Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

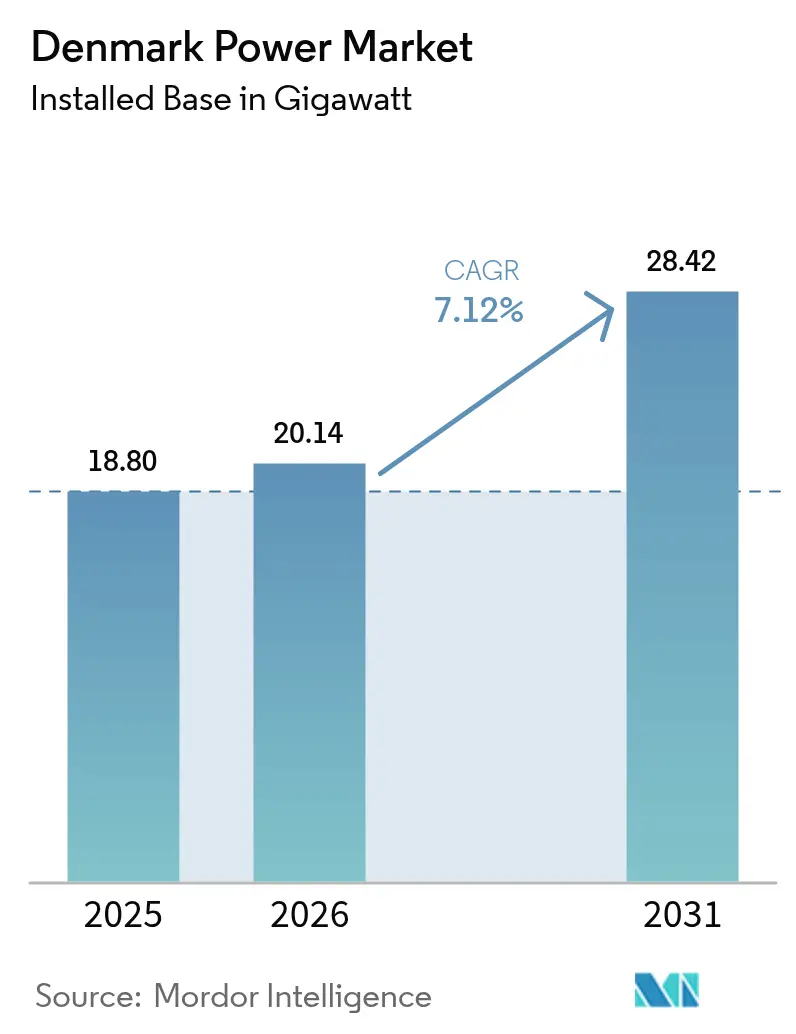

| Base Year Market Size (2025) | 18.80 gigawatt |

| Market Volume (2026) | 20.14 gigawatt |

| Market Volume (2031) | 28.42 gigawatt |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

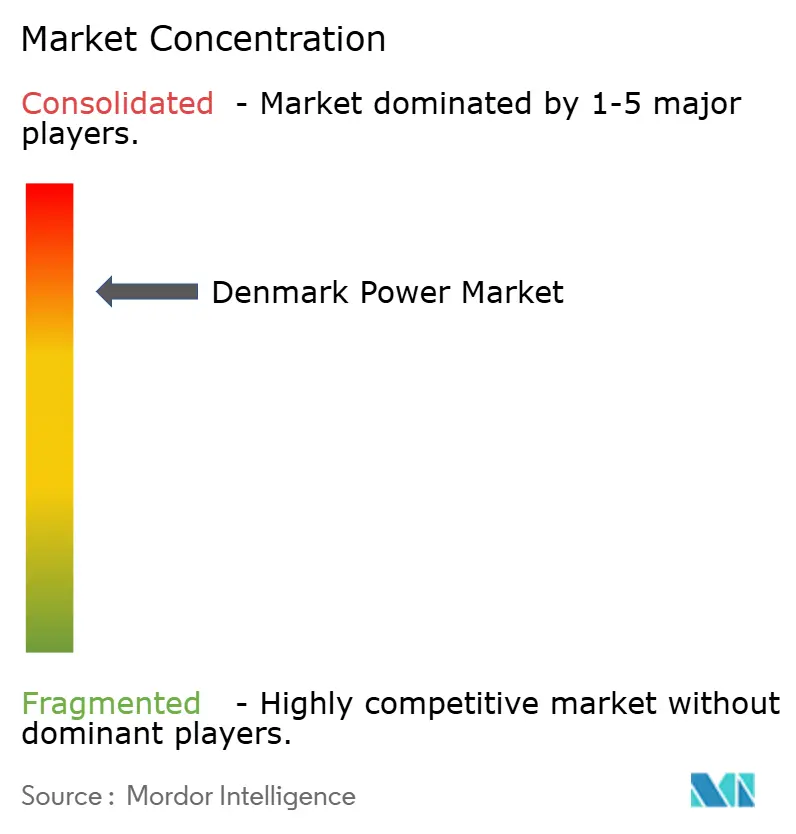

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Power Market Analysis by Mordor Intelligence

The Denmark Power Market size is expected to grow from 18.80 gigawatt in 2025 to 20.14 gigawatt in 2026 and is forecast to reach 28.42 gigawatt by 2031 at 7.12% CAGR over 2026-2031.

Growth is propelled by government-backed offshore wind tenders, rapid corporate renewable procurement, and the country’s emerging role as a Power-to-X export hub. Investments in grid digitalization, hybrid renewable installations, and battery storage keep momentum high even as onshore siting constraints tighten.[1]Danish Energy Agency, “Monthly Electricity Statistics,” ens.dk The Denmark power market already integrates 58.7% wind in its generation mix, turning the grid into a living laboratory for flexible technologies and cross-border energy trade, Danish Energy Agency. Industrial electrification and data-center expansion add fresh demand, while large-scale energy-island projects promise surplus-power exports to mainland Europe. Policymakers continue to align carbon taxes, permitting reforms, and interconnector funding, reducing investor risk and underpinning the Denmark power market’s long-term trajectory.[2]International Energy Agency, “Denmark 2024 Energy Policy Review,” iea.org

Key Report Takeaways

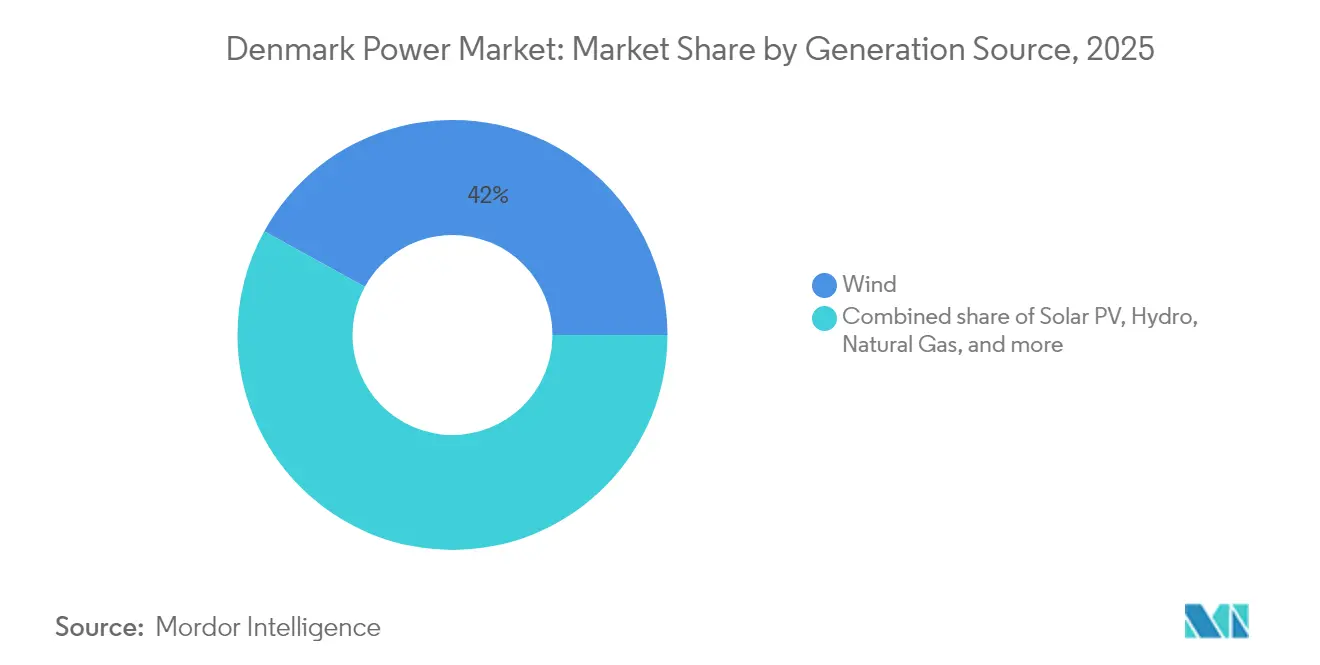

- By generation source, wind power led with 41.98% revenue share in 2025; solar PV is projected to expand at a 8.74% CAGR to 2031, securing the fastest-growing slot in the Denmark power market.

- By end user, the utilities segment held 59.35% of the Denmark power market share in 2025; the commercial and industrial segment records the highest projected CAGR at 8.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of renewable energy targets | +1.2% | North Sea regions | Medium term (2-4 years) |

| Rising corporate PPAs and green procurement | +0.8% | Hovedstaden, Midtjylland | Short term (≤ 2 years) |

| Accelerated offshore wind tender pipeline | +1.5% | North Sea coast, Bornholm Energy Island | Long term (≥ 4 years) |

| Electrification of district heating networks | +0.7% | Copenhagen metropolitan area | Medium term (2-4 years) |

| EU-mandated coal phase-out deadlines | +0.6% | Legacy thermal plant regions | Short term (≤ 2 years) |

| Surplus-power-to-e-fuels demand pull | +0.9% | Western Denmark | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration of Renewable Energy Targets

Sector coupling, storage, and 18 GW of planned offshore wind capacity make system-wide optimization the backbone of Denmark’s decarbonization model. Market Model 3.0 clarifies ownership rules for grid-supporting assets, unlocking private finance for batteries, hydrogen electrolyzers, and flexible demand. Surplus output during high-wind hours is increasingly steered into export lines, district-heating boilers, or Power-to-X plants, helping the Denmark power market reduce curtailment and stabilize prices.

Rising Corporate PPAs and Green Power Procurement

Denmark’s transparent certificate regime and stable contracts draw global brands into long-term PPAs. Better Energy’s 12 additional deals in 2024 and Bloomberg’s 15-year agreement with Ørsted exemplify a shift from compliance-driven buying toward strategic carbon-footprint control. [3]Better Energy, “Annual Report 2024,” betterenergy.com This pipeline secures predictable cash flows for new renewable capacity and strengthens the Denmark power market against wholesale price volatility.

Accelerated Offshore Wind Tender Pipeline

Tenders emphasizing innovation and hybrid energy-island integration differentiate Denmark from pure lowest-cost auctions. The 6 GW program ties capacity awards to Power-to-X readiness and local supply-chain content, encouraging novel cable, converter, and floating-foundation solutions. RWE’s Thor project, backed by a EUR 1.2 billion EIB loan, signals confidence that the Denmark power market can scale these concepts to commercial reality.

Electrification of District Heating Networks

HOFOR and Danfoss have begun data-centric pilot schemes where heat pumps modulate consumption to soak up excess renewable generation, tightening sector coupling. With half of Danish heat delivered via district systems, electrification adds a sizable, controllable load that supports grid balance while lowering urban emissions.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion in Western Denmark | -0.8% | Jutland peninsula | Short term (≤ 2 years) |

| Limited onshore siting and local opposition | -0.5% | Rural areas | Medium term (2-4 years) |

| Long lead-times for sub-sea HV cables | -1.1% | Offshore wind areas, interconnectors | Long term (≥ 4 years) |

| Scarcity of skilled wind-turbine technicians | -0.6% | Offshore regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion in Western Denmark

Wind-rich Jutland often produces more power than its lines can carry eastward, triggering curtailment and undermining new-build economics. Energinet’s 172 km West Coast Connection will ease some pressure, yet completion stretches into the late 2020s, placing a near-term ceiling on renewable buildouts.[4]Energinet, “West Coast Connection Project Update,” energinet.dk

Long Lead-Times for Sub-Sea HV Cables

Global demand for XLPE and HVDC export cables has stretched delivery slots past four years. Denmark’s energy-island vision hinges on timely cable availability, so developers lock contracts early, tying up capital and complicating risk profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Generation Source: Wind Dominance Drives Grid Innovation

Wind’s 41.98% share in 2025 underlines its position as the anchor of the Denmark power market. The upcoming North Sea energy-island hub and incremental offshore rounds push installed wind beyond 18 GW by 2030. Solar’s 8.74% CAGR balances daytime generation, especially where rooftop PV feeds urban substations. The Denmark power market size for wind is projected to widen further as hybrid layouts pair turbines, batteries, and electrolysers near Bornholm, damping variability and opening revenue from ancillary services.Biomass and biogas keep a near-steady output by leveraging agricultural residues and district-heating compatibility. Gas and oil assets drop into reserve mode, supplying inertia and black-start capability when the wind calms. With coal fully retired, the Denmark power industry prioritizes grid-forming inverters, synchronous condensers, and battery-based virtual inertia, ensuring stable frequency without fossil plants.

By Transmission & Distribution Infrastructure: Smart Grid Transformation

High-voltage transmission infrastructure is booming, reflecting Denmark's focus on grid backbone development to support renewable energy integration and regional interconnection. Smart metering infrastructure is rapidly growing, driven by regulatory mandates and consumer demand for energy management capabilities. Medium-voltage distribution networks require substantial upgrades to accommodate distributed generation and electric vehicle charging infrastructure, creating sustained investment opportunities. Low-voltage systems face increasing complexity from bidirectional power flows and prosumer integration, necessitating advanced control systems and monitoring equipment.

Transmission line investments prioritize offshore wind integration and cross-border interconnection capacity, with projects like the Viking Link enhancing Denmark's role as a regional energy hub Energinet. Substations and transformer upgrades focus on grid flexibility and renewable integration capabilities, incorporating advanced power electronics and control systems. The smart grid transformation encompasses infrastructure hardware and digital systems, creating opportunities for technology providers and system integrators. Grid digitalization enables new business models and services, from peer-to-peer energy trading to grid-scale optimization algorithms.

By End-User Consumption: Utilities Dominance Meets Commercial Electrification

Utilities handled about 59.35% of Denmark’s electricity use in 2025, mirroring an integrated system where transmission and distribution companies operate the grid and oversee wholesale trading. Their share grows as they modernize networks, add digital controls, and earn new income from grid-support services.

The spotlight, however, is shifting toward businesses. Electricity use in the commercial and industrial segments is rising at an 8.12% CAGR through 2031, a pace driven by firms swapping fossil-fuel equipment for electric alternatives and locking in long-term renewable power deals. Data centers sit at the heart of this surge: they create dense, round-the-clock loads that need tailor-made connections and guaranteed green supply. Households show a steadier demand line. Efficiency upgrades, smarter appliances, and widespread heat pump adoption keep residential consumption flat even as the population edges higher. Altogether, these shifts push Denmark’s grid toward a smarter, more flexible future where demand response, sector coupling, and rapid renewables growth work in tandem to deliver a low-carbon power system.

Geography Analysis

Denmark’s five NUTS-2 regions form an increasingly meshed network rather than isolated load pockets. Hovedstaden alone accounted for 38.10% of demand in 2025, underpinned by the Copenhagen metro’s advanced manufacturing and digital services sectors. Sjælland’s 7.43% CAGR signals a pivot as new 220 kV circuits tie Bornholm’s offshore hub into Zealand’s mainland grid, turning the island into a generation and hydrogen-export staging zone.Midtjylland and Nordjylland secure the lion’s share of onshore and near-shore turbines, yet they grapple with wind-linked congestion. Ongoing 132 kV reinforcements and synchronized curtailment platforms seek to unblock power flows to east-coast load centers, ensuring the Denmark power market can absorb incremental renewable builds without destabilization.Syddanmark blends biomass co-generation, port-side green-ammonia pilots, and heavy-industry consumption. Cross-border capacity with Germany brings price triangulation and arbitrage opportunities, while the Øresund link positions Hovedstaden as a balancing node between the Nordic and continental zones. Together, these geographic dynamics underscore how the Denmark power market is maturing from a domestic supply system into a regional trading and flexibility platform.

Competitive Landscape

First-tier players hold sizable but not monopolistic positions, creating a concentrated arena where innovation counts. Ørsted eclipsed 10 GW of operating offshore wind in 2025, pairing assets with co-located batteries and entering selective project exits when risk profiles widened. Vestas supplied 17 GW of turbines in 2024 and is evolving service contracts into subscription-based performance packages. Vattenfall and RWE lean on integrated generation-to-retail models, seizing hybrid tender slots that reward storage and green-hydrogen attachments.

Mid-tier developers such as Better Energy and Eurowind diversify through solar-plus-storage farms and behind-the-meter PPA structures that anchor financing without merchant-price exposure. Grid-tech vendors—ABB, Siemens Grid Software, Hitachi Energy—embed virtual inertia and synthetic-grid services, selling value-added O&M that widens revenue per megawatt installed. The Denmark power industry also hosts niche specialists: Topsoe’s SOEC electrolyzers position it to capture Europe’s green-hydrogen wave, while NKT’s factory expansion enhances cable supply security for domestic and export projects.

Competition now turns on data leverage and lifecycle optimization. Predictive analytics cut turbine downtime, while algorithmic trading monetizes forecast accuracy across Nord Pool and GB hubs. Firms combining asset ownership, digital IP, and flexible-market access are set to secure disproportionate profit, keeping the Denmark power market technology-driven and globally relevant.

Denmark Power Industry Leaders

Ørsted A/S

Vattenfall A/S

Energinet (TSO)

European Energy A/S

Better Energy A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Eurowind Energy deployed one of Denmark’s largest battery storage systems at a hybrid plant, enhancing grid flexibility in Skive, a hybrid power plant harnesses both wind and solar energy. With a capacity of 45 MWh and a 2-hour duration, this Battery Energy Storage System (BESS) bolsters grid flexibility and stability, facilitating the seamless integration of renewable energy into the grid.

- February 2025: Vestas noted a record 17 GW orders in 2024 and announced a DKK 0.55 dividend and EUR 100 million share buyback.

- January 2025: Hitachi Energy won a STATCOM contract for Hornsea 4, marking Europe’s first offshore technology deployment.

- December 2024: HOFOR and Danfoss launched an analytics project to optimize Copenhagen’s district heating grid.

Denmark Power Market Report Scope

Power generation is generated through various primary sources such as coal, hydro, solar, thermal, etc. In utilities, it's a step before its delivery to its end users. Then the process is followed by transmission and distribution. Under this, the power generated is distributed via high-voltage lines (transmission lines) and low-voltage lines (distribution lines) as per the requirement of the end user.

The Denmark power market is segmented by generation and power transmission & distribution (T&D). The market is segmented by generation into wind, solar, coal, and other sources. Each segment's market sizing and forecasts are based on installed gigawatts (GW) capacity.

Generation (by Power Source)

| Wind (Onshore and Offshore) |

| Solar PV |

| Biomass and Biogas |

| Hydro |

| Coal |

| Natural Gas and Oil |

End-User Consumption

| Utilities |

| Commercial and Industrial |

| Residential |

| Generation (by Power Source) | Wind (Onshore and Offshore) |

| Solar PV | |

| Biomass and Biogas | |

| Hydro | |

| Coal | |

| Natural Gas and Oil | |

| End-User Consumption | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

What is the current size of the Denmark power market?

The market reached 20.14 GW in 2026 and is projected to expand to 28.42 GW by 2031 at a 7.12% CAGR.

Which generation source dominates the Denmark power market?

Wind power leads with 41.98% share in 2025, supported by strong offshore expansion plans.

How fast is commercial and Industrial sector increasing their electricity demand?

Commercial and Industrial consumption is expected to grow at a 8.12% CAGR through 2031, driven by Copenhagen’s digital-infrastructure boom.

How important are offshore wind tenders to future capacity additions?

Government tenders covering at least 6 GW by 2031—plus energy-island projects—anchor most new capacity and attract sizable foreign investment.

Why are corporate power purchase agreements (PPAs) becoming central to market growth?

Long-term PPAs give industrial and digital-service firms price certainty and sustainability credits, helping finance new wind and solar farms.

What measures are in place to ease grid congestion in western Denmark?

Energinet’s 172 km West Coast Connection and other 400 kV upgrades aim to move surplus wind power eastward and slash curtailment risk.

Page last updated on: