Dextrose Monohydrate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.95 Billion |

| Market Size (2031) | USD 6.41 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

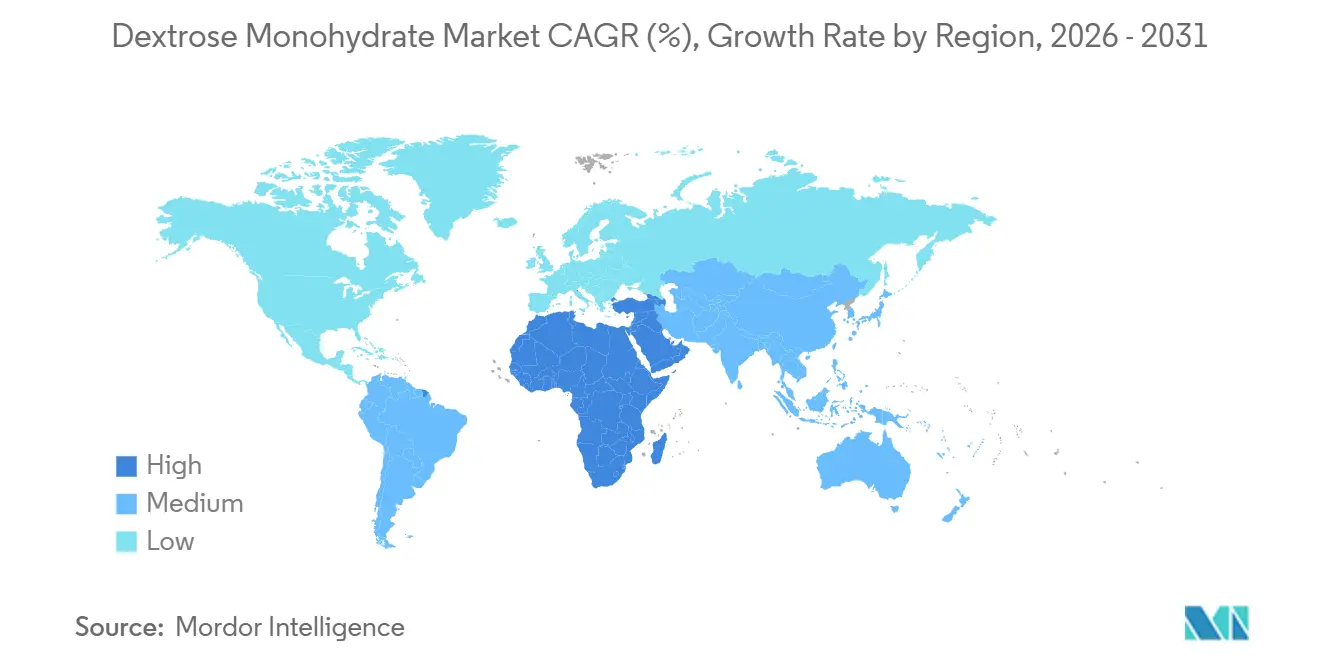

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

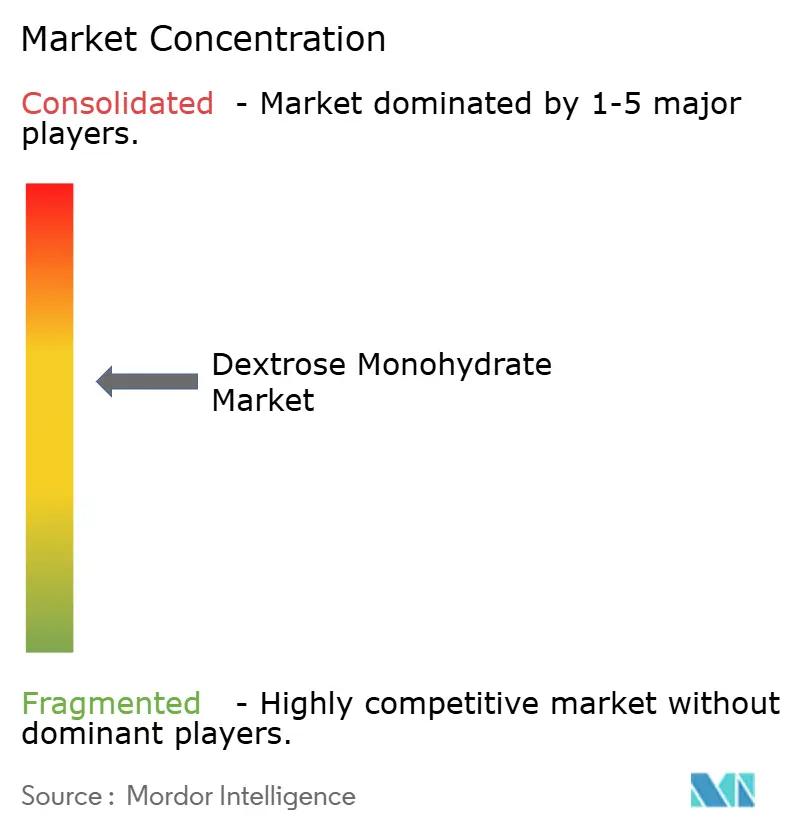

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dextrose Monohydrate Market Analysis by Mordor Intelligence

The dextrose monohydrate market is projected to reach USD 4.71 billion by 2025, USD 4.95 billion by 2026, and USD 6.41 billion by 2031, with a CAGR of 5.31% from 2026 to 2031. Growth is supported by the ingredient's dual functionality: reducing recipe costs in processed foods while complying with strict compendial standards for parenteral nutrition. Increased investment in regional starch production and the alignment of United States Pharmacopeia (USP), European Pharmacopeia (EP), British Pharmacopeia (BP), and Japanese Pharmacopeia (JP) monographs have streamlined formulation processes, boosting pharmaceutical demand. Feedstock diversification, including corn, wheat, and cassava, helps manage cost fluctuations; however, energy price inflation and limited availability of non-GMO corn continue to impact margins in Europe. Mergers and acquisitions indicate that market players are diversifying with sugar-reduction portfolios and expanding geographically, increasing competition while enhancing supply chain resilience in the global dextrose monohydrate market.

Key Report Takeaways

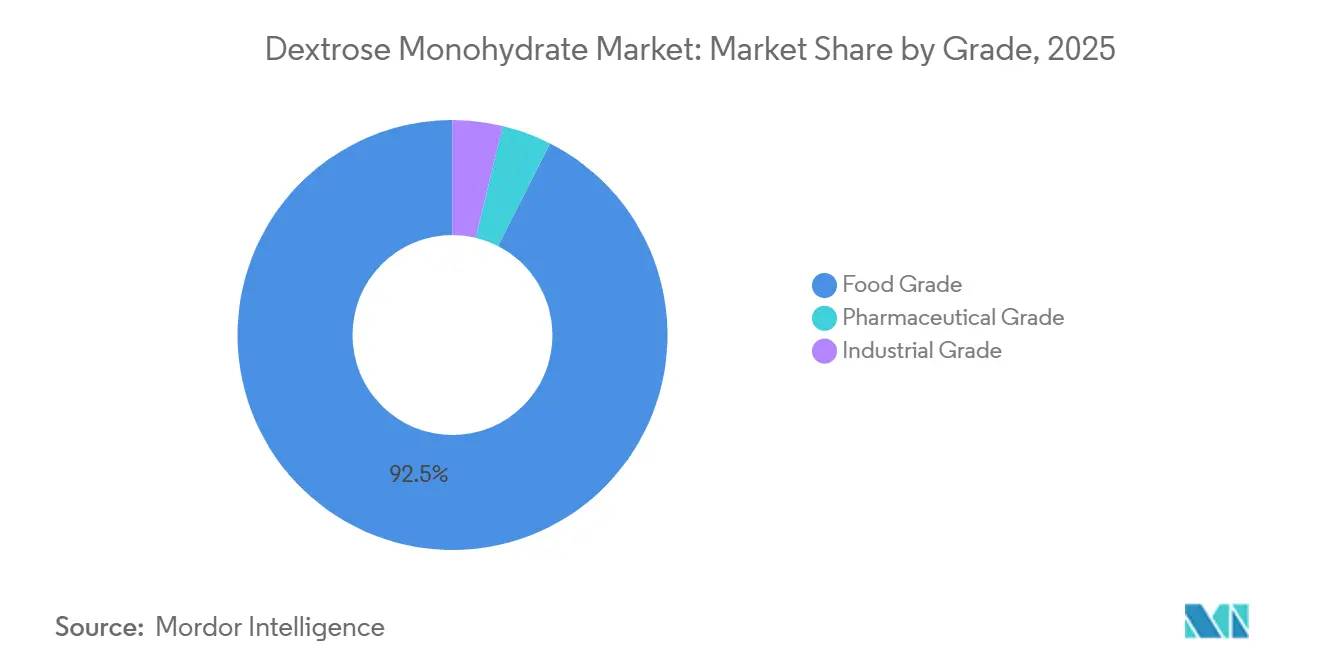

- By grade, food-grade material dominated with 92.50% share in 2025; pharmaceutical grade is advancing at a 6.21% CAGR to 2031 on rising parenteral nutrition volumes.

- By source, corn-based supply held 78.25% of the 2025 dextrose monohydrate market size, yet wheat-based output is forecast to expand at 6.13% CAGR to 2031 as EU processors pivot toward locally available wheat starch.

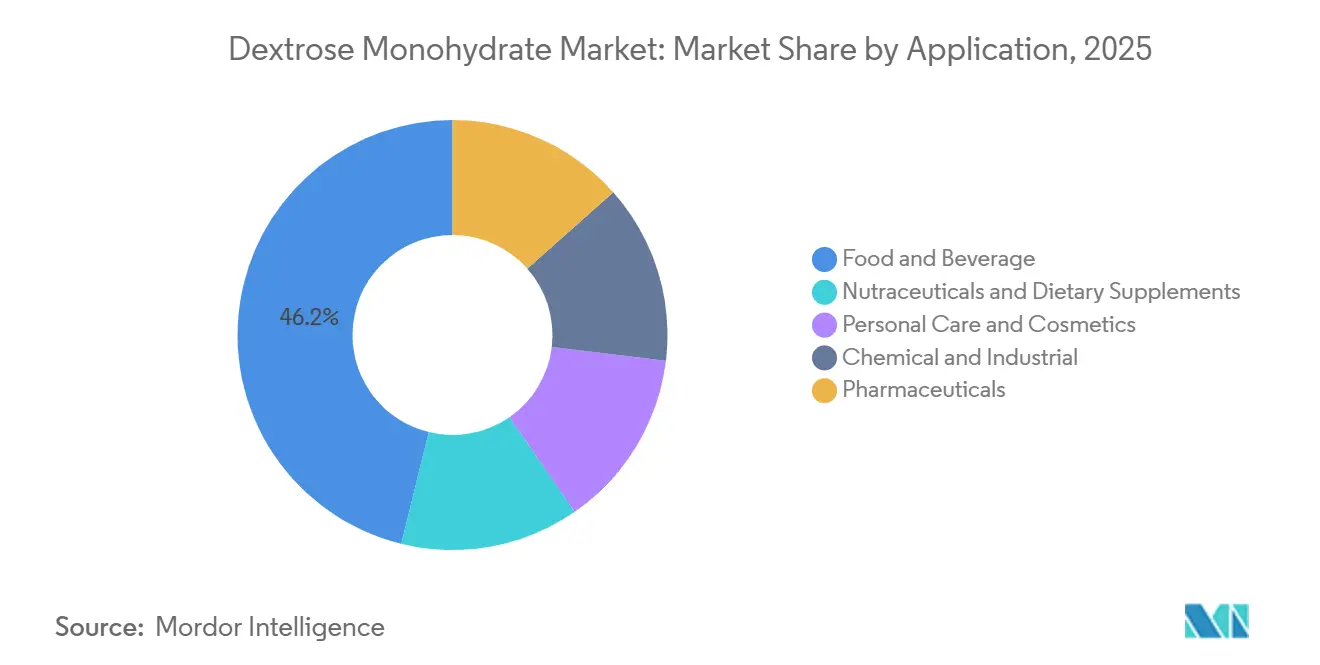

- By application, food and beverage accounted for 46.17% of 2025 demand, whereas nutraceuticals are projected to rise at 6.34% CAGR between 2026 and 2031 on the back of sports nutrition formulations.

- By geography, Asia-Pacific led with 41.40% of the 2025 dextrose monohydrate market share, while the Middle East & Africa is forecast to grow at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dextrose Monohydrate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from food and beverage manufacturers (clean-label sweetening) | +1.2% | Global, with premium uptake in North America & EU | Medium term (2-4 years) |

| Rapid uptake in parenteral nutrition and injectable biologics | +1.5% | Global, led by North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Expansion of processed-food capacity in emerging economies | +1.3% | APAC core, spill-over to MEA and South America | Long term (≥4 years) |

| Cost-effective bulking and browning alternative to sucrose | +0.8% | Global | Short term (≤2 years) |

| Formulation uptake in plant-based meat analogues | +0.6% | North America, EU, APAC urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Food and Beverage Manufacturers (Clean-Label Sweetening)

Organic and non-genetically modified organism (non-GMO) certified variants are increasingly prioritized by retailers due to their clear ingredient panels. These variants maintain premiums of 20%-50%, driven by limited certified acreage and long-term specialty grain contracts that secure supply for several seasons[1]Biostarch, “Organic Dextrose Unveiled,” bio-starch.com. With solubility near 100 grams per 100 milliliters (g/100 mL) and approximately 70% sucrose sweetness, these products enable formulators to partially replace sucrose without compromising texture, supporting their use in organic bakery products, powdered beverages, and sports gels. The complexity of procurement related to traceability and certification acts as a barrier, protecting premium positions from competition with commodity alternatives. Medium-term growth in the dextrose monohydrate market will rely on scaling certified feedstock and reformulations by mainstream brands, ensuring sustained market expansion.

Rapid Uptake in Parenteral Nutrition and Injectable Biologics

Compendial alignment under United States Pharmacopeia (USP), European Pharmacopeia (EP), British Pharmacopeia (BP), and Japanese Pharmacopeia (JP) regulations has streamlined cross-border sourcing processes. Fresenius Kabi offers parenteral bags containing 63 grams to 165 grams of dextrose monohydrate, indicating consistent demand for high-purity products[2]Fresenius Kabi, “Parenteral Nutrition Portfolio,” fresenius-kabi.com. This excipient also plays a key role in stabilizing lyophilized biologics and supporting cell-culture fermenters. The aging populations in North America, Europe, and East Asia are driving increased infusion volumes, contributing to the long-term growth potential for pharmaceutical-grade dextrose monohydrate in the market.

Expansion of Processed-Food Capacity in Emerging Economies

Greenfield plants in Vietnam, India, and Egypt highlight the increasing adoption of starch-based sweeteners. TH Group’s VND 6,000 billion (USD 0.22 billion) clean-food complex and Sanstar’s 2,100 tons per day maize expansion provide dedicated dextrose streams for both domestic and export markets. Additionally, Cairo 3A’s USD 150 million initiative aims to establish Egypt as a regional supplier of pharmaceutical-grade dextrose. These developments are concentrated in economies with rising disposable incomes, supporting sustained volume growth in the dextrose monohydrate market.

Cost-Effective Bulking and Browning Alternative to Sucrose

With a sweetness level of 70-75% compared to sucrose, dextrose helps reduce recipe costs while supporting Maillard browning, which enhances crust formation and aroma in bakery products. Its neutral flavor and high solubility enable seamless substitution during production without requiring equipment modifications, facilitating adoption in cost-sensitive operations. However, energy price inflation affects final profit margins, linking short-term adoption to the hedging capabilities of processors.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over excessive sugar intake and obesity regulations | -1.0% | Global, most acute in North America & the EU | Medium term (2-4 years) |

| Proliferation of high-intensity/rare sugars (stevia, allulose, monk-fruit) | -0.9% | Global, led by North America, Europe, and the Asia-Pacific | Long term (≥4 years) |

| Volatility in corn and wheat starch feedstock prices | -0.8% | Global, particularly acute in import-dependent regions | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over Excessive Sugar Intake and Obesity Regulations

The United States Department of Agriculture's (USDA) 2025-2030 Dietary Guidelines set the recommended limit for added sugars to below 6% of total calorie intake, while the World Health Organization (WHO) recommends a free-sugar intake of less than 5%. European sugar taxes and mandatory front-of-pack labeling are designed to reduce the use of caloric sweeteners. These policies are expected to impact discretionary categories, such as confectionery and sodas, thereby influencing short-term demand in the dextrose monohydrate market.

Proliferation of High-Intensity/Rare Sugars

Stevia, allulose, and monk fruit collectively account for over USD 2.8 billion, growing at a compound annual growth rate (CAGR) of 5-7%, and are increasingly replacing sugar in reduced-sugar formulations. Ingredion's near-complete acquisition of PureCircle highlights starch processors diversifying across sweetener categories. However, the World Health Organization's (WHO) 2023 advisory on non-nutritive sweeteners introduces uncertainty, potentially affecting adoption rates and providing partial support to the dextrose monohydrate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Pharma Purity Drives Premium Growth

The pharmaceutical-grade segment is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.21%, exceeding the overall dextrose monohydrate market, driven by the expansion of parenteral nutrition programs in hospitals and the development of biologic pipelines. Food-grade dextrose monohydrate is expected to account for 92.50% of the market share by 2025 but faces challenges due to increasing sugar-reduction trends. Industrial-grade demand remains stable, supported by its cost advantages in fermentation and textiles, particularly in regions with less stringent regulatory requirements. The introduction of Cairo 3A’s Pharma Copia-certified production lines in Egypt highlights the emergence of regional hubs aiming to meet growing infusion demand.

Pharmaceutical-grade buyers prioritize batch-to-batch consistency and compliance with multiple compendial standards, which helps stabilize prices against commodity market fluctuations. In contrast, food-grade buyers must balance the premium for clean-label products with the competitive pressure from natural high-intensity sweeteners. This dynamic reflects a two-speed growth pattern within the broader dextrose monohydrate market.

By Source: Wheat Gains as Non-GMO Corn Tightens

Corn accounts for 78.25% of the global supply, enabling economies of scale in regions such as the Americas and Asia. However, the limited availability of non-genetically modified organism (non-GMO) corn in Europe and increasing energy costs are driving a shift toward wheat starch, with wheat-based production projected to grow at a CAGR of 6.13% through 2031. Tereos currently sources 68.6% of its feedstock from wheat for its sweetener division, and its 150,000 tons per year offtake agreement with Futerro ensures diversification of its output channels.

Cassava- and potato-based dextrose are emerging as niche but expanding segments, valued for their allergen-free and gluten-free attributes. Amafil’s investment of ZAR 50 million (USD 2.96 million) in a cassava processing plant in Paraná highlights Latin America’s efforts to diversify feedstock and enhance local value addition. Feedstock diversification is increasingly viewed as a strategic approach to mitigate raw material supply disruptions and sustain the dextrose monohydrate market.

By Application: Nutraceuticals Outpace Traditional Food Use

The food and beverage segment accounted for 46.17% of the projected 2025 share, while sports-focused nutraceuticals are growing at a CAGR of 6.34%. Products such as electrolyte gels and recovery drinks utilize dextrose’s glycemic index of 100 to restore glycogen, increasing demand for organic variants with higher price points. Pharmaceutical applications are expanding with the scaling of biologics, and personal care products use dextrose as a humectant in leave-on formulations. This functional versatility supports resilience across the dextrose monohydrate market.

Industrial applications, including fermentation substrates and paper sizing, remain price-sensitive yet stable, absorbing capacity during periods of reduced demand in food applications. As the use of natural sweeteners increases, dual-use formulations combining dextrose with alternatives like stevia or allulose are expected to influence future product development strategies.

Geography Analysis

Asia-Pacific is projected to account for 41.40% of the 2025 dextrose monohydrate market size, driven by significant investments in starch production across China, India, and ASEAN (Association of Southeast Asian Nations) countries. Examples include TH Group’s VND 6,000 billion (USD 0.22 billion) complex and Sanstar’s 2,100 tons per day maize plant, which highlight vertical integration strategies to secure local sweetener supply. Additionally, cross-border trade facilitated by the Regional Comprehensive Economic Partnership (RCEP) enhances ingredient flow, while urban dietary shifts favor packaged foods.

India's dextrose monohydrate market has seen increased activity following Riddhi Siddhi’s acquisition of Cargill’s 300,000 tons per year wet-milling asset for INR 2,500 million (USD 26.81 million). This move reintroduces Riddhi Siddhi into a market historically dominated by Roquette, intensifying competition and adding new production capacity to South Asia’s market landscape.

North America and Europe continue to serve as key markets for clean-label and pharmaceutical-grade dextrose monohydrate. Ingredion’s USD 100 million expansion in Indianapolis and its joint venture with Agrana in Romania ensure proximity to wheat and specialty starch customers. However, rising energy costs and sugar tax policies are reducing demand for traditional sugary beverages, prompting formulators to explore blended sweetener systems.

The Middle East and Africa are expected to achieve the fastest growth in the dextrose monohydrate market, with a forecasted CAGR of 6.18%. Cairo 3A’s Pharma Copia-certified production lines in Egypt, along with ISO 22000 compliance, are improving local production quality and reducing reliance on imports.

South America, led by Brazil’s focus on cassava, is contributing to feedstock diversification in the global dextrose monohydrate market. This diversification helps mitigate risks associated with dependence on single-crop sources, providing greater stability to the market.

Competitive Landscape

The dextrose monohydrate market is moderately concentrated, with the top five companies: Ingredion, Roquette, ADM, Tereos, and Cargill. Ingredion has allocated a capital expenditure of USD 400-440 million for 2026, part of which is directed toward expanding texture-solution lines beyond corn sweeteners. Additionally, its integration of PureCircle provides a strategic advantage in sugar-reduction solutions.

Tereos is investing EUR 800 million (USD 927.08 million) in decarbonization initiatives to attract environmentally conscious customers, while its partnership with Futerro secures industrial-grade production volumes. Roquette is expanding its wheat processing capacity to address non-genetically modified organism (non-GMO) requirements and has implemented efficiency upgrades aimed at reducing gas consumption by 12% by 2025. Meanwhile, Riddhi Siddhi’s acquisition of assets highlights increasing regional competition in India.

Smaller processors are focusing on differentiation through organic or cassava-based variants, which command price premiums of 20-50%. However, the limited availability of certified acreage constrains supply, maintaining price disparities. Advanced hedging strategies further distinguish market leaders from smaller players, as volatility in corn and gas prices continues to shape the tiered structure of the dextrose monohydrate market.

Dextrose Monohydrate Industry Leaders

ADM

Cargill

Roquette Frères

Tereos

Ingredion

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: TH Group initiated the construction of a clean-food plant in Vietnam with an investment of VND 6,000 billion (USD 0.22 billion). The facility is expected to add 852,351 tons per year of production capacity for processed foods and ingredient fractions, including Dextrose Monohydrate, which is widely used in food, beverage, and pharmaceutical applications.

- January 2026: Riddhi Siddhi Gluco Biols acquired Cargill India’s 300,000 tons per year Davangere starch plant for INR 250 crore (USD 30 million). This acquisition marks its re-entry into corn wet-milling after a decade. The facility is expected to enhance the production of starch derivatives, including Dextrose Monohydrate, and strengthen its position in the South Asian market.

Global Dextrose Monohydrate Market Report Scope

Dextrose monohydrate is a purified, crystalline form of D-glucose (Dextrose-Glucose) obtained from corn or potato starch. It is used as a fast energy source, sweetener, and binder in food and pharmaceutical applications. Additionally, it is utilized to treat low blood sugar (hypoglycemia), support hydration, and address severe physical fatigue.

The dextrose monohydrate market is segmented by grade, source, application, and geography. By grade, the market is segmented into food grade, pharmaceutical grade, and industrial grade. By source, the market is segmented into corn-based, wheat-based, and other starch sources (cassava, tapioca, potato). By application, the market is segmented into food and beverage, pharmaceuticals, nutraceuticals and dietary supplements, personal care and cosmetics, and chemical and industrial. The report also covers the market size and forecasts for dextrose monohydrate in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Food Grade |

| Pharmaceutical Grade |

| Industrial Grade |

| Corn-based |

| Wheat-based |

| Other Starch Sources (cassava, tapioca, potato) |

| Food and Beverage |

| Pharmaceuticals |

| Nutraceuticals and Dietary Supplements |

| Personal Care and Cosmetics |

| Chemical and Industrial |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Food Grade | |

| Pharmaceutical Grade | ||

| Industrial Grade | ||

| By Source | Corn-based | |

| Wheat-based | ||

| Other Starch Sources (cassava, tapioca, potato) | ||

| By Application | Food and Beverage | |

| Pharmaceuticals | ||

| Nutraceuticals and Dietary Supplements | ||

| Personal Care and Cosmetics | ||

| Chemical and Industrial | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the dextrose monohydrate market in 2031?

The Dextrose Monohydrate Market size is expected to grow from USD 4.71 billion in 2025 to USD 4.95 billion in 2026 and is forecast to reach USD 6.41 billion by 2031 at 5.31% CAGR over 2026-2031.

Which region holds the largest share today?

Asia-Pacific accounts for 41.40% of 2025 market share, making it the largest regional contributor.

Why is pharmaceutical-grade demand growing faster than food grade?

Hospital parenteral nutrition growth and biologics pipelines require multi-compendial, high-purity dextrose, driving a 6.21% CAGR for pharma-grade volumes.

How are processors mitigating corn price volatility?

Leading firms hedge grain and energy exposure, diversify into wheat or cassava starch, and sign long-term offtake agreements to stabilize input costs.

Page last updated on: