Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

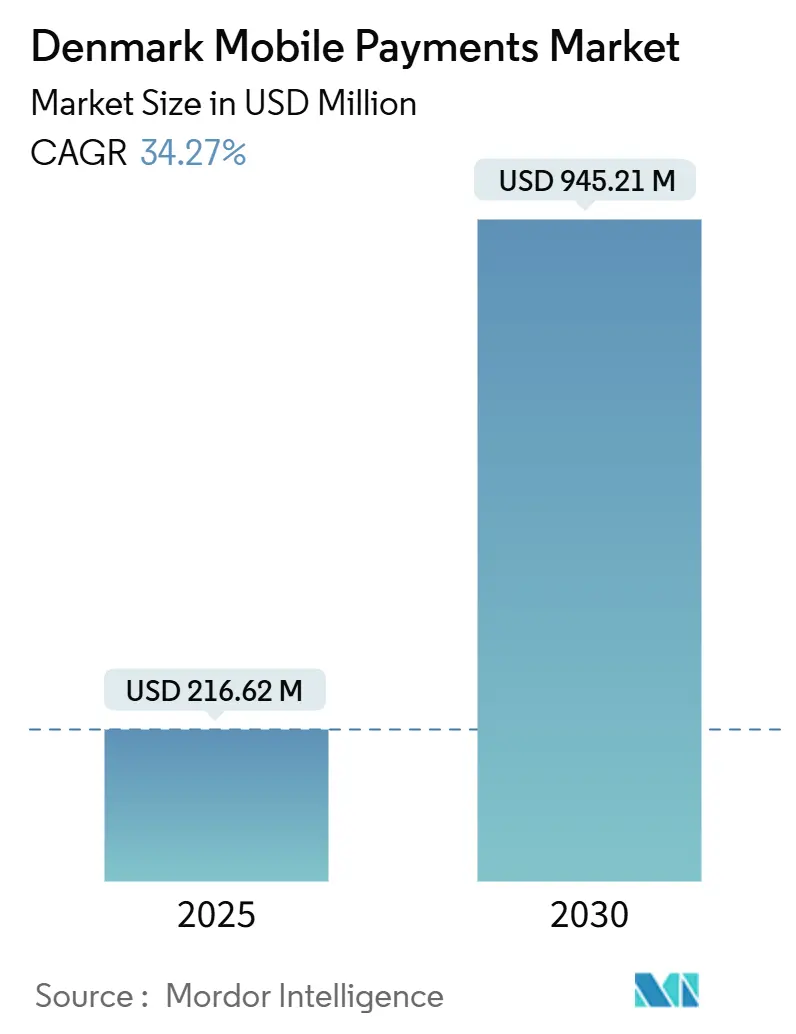

| Market Size (2025) | USD 216.62 Million |

| Market Size (2030) | USD 945.21 Million |

| Growth Rate (2025 - 2030) | 34.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Mobile Payments Market Analysis by Mordor Intelligence

The Denmark mobile payments market stands at USD 216.62 million in 2025 and is forecast to reach USD 945.21 million by 2030, advancing at a 34.27% CAGR. Rapid consumer migration from cash to digital transactions, the merger of Vipps and MobilePay, and EU-wide instant-payment rules are accelerating adoption. Real-time rails such as Express Clearing, near-universal smartphone penetration, and robust e-commerce demand continue to lower the friction of day-to-day spending. Cross-border wallet interoperability across the Nordic region is expanding addressable volume, while growing business use cases unlock new revenue streams. Intensifying competition among local champions and global technology firms is expected to sharpen pricing, enhance feature sets, and push providers into new verticals.

Key Report Takeaways

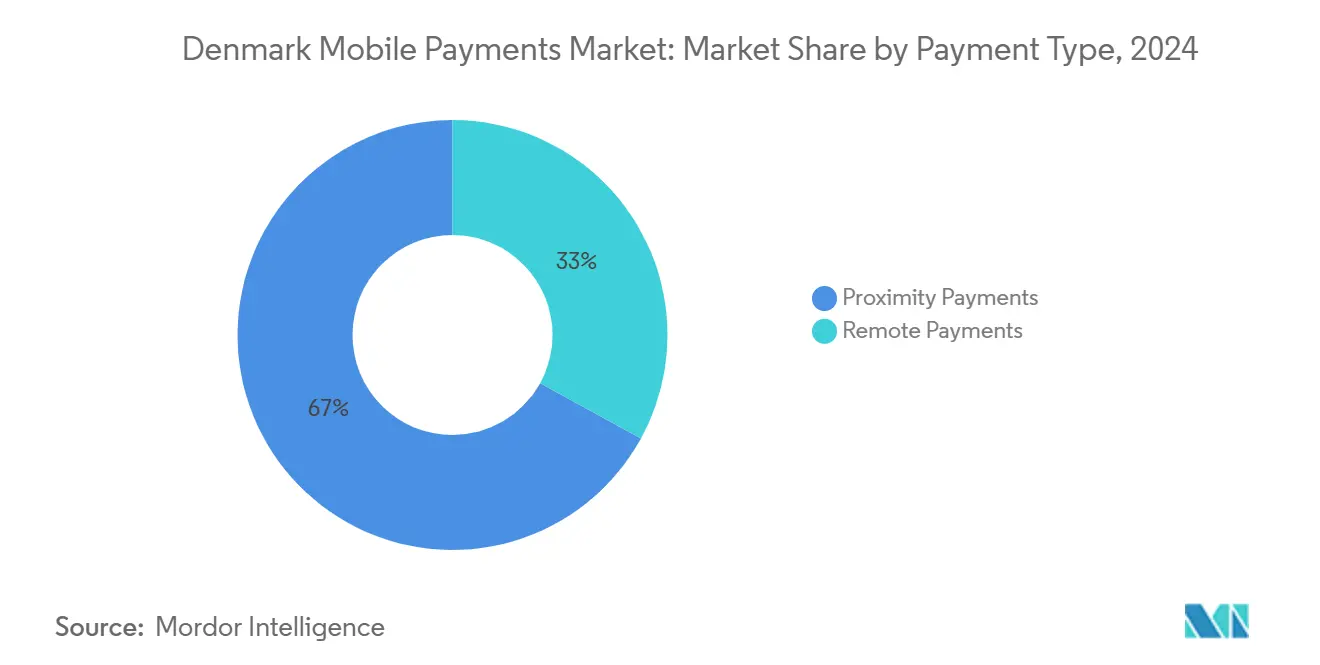

- By payment type, Proximity Payments led with 67% of Denmark mobile payments market share in 2024; Remote Payments are projected to expand at a 42.1% CAGR through 2030.

- By transaction type, the P2P segment accounted for 58% of the Denmark mobile payments market size in 2024, while In-store POS is set to grow at 32.5% CAGR between 2025-2030.

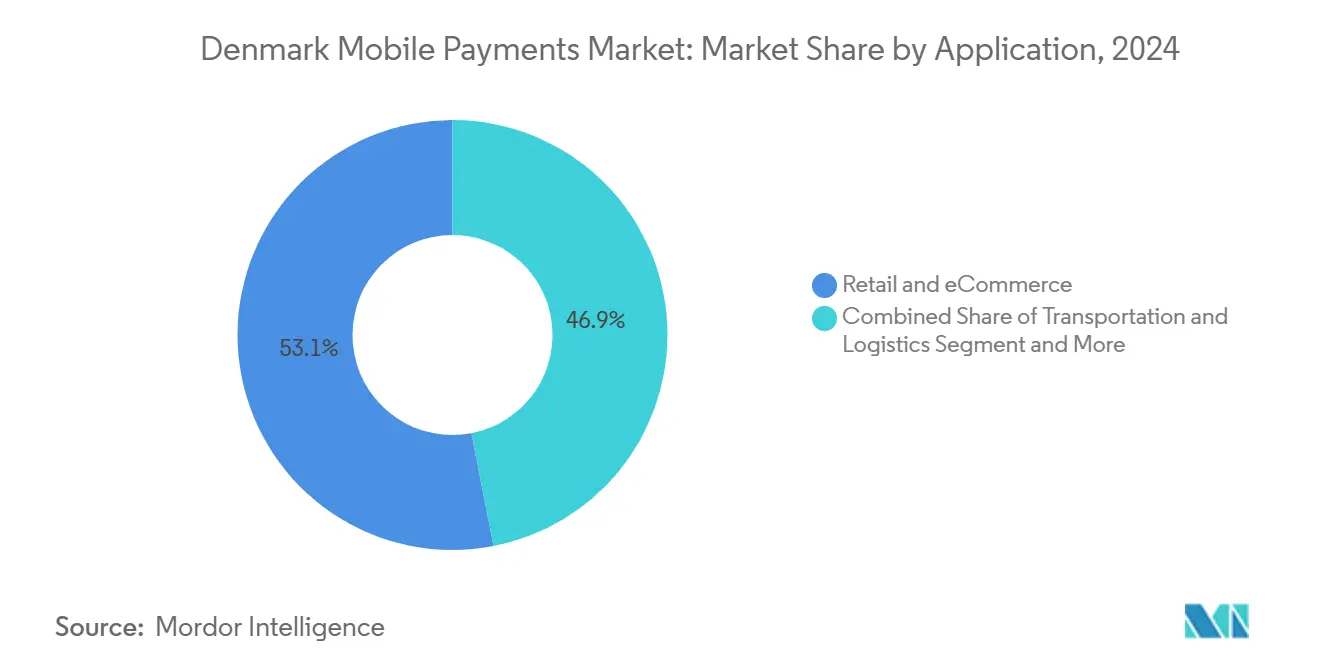

- By application, Retail and eCommerce captured 53.06% of the Denmark mobile payments market in 2024; Transportation and Logistics is forecast to register the fastest 33.04% CAGR to 2030.

- By end-user, Personal users represented 80.12% of the Denmark mobile payments market in 2024, yet the Business segment will advance at 35.7% CAGR through 2030.

Denmark Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High internet and smartphone penetration | +13.7% | National, with higher impact in urban centers | Short term (≤ 2 years) |

| Expansion of e-commerce and digital wallets | +8.6% | National, with cross-border implications | Medium term (2-4 years) |

| Government push toward cash-lite economy | +5.1% | National, with emphasis on public sector services | Medium term (2-4 years) |

| Instant-payment rails (Express Clearing) speed adoption | +3.4% | National, with integration into EU systems | Short term (≤ 2 years) |

| Nordic cross-border wallet integration (Vipps-MobilePay) | +1.7% | Nordic region (Denmark, Norway, Finland, Sweden) | Medium term (2-4 years) |

| EU biometric-ID mandates boost trust | +1.7% | EU-wide, with implementation in Denmark | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Internet and Smartphone Penetration

Nearly every Danish household is online, and 91% of citizens shop digitally, creating fertile ground for the Denmark mobile payments market. [1]Danmarks Nationalbank, “The Digital Retail Payment Market is Changing,” nationalbanken.dk Monthly activity across MobilePay’s 4.5 million Danish users exceeds 92%. Younger cohorts set the pace, but usage is diffusing into older age brackets, aided by intuitive interfaces. Each additional user raises network utility, improving acceptance at the point of sale and reinforcing repeat transactions. The ubiquity of smartphones also enables biometric checks that strengthen trust and compliance with forthcoming PSD3 rules.

Expansion of E-commerce and Digital Wallets

Domestic e-commerce revenue is projected to reach USD 8.91 billion in 2025. Digital wallets already account for 29% of online spend, eroding card dominance. Mobile commerce is on track to represent 73% of online sales by 2025, which feeds back into wallet usage as consumers value seamless checkout. Embedded Buy Now, Pay Later (BNPL) tools further broaden appeal, letting shoppers split payments inside the wallet environment without switching channels.

Government Push Toward Cash-Lite Economy

Denmark ranked first in the 2024 UN E-Government Survey with an EGDI score of 0.9992. Mandatory digital self-service since 2015 has accustomed residents to secure online interactions. The 2023 Digital Growth Strategy dedicates USD 138 million to strengthen digital public services through 2027. This sustained policy support encourages citizens to default to mobile channels and provides merchants a predictable compliance path, thereby bolstering the Denmark mobile payments market.

Instant-Payment Rails Speed Adoption

Express Clearing, launched in 2014, allows real-time settlement that underpins innovative wallet features. Migrating to TARGET DKK in April 2025 will integrate high-value and instant payments with European Central Bank infrastructure, heightening cross-border reach. The EU Instant Payments Regulation, effective January 2025, mandates parity between instant and regular transfer fees, cutting costs for consumers and merchants. [2]European Commission, “Payment Services,” finance.ec.europa.eu

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security and fraud concerns | -5.1% | National, with higher impact in e-commerce | Medium term (2-4 years) |

| Regulatory and compliance overheads (PSD3, AMLD6) | -3.4% | EU-wide, with implementation in Denmark | Medium term (2-4 years) |

| Interchange-fee caps squeeze provider margins | -1.7% | EU-wide, with implementation in Denmark | Short term (≤ 2 years) |

| Urban-market saturation limits new user growth | -1.7% | Urban centers, particularly Copenhagen | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Security and Fraud Concerns

Fraud losses climbed to Dkr627.4 million (USD 90 million) in 2023, with card fraud representing nearly half the total. Social-engineering attacks such as smishing rose 130% year on year. Heightened awareness among older consumers is slowing uptake for higher-value transactions. Providers are investing in biometric ID, AI-powered risk scoring, and user education to counter evolving threats.

Regulatory and Compliance Overheads

PSD3 and the Payment Services Regulation will broaden liability, mandate stronger customer authentication, and require new accessibility standards. [4]OneSpan, “PSD3 Proposes Changes to SCA & APP Fraud Prevention,” onespan.com The Digital Operational Resilience Act, effective January 2025, compels providers to embed comprehensive cyber-risk frameworks. Smaller firms may struggle with the resource burden, which could slow innovation or push them into partnerships with larger players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Proximity Leadership Amid Remote Surge

Proximity Payments contributed 67% of 2024 revenue, underlining Denmark’s early embrace of contactless wallets at the point of sale. This share translates into USD 145 million of the Denmark mobile payments market size, supported by near-field communication acceptance at 90% of in-store terminals. Remote Payments, however, are set to grow 42.1% annually through 2030, driven by the expanding digital cart and the EU’s ten-second settlement rule.

Growth on the remote side is amplified by one-click checkout, QR invoicing, and social-commerce payment links. Payment providers are embedding credit, loyalty, and installment options directly into the remote flow, which blurs boundaries between card and account-to-account transfers. As merchant tolerance for high interchange fees wanes, remote account-based payments are poised to chip away at card volume, gradually narrowing the historical gap with proximity usage in the Denmark mobile payments market.

By Transaction Type: POS Adoption Closes Gap on P2P

P2P transfers remain the behavioural anchor, holding 58% volume in 2024. They form the habitual base that keeps users inside a single wallet and funnels them toward additional services. Yet in-store POS is on a 32.5% CAGR trajectory, powered by software-based acceptance such as Tap to Pay on iPhone, which removes the need for dedicated terminals.

The Denmark mobile payments market is likely to witness converging transaction shares as omnichannel retailers roll out the same tokenized credentials for online and POS environments. Vipps MobilePay’s forthcoming tap-to-pay feature for Android and Apple devices aims to activate 1 million Danish users, further shrinking hardware barriers and widening merchant acceptance.

By Application: Logistics Races Ahead

Retail and eCommerce controlled 53.06% revenue in 2024, equal to USD 115 million of the Denmark mobile payments market size, sustained by high web-shop penetration. Transportation and Logistics, by contrast, will post a 33.04% CAGR through 2030 thanks to Denmark’s kilometer-based truck tolling scheme that integrates mobile payments. [3]Be-Mobile, “Denmark Successfully Launches National Truck Tolling Scheme,” be-mobile.com Transit operators are embedding account-based ticketing that lets riders tap smartphones without pre-loading value.

Hospitality and food service providers are next in line, switching to pay-at-table and digital tipping that resolve staff shortages and improve turnover time. The Denmark mobile payments industry is also inching into public-sector scenarios, including municipal fees and citizen disbursements, creating additional stickiness for wallet brands.

By End-user: Corporate Uptake Shifts Next

Personal users still account for 80.12% of the 2024 value, reflecting the consumer roots of early wallet propositions. Corporate users, however, are scaling faster at 35.7% CAGR, attracted to automated expense capture, integrated receivables, and cross-border payroll features. Combined with streamlined onboarding, those capabilities reduce reconciliation cycles and enhance cash-flow visibility for small and midsize enterprises.

The Denmark mobile payments market is responding with tailored dashboards, spending controls, and API access that sync with enterprise systems and embedded finance platforms. Growing Nordic trade reinforces demand for interoperable B2B flows, pushing providers to fuse domestic real-time rails with foreign exchange settlement layers.

Geography Analysis

Urban Denmark commands the lion’s share of transaction value, with Copenhagen alone accounting for roughly one-third of national volume. Smartphone penetration exceeds 98% in the capital, enabling pervasive tap-and-go habits at cafés, transit gates, and cultural venues. Rural areas, while trailing on absolute numbers, are catching up quickly as 5G coverage widens and local merchants migrate to cloud POS software.

The country’s integration into the TARGET Instant Payment Settlement system in March 2025 positions Danish institutions to clear cross-border euro payments within seconds. That capability increases outbound commerce for tourism and professional services, cementing Denmark’s role as a pilot market for pan-European wallet features. The Denmark mobile payments market benefits directly, since local wallets gain the back-end reach to move funds in real time beyond domestic borders.

Nordic cooperation is another catalyst. The Vipps-MobilePay platform covers 12 million users across Denmark, Norway, and Finland, processing 1.52 billion transactions in 2024. Seamless cross-border P2P launched in June 2024 and is likely to spill into merchant payments once regulatory approvals clear. These regional synergies increase the network benefit for Danish consumers and strengthen export potential for local fintech expertise.

Competitive Landscape

Local incumbents and global platforms are locked in a race to innovate. Vipps MobilePay retains a dominant user base but faces rapid share gains from Apple Pay and Google Pay, which leverage handset embeds and global acceptance footprints. Nets Denmark A/S and Dankort continue to anchor card infrastructure while investing in tokenization to stay relevant at the wallet layer.

Product development focuses on frictionless acceptance, loyalty integration, and embedded financing. Vipps MobilePay will roll out tap-to-pay across all major operating systems, seeking to entrench itself before Apple Pay widens NFC access under the recent EU agreement. Adyen and Stripe target enterprise merchants with unified commerce stacks that compress settlement times and cut reconciliation costs.

Strategically, partnerships are outpacing acquisitions. Telenor Denmark teamed with CSG to enhance omnichannel customer monetization. Banks are opening APIs under PSD2 to defend relevance, while specialty lenders such as ViaBill integrate BNPL modules into wallet flows, diversifying revenue from interchange to lending and subscription fees. Competitive pressure keeps fees low and speeds up the feature release cycle, ultimately supporting end-user adoption across the Denmark mobile payments market.

Denmark Mobile Payments Industry Leaders

Apple Inc. (Apple Pay)

Google LLC (Google Pay)

Samsung Electronics Co. Ltd. (Samsung Pay)

PayPal Holdings Inc.

Amazon Payments Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Adyen extended Tap to Pay on iPhone to Denmark, allowing merchants to accept contactless payments with no extra hardware. Strategy: accelerate in-store adoption by removing terminal costs and capturing small merchants at scale.

- April 2025: Vipps MobilePay posted NOK 1,707 million revenue for 2024 and confirmed a rollout of tap-to-pay on iOS and Android in Denmark. Strategy: deepen ecosystem stickiness and pre-empt rivals through hardware-agnostic acceptance.

- March 2025: Denmark joined the TARGET Instant Payment Settlement system, enabling pan-European real-time transfers. Strategy: bolster cross-border commerce and support domestic wallets with EU-level rails.

- January 2025: A kilometer-based truck toll using mobile payments launched nationwide. Strategy: digitize fee collection, nudge greener logistics behavior, and enlarge the Transportation and Logistics segment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Denmark mobile payments market as the total value of person-to-person, in-store, e-commerce, and bill-pay transactions that are initiated and authenticated on a smartphone or wearable and settled either through card rails or instant-payment rails.

Scope exclusion: hardware sales such as point-of-sale terminals, pure desktop card payments, and wholesale bank-to-bank transfers stay outside this analysis.

Segmentation Overview

- By Payment Type

- Proximity Payments

- Remote Payments

- By Transaction Type

- Peer-to-Peer (P2P)

- In-store Point-of-Sale (POS)

- Person-to-Merchant (P2M/Checkout)

- Other Transaction Types

- By Application

- Retail and eCommerce

- Transportation and Logistics

- Hospitality and Food-Service

- Government and Public Sector

- Other Applications (Education, Healthcare)

- By End-user

- Personal

- Business

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview Danish acquiring banks, wallet product leads, and large merchants across Copenhagen, Aarhus, and Odense. These conversations validate adoption curves, promotional pricing, and year-ahead roadmap assumptions that secondary data alone cannot surface.

Desk Research

We start by mapping the addressable pool through open datasets such as Danmarks Nationalbank's quarterly card-turnover files, Eurostat ICT surveys, and Danish Commerce & Services payment barometers, which anchor mobile wallet share, ticket size, and transaction mix. Company filings and press releases enrich wallet user counts, while paid platforms, D&B Hoovers for issuer revenue splits and Dow Jones Factiva for deal trackers, fill remaining gaps.

Trade associations like Finans Danmark and the European Payments Council provide rule-change timelines and fee benchmarks that inform scenario tests. The sources cited are illustrative; many other public and subscription datasets support collection, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction begins with 2024 mobile wallet and instant-payment value reported by the central bank, which is then split by payment context through surveyed share metrics. Results are corroborated through a bottom-up roll-up of sampled provider KPIs and average spend per active user, letting our team adjust for double counting. Key variables include smartphone penetration, contactless acceptance density, interchange caps, cross-border e-commerce growth, and the Vipps-MobilePay integration timeline. An ARIMA forecast supplemented by scenario analysis projects CAGR impacts of regulatory shifts and new Apple Pay NFC access.

Data Validation & Update Cycle

Outputs pass multi-analyst variance checks against external time series, and anomalies prompt re-contact of select respondents. Reports refresh each year, with interim model tweaks when material events, such as new fee regulation, occur. A last-mile review is completed before client delivery.

Why Mordor's Denmark Mobile Payments Baseline Earns Trust

Published numbers differ because firms make unique scope and currency choices, apply varying refresh cadences, and assume contrasting adoption ramps.

Key gap drivers here include whether P2P transfers are counted, which exchange rate is locked, and how aggressively proximity wallets are projected to cannibalize cards. Mordor's model discloses each choice and updates annually, while some publishers freeze inputs for multiple cycles or roll Denmark into broader Nordic totals, inflating or deflating the standalone view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 216.62 M (2025) | Mordor Intelligence | - |

| USD 206.41 M (2024) | Global Consultancy A | Excludes P2P transfers and applies a single transaction fee proxy |

| USD 165.20 M (2023) | Regional Consultancy B | Uses 2021 smartphone base, omits instant-payment wallet spend |

Taken together, the comparison shows that Mordor's disciplined scope selection, live-data refresh, and transparent variable list deliver a balanced, decision-ready baseline that stakeholders can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the Denmark mobile payments market?

The market is valued at USD 216.62 million in 2025 and is projected to climb to USD 945.21 million by 2030 at a 34.27% CAGR.

Which payment type leads the Denmark mobile payments market?

Proximity Payments hold 67% share in 2024, thanks to widespread contactless acceptance, although Remote Payments are expanding faster at 42.1% CAGR.

How significant is fraud for Danish mobile payments?

Fraud losses reached Dkr627.4 million (USD 90 million) in 2023, prompting providers to invest heavily in biometric security and AI-driven monitoring.

Why is the Transportation and Logistics segment growing so fast?

A kilometer-based tolling system and broader mobility integrations push the segment toward a 33.04% CAGR through 2030.

How will EU regulation affect mobile payments in Denmark?

The Instant Payments Regulation caps transaction fees, while PSD3 and DORA add security and resilience requirements, raising compliance costs but improving consumer trust.

Are businesses adopting mobile payments?

Yes. The Business segment of the Denmark mobile payments market is forecast to grow at 35.7% CAGR as companies embrace automated expense and supplier-payment tools.

Page last updated on: