Decentralized Finance (DeFi) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 238.54 Billion |

| Market Size (2031) | USD 770.56 Billion |

| Growth Rate (2026 - 2031) | 26.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Decentralized Finance (DeFi) Market Analysis by Mordor Intelligence

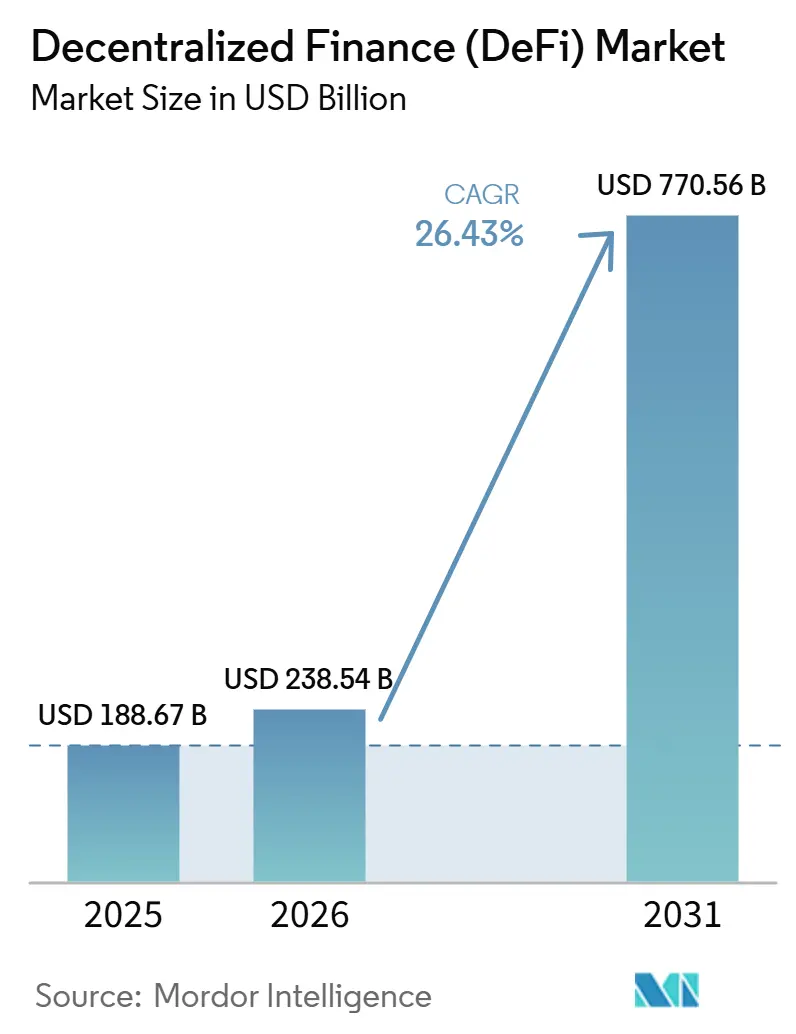

The Decentralized Finance Market size is projected to expand from USD 188.67 billion in 2025 and USD 238.54 billion in 2026 to USD 770.56 billion by 2031, registering a CAGR of 26.43% between 2026 to 2031.

Policy-backed access points like spot Bitcoin ETFs, combined with the European Union’s MiCA framework, are pulling institutional capital into compliant, on-chain channels that are designed to integrate with existing custody and disclosure standards. Stablecoin settlement pilots by major networks, alongside bank-aligned trust structures for digital assets, are bringing DeFi operations closer to the core of treasury, payments, and liquidity management workflows. Layer-2 fee compression and rollup roadmaps that emphasize scalability and pre-confirmation are improving the user experience for frequent, smaller transactions while keeping settlement aligned with Layer-1 security assumptions [1]Max Wadington, “The Fusaka Upgrade: Scaling Meets Value Accrual,” Fidelity Digital Assets, fidelitydigitalassets.com. Together, these catalysts point to a growth cycle that is less tied to speculative incentives and more anchored in regulatory clarity, compliant tokenization, and payment-grade rails that mainstream institutions can adopt within their existing control frameworks.

Key Report Takeaways

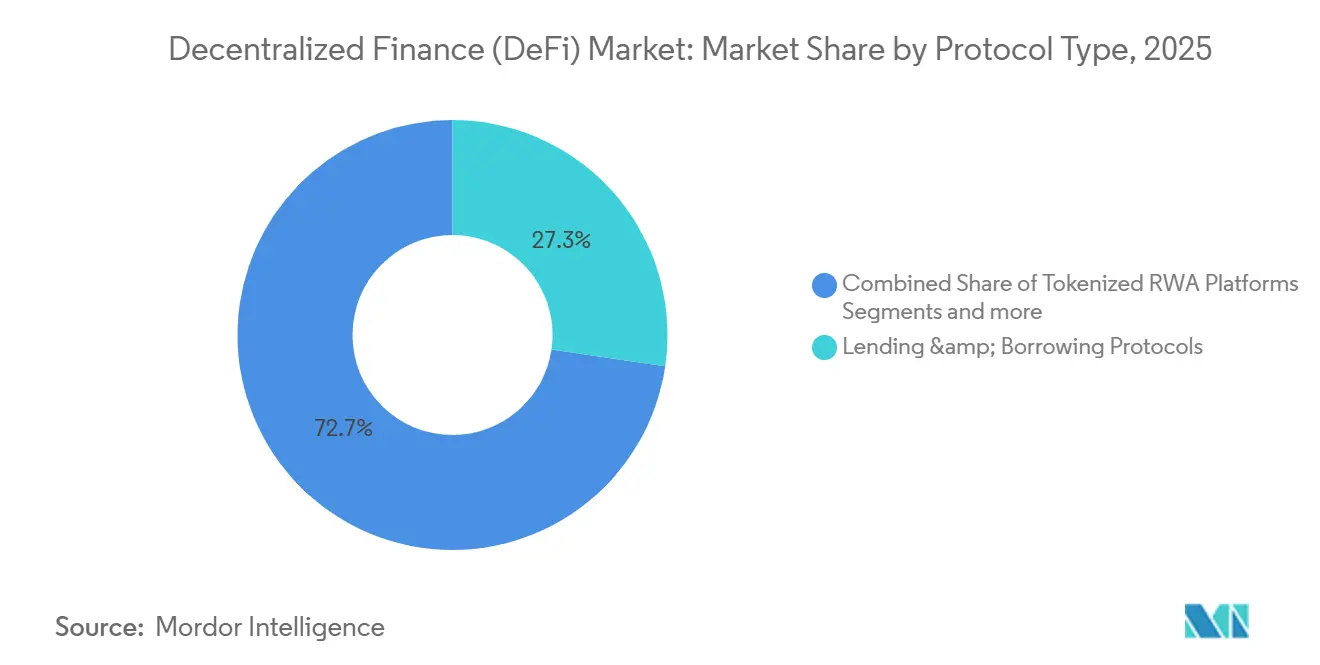

- By protocol type, lending & borrowing protocols led with 27.33% of the decentralized finance market share in 2025, while tokenized RWA platforms are forecasted to expand at a 39.72% CAGR through 2031.

- By end-use application, savings & yield farming accounted for 36.52% of the market share in 2025, and payments, remittances & cross-border treasury are projected to grow at a 34.67% CAGR to 2031.

- By end user, retail users held 62.12% of the Decentralized Finance (DeFi) market share in 2025, while institutional investors & asset managers are expected to grow at a 32.55% CAGR through 2031.

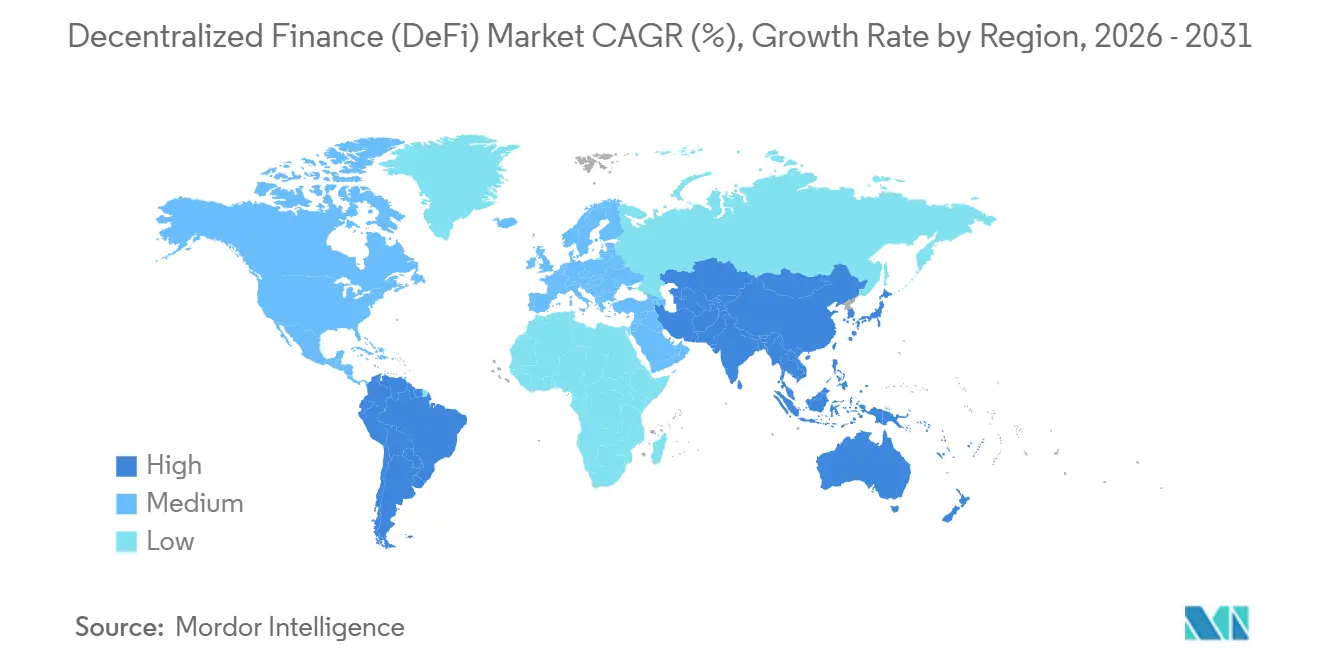

- By geography, North America retained 42.78% of the decentralized finance market share in 2025, and Asia-Pacific is set to advance at a 31.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Decentralized Finance (DeFi) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Total-Value-Locked across core DeFi verticals | +4.8% | Global, with Ethereum maintaining 60% dominance | Medium term (2-4 years) |

| Regulatory clarity in the United States (ETF) & EU (MiCA) unlocks institutional flows | +7.2% | North America & EU core, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Layer-2 fee compression expands viable use-cases | +3.5% | Global, concentrated in Ethereum L2s (Base, Arbitrum, Optimism) | Medium term (2-4 years) |

| Tokenized real-world-asset (RWA) platforms gain banking-grade traction | +6.9% | Global, early gains in the United States (BlackRock BUIDL), EU (MiCA compliance) | Long term (≥ 4 years) |

| Emerging AI-driven "DeFAI" robo-agents automate yield strategies | +2.4% | Global, with Solana and Ethereum ecosystems leading | Long term (≥ 4 years) |

| Payment-network integrations bridge mainstream rails with DeFi | +5.6% | North America, EU, emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Total-Value-Locked Across Core DeFi Verticals

Liquidity depth on leading chains and exchanges supports more efficient pricing, routing, and collateral management as the DeFi market attracts users seeking reliable execution and audited code paths. High and sustained stablecoin transfer volumes, alongside growth in Layer-2 activity, point to a structural shift from episodic speculation to continuous settlement utility that feeds protocol revenue and long-term user retention. As capital consolidates on platforms with stronger governance and security, the market benefits from lower slippage and tighter spreads under normal conditions. International bodies have noted that rising interlinkages also transmit stress more quickly across venues, which increases the value of rigorous risk controls and diversified oracle sources[2]Financial Stability Board Staff, “The Financial Stability Risks of Decentralised Finance,” Financial Stability Board, fsb.org. The net effect is a market structure where depth, speed, and composability support growth while requiring consistent attention to systemic risk and transparency across major liquidity pools.

Regulatory Clarity in the United States (ETF) & the EU (MiCA) Unlocks Institutional Flows

The approval of spot Bitcoin exchange-traded products created a regulated wrapper that traditional allocators can use under existing policies, which reduces operational friction for exposure that often interacts downstream with DeFi liquidity venues. MiCA outlines authorization pathways for crypto-asset service providers and establishes reserve and disclosure requirements for asset-referenced and e-money tokens, enhancing passportability and reducing regulatory uncertainty for compliant issuers and intermediaries across the bloc. Payment-network pilots for stablecoin settlement now operate within bank-partner models that align with core reconciliation and dispute processes, a development that ties the DeFi market to mainstream acceptance infrastructure. United States banking and trust structures for digital assets further move custody and settlement inside prudential oversight, which helps large institutions meet supervisory expectations while participating in tokenized finance. Together, these frameworks lower perceived compliance risk, enable scaled product rollouts, and shift capital from pilot programs to production deployments across North America and Europe, with spillover to Asia-Pacific hubs that align with similar rules.

Layer-2 Fee Compression Expands Viable Use-Cases

The migration of activity to rollups has reduced transaction costs and increased throughput, which makes frequent, smaller-value interactions feasible for consumer and institutional users in the DeFi market. Roadmaps that add pre-confirmation and align value accrual with validator economics are designed to sustain low fees while reinforcing settlement assurances on the base layer. Lower fees and faster confirmations expand the set of use cases, such as micro-treasury sweeps, agent-driven rebalancing, and high-frequency routing that were uneconomic at higher gas price regimes. Liquidity providers and market makers benefit as order flow disperses across rollups while staying composable through cross-chain messaging and canonical bridges that reflect policy constraints. These network-level improvements help the DeFi market support real-time activity in trading, lending, and settlement while preserving the regulatory posture that institutions require for scaled participation.

Tokenized Real-World-Asset (RWA) Platforms Gain Banking-Grade Traction

Tokenized funds and fixed income instruments now operate under regulated structures with clear redemption paths, audited reserves, and transparent on-chain reporting, which aligns with enterprise-grade custody and disclosure standards [3]Centrifuge Editorial Team, “2026: What to Expect from Real-World Asset Tokenization,” Centrifuge, centrifuge.io. Large asset managers and banks have launched tokenized products that fit within existing investor protections while delivering faster settlement and more automated administration, which directly supports broader adoption in the DeFi market. Issuers that streamline securitization, reduce reconciliation steps, and standardize attestations increase operational efficiency, which is a compelling driver for migration from pilots to production. Permissioned pools and identity-aware access controls allow institutional buyers to meet compliance requirements while interacting with decentralized settlement and liquidity. As documentation standards, custody practices, and secondary liquidity improve, RWA platforms become a high-growth infrastructure layer that connects traditional instruments with composable DeFi workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-contract exploits & oracle manipulation risk | -5.2% | Global, concentrated in high-TVL protocols (Ethereum, BSC) | Short term (≤ 2 years) |

| AML / KYC enforcement actions on non-compliant dApps | -4.7% | North America, EU (MiCA enforcement), APAC (FATF Travel Rule) | Medium term (2-4 years) |

| Liquidity concentration on a handful of pools elevates systemic risk | -3.8% | Global, with top 10 lending protocols holding 89% TVL | Medium term (2-4 years) |

| Targeted regulatory actions on leverage and derivatives create uncertainty | -4.1% | North America (SEC/CFTC), United Kingdom (FCA consultation), EU (MiCA oversight) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smart-Contract Exploits & Oracle Manipulation Risk

Security incidents and logic flaws can drain funds or disrupt price discovery, which affects confidence, slows onboarding, and raises the cost of capital for new deployments in the DeFi market. Composability amplifies both benefits and risks, since a single faulty contract or price feed can propagate across lending, trading, and collateral management within minutes. International bodies have flagged the centralization of certain operational controls as a point of failure that can undermine claims of decentralization when governance and upgrades concentrate among a few actors. This pattern increases the premium on formal verification, multifactor upgrade paths, and layered oracle designs with diversified data sources. As institutional participation grows, the market will need stronger assurance controls and documented incident response to meet the expectations associated with prudential oversight.

Targeted Regulatory Actions on Leverage and Derivatives Create Uncertainty

Supervisors have signalled limits on high-multiple leveraged products through actions that block certain ETF structures tied to crypto benchmarks, which indicates a policy preference for risk-limiting measures. Parallel consultations and policy statements in the United Kingdom and the European Union expand oversight of staking, lending, and core crypto-asset activities, which increases compliance overhead for leverage-intensive strategies. Institutions often require clarity on custody, margin treatment, and bankruptcy-remote structures before committing balance sheets to derivatives in size, which delays deeper liquidity formation in regulated channels. Even with this constraint, standardization can improve long-run stability by reducing forced liquidations and aligning market conduct with existing rules for investor protection. The DeFi market is therefore navigating a two-track environment where compliant venues operate under stricter rules while offshore platforms retain looser practices that fragment liquidity and raise basis spreads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protocol Type: Tokenized RWA Platforms Emerge as Fastest-Growing Infrastructure Layer

Lending & Borrowing Protocols captured 27.33% share in 2025, while Tokenized RWA Platforms are projected to expand at a 39.72% CAGR through 2031, setting a new growth baseline for capital that needs compliant issuance, custody, and reporting. Tokenization of money market exposures and fixed income instruments under established investor protections is creating an on-ramp for asset managers and treasurers to tap on-chain liquidity without compromising on governance and controls. Issuers that pair transparent reserves with permissioned access and standardized attestations can streamline reconciliation and reduce operational friction, which strengthens the case for token-based administration at scale. The DeFi market is seeing RWA platforms serve as connective tissue between regulated assets and decentralized settlement as they embed policy requirements into code and process design. As a result, lending protocols remain an anchor for collateral and yield, while RWA rails capture the fastest growth by unlocking product formats that fit within traditional mandates.

Exchanges continue to drive price discovery and volume concentration, and their evolution toward fee-based value accrual reflects a wider shift away from incentive-heavy models in the DeFi market. Market-share leadership among a few DEXs delivers liquidity benefits that also heighten the need for robust oracles and transparent parameter governance. Layer-2 fee compression creates room for more active liquidity management and smaller trade sizes, which expands the user base across retail and institutions. Stablecoin issuance aligned with disclosure and reserve rules benefits from payments integration and bank partnerships, which pull traditional workflows closer to on-chain rails. Over the forecast window, the DeFi market will likely see protocol differentiation around compliance readiness, permissioned pools, and institutional reporting, with RWA platforms anchoring the fastest-expanding layer.

By End-Use Application: Payments Segment Poised to Eclipse Savings as Stablecoin Rails Mature

Savings & Yield Farming held 36.52% in 2025, while the Payments, Remittances & Cross-Border Treasury segment is projected to grow at a 34.67% CAGR through 2031, supported by stablecoin settlement pilots that integrate directly with bank partners and card networks. Payment-grade use cases are scaling because programmable settlement can reduce costs and speed reconciliation without sacrificing fraud controls and dispute management. As these pilots transition to production, corporates gain tools for supplier payments, cross-border treasury, and marketplace payouts that are natively interoperable with wallets and banks. Savings remain important because fee-based revenue distribution and buybacks are replacing incentive-heavy models, which can create steadier returns aligned with protocol fundamentals. Together, these shifts position the DeFi market to blend passive income products with payments-grade settlement in a way that diversifies growth drivers and smooths volatility across cycles.

Trading & Investment remains a core application given the need for price discovery, hedging, and routing across assets and chains in the DeFi market. The pivot toward fee switches and protocol revenue alignment supports sustainable economics and reduces reliance on token inflation or subsidies over time. Payment growth will depend on issuer compliance and network-grade reliability that can meet merchant and bank standards across jurisdictions. Lower transaction costs expand viable ticket sizes for consumer and B2B payments, which increases the addressable flow for stablecoins in everyday commerce. Over the forecast period, the application mix will reflect the rise of payments alongside persistent demand for savings and trading, with product design that balances permissionless access and permissioned controls in the market.

By End User: Institutional Surge Signals Professionalization, Yet Retail Remains Dominant

Retail Users held 62.12% in 2025, while Institutional Investors & Asset Managers are projected to grow at a 32.55% CAGR through 2031, reflecting the impact of regulated wrappers, custody expansion, and bank-aligned trust structures on participation in the DeFi market. ETF approval provides a standardized exposure path that many mandates can adopt within existing fiduciary and reporting frameworks. As banks and trust entities expand digital asset services, treasury teams and asset managers gain policy-aligned ways to interact with token rails and DeFi liquidity under supervisory expectations. Retail participation remains strong due to permissionless access, rapid product iteration, and low minimums, which sustains wide experimentation alongside institutional lanes. This dual-track adoption increases the value of routing and aggregation across venues, which is a core function for execution quality in the market.

Institutions typically demand clear rules on custody, disclosures, and market conduct, which is why MiCA’s authorization regime, reserve rules, and operational standards improve the case for scaled deployment in Europe. Payment-network pilots and compliant stablecoin issuance further reduce operational friction for enterprise use cases such as cross-border treasury and supplier payments. Liquidity providers benefit as institutions bring larger orders under policy controls that tie settlement and custody to established practices in the DeFi market. Over the forecast window, the DeFi industry is likely to see continued retail leadership by user count and a growing institutional share by volume as bank-grade channels mature. The combination of regulated access and open composability supports a broad user mix that drives deeper liquidity and a more resilient market structure.

Geography Analysis

North America accounted for 42.78% in 2025, supported by regulated ETF access, custody expansion, and early payment-network pilots that connect bank partners with tokenized settlement in the DeFi market. ETF approvals created a familiar product format that institutions could incorporate under existing policy and disclosure regimes, which accelerated flows into regulated channels. Banking and trust charters for digital assets moved settlement and custody inside prudential oversight, which aligns DeFi interactions with supervisory expectations and risk controls. In parallel, stablecoin settlement pilots demonstrated how merchant acceptance, reconciliation, and dispute management can operate with programmable assets, which pulls more treasury activity toward the DeFi market. This mix of product access, oversight, and payments utility explains why North America maintains a leading position while creating a template that other regions adapt within their legal context.

Europe’s share reflects a rules-based approach that codifies authorization, reserve, and disclosure requirements under MiCA, which improves passportability for issuers, custodians, and exchanges that serve the DeFi market. The combination of e-money alignment and transfer-of-funds obligations brings identity and traceability into the crypto transfer process, which favours providers that can meet operational standards across member states. Banks experimenting with euro-denominated settlement tokens and tokenized instruments demonstrate how the region is integrating decentralized components with established financial plumbing. Over the forecast period, Europe’s contribution will hinge on how quickly MiCA-aligned providers scale across borders and expand listings and custody within the market. The emphasis on disclosure, reserves, and operational resilience positions the region for steady, policy-led growth rather than speculative cycles.

Asia-Pacific is projected to grow at a 31.89% CAGR through 2031 as regulatory hubs implement stablecoin rules and tokenized-deposit pilots that enable compliant participation in the DeFi market. Regional policy changes, including frameworks for blockchain-based funds and payments, are drawing activity into supervised channels that interoperate with bank-grade infrastructure. Payment-network pilots and wallet-bank integrations support cross-border commerce and remittances, which creates practical demand for stablecoins within regulated corridors. As connectivity improves across banks, custodians, and exchanges, liquidity will continue to diversify across chains and rollups while maintaining access to compliant issuers and venues in the DeFi market. The region’s growth path reflects a balance of regulatory experimentation in hubs and strong enterprise demand for programmable settlement that is consistent with local rules.

Competitive Landscape

The competitive landscape shows leadership in lending, exchanges, and stablecoins, yet remains moderately fragmented with active competition across execution models in the DeFi market. Established venues concentrate meaningful volume, which improves routing efficiency and reduces slippage for larger orders under normal conditions. Protocols are shifting from token incentives to fee-based value accrual, a pattern that indicates maturation and alignment of token economics with real usage. Stablecoin issuers that emphasize reserve transparency and regulatory alignment are gaining leverage through partnerships with networks and bank partners. Tokenization providers that deliver issuance, custody, and standardized reporting are moving use cases from pilots to production, which attracts institutional demand to the market.

Strategic moves include fee-switch activation by leading DEXs that redirect revenue to value accrual, which is a durable alternative to incentive-heavy growth models in the DeFi market. Payment networks launched stablecoin settlement pilots that position programmable assets inside card and acquiring workflows aligned with bank partners. Banks and trust companies advanced custody and tokenization, while large exchanges pursued acquisitions to expand derivatives and institutional coverage, signalling a trend toward hybrid centralized-decentralized offerings. Tokenization specialists forged partnerships with index providers to demonstrate production-grade operations for index-linked instruments on-chain. These moves reflect a broader pivot toward compliance readiness, operational scale, and product sustainability across the DeFi market.

Technology investment focuses on rollup scaling, pre-confirmation, and validator-aligned value accrual to keep fees low while preserving security and economic incentives in the DeFi market. Payments innovation highlights agentic credentials, programmable settlement, and merchant acceptance enhancements that reduce friction without removing risk controls. ETF and ETP growth improve on-ramps for institutions that need regulated formats and custodial clarity, which improves the flow of capital into compliant venues. Legal and regulatory updates expand supervision to staking, lending, and related activities, which shape product design and margin frameworks across providers. The winners are likely to be platforms that combine governance strength, transparent risk management, and integration into bank-grade workflows at scale in the market.

Decentralized Finance (DeFi) Industry Leaders

MakerDAO

Uniswap Labs

Curve Finance

Lido Finance

Compound Labs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Visa Inc. announced the launch of USDC settlement in the United States, allowing issuer and acquirer partners to settle transactions using Circle’s USDC stablecoin. This initiative enhances settlement speed, seven-day availability, and operational resilience without impacting consumer card experiences.

- December 2025: JPMorgan introduced the My Onchain Net Yield Fund (MONY) for qualified investors on a public blockchain, enabling redemption in cash or stablecoins. The fund integrates money market exposure with transparent, efficient settlement via token-based systems, demonstrating how regulated fund structures can operate on-chain while adhering to custody standards and advancing tokenized instruments in decentralized finance.

- December 2025: Uniswap implemented protocol fee switches for V2 and V3 pools following a community vote, channelling fees toward value accrual and token burn mechanisms supported by protocol revenue. This development highlights a shift in the DeFi market from liquidity mining to sustainable fee-based models, aligning token value with usage and revenue generation.

- August 2025: Coinbase’s acquisition of Deribit aims to enhance derivatives offerings and institutional coverage by integrating DeFi-native capabilities into hybrid exchange models. This move highlights the importance of derivatives liquidity, margin infrastructure, and policy alignment for institutional DeFi participation, while reflecting consolidation trends in execution, custody, and product diversification within the market.

Global Decentralized Finance (DeFi) Market Report Scope

Decentralized Finance (DeFi) is a blockchain-based financial system that leverages smart contracts to automate services such as lending, borrowing, and trading. By eliminating intermediaries like banks, it facilitates transparent, permissionless transactions, offering benefits such as cost efficiency and faster settlements, while presenting complexities and risks associated with decentralization.

The decentralized finance (defi) market is segmented by protocol type (decentralized exchanges (DEX), lending & borrowing protocols, stablecoin issuance platforms, tokenized rwa platforms, others), end-use application (payments, remittances & cross-border treasury, trading & investment, savings & yield farming, others), end user (retail users, small & medium enterprises (SMEs), large enterprises, institutional investors & asset managers), and geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Decentralized Exchanges (DEX) |

| Lending & Borrowing Protocols |

| Stablecoin Issuance Platforms |

| Tokenized RWA Platforms |

| Others (Derivatives, Yield Aggregators, Liquid Staking, etc.) |

| Payments, Remittances & Cross-Border Treasury |

| Trading & Investment |

| Savings & Yield Farming |

| Others (Insurance, Infrastructure, GameFi) |

| Retail Users |

| Small & Medium Enterprises (SMEs) |

| Large Enterprises |

| Institutional Investors & Asset Managers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Protocol Type | Decentralized Exchanges (DEX) | |

| Lending & Borrowing Protocols | ||

| Stablecoin Issuance Platforms | ||

| Tokenized RWA Platforms | ||

| Others (Derivatives, Yield Aggregators, Liquid Staking, etc.) | ||

| By End-Use Application | Payments, Remittances & Cross-Border Treasury | |

| Trading & Investment | ||

| Savings & Yield Farming | ||

| Others (Insurance, Infrastructure, GameFi) | ||

| By End User | Retail Users | |

| Small & Medium Enterprises (SMEs) | ||

| Large Enterprises | ||

| Institutional Investors & Asset Managers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the DeFi market’s growth outlook through 2031?

The DeFi market size is USD 238.54 billion in 2026 and is projected to reach USD 770.56 billion by 2031 at a 26.43% CAGR, supported by regulated access, tokenization, and payment-grade settlement.

Which protocol type is growing fastest in the DeFi market?

Tokenized RWA platforms are projected to expand at a 39.72% CAGR through 2031 as compliant issuance and custody align with institutional requirements.

Which application area is set to accelerate the most within the DeFi market?

Payments, Remittances & Cross-Border Treasury is projected to grow at a 34.67% CAGR on the back of stablecoin settlement pilots that fit bank and network standards.

How is institutional participation changing the DeFi market?

Institutional Investors & Asset Managers are projected to grow at a 32.55% CAGR as ETFs, custody, and trust structures make policy-aligned access operationally feasible.

Which regions lead and grow fastest in the DeFi market?

North America held 42.78% in 2025 under mature oversight, while Asia-Pacific is projected to advance at a 31.89% CAGR through 2031 as hubs implement stablecoin and tokenization rules.

What risks could slow the DeFi market’s expansion?

Key risks include smart-contract exploits, AML/KYC enforcement, liquidity concentration, and targeted limits on leverage and derivatives that raise compliance and operational burdens.

Page last updated on: