Size and Share of Electronic Components Market For HVDC Systems

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Growth Rate | 9.27% CAGR |

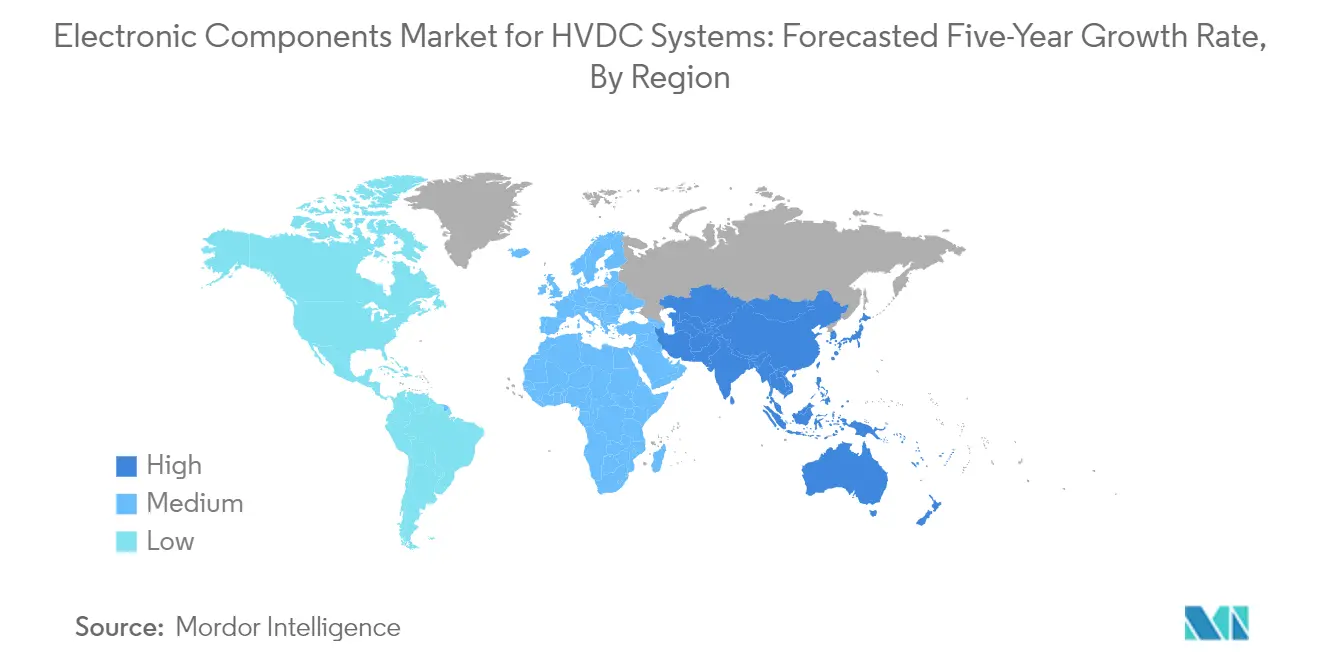

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Electronic Components Market For HVDC Systems by Mordor Intelligence

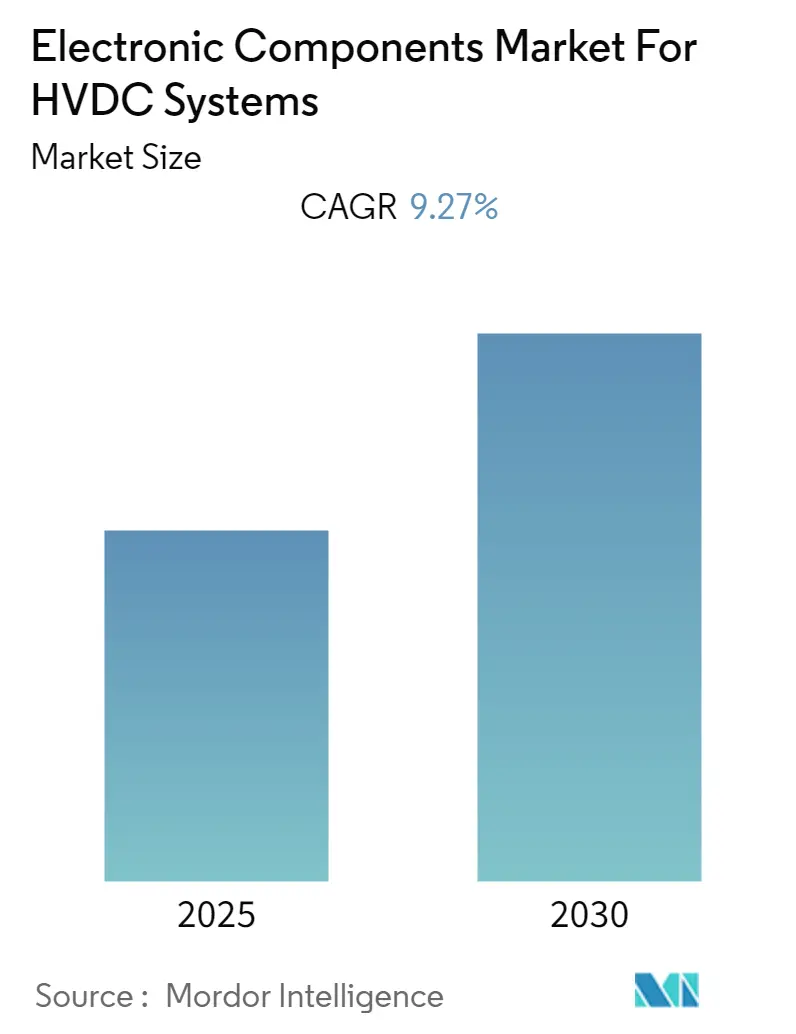

The Electronic Components Market For HVDC Systems Industry is expected to register a CAGR of 9.27% during the forecast period.

The electronic components market for HVDC systems is experiencing significant transformation amid broader energy sector developments. According to the International Energy Agency, clean energy investment exceeded USD 1.4 trillion in 2022, accounting for approximately three-quarters of the growth in overall energy investment. The ongoing geopolitical tensions, particularly the Russia-Ukraine conflict, have significantly impacted the market by disrupting supply chains and causing price volatility in raw materials such as nickel and palladium, which are crucial for manufacturing semiconductor chips and other electronic components. These disruptions have led to increased prices for multilayered ceramic chip capacitors and other critical components of HVDC systems, forcing manufacturers to reassess their supply chain strategies and pricing models.

The industry is witnessing substantial technological advancements in power transmission infrastructure. In March 2023, Hitachi Energy inaugurated a new High-Voltage Direct Current (HVDC) and Power Quality factory in Chennai, India, focusing on manufacturing power electronics for HVDC for high-power transmission solutions. Similarly, LS Cable & System completed the construction of Submarine Building 4 in March 2023, representing Asia's largest HVDC underwater cable plant with an investment of approximately USD 141 million. These developments indicate a growing focus on enhancing manufacturing capabilities and technological innovation in the components of HVDC systems sector.

The market is experiencing a significant shift toward grid modernization and efficiency improvements. According to IRENA, global renewable generation capacity reached 3,372 Gigawatts (GW) by the end of 2022, with renewables accounting for an impressive 83% of all power capacity added during the year. This transformation has led to increased demand for advanced electronic components that can support more efficient and reliable power transmission systems. The industry is particularly focusing on developing components that can handle higher voltage levels and provide better control capabilities for modern HVDC converters.

The sector is witnessing substantial investments in infrastructure development. In January 2023, State Grid Corporation announced plans to invest USD 77 billion in transmission infrastructure for 2023 alone, with a total investment of USD 329 billion planned throughout the 2021-2025 period. In May 2023, Pattern Energy selected Hitachi Energy to supply HVDC converter technologies for the SunZia Transmission Project, which will be among the world's largest transmission links for renewable energy. These investments reflect the industry's commitment to expanding and modernizing HVDC infrastructure, driving demand for advanced electronic components and creating opportunities for technological innovation in the sector.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Electronic Components Market For HVDC Systems

Growing Adoption of Renewable Energy

The increasing focus on renewable energy adoption is driving significant demand for electronic components in HVDC systems, as these components play a crucial role in efficiently transmitting power from renewable sources to consumption centers. According to the U.S. Energy Information Administration (EIA), renewable energy consumption in the United States reached 8.24 quadrillion British thermal units in 2023, marking an increase from the previous year, while fossil fuel consumption declined to 77.18 quadrillion British thermal units. This transition toward renewable energy sources necessitates advanced HVDC transmission systems equipped with sophisticated electronic components like capacitors and thyristors to manage power flow efficiently and maintain grid stability. The growing installation of offshore wind farms and solar power plants at remote locations has particularly accelerated the need for HVDC systems that can transmit power over long distances with minimal losses.

The global push for carbon neutrality and renewable energy integration has led to substantial investments in HVDC infrastructure development. For instance, in May 2023, Hitachi Energy was selected by Pattern Energy to supply HVDC technologies for the SunZia Transmission Project, which will connect the 3,500-megawatt SunZia Wind project in New Mexico to power grids in Arizona and Southern California. This project exemplifies how electronic components in HVDC systems are becoming increasingly critical for enabling the efficient transmission of renewable energy across vast distances. Additionally, various countries are setting ambitious renewable energy targets, with many aiming to achieve significant portions of their power generation from renewable sources by 2030, driving the demand for advanced HVDC components such as HVDC converters and HVDC transformers that can support this transition while ensuring grid reliability and stability.

Increasing Investments in Submarine Power Transmission

The surge in submarine power transmission projects is creating substantial demand for electronic components in HVDC systems, as these components are essential for efficient underwater power transmission. In February 2023, Hitachi Energy India expanded its capabilities by launching a new assembly and testing factory near Chennai, focusing on manufacturing advanced power electronics for HVDC Light, HVDC Classic, and STATCOM systems. This development reflects the growing importance of submarine power transmission in global energy infrastructure. The increasing number of offshore wind farms and the need to connect remote island territories to mainland power grids have made submarine HVDC transmission systems a critical component of modern energy infrastructure, driving demand for specialized electronic components designed to operate in challenging marine environments.

Recent developments in submarine power transmission projects demonstrate the increasing scale of investments in this sector. For instance, in March 2023, Hitachi Energy signed an agreement with the Gulf Cooperation Council Interconnection Authority to upgrade the Al Fadhili HVDC converter station in Saudi Arabia, highlighting the growing focus on enhancing submarine power transmission capabilities. Similarly, Sumitomo Electric Industries received a significant contract worth approximately USD 200 million in February 2023 from Samsung C&T Corporation to deliver HVDC cables for Abu Dhabi National Oil Company (ADNOC) in the United Arab Emirates, with system operations expected to commence in 2025. These investments in submarine power transmission infrastructure are driving innovation in electronic component design and manufacturing, particularly for components that must withstand the unique challenges of subsea operations while maintaining high efficiency and reliability. The integration of HVDC control systems and HVDC circuit breakers is vital in ensuring the safety and efficiency of these complex underwater networks.

Segment Analysis

Passive Components Segment in Electronic Components Market for HVDC Systems

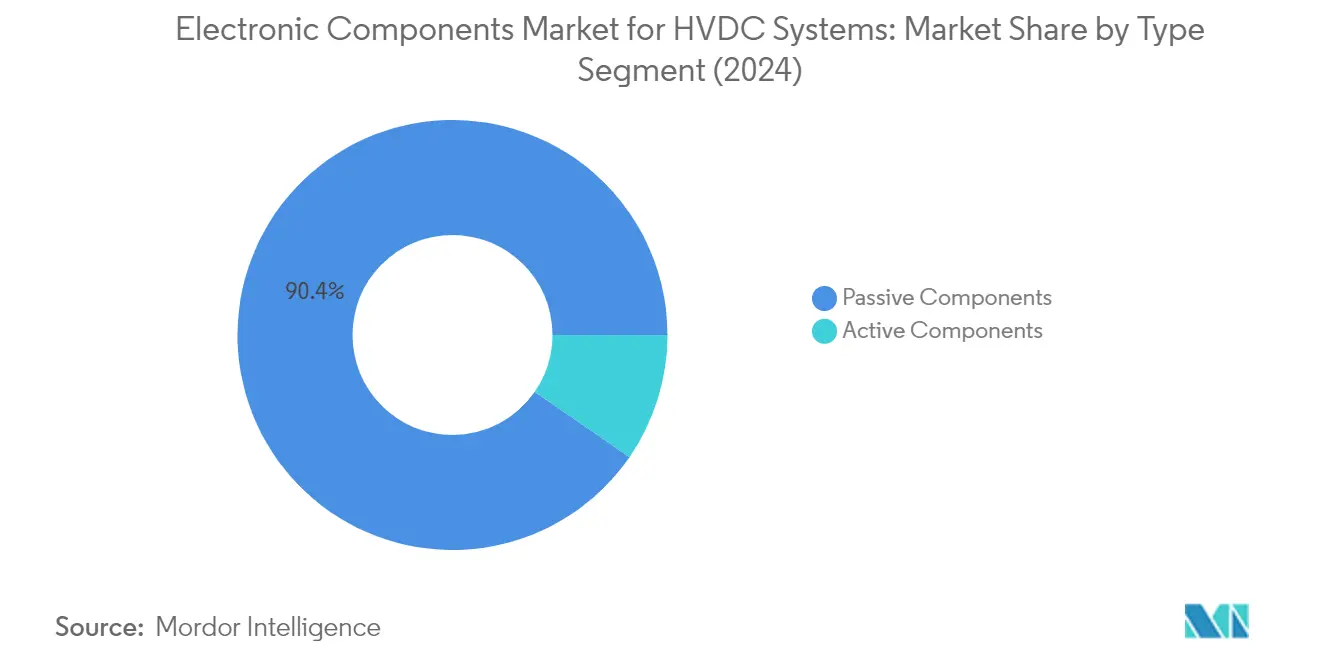

The Passive Components segment dominates the Electronic Components Market for HVDC Systems, commanding approximately 90% market share in 2024. This dominance is driven by the extensive use of HVDC capacitors and resistors in HVDC transmission systems. HVDC capacitors play a crucial role in converting AC to DC, transmitting power between HVDC converter stations, and converting DC back to AC for feeding electricity into the power grid. The segment's growth is primarily fueled by increasing investments in renewable energy projects and submarine power transmission infrastructure worldwide. Passive components, particularly HVDC capacitors, are witnessing heightened demand due to their application in voltage stabilization, power quality improvement, and reduction of transmission losses in HVDC systems. The segment is projected to maintain its market leadership position and experience robust growth at around 10% CAGR through 2024-2029, supported by the rapid expansion of HVDC transmission projects globally and the increasing adoption of renewable energy sources. The HVDC capacitor market is expected to benefit significantly from these trends.

Active Components Segment in Electronic Components Market for HVDC Systems

The Active Components segment, comprising IGBTs and HVDC thyristors, plays a vital role in HVDC systems by providing essential power control and conversion capabilities. These components are fundamental in voltage-source converters (VSC) and line-commutated converters (LCC), which are the two main types of HVDC technologies currently dominating the landscape. IGBTs are particularly crucial in VSC-HVDC systems, offering advantages such as compact design and superior control capabilities, making them ideal for offshore wind power transmission and applications with space constraints. HVDC thyristors continue to maintain their significance in traditional HVDC systems, especially in high-power, long-distance transmission applications. The segment's development is closely tied to technological advancements in semiconductor devices and the growing demand for more efficient power electronic devices in HVDC applications.

Geography Analysis

Electronic Components Market for HVDC Systems in North America

The North American electronic components market for HVDC systems maintains a significant presence, commanding approximately 21% of the global market share in 2024. The region's market is primarily driven by the increasing adoption of renewable energy sources and rapid urbanization across the United States and Canada. The growing focus on reducing energy losses in power transmission and distribution networks has spurred investments in HVDC infrastructure. The region's commitment to achieving 100% clean electricity and a zero-emissions economy has catalyzed the development of high-voltage transmission facilities. The market is further strengthened by substantial investments in grid modernization initiatives and the implementation of advanced HVDC system components in HVDC systems. The presence of established manufacturers and ongoing technological advancements in power transmission systems continues to reinforce North America's position as a key market for HVDC electronic components.

Electronic Components Market for HVDC Systems in Rest of Americas

The Rest of Americas region, predominantly comprising Latin American countries, has demonstrated steady growth in the HVDC electronic components market, with an approximate growth rate of 5% during 2019-2024. The market dynamics in this region are shaped by increasing energy consumption patterns and the growing adoption of renewable energy sources. Latin American countries are actively pursuing the modernization of their power transmission infrastructure to accommodate the rising electricity demand. The region's focus on enhancing grid reliability and efficiency through HVDC technology implementation has created sustained demand for electronic components. Market growth is further supported by governmental initiatives promoting clean energy adoption and grid modernization efforts. The increasing integration of renewable energy sources into the power grid has necessitated advanced HVDC solutions, driving the demand for various electronic components such as capacitors and other passive components.

Electronic Components Market for HVDC Systems in Europe, Middle East & Africa

The Europe, Middle East & Africa (EMEA) region exhibits robust growth prospects in the HVDC electronic components market, with projections indicating a strong growth trajectory of approximately 10% during 2024-2029. The market is characterized by extensive investments in renewable energy infrastructure and cross-border power transmission projects. European nations are particularly focused on developing a unified energy market, driving the adoption of HVDC technology. The region's commitment to carbon neutrality has accelerated the deployment of electronic components in HVDC systems. The Middle East's growing focus on renewable energy integration and Africa's expanding power infrastructure create additional growth opportunities. The market benefits from technological advancements in HVDC systems and the presence of major manufacturing facilities. Regional cooperation in power transmission projects further strengthens the market dynamics.

Electronic Components Market for HVDC Systems in China

China represents a dominant force in the global HVDC electronic components market, driven by its ambitious renewable energy goals and extensive power transmission infrastructure development. The country's leadership in HVDC installations and manufacturing capabilities positions it as a crucial market player. China's commitment to expanding its domestic grid network, particularly in ultra-high-voltage transmission systems, continues to drive demand for electronic components. The nation's focus on connecting renewable energy sources to load centers through HVDC technology creates sustained market opportunities. The presence of advanced manufacturing facilities and ongoing technological innovations in power transmission systems further strengthens China's market position. The country's strategic investments in grid infrastructure and emphasis on efficient power transmission solutions continue to shape market dynamics, with a notable demand for HVDC transformers and other power electronic devices.

Electronic Components Market for HVDC Systems in Rest of Asia-Pacific

The Rest of Asia-Pacific region, encompassing countries like Japan, India, South Korea, and Australia, demonstrates significant potential in the HVDC electronic components market. The region's transition towards renewable energy sources and modernization of power transmission infrastructure drives market growth. Countries in this region are actively investing in grid enhancement projects and HVDC transmission systems to improve power distribution efficiency. The market benefits from technological advancements and the presence of major electronic component manufacturers. Strategic investments in power transmission projects and the increasing focus on renewable energy integration continue to create opportunities for market expansion. The region's commitment to reducing carbon emissions and improving grid reliability further supports the adoption of HVDC technology and associated electronic components, including HVDC power electronics and HVDC transformers.

Competitive Landscape

Top Companies in Electronic Components Market for HVDC Systems

The electronic components market for HVDC systems is led by established players, including Infineon Technologies, Renesas Electronics, Texas Instruments, Toshiba Corporation, Microchip Technology, STMicroelectronics, Broadcom, Mitsubishi Electric, Hitachi Energy, and Vishay Intertechnology. These companies demonstrate a strong commitment to product innovation through substantial R&D investments, particularly in developing advanced IGBTs, thyristors, and capacitors optimized for HVDC system components. Operational agility is evidenced by their focus on manufacturing technology improvements and supply chain optimization to ensure consistent component availability. Strategic initiatives include vertical integration of manufacturing processes, long-term partnerships with key distributors, and collaboration with research institutions to accelerate technological advancement. Geographic expansion remains a key priority, with companies establishing regional manufacturing facilities and technical support centers to better serve growing markets, particularly in Asia Pacific and Europe, where HVDC infrastructure development is accelerating.

Market Dominated by Diversified Technology Conglomerates

The competitive landscape is characterized by the dominance of large, diversified technology conglomerates that possess extensive manufacturing capabilities, established distribution networks, and significant financial resources. These major players leverage their broad technology portfolios and cross-sector expertise to develop comprehensive component solutions for HVDC applications. The market demonstrates moderate consolidation, with the leading companies controlling substantial market share through their established relationships with major HVDC system manufacturers and utilities. Many of these companies have maintained their market positions through decades of experience in power electronic devices and continued investment in advanced manufacturing facilities.

The industry has witnessed strategic consolidation through mergers and acquisitions, primarily aimed at expanding product portfolios and gaining access to specialized technologies or regional markets. Companies are increasingly focusing on acquiring smaller, specialized firms that possess innovative technologies or unique capabilities in specific component categories. This consolidation trend has been particularly evident in the power semiconductor segment, where larger companies seek to strengthen their positions in high-voltage applications and enhance their technological capabilities for next-generation HVDC systems.

Innovation and Adaptability Drive Market Success

For incumbent players to maintain and expand their market share, continuous investment in research and development remains crucial, particularly in areas such as wide-bandgap semiconductors and advanced passive components. Success increasingly depends on the ability to offer comprehensive solutions that address the evolving requirements of HVDC systems, including higher voltage ratings, improved efficiency, and enhanced reliability. Companies must also strengthen their manufacturing capabilities to achieve economies of scale while maintaining product quality and reliability. Building strong relationships with key HVDC system manufacturers and maintaining close collaboration with utilities and grid operators has become essential for understanding evolving market needs and securing long-term contracts.

For new entrants and smaller players seeking to gain ground, focusing on specialized niches and developing innovative solutions for specific HVDC applications presents the most viable strategy. The market's high barriers to entry, including substantial capital requirements and stringent quality standards, necessitate careful strategic positioning and potentially strategic partnerships with established players. The regulatory environment, particularly regarding grid connectivity standards and environmental requirements, continues to shape market dynamics and create opportunities for companies that can effectively address these requirements. While end-user concentration in the utility sector presents challenges, the growing adoption of HVDC technology in renewable energy integration and cross-border power transmission creates new opportunities for market participants, particularly in the development of HVDC converters and HVDC transformers.

Leaders of Electronic Components Market For HVDC Systems

Infineon Technologies AG

Renesas Electronics Corporation

Texas Instruments Incorporated

Toshiba Corporation

Microchip Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2023 - Hitachi Energy India Ltd (formerly ABB Power Products and Systems India) expanded its regional facility by launching a new assembly and testing factory near Chennai, India. The new factory would manufacture advanced power electronics for HVDC Light, HVDC Classic, and STATCOM, together with a MACH control and protection system. It would deliver cutting-edge solutions to accelerate the energy transition, enabling Hitachi Energy to increase its production capacity.

- December 2022 - Vishay Intertechnology Inc. announced the release of a new series of screw terminal aluminum electrolytic capacitors 202 PML- ST, which is practical for designers and ideal for a variety of pulsed power filtering, buffering, and energy storage applications needing a lifetime of 10 to 15 years.

Scope of Report on Electronic Components Market For HVDC Systems

High voltage direct current (HVDC) power systems utilize direct current to transmit bulk power over long distances. The devices used in an HVDC transmission system are constructed using active and passive electronic components. While an active component provides energy to an electrical circuit, a passive component stores the energy for later use.

The Electronic Components Market for HVDC Systems is segmented by type (active components (IGBT and thyristors) and passive components (capacitors and resistors)) and geography (North America, Rest of the Americas, Europe, Middle East and Africa, China, and Rest of Asia Pacific). The report offers market forecasts and size in value (USD) for all the above segments.

| Active Components | IGBT |

| Thyristor | |

| Passive Components | Capacitors |

| Resistors |

| North America |

| Rest of the Americas |

| Europe, Middle East and Africa |

| China |

| Rest of Asia Pacific |

| By Type | Active Components | IGBT |

| Thyristor | ||

| Passive Components | Capacitors | |

| Resistors | ||

| By Geography | North America | |

| Rest of the Americas | ||

| Europe, Middle East and Africa | ||

| China | ||

| Rest of Asia Pacific | ||

Key Questions Answered in the Report

What is the current HVDC Systems Electronic Components Market size?

The HVDC Systems Electronic Components Market is projected to register a CAGR of 9.27% during the forecast period (2025-2030)

Who are the key players in HVDC Systems Electronic Components Market?

Infineon Technologies AG, Renesas Electronics Corporation, Texas Instruments Incorporated, Toshiba Corporation and Microchip Technology Inc. are the major companies operating in the HVDC Systems Electronic Components Market.

Which is the fastest growing region in HVDC Systems Electronic Components Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in HVDC Systems Electronic Components Market?

In 2025, the Asia Pacific accounts for the largest market share in HVDC Systems Electronic Components Market.

What years does this HVDC Systems Electronic Components Market cover?

The report covers the HVDC Systems Electronic Components Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the HVDC Systems Electronic Components Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: