Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

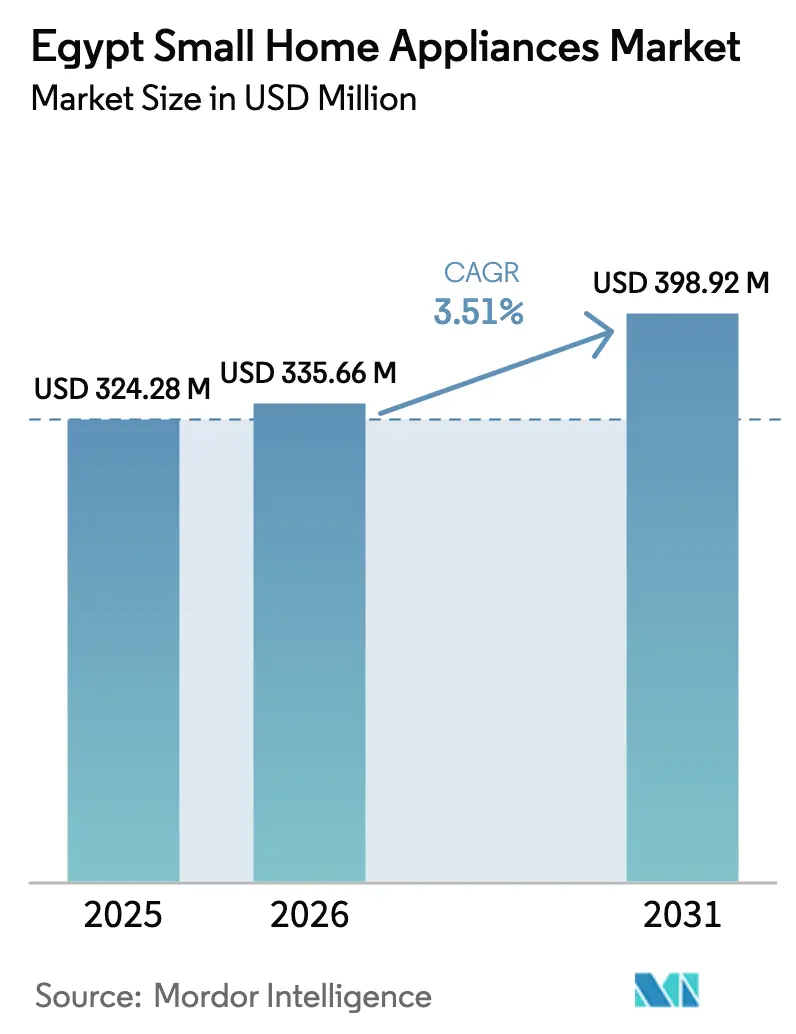

| Base Year Market Size (2025) | USD 324.28 Million |

| Market Size (2026) | USD 335.66 Million |

| Market Size (2031) | USD 398.92 Million |

| Growth Rate (2026 - 2031) | 3.51% CAGR |

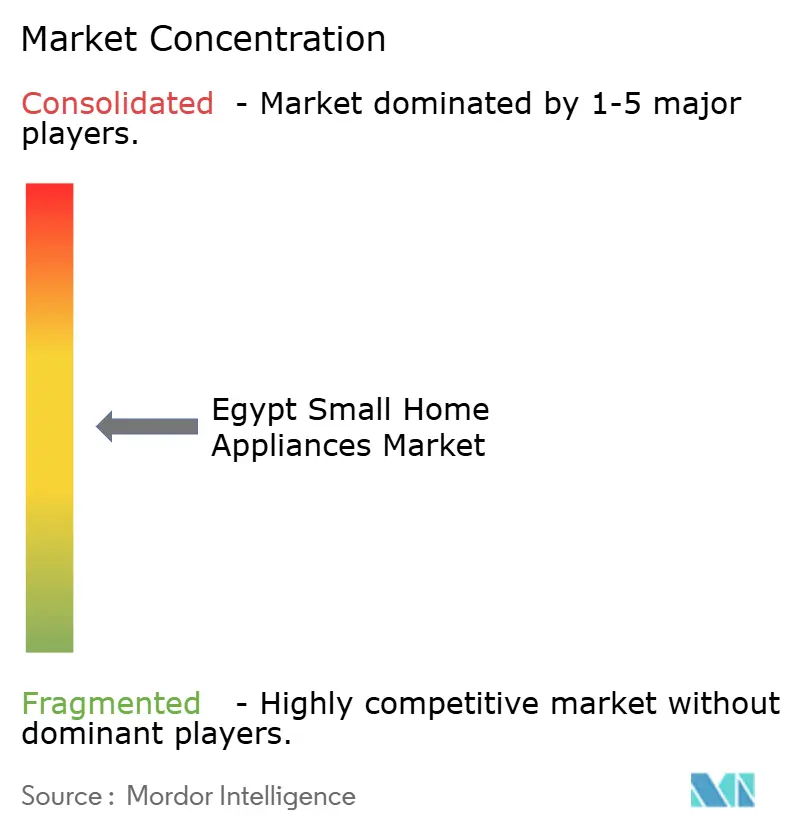

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Small Home Appliances Market Analysis by Mordor Intelligence

The Egypt small home appliances market size is expected to increase from USD 324.28 million in 2025 to USD 335.66 million in 2026 and reach USD 398.92 million by 2031, growing at a CAGR of 3.51% over 2026-2031. Policy support for localization, rising adoption of energy-efficient models, and the export orientation of new capacity expansions are shaping the competitive balance and long-term growth profile. The government is using golden licenses, tax holidays, and lower machinery import duties to anchor multinational production in Egypt, while also nudging manufacturers toward higher local-content thresholds. These incentives align to lower the national import bill and build a regional export base in Africa and the Middle East. Manufacturers are also incorporating inverter motors and higher-efficiency components to comply with labelling rules and to meet consumers’ need to manage electricity costs. Currency swings and elevated input costs remain headwinds, yet they reinforce the export case for locally made products and encourage more suppliers to qualify Egyptian component makers for regional value chains.

Key Report Takeaways

- By product type, juicers and blenders held 17.12% of the Egypt small home appliances market share in 2025, and air fryers are forecast to expand at a 4.12% CAGR through 2031.

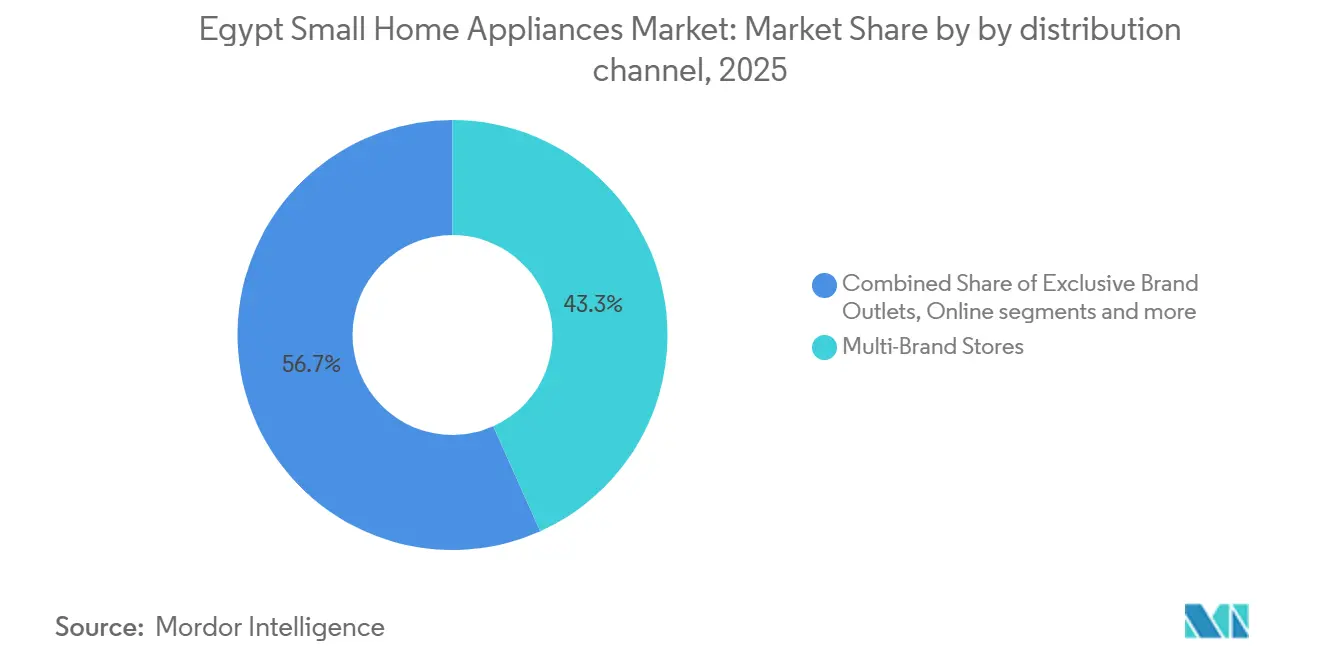

- By distribution channel, multi-brand stores accounted for 43.31% of the Egypt small home appliances market share in 2025, while online channels are projected to grow at a 4.83% CAGR during 2026–2031.

- By geography, Greater Cairo captured 39.13% of the Egypt small home appliances market share in 2025, and Alexandria and the Coastal Region are the fastest-growing areas at a 4.38% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Small Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & urban migration | +0.9% | National, concentrated in Greater Cairo, New Administrative Capital, and New Alamein. | Medium term (2-4 years) |

| E-commerce proliferation and last-mile logistics maturity | +0.7% | National, strongest in Greater Cairo, Alexandria, and Delta cities, with fulfillment hubs | Short term (≤ 2 years) |

| Demand for energy-efficient devices amid rising power tariffs | +0.6% | National, early gains in new-city developments, including New Cairo and Sheikh Zayed | Medium term (2-4 years) |

| Government incentives for local assembly and component sourcing | +0.8% | National industrial zones, including 10th of Ramadan, 6th of October, Badr City, and Borg El Arab | Long term (≥ 4 years) |

| Buy-Now-Pay-Later and micro-credit penetration | +0.5% | National, the highest uptake in urban middle-income segments | Short term (≤ 2 years) |

| Expansion of rental housing and smaller household sizes are driving compact appliance demand | +0.6% | Urban centers nationwide, especially Greater Cairo, Alexandria, Giza, and emerging mixed-use developments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Urban Migration

Egypt is experiencing sustained urbanization, with around 43% of the population living in urban areas and the share continuing to rise as internal migration channels households toward cities such as Greater Cairo and Alexandria, where income opportunities are stronger[1]UN-Habitat, “Urbanization in Egypt: Urban Population and Growth,” unhabitat.org, Urban numbers section. Urban migration is increasingly concentrated in planned new cities, including the New Administrative Capital, New Cairo, and New Alamein, which are designed around reliable power supply, fibre connectivity, and modern residential infrastructure. These developments favour compact apartment layouts and standardized kitchen fit-outs, accelerating demand for space-saving, efficient small home appliances. Developers and homebuilders in these zones act as early catalysts for appliance adoption, particularly for energy-efficient and premium models suited to smaller footprints. In parallel, concentrated urban housing pipelines strengthen after-sales networks for installation, maintenance, and spare parts, improving product lifetime value and supporting faster replacement cycles and higher-spec appliance uptake across core metropolitan and satellite urban markets.

E-commerce Proliferation and Last-Mile Logistics Maturity

Egypt’s e‑commerce market reached approximately EGP 60 billion (USD 1.18 billion), with 21,800 businesses operating online, representing roughly 14.9% of total national revenue[2]Source: CAPMAS, Sixth Economic Census – E‑commerce in Egypt, youm7.com summary of official CAPMAS data, showing EGP 60 billion e‑commerce value and 21.8k online businesses, youm7.com. Online channels increasingly offer integrated payment solutions, installment options, and next-day or same-day delivery in major cities, expanding access to a broader SKU range, including mid-tier and premium small appliances, for time-constrained households. Fintech partnerships have reduced checkout friction, with licensed consumer-finance providers reporting strong adoption and higher transaction volumes for electronics and household devices in 2024. Consumer finance platforms and retail apps allow buyers to spread payments over 6 to 24 months, encouraging upgrades to higher-quality models. Omnichannel retailers leverage store networks as micro-fulfillment hubs, enabling click-and-collect services and faster returns, improving overall customer satisfaction, while ongoing logistics and payment innovations continue to drive growth in Egypt’s small home appliances market.

Demand for Energy-Efficient Devices Amid Rising Power Tariffs

Energy-efficiency standards and labelling requirements are now mandatory for many household categories, signalling a clear policy path toward lower device-level electricity consumption. Manufacturers respond by adding inverter motors, brushless DC components, and redesigned control software to improve kilowatt-hour usage profiles and qualify for higher efficiency classes. The labelling regime gives retailers and buyers a transparent yardstick for comparing performance, which supports premium pricing for compliant models and improves sell-through of newer SKUs. Independent test bodies accredited in Egypt report increased certification requests for higher-efficiency classes, reflecting both compliance and consumer demand. Programs linked to green financing have supported factory retrofits that cut energy use in production, and those investments also translate into product-level efficiency upgrades that meet regulatory targets.

Government Incentives for Local Assembly and Component Sourcing

Golden licenses, multi-year corporate tax exemptions, and reduced customs duties on production machinery lower initial costs and shorten time-to-market for both multinational and local players. The incentive framework includes geographic tiers that award higher deductions in designated zones, which encourages dispersion of factories into industrial cities outside central Cairo. Tariff policy distinguishes between CKD kits, subassemblies, and finished goods, which rewards projects that increase local content through supplier qualification programs. Administrative streamlining and unified approval tracks have improved visibility for investors on plant commissioning timelines. These measures collectively reinforce a structural localization shift that sustains component sourcing in Egypt and supports the export positioning of the Egypt small home appliances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High inflation and Egyptian pound depreciation | -1.2% | National, acute pressure on lower-income households nationwide | Short term (≤ 2 years) |

| Import-linked supply-chain volatility | -0.5% | National, significant for manufacturers reliant on imported components | Medium term (2-4 years) |

| Rising electricity prices are reducing discretionary appliance purchases | -0.6% | National, with a stronger impact in urban and peri-urban residential areas | Medium term (2–4 years) |

| Limited consumer access to after-sales service and spare parts outside major cities | -0.4% | Secondary cities and rural governorates, including Upper Egypt and frontier regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Inflation and Egyptian Pound Depreciation

Macroeconomic pressures reduce discretionary budgets for non-essential devices, increasing price sensitivity and extending replacement cycles in the mass market. Inflation in household furnishings and equipment remained elevated in late 2025, which pushed retailers to recalibrate pricing and promotions to sustain footfall. Volatility in exchange rates and commodity prices raises input costs for copper, sheet metal, and electronics, and not all manufacturers can hedge or absorb those hikes. Brands with global procurement networks have more levers to manage input volatility, while local producers lean on tactical discounts when demand softens. The resulting bifurcation favors premium energy-efficient SKUs for affluent buyers and slows mid-range adoption among price-sensitive segments.

Import-Linked Supply-Chain Volatility

A sizable share of key inputs still comes from overseas suppliers, which exposes local factories to freight rerouting, port congestion, and longer lead times during regional disruptions. Shipping adjustments in 2024 and 2025 lengthened delivery times from Asian hubs to Egyptian ports, raising landed costs and forcing higher safety stock levels of critical components. Certification and testing queues increased at labs, adding clearance days that tie up working capital and delay market entry for updated models. Manufacturers have responded by establishing dual sourcing for non-critical inputs and by validating Egyptian vendors for packaging, harnesses, and simple assemblies. These mitigations reduce exposure but still carry higher carrying costs, compressing operating margins in the Egyptian small home appliances market during volatile periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Category Leadership Masks Divergent Growth Trajectories

Juicers and blenders accounted for 17.12% of 2025 revenues, reflecting broad use across income tiers and a clear path to upgrades to higher-wattage or multi-attachment models in the Egyptian small home appliances market. Air fryers are the fastest-growing category, with a 4.12% CAGR through 2031, supported by healthy cooking preferences, rapid adoption of air-fryer technology, and frequent retail promotions on 3.5-to-12-liter units. Retailers list entry- and mid-range models across multiple brands, and the mix spans preset menus, digital controls, and larger baskets suited to family-size preparation. Coffee makers, kettles, and food processors remain day-to-day utility items for core kitchens, supported by price bands that enable step-ups within the same brand. Vacuum cleaners are split into barrel and upright models for traditional needs, and cordless stick or robotic units that meet apartment storage and convenience requirements.

The range of price points and the accessories ecosystem drive configuration choices as buyers weigh counter space, functionality, and durability in the Egyptian small home appliances industry. Category leaders expand attachment bundles for processors and blenders, while budget brands focus on simple, repairable designs to maintain affordability. Retailers also leverage bundles that pair a blender with a processor or pair kettles with toasters, creating value packs that lift sell-through when promotions run. Merchant assortment strategies reflect seasonal peaks in fans and heaters, and longer-cycle purchases in kitchen prep categories, while managing inventory by region and season. Category fragmentation presents room for brand differentiation, and robust after-sales support encourages repeat purchases and upgrades over time.

By Distribution Channel: Online Gains Belie Brick-and-Mortar’s Enduring Grip

Multi-brand stores accounted for 43.31% of the market in 2025 by offering hands-on product trials and immediate fulfillment, which remain attractive to appliance buyers who value touch and feel in the Egyptian small home appliances market. Retailers deploy experiential zones for key categories and offer store-based finance options, extended warranties, and product demos that move shoppers through the funnel. Exclusive brand outlets reinforce engagement by showcasing new lines and by cross-selling complementary SKUs and service plans at the point of sale. Online channels are projected to grow at a 4.83% CAGR through 2031, driven by integrated payments, last-mile delivery in major cities, and deeper SKU visibility across price bands. Consumer-finance partners and retail apps are lifting conversion and basket sizes online, and omnichannel operations link stores and digital platforms for flexible fulfillment.

Outside Greater Cairo and Alexandria, delivery surcharges and multi-day windows temper online adoption, preserving the role of independent bazaars and regional chains in the Egyptian small home appliances market. Retailers use store networks to reach areas where cash is preferred, and they maintain relationships with local installers and servicers to keep after-sales costs predictable. Enterprise buyers in hospitality and healthcare channels procure small appliances in bulk and sign service agreements that smooth revenue, particularly for coffee machines, kettles, and vacuums. Across channels, retailer and brand data sharing is improving assortment decisions and price positioning by region and store format. Tighter controls on quality and certifications also benefit organized retail, deepening trust and reducing returns in categories where brand authenticity matters.

Geography Analysis

Greater Cairo captured 39.13% of 2025 revenues due to its scale, density of retail locations, and concentration of appliance manufacturing footprints, which together create an integrated production and sales hub for the Egyptian small home appliances market. New-city housing around the capital is driving demand for compact, energy-efficient appliances, including built-in and slimline options that suit smaller kitchen footprints. Factory commissioning and supplier qualification are often staged in industrial cities near Cairo, enabling faster time-to-market and stronger after-sales coverage. Export-focused capacity additions by multinationals operating in Egypt also coordinate with capital-region logistics and distribution nodes. Capital-area buyers adopt premium devices at higher rates, which supports the introduction of new features and connected functions ahead of the national average.

Alexandria and the Coastal Region are the fastest-growing areas, with a 4.38% CAGR through 2031, driven by port proximity, trade flows, and seasonal tourism that creates bulk demand for hospitality devices. Export activity and inbound components flow through coastal gateways, lowering transport costs for factories and distributors serving nearby markets. Seasonal outfitting of coastal residences and resorts drives sales of kettles, coffee makers, and vacuums during specific months, requiring dynamic inventory management. Coastal demand for premium energy-rated products trails the capital region, but product availability and retail footprint expansion are narrowing the gap. New investments across coastal industrial zones support additional assembly and component sourcing, serving both domestic and export channels.

The Nile Delta and the remaining governorates contribute steady demand through a mix of organized retail, independent outlets, and online platforms with longer delivery windows. Product selection aligns with income bands and with electrification and broadband availability, which influences the adoption of connected SKUs. Retailers position installer networks and service centres to build trust in areas where the used market and informal channels remain active. Seasonal sales patterns for climate-related products guide stock positioning and promotional calendars across the Delta and Upper Egypt. As logistics mature and regulated finance becomes more accessible, regional buyers gain entry to more brands and to installment plans that reduce upfront costs for mid-tier models.

Competitive Landscape

The competitive field is structured into three tiers: local-scale brands, multinational platforms, and specialist brands targeting niche categories in the Egyptian small home appliances market. Local champions leverage vertically integrated supply chains and contracted component output to supply multiple brands while also advancing their own product portfolios. Multinational manufacturers are accelerating a pivot to local assembly and content, working with Egyptian partners to qualify parts and to meet export content rules for regional trade agreements. Specialists tune portfolios for coffee preparation, kitchen prep, and compact cooking, often pairing innovation cycles with retail partnerships that widen physical and digital reach.

Multinational capacity additions provide a steady stream of export-ready volume and support domestic SKU breadth across price tiers. Multinational capacity additions provide a steady stream of export-ready volume and support domestic SKU breadth across price tiers. BSH opened its first African production site in 2025 with a 350,000-unit annual capacity focused on cooking appliances, and half of the output is designated for export to the Middle East, Africa, and beyond[3]BSH Hausgeräte GmbH, “New BSH Plant in Egypt,” bsh-group.com, press.bsh-group.com. Beko began implementing an industrial park and export hub in Egypt, including ovens and refrigerators with meaningful export allocations, supported by third-party brand production. Electrolux confirmed its commitment to expanding operations in Egypt in 2025, positioning it for export growth and incremental market-share gains. These moves raise the export profile of Egypt-based plants and empower firms to adapt product portfolios to regional preferences while preserving duty advantages tied to local content.

Brand differentiation in premium and specialist niches is visible in coffee systems, kitchen processors, and connected housekeeping devices. Panasonic partnered with a smart-home distributor in late 2025 to bring IoT-enabled devices to Egypt, signaling demand for connected ecosystems that combine appliances with home-automation platforms[4]Source: Panasonic Middle East, “Panasonic Appoints NexGen as Partner in Egypt,” panasonic.com, panasonic.com. Coffee device makers and kitchen system brands continue to update their portfolios, with accessory ecosystems and feature bundles driving step-ups from entry models. Samsung and other multinationals maintain capacity in adjacent categories and can move into select small-appliance lines as local partnerships and demand signals strengthen. These strategic moves broaden the feature set available to consumers and push category leaders to maintain a cadence of hardware and software upgrades.

Egypt Small Home Appliances Industry Leaders

Fresh Electric

Unionaire

LG Electronics

Samsung Electronics

Midea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Panasonic partnered with NexGen to expand smart-home solutions in Egypt, with NexGen serving as the exclusive distributor and service provider for IoT-enabled devices focused on energy efficiency and connectivity.

- July 2025: Midea Group expanded its African footprint by investing in new washing machine and refrigerator factories in Egypt. The company planned production to begin in 2025, leveraging Egypt’s strategic location and government support to strengthen regional manufacturing and exports.

- June 2025: BSH Home Appliances Group inaugurated its first production facility in Africa, located in 10th of Ramadan City. The site boasts an annual production capacity of 350,000 units, with approximately 50% of the output designated for export to various international markets.

- March 2025: Beko, owned by Arçelik, announced the official launch of the Hitachi brand in Egypt along with plans to manufacture locally at the Beko Egypt Industrial Park as part of a USD 110 million investment focused on refrigerators, dishwashers, and vacuum cleaners.

Egypt Small Home Appliances Market Report Scope

Small appliances are semi-portable or portable machines, basically used on platforms such as countertops and tabletops to accomplish a certain household task. They include portable types of electrical appliances such as cooking appliances, food processing/preparation, personal care, floor care, etc.

The Egypt Small Home Appliances Market Report is segmented by product type (coffee makers, food processors, grills & toasters, electric kettles, juicers & blenders, air fryers, vacuum cleaners, electric rice cookers, other small home appliances), distribution channel (multi-brand stores, exclusive brand outlets, online, other distribution channels), technology (conventional, smart/connected), and geography (Greater Cairo, Alexandria & Coastal Region, Nile Delta, Rest of Egypt). The market forecasts are provided in terms of value (USD Million).

By Product Type

| Coffee Makers |

| Food Processors |

| Grills & Toasters |

| Electric Kettles |

| Juicers & Blenders |

| Air Fryers |

| Vacuum Cleaners |

| Electric Rice Cookers |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Greater Cairo |

| Alexandria & Coastal Region |

| Nile Delta |

| Rest of Egypt |

| By Product Type | Coffee Makers |

| Food Processors | |

| Grills & Toasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Other Small Home Appliances | |

| By Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Geography | Greater Cairo |

| Alexandria & Coastal Region | |

| Nile Delta | |

| Rest of Egypt |

Key Questions Answered in the Report

What is the current size and expected growth of the Egypt small home appliances market?

The market stands at USD 335.66 million in 2026 and is set to reach USD 398.92 million by 2031 at a 3.51% CAGR.

Which product categories lead and which are growing fastest in Egypt?

Juicers and blenders lead with 17.12% share in 2025, while air fryers are the fastest growing with a 4.12% CAGR through 2031.

How are distribution channels evolving for small appliances in Egypt?

Multi-brand stores remain dominant with a 43.31% share in 2025, and online channels are expanding at a 4.83% CAGR as payments and last-mile delivery improve.

What is the technology mix for small appliances in Egypt?

Conventional products represent 81.31% of 2025 volume, and smart or connected devices are set to grow at a 4.47% CAGR through 2031.

Which regions account for the greatest and fastest-growing demand?

Greater Cairo holds 39.13% of 2025 revenues, and Alexandria and the Coastal Region are the fastest-growing at a 4.38% CAGR.

Page last updated on: