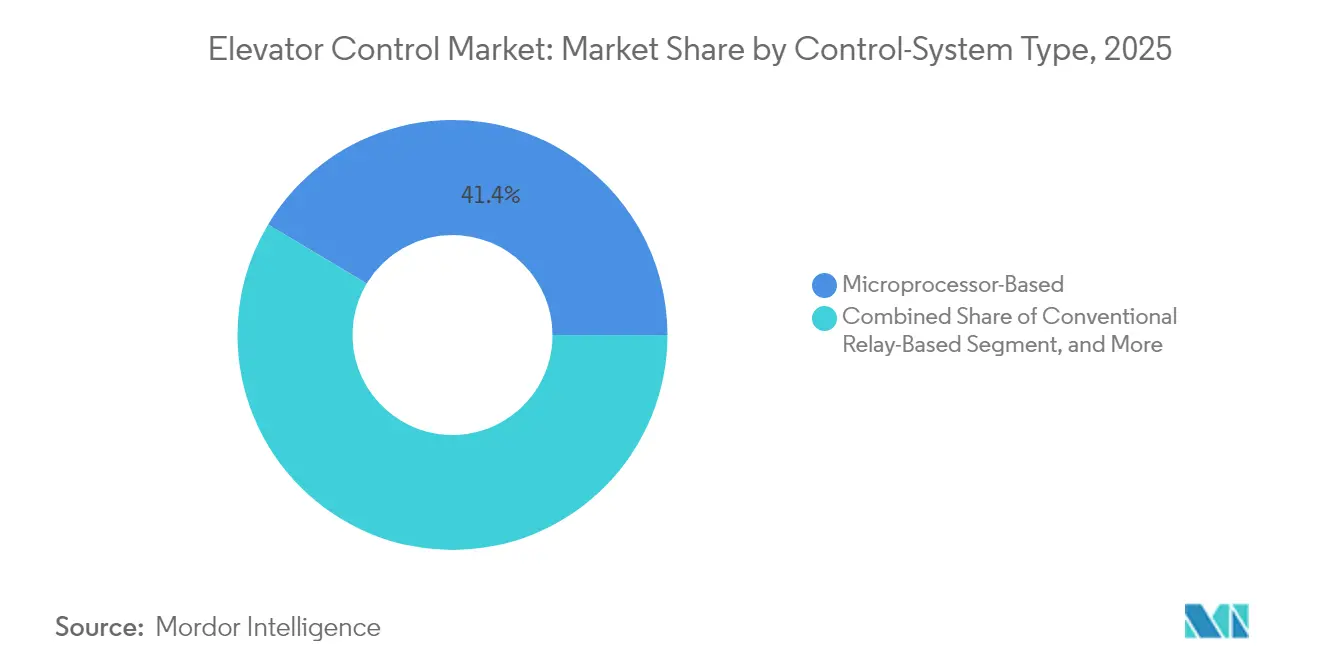

- By control-system type, microprocessor-based solutions held 41.40% share of the elevator control market in 2025, but IoT-enabled smart controls are on track for a 7.55% CAGR.

- By elevator technology, traction systems secured a 54.70% share in 2025, with machine-room-less traction forecast to register a 7.25% CAGR up to 2031.

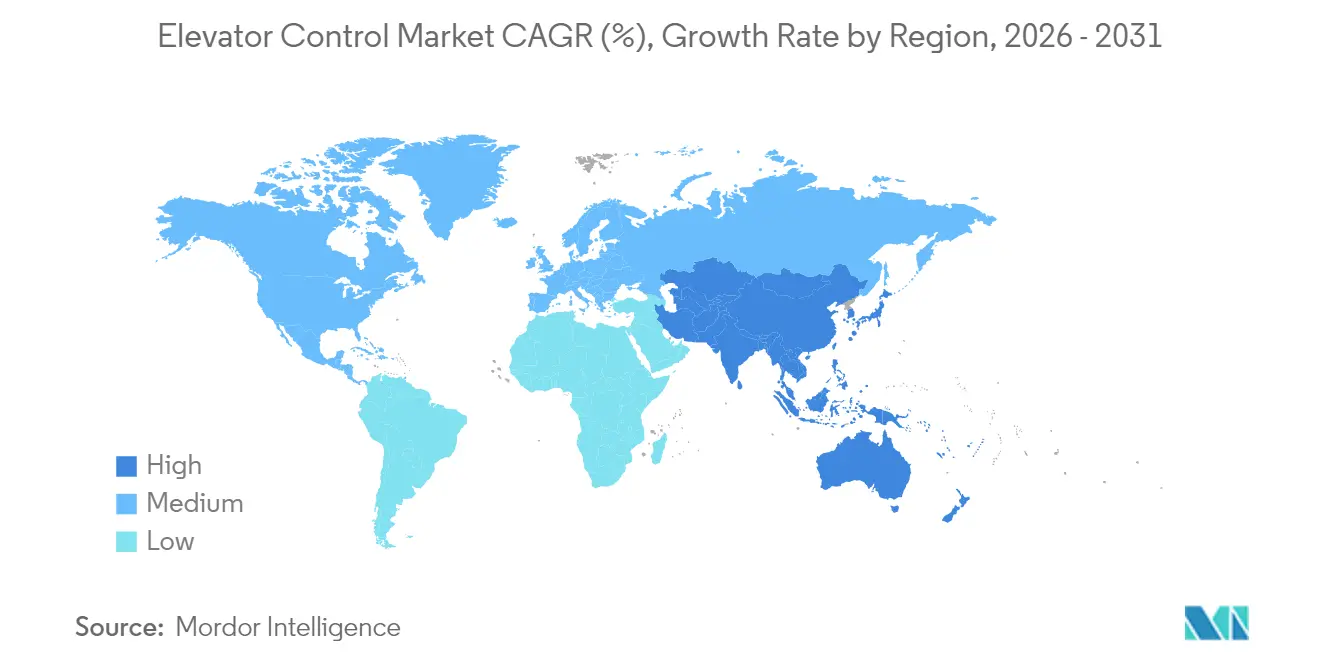

- By geography, Asia-Pacific commanded 43.30% of 2025 revenue and is positioned for the quickest regional advance at an 7.95% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Elevator Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid implementation of advanced technologies in elevator controls | +1.20% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Infrastructure spending on high-rise buildings and metros | +0.90% | Asia-Pacific core, spill-over to Middle East and Latin America | Long term (≥ 4 years) |

| Accelerated modernization of aging elevator stock | +0.80% | North America and Europe, emerging in developed Asia-Pacific | Medium term (2-4 years) |

| Rise of AI-based predictive-maintenance platforms | +0.70% | Global, early adoption in North America and Northern Europe | Medium term (2-4 years) |

| Adoption of touch-free human-machine interfaces | +0.40% | Global, accelerated in high-traffic commercial environments | Short term (≤ 2 years) |

| Mandates for energy-efficient destination-dispatch systems | +0.60% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Implementation of Advanced Technologies

Elevator groups are embedding artificial intelligence to analyze passenger flow, historical traffic, and real-time occupancy data, trimming wait times and cutting energy use by as much as 30% compared with conventional controls.[1]KONE, “Destination control systems reduce wait times and energy use,” KONE.COM Cloud-connected sensors feed live performance metrics to analytics dashboards, enabling predictive alerts weeks before a failure point. Edge processors resident in the controller cabinet maintain responsiveness even when network connectivity drops, ensuring dispatch quality during service interruptions. The feature set appeals to premium office towers that value tenant experience and energy-benchmark ratings. Simultaneously, retrofit kits are bringing similar capability to mid-tier properties, expanding the elevator control market beyond new build opportunities.

Infrastructure Spending on High-Rise Buildings and Metros

Mega-projects in China, India, Indonesia, and Saudi Arabia are allocating record budgets to vertical-transport infrastructure, including destination-dispatch elevators integrated with metro hubs and mixed-use skyscrapers.[2]MENAFN, “Elevator and escalator global market forecast report 2024-2032,” MENAFN.COM Smart-city mandates now place elevator controls within the broader building-management and smart-grid ecosystems, creating pull-through demand for controllers that support open protocols and battery-backed rescue drives. Funding visibility stretching to 2030 gives OEMs confidence to expand local manufacturing footprints and service centers across Asia–Pacific and the Gulf, reinforcing first-mover advantages in high-growth corridors.

Accelerated Modernization of Aging Elevator Stock

In the United States and Europe, more than 4 million elevators exceed 20 years of service and rely on obsolete relay logic that fails to meet current EN 81-20/50 or ASME A17.1 safety clauses.[3]WW Lift, “New European standards for lifts EN 81-20,” WWLIFT.DE Modernization packages typically replace controllers, drives, and hall fixtures, extending unit life by up to 20 years and lowering energy bills by 40-60%. Insurance carriers increasingly require such upgrades before renewing coverage, shrinking payback periods for owners. Manufacturers offer modular kits with factory-prewired harnesses that reduce on-site labor, accelerating the elevator control market’s retrofit cycle.

Rise of AI-Based Predictive Maintenance Platforms

Sensor arrays mounted on motors, doors, and guide rails capture vibration spectra, torque curves, and door-cycle counts. Machine-learning models trained on millions of run hours predict failure modes with accuracy rates above 85%, reducing unplanned outages by up to 80%.[4]VisionNav Robotics, “The role of automated lift trucks in modern warehousing,” VISIONNAV.COM Service firms monetize these insights through uptime-guaranteed contracts, underpinning a shift from reactive repairs to outcome-based maintenance. Integration with augmented-reality headsets lets junior technicians diagnose faults in near real time, partially alleviating labor shortages and improving first-visit fix rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure | -0.80% | Global, particularly acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Shortage of certified installation technicians | -0.60% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Cyber-security and data-privacy concerns in connected controls | -0.40% | Global, heightened in regulated industries and government facilities | Medium term (2-4 years) |

| Volatility in semiconductor and power-electronics supply chains | -0.50% | Global, with regional variations in component availability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

Full controller retrofits run between USD 15,000 and USD 50,000 per car, and ancillary electrical and IT work can add another 20-30%. In price-sensitive emerging markets, owners postpone upgrades despite energy savings because financing windows remain short and interest rates high. Temporary service outages also deter tenants, leading landlords to stage work during off-hours at premium labor rates, prolonging return-on-investment periods.

Shortage of Certified Installation Technicians

Vacancy rates exceed 15% for union-licensed elevator mechanics in major U.S. and European metros. The skill mix has shifted from mechanical know-how toward software commissioning and cybersecurity, but training pipelines have not kept pace. Variable certification rules limit cross-border talent mobility, stretching project timelines and inflating labor costs. OEMs now operate proprietary academies and remote-support centers to bridge the gap, but field capacity remains a gating factor for the elevator control market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Commercial Leadership and Logistics Momentum

Commercial buildings contributed USD 4.19 billion to the elevator control market size in 2025 and retained a 45.80% share as property managers demanded sophisticated destination dispatch and remote-monitoring suites to enhance tenant experience. Energy benchmarking programs such as LEED and BREEAM intensified the adoption of regenerative drives and AI-based traffic-optimization modules. Meanwhile, the 6.05% CAGR forecast for industrial and logistics facilities underlines e-commerce operators’ appetite for vertical lift modules that integrate seamlessly with warehouse-execution software.

The residential segment is adding growth on the back of smart-home ecosystems that link elevator calls to mobile credentials and building security. Infrastructure and public facilities, including airports and metro stations, seek vandal-resistant hall fixtures and redundant safety relays to handle heavy passenger loads. Across applications, retrofit demand is rising as owners chase lower energy bills and seek to comply with disability-access mandates such as EN 81-70. Commercial landlords especially prize controllers that harvest granular ride data, feeding occupancy analytics and informing space-utilization strategies—effects that reinforce the elevator control market’s service-revenue loop.

By Component: Controllers Rule but Software Surges

Controllers delivered 38.20% of 2025 revenue by serving as the command brain that enforces safety logic, group dispatch, and network connectivity. Controller upgrades remain the cornerstone of modernization packages, ensuring the elevator control market share associated with this component stays broad-based across geographies. Yet, software and connectivity platforms are poised for a 6.25% CAGR through 2031 as OEMs push subscription-based dashboards, cybersecurity updates, and predictive-maintenance engines.

Drives and inverters hold stable volume because every modernization swings in a high-efficiency variable-voltage drive to curb electricity draw and enable regenerative braking. Hall fixtures and COP/LOP panels are morphing into touchless and mobile-enabled interfaces, a shift accelerated by post-pandemic hygiene expectations. Sensor and I/O modules proliferate as condition-monitoring becomes the norm. Overall, the value migrates from hardware margins to recurring software fees, a shift reshaping revenue models across the elevator control market.

By Control-System Type: Smart Controls Gain Ground

Microprocessor-based units represented 41.40% of 2025 shipments, a testament to their balance of cost and capability. However, IoT smart controls are growing 7.55% annually, fueled by building-management integration requirements and tenant demand for real-time elevator status updates. The elevator control market size allocated to smart controls is expected to more than double by 2031, partly at the expense of conventional microprocessor replacements.

Relay logic remains in legacy freight and low-rise stock but commands a limited future share. Destination dispatch systems continue to penetrate premium offices where travel-time savings justify higher capex. Group and AI traffic-optimized controls occupy the top tier, harnessing cloud analytics to adapt sequences during exceptional events. Connectivity and analytics have thus become decisive purchase criteria, tilting competitive advantage toward vendors with robust digital ecosystems.

By Elevator Technology: Traction Dominates, MRL Accelerates

Traction elevators held 54.70% of revenue in 2025, leveraging high energy efficiency and adaptability to mid- and high-rise buildings. Yet, machine-room-less (MRL) traction designs are rising at 7.25% CAGR as architects aim to reclaim mechanical-room space for leasable area. Controllers for MRL deployments must withstand higher ambient temperatures and tighter footprints, prompting innovation in compact power electronics.

Hydraulic systems remain cost-effective for low-rise installations but confront environmental headwinds tied to fluid leakage and energy intensity. Pneumatic and linear-motor technologies linger in niche segments such as panoramic lifts and high-speed observation decks. Even so, all technologies are migrating toward regenerative drives and power-factor-correction modules, trends that buttress demand across the elevator control market.

Geography Analysis

Asia–Pacific captured 43.30% of 2025 revenue, reflecting dense new-building pipelines and policy support for smart-city rollouts. China’s urban-renewal schemes and India’s 100-smart-cities program ensure sustained controller demand, while Southeast Asian nations embrace machine-room-less designs to fit constrained footprints. Local OEM assembly plants shorten lead times and tailor features to regional codes, insulating the elevator control market from severe currency shocks.

North America constitutes a mature installed base ripe for modernization. Legislative updates, including California’s seismic safety amendments and New York City’s door-lock monitoring requirement, incentivize owners to replace mid-1990s controllers. Predictive-maintenance subscriptions resonate with real-estate investment trusts that prioritize uptime metrics, supporting premium pricing. Additionally, Canada’s green-building policies accelerate the adoption of regenerative drives and energy-reporting dashboards.

Europe remains steady as EN 81-20/50 compliance vaults safety and accessibility to the top of procurement criteria. High penetration means growth hinges on retrofits, yet strong sustainability agendas trigger adoption of destination dispatch and energy-recovery hardware. Meanwhile, the Middle East and Africa witness rapid greenfield activity across Gulf megaprojects, demanding climate-resilient controllers with dust-ingress protection. Latin America’s gradual economic rebound lifts new installations, though currency volatility tempers capex, stalling some elevator control market conversions.

Competitive Landscape

The elevator control market is moderately consolidated; the top four companies collectively hold major revenue from global service contracts. Their nationwide technician fleets, proprietary spare parts, and bundled service subscriptions create high switching costs for property owners. Product roadmaps emphasize cloud dashboards, encrypted firmware pipelines, and AI-driven traffic optimization, differentiating brands through software rather than motors and relays.

Mid-tier specialists such as Thames Valley Controls and Lester Controls focus on open-protocol retrofits, appealing to independent maintenance firms that wish to avoid OEM lock-in. Suppliers of vertical lift modules, notably SSI SCHAEFER, extend advanced control algorithms to logistics applications, carving out a high-growth adjacency. Component vendors, including Nidec and SICK AG, concentrate on drives and safety sensors, partnering with OEMs to integrate condition-monitoring features at the board level.

M&A has accelerated as majors seek geographic reach and digital capability. KONE’s 2024 buyout of Capitol Elevator widened its U.S. modernization network. Otis continues to acquire regional service companies to shore up aftermarket revenue, while Kings III’s purchase of LiftNet in April 2025 bolstered telemetry and emergency-communication capacity. Patent filings cluster around cybersecurity, AI dispatch, and regenerative power capture, signaling where future elevator control market competition will intensify.

Elevator Control Industry Leaders

Mitsubishi Electric Corporation

Hyundai Elevator Co., Ltd.

Toshiba Elevator and Building Systems Corporation

Thames Valley Controls Ltd.

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kings III Emergency Communications acquired LiftNet to deepen its cloud-based elevator monitoring suite; the deal strengthens recurring SaaS revenue while giving building owners unified emergency-call and analytics dashboards.

- September 2024: Elevator Solutions bought several Saudi service firms, securing local technician capacity crucial for Gulf megaproject installations and ensuring regulatory familiarity with GCC safety codes.

- August 2024: KONE finalized the purchase of Capitol Elevator, enhancing regional density in the U.S. Southeast and accelerating controller-upgrade sales into aging mid-rise portfolios.

- June 2024: Cibes Lift Group acquired Morning Star Elevator to expand its North American access-lift lineup, targeting residential retrofits that demand compact controllers and mobile-app integration.

Global Elevator Control Market Report Scope

The scope of the current publication on Elevator market includes new as well as retrofit demand/consumption of Elevator control units. In other words, we have identified the demand for various types of hardware components and control systems integrated into the final installation, for both residential and commercial segments.

An elevator control unit is a system comprising of sensors, switches and controllers (primarily), to control the elevators both manually and automatically. The need for a control unit is aligned with performance of tasks such as coordination of elevator travel, door opening & closing speed, delays and leveling, to name a few.

Further, considering the competitive analysis, stakeholders such as elevator manufacturers (Mitsubishi, Toshiba etc.), standalone elevator control manufacturers (MEC, Thames Valley Controls) and component manufacturers (Honeywell, SICK) are made part of the analysis.

| Residential |

| Commercial |

| Industrial and Logistics |

| Infrastructure and Public Facilities |

| Controllers |

| Drives and Inverters |

| Control Panels and COP/LOP |

| Sensors and I/O Modules |

| Software and Connectivity Platforms |

| Conventional Relay-Based |

| Microprocessor-Based |

| Destination-Control Systems |

| IoT-Enabled Smart Controls |

| Group / AI Traffic-Optimised Controls |

| Traction |

| Machine-Room-Less Traction |

| Hydraulic |

| Others (Pneumatic, Linear-Motor) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application | Residential | ||

| Commercial | |||

| Industrial and Logistics | |||

| Infrastructure and Public Facilities | |||

| By Component | Controllers | ||

| Drives and Inverters | |||

| Control Panels and COP/LOP | |||

| Sensors and I/O Modules | |||

| Software and Connectivity Platforms | |||

| By Control-System Type | Conventional Relay-Based | ||

| Microprocessor-Based | |||

| Destination-Control Systems | |||

| IoT-Enabled Smart Controls | |||

| Group / AI Traffic-Optimised Controls | |||

| By Elevator Technology | Traction | ||

| Machine-Room-Less Traction | |||

| Hydraulic | |||

| Others (Pneumatic, Linear-Motor) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the elevator control market in 2026?

The elevator control market size reached USD 9.59 billion in 2026 and is forecast to hit USD 12.19 billion by 2031.

Which region leads demand for elevator controls?

Asia-Pacific holds 43.30% of global revenue thanks to rapid urbanization and smart-city investments.

What segment grows fastest to 2031?

Industrial and logistics applications post the quickest advance at a 6.05% CAGR as warehouses adopt vertical lift modules.

Why are smart controls gaining share?

IoT-enabled controllers deliver predictive maintenance, energy savings, and tenant-experience gains that outweigh higher capex.

What is the main restraint on adoption?

High upfront capital expenditure, ranging from USD 15,000 to USD 50,000 per car, deters owners despite long-term savings.

Which companies dominate the competitive landscape?

Otis, KONE, Schindler, and TK Elevator lead, controlling over half of global service revenue through expansive maintenance networks.

Page last updated on: