Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

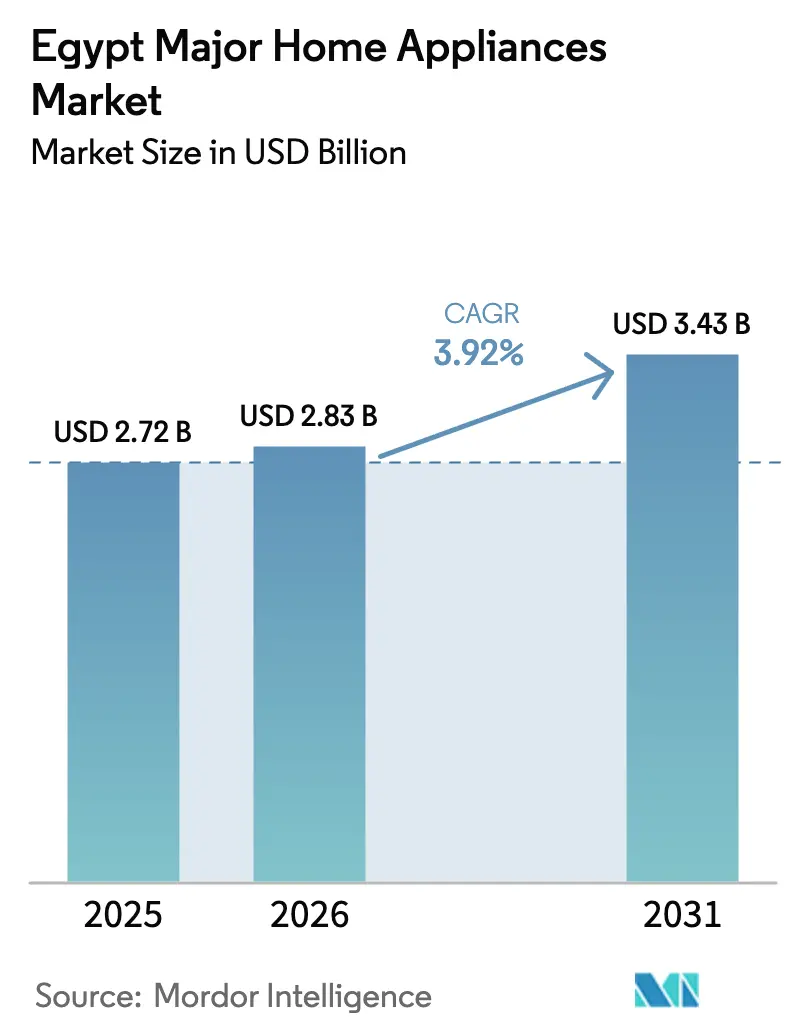

| Base Year Market Size (2025) | USD 2.72 Billion |

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Major Home Appliances Market Analysis by Mordor Intelligence

The Egypt major home appliances market size is expected to grow from USD 2.72 billion in 2025 to USD 2.83 billion in 2026 and is forecast to reach USD 3.43 billion by 2031 at 3.92% CAGR over 2026-2031. The near-term outlook is shaped by a pivot toward local manufacturing and exports as global brands and large domestic players add capacity and deepen localization to reduce foreign-currency exposure and leverage trade preferences. Duty-free access via Qualified Industrial Zones and Egypt’s trade agreements with the European Union and the United States continue to support the export proposition into large consumer markets. Domestic demand softened in late 2025 as inflation stayed elevated and policy rates remained tight, but easing monetary conditions in 2026, the growth of installment-led e-commerce, and a visible shift to energy-efficient appliances underpin a gradual volume recovery. Structural import substitution is evident in lower import values for refrigerators and washing machines in 2025, which coincides with fresh capacity coming online and more aggressive price competition among local assemblers. Conversely, imports of refrigerators and washing machines dropped USD 50 million in the first nine months of 2025 versus the prior year, signaling a structural pivot to domestic manufacturing that is reducing foreign-currency leakage even as it intensifies local rivalry[1]Youm7, “ Youm7, January 5, 2026,” Youm7, youm7.com.

Key Report Takeaways

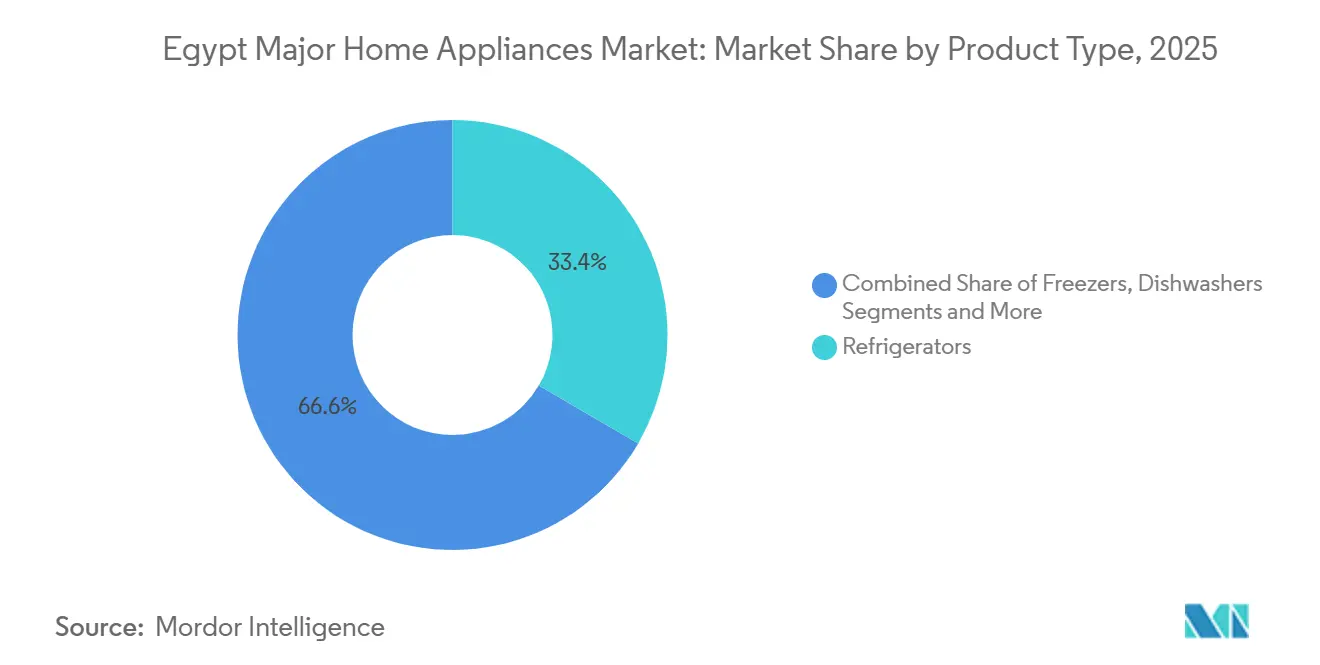

- By product type, refrigerators led with 33.41% of the Egypt major home appliances market share in 2025, while dishwashers are projected to expand at a 4.81% CAGR through 2031.

- By distribution channel, multi-brand and exclusive-brand stores accounted for 40.41% of the Egypt major home appliances market in 2025, while online platforms recorded the highest projected CAGR of 5.52% through 2031.

- By geography, Greater Cairo and Giza accounted for 37.62% of Egypt's major home appliances market size in 2025, while Alexandria and the Mediterranean Coast are set to register the fastest CAGR of 5.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter energy-efficiency labels are stimulating replacement | +0.8% | National, strongest in Greater Cairo, Alexandria | Medium term (2-4 years) |

| Local manufacturing and export-oriented capacity expansion | +1.2% | National, concentrated in 10th of Ramadan, Quesna, 6th of October | Long term (≥ 4 years) |

| Omnichannel and e-commerce growth with BNPL enabling big-ticket purchases | +1.0% | Urban centers, Cairo, Alexandria, Giza, Mansoura | Short to medium term (≤ 3 years) |

| Consumer finance penetration under FRA-regulated installment schemes | +0.7% | National, higher penetration in urban governorates | Medium term (2-4 years) |

| Power-rationing and tariff hikes are accelerating inverter and efficient models | +0.9% | National, acute in summer-peak regions | Short term (≤ 2 years) |

| Import-process normalization (LC removal, ACI), improving assortment recovery | +0.4% | National, particularly port-adjacent industrial zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Energy-Efficiency Labels Stimulating Replacement Demand

Egypt's 2025 transition from Energy Efficiency Ratio (EER) to Seasonal Energy Efficiency Ratio (SEER) for air conditioners, mandated by the Egyptian Organization for Standardization & Quality (EOS) under Ministerial Decree 502/2023, imposes seven efficiency tiers (S1 through S7) with S1 units achieving SEER ≥12 for non-ducted variable-speed models[2]meetMED, “Minimum Energy Performance Standards and Energy Labeling Implementation Manual,” meetMED, meetmed.org. The change overlaps with higher household electricity tariffs implemented in 2024 and 2025, which increased monthly bills and shifted buyer preference toward inverter units with lower lifetime operating costs. Appliance makers now prioritize visible energy claims and SEER labels on packaging to convert delayed replacements, positioning inverter portfolios as the default choice in urban showrooms and e-commerce listings. Installment-led promotions help close the upfront price gap, with retailers and manufacturers partnering on zero-interest payment plans to spread higher ticket prices over longer tenors. Compliance relies on standardized testing and digital registries, with the national standards authority publishing updated protocols that align with international norms to keep substandard imports out of the formal channel.

Local Manufacturing and Export-Oriented Capacity Expansion

Global brands and domestic manufacturers accelerated factory investments and joint ventures, focusing on product lines like refrigerators, ovens, and air conditioners, as part of Egypt’s repositioning as a supply hub for MENA and selected European destinations. The newest facilities target rising local-content ratios through component localization and supplier development, thereby reducing dollar exposure and aligning with rules-of-origin benefits under Egypt’s trade pacts for duty-free export into key partner markets. The National Industry Strategy (2024-2030) targets raising industrial GDP contribution from 14% to 20%, backstopped by a doubled EGP 45 billion (USD 942.6 million) Export Rebate Programme for FY2025-2026[3]Sherine Abdel-Razek, “2025 Yearender: Bridging the energy gap,” Sherine Abdel-Razek, english.ahram.org.eg. Administrative streamlining through special investment licensing and incentives has shortened permitting timelines for large greenfield projects and supported export rebates that reward higher efficiency standards and employment thresholds. Domestic champions expanded capacity and committed to higher export ratios, a strategy that helped absorb late-2025 inventory overhang and stabilized utilization while domestic sales slowed. This investment cycle elevates competition on features, quality, and after-sales, while deepening supplier ecosystems for key parts such as compressors and motors to raise local value capture over time.

Omnichannel and E-Commerce Growth with BNPL Enabling Big-Ticket Purchases

In 2025-2026, buy now pay later financing and regulated consumer finance became common, especially for significant purchases like home appliances, both in physical stores and online. Egypt witnessed a surge in buy now pay later transaction volumes, increasing from USD 1.26 billion in 2024 to an anticipated USD 4.74 billion by 2030. Online platforms and chain showrooms integrated buy now pay later services directly into their checkout processes. These providers offered zero-interest plans spanning 6 to 18 months, effectively reducing cart abandonment and increasing average order values for items like refrigerators, air conditioners, and washing machines. ValU, Egypt's top buy now pay later provider with a 25% market share, achieved a gross merchandise volume of EGP 16.5 billion (USD 345.6 million) in 2024. In March 2024, ValU introduced the ValU Card, transitioning the previously closed-loop merchant network to an open-loop system now accepted by Visa. Transactions via the ValU Card accounted for 30.7% of the total volume in FY2024. The average daily gross merchandise volume increased significantly, rising from EGP 25 million (USD 0.5 million) in FY2023 to EGP 44 million (USD 0.9 million) in FY2024[4]EFG Holding, “EFG Holding. Accessed February 19, 2026,” EFG Holding, efgholding.com. The introduction of open-loop BNPL cards extended usage beyond closed merchant networks, enabling financed payments at thousands of merchants and accelerating repeat purchases for connected appliances and accessories. Payments infrastructure scaled in parallel, with instant payments and broad offline acceptance through national payment aggregators that collect installment dues at neighborhood points of sale, expanding access beyond salaried urban consumers. Oversight rules that standardize disclosures, limit fees, and cap concentration help sustain expansion without overstretching household balance sheets, while channel partners benefit from higher conversion and deeper data on lifetime value.

Consumer Finance Penetration Under FRA-Regulated Installment Schemes

Formal financial inclusion climbed in 2024 on the back of mobile wallets, instant payments, and steady banking-system digitization, which together broadened the pool of consumers eligible for durable-goods financing in 2025-2026. The Central Bank of Egypt regulates banks and their consumer-finance subsidiaries, while the Financial Regulatory Authority supervises non-bank consumer finance firms under the durable-goods finance law, creating parallel rails that serve salaried and informal workers with tailored underwritingAppliance makers partner with banks and licensed financiers so buyers can split payments over 12-24 months for core categories like refrigerators, ACs, and washers through in-store terminals and online checkouts. Instant-payment rails and bill-collection networks support on-time settlement, while regulatory guidance promotes clear disclosures and supplier-linked financing to reduce misuse and direct borrowers toward authorized channels. A unified approach to data sharing and credit history across banks and non-banks is advancing under the regulators’ oversight, with phased implementations in 2026 designed to improve risk pricing and limit overextension.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Purchasing-power erosion from inflation and currency volatility | -1.3% | National, severe in rural Upper Egypt, and Delta governorates | Short to medium term (≤ 3 years) |

| FX availability and import-cost exposure for components | -0.6% | National, affects component-import-reliant assemblers | Medium term (2-4 years) |

| Grid load-shedding constrains energy-intensive usage | -0.4% | National, intermittent, based on seasonal demand | Short term (≤ 2 years) |

| Grey-market and unauthorized imports are pressuring formal channels | -0.5% | Border governorates, Red Sea ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Purchasing-Power Erosion from Inflation and Currency Volatility

Inflation remained elevated through 2024, compressing real incomes and forcing many households to delay big-ticket purchases into 2026 despite price promotions and installment offers. Currency volatility and the post-March 2024 exchange-rate reset increased the cost of imported components, constraining assemblers' ability to cut prices without sacrificing margins and reducing the assortment of certain higher-end models. Interest rates stayed tight until late 2025, and high-yield time deposits attracted household savings that would otherwise have supported replacement cycles for refrigerators, washing machines, and air conditioners. Industry associations reported late-2025 sales volume declines despite markdowns, reinforcing the view that the market’s 2026 recovery will rely on gradual disinflation, an improved rate environment, and maturing deposit instruments that return liquidity to consumption. Export-oriented production helped some manufacturers maintain capacity utilization, limiting layoffs and keeping after-sales networks intact as the domestic cycle reset.

FX Availability and Import-Cost Exposure for Components

Egypt’s flexible exchange-rate regime, adopted in March 2024, improved transparency in FX markets but translated currency moves into higher landed costs for imported components that still account for a large share of bill-of-materials in categories such as air conditioners and refrigerators. Net foreign reserves strengthened into late 2025, but component exposure remains a structural headwind until deeper localization of PCBs, compressor motors, and specialty materials materializes at scale. Larger multinationals managed hedging and supplier contracts through centralized treasury arrangements, while smaller assemblers faced wider bid-ask spreads during tight FX windows and chose narrower assortments to preserve working capital. Localization initiatives for compressor lines and refrigerator motors are scheduled to ramp in 2026, which can shave FX intensity and reduce pass-through risk to retail prices as local-content ratios rise. The net effect keeps pricing sensitive to the exchange rate in the near term, with import-cost pressures now a gating factor for product refreshes that rely on offshore parts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refrigerators Anchor, Dishwashers Accelerate on Premiumization

Refrigerators captured a 33.41% share in 2025, anchoring the category mix, as first-time buyers and upgraders prioritized cold-chain reliability and energy savings in urban and peri-urban homes. This position frames the Egypt major home appliances market share for large cold appliances within household baskets. Dishwashers remain a small base, but they are set to post the fastest 4.81% CAGR through 2031 as urban lifestyles, dual-income households, and premium kitchen renovations broaden the addressable audience in Greater Cairo and other large cities. New investments in Egypt by global brands are designed to serve both domestic and export demand for refrigerators, ovens, and dishwashers, helping smooth production runs through macroeconomic swings and improving feature availability in local stores. Washing-machine imports fell in 2025, a trend aligned with rising domestic production under local partnerships that scale volume and lift local-content ratios for mainstream configurations. In air conditioning, inverter penetration rose as energy prices increased, with makers leaning on SEER labeling and targeted marketing to nudge replacements in heat-prone districts and new housing projects.

Premium cookers, built-in ovens, and specialty dishwashers are benefiting from plant expansions that speed up product refreshes, tailor SKUs to local preferences, and support export models with harmonized compliance footprints across MENA and beyond. In parallel, domestic champions have introduced AI-enhanced cooking features and energy-saving controls in mainstream ranges to defend share and create step-up options without pricing out mass buyers. Feature-led differentiation, thoughtful price ladders, and firm installment offers define 2026 merchandising and align with how shoppers in the major home appliances industry in Egypt now weigh upfront costs against lifetime power bills. As domestic factories deepen product depth in core categories, retailers can deliver broader assortments without long lead times, which helps stabilize sell-through during seasonal peaks. The upgraded product build cadence, in turn, supports the export case for Egypt-made appliances to select African and Middle Eastern markets that share voltage, capacity, and regulatory profiles.

By Distribution Channel: E-Commerce Surges as BNPL Dissolves Upfront Barriers

Multi-brand and exclusive-brand stores accounted for 40.41% of the 2025 value, as experiential showrooms, installation services, and after-sales support enabled complex categories and quick fulfillment across Egypt’s main city clusters. Online platforms are growing fastest, at a 5.52% CAGR through 2031, as BNPL, instant payments, and mobile-first usage reshape how households source big-ticket appliances and coordinate delivery windows in dense neighborhoods. Chain retailers embedded installment terminals at checkout and on their websites, lifting conversion among shoppers targeting inverter ACs and larger refrigerators, where initial prices require financing support to close. The Egypt major home appliances market continues to blend store-led and digital journeys, with shoppers often researching energy labels and features online, then closing in-store to coordinate delivery, installation, and warranty services. These connected paths reduce returns, secure safer installations, and keep after-sales tied to authorized dealer networks that meet regulatory standards and preserve warranties.

Online marketplaces scaled in 2025 through direct integrations with licensed BNPL providers, improving cart conversion for refrigerators, air conditioners, washers, and built-in cooking packages with 6-12-month zero-interest offers. Payment rails and bill-collection points expanded reach into secondary cities and neighborhoods, enabling consumers to authorize and repay installments without visiting a bank branch, supporting diffusion beyond core, affluent districts. Brand-owned websites complement marketplace growth by offering curated assortments, bundles, and direct control over delivery and warranty, helping contain grey-channel substitution and protecting brand equity. As logistics density improves, channel margins should balance speed, installation complexity, and the financing offers needed to move higher-ASP items in 2026. This omnichannel rhythm positions the Egyptian major home appliances market for broader access to smart, connected options that rely on app onboarding and remote diagnostics.

Geography Analysis

Greater Cairo and Giza accounted for 37.62% of the 2025 value, reflecting dense retail footprints, high air-conditioning usage intensity, and strong adoption of omnichannel journeys that blend showroom service with BNPL-enabled e-commerce checkouts. Energy-sensitive buyers leaned into inverter ACs and efficient refrigerators as tariffs rose in 2024 and 2025, shifting category mixes toward SEER-labeled models and quick-install formats that balance up-front cost and running expenses. In 2026, better credit availability and steady digital payments are supporting renewed throughput in mainstream categories, with promotions and bundles timed to seasonal peaks in air conditioning and back-to-school purchase windows. The Egypt major home appliances market in Greater Cairo remains a bellwether for price discovery and feature-led merchandising that then cascades into secondary cities. Retailers continue to use store networks and online channels in tandem to serve complex installations and fast replacements.

Alexandria and the Mediterranean Coast are set to advance at a 5.05% CAGR to 2031, supported by hospitality and second-home developments that favor complete multi-appliance purchases and frequent replacements tied to seasonal usage. Local industrial zones and nearby plants accelerated output in 2025-2026, improving availability and supporting export flows while also reinforcing brand presence at coastal retail nodes. Port-city dynamics also require tighter enforcement to curb unauthorized imports, making customs oversight and energy-label compliance key tools for fair competition in formal channels. The Egypt major home appliances market is also benefiting from export-oriented capacity, which allows brands to right-size domestic allocations during shoulder seasons without creating stockouts. Dealer financing, BNPL partnerships, and on-site service arrangements help coastal clusters sustain premium product mixes in air conditioning and refrigeration.

The Nile Delta and Upper Egypt are more sensitive to macro and tariff conditions, which lengthens replacement cycles and keeps conventional formats prominent even as inverter and connected features improve their value propositions in 2026. Retailers and domestic makers lean on dense distributor networks and service points to maintain coverage and keep lifetime costs predictable, which matters more for price-conscious households during inflationary periods. In the Suez Canal and Sinai corridor, special economic zones and new capacity announcements drew added attention from global brands in 2025, bringing production, training centers, and showrooms closer to logistics hubs and hospitality customers. Commercial procurement in Red Sea governorates and resort areas remains a steady driver of premium-grade AC, commercial refrigeration, and dishwashers, creating a product mix skew that differs from national averages and favors after-sales density and uptime guarantees. Across regions, stronger import oversight and wider access to financing are common enablers for formal-channel growth as 2026 progresses.

Competitive Landscape

The Egyptian major home appliances market shows moderate concentration with active competition between local champions and multinational brands that expanded local manufacturing footprints and after-sales networks through 2025-2026. Strategic priorities center on vertical integration of key components, deeper localization to manage currency exposure, and export scaling to balance domestic cycles and capture regional opportunities. Global brands upgraded connected ecosystems and energy-saving features, while domestic leaders introduced AI-enabled functions in mainstream ranges to defend share and offer accessible step-ups through installment programs.

Announced investments in 2024-2026 include new or expanded plants for refrigerators, ovens, and dishwashers, as well as partnerships for compressors and motors that lift local content and bolster export competitiveness. Select brands reversed earlier divestment plans or restated growth targets for Egypt, signaling confidence in long-term fundamentals despite near-term consumer strain and FX pressures. Leading HVAC specialists deepened commercial engagement by opening new headquarters and training facilities to tap hospitality and strong residential demand along the Red Sea coast and in fast-growing new city districts.

Late-2025 pricing actions did not fully offset the demand shock from inflation and tight monetary policy, which prompted temporary production adjustments and a larger export push to absorb inventory. Policy proposals that lift tariffs on fully built imports while easing input duties could favor local assemblers and vertically integrated players if implemented, accelerating the shift from reliance on imports to domestic value capture. Compliance with national energy standards and serial-numbered customs registries remains a practical moat for incumbents, limiting grey-market substitution and ensuring official after-sales coverage in formal channels.

Egypt Major Home Appliances Industry Leaders

ELARABY Group

Electrolux Egypt

Fresh Electric

Unionaire Group Technology (UGT)

Kiriazi Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Electrolux Group reversed the divestment decision from July 2023 and retained Egyptian operations, which include brands such as Zanussi, Olympic Electric, and Ideal. This decision aims to leverage market growth, increase exports, and capitalize on the region's 90% customer satisfaction ratings, the highest globally.

- August 2024: Hisense, in partnership with the United Arab Emirates-based FBB Tech, started construction on a USD 38 million factory spanning 38,318 m². Located in the China-Egypt TEDA Suez Economic Zone, the factory is expected to produce 1.635 million television units annually, with plans to expand into white goods.

- September 2024: Haier Group began the second phase of the 200,000 m² ecological park in Egypt. The facility is projected to produce 300,000 refrigerator and freezer units annually by 2027, with a target of 60% local content. This initiative aligns with the existing 70% local-component ratio in air conditioners and partnerships with Taiwan's Rechi for compressors.

- September 2024: Beko invested USD 110 million to open an industrial park in Egypt, covering 114,000 m². In the first phase, the facility is expected to produce 1.5 million units annually, including refrigerators, ovens, and dishwashers. 60% of the output is planned for exports to the Middle East and North Africa region and Europe. The park incorporates LEED Gold sustainability design and includes the 31st global research and development center, which employs 50 engineers for regional product development.

Egypt Major Home Appliances Market Report Scope

Major domestic appliances (MDA), as they are commonly referred to in the industry, comprise large household electrical appliances used for core domestic functions such as food preservation, cooking, cleaning, and climate control. These typically include refrigerators, freezers, washing machines, dishwashers, cooktops and ranges, microwave ovens, air conditioners, and other large kitchen and home appliances, available in both freestanding and built-in formats.

The Egypt Major Home Appliances Market is segmented by product type, distribution channel, installation type, technology, and geography. By product type, the market is segmented into refrigerators, freezers, washing machines, dishwashers, cooktops & ranges, microwave ovens, air conditioners, and others (electric hobs). By distribution channel, the market is segmented into multi-brand and exclusive brand stores (EBOs), hypermarkets & supermarkets, online/e-commerce platforms, and direct-to-consumer (D2C) & subscription models. By installation type, the market is segmented into freestanding and built-in/integrated appliances. By technology, the market is segmented into conventional appliances and smart/connected appliances. By geography, the market is segmented into Greater Cairo & Giza, Alexandria & Mediterranean Coast, Nile Delta, Upper Egypt, Suez Canal & Sinai, and Red Sea Governorates. The report offers market size and forecasts for the Egypt Major Home Appliances Market in value (USD) for all the above segments.

By Product Type

| Refrigerators |

| Freezers |

| Washing Machines |

| Dishwashers |

| Cooktops & Ranges |

| Microwave Ovens |

| Air Conditioners |

| Other Major Home Appliances |

By Distribution Channel

| Multi-Brand and Exclusive Brand Stores (EBOs) |

| Hypermarkets & Supermarkets |

| Online / E-commerce Platforms |

| Direct-to-Consumer (D2C) & Subscription Models |

By Geography

| Greater Cairo & Giza |

| Alexandria & Mediterranean Coast |

| Nile Delta |

| Upper Egypt |

| Suez Canal & Sinai |

| Red Sea Governorates |

| By Product Type | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Cooktops & Ranges | |

| Microwave Ovens | |

| Air Conditioners | |

| Other Major Home Appliances | |

| By Distribution Channel | Multi-Brand and Exclusive Brand Stores (EBOs) |

| Hypermarkets & Supermarkets | |

| Online / E-commerce Platforms | |

| Direct-to-Consumer (D2C) & Subscription Models | |

| By Geography | Greater Cairo & Giza |

| Alexandria & Mediterranean Coast | |

| Nile Delta | |

| Upper Egypt | |

| Suez Canal & Sinai | |

| Red Sea Governorates |

Key Questions Answered in the Report

What is the current size and growth outlook of the Egypt major home appliances market?

The Egypt major home appliances market size was USD 2.72 billion in 2025 and is projected to reach USD 3.43 billion by 2031 at a 3.92% CAGR through 2031. Growth reflects a pivot to local manufacturing, export scaling, and installment-led retail recovery.

Which product categories lead demand in Egypt and which are growing fastest?

Refrigerators led with 33.41% share in 2025, while dishwashers are set to grow the fastest at a 4.81% CAGR through 2031 as premium kitchens and dual-income households expand in urban clusters.

How is e-commerce influencing appliance purchases in Egypt in 2026?

E-commerce is the fastest-growing channel, with a 5.52% CAGR, driven by BNPL and instant payments integrated at checkout, while omnichannel retailers offer installation, warranty coverage, and in-store pickup to manage complex deliveries.

What factors are pushing consumers toward inverter and efficient models?

SEER energy labels introduced in 2025 and higher electricity tariffs are nudging replacements toward inverter ACs and efficient refrigerators, supported by clear energy claims and installment plans that ease up-front cost gaps.

Where is regional growth strongest within Egypt?

Alexandria and the Mediterranean Coast are projected to post the fastest 5.05% CAGR in hospitality demand and second-home developments through 2031, while Greater Cairo remains the largest region by value, with a 37.62% share in 2025.

Which strategies define competition among leading brands in Egypt?

Leaders focus on vertical integration and local manufacturing to reduce FX risk, build export momentum, and differentiate through connected ecosystems and energy efficiency, while leveraging installment financing to drive sell-through.

Page last updated on: