Cryptocurrency Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

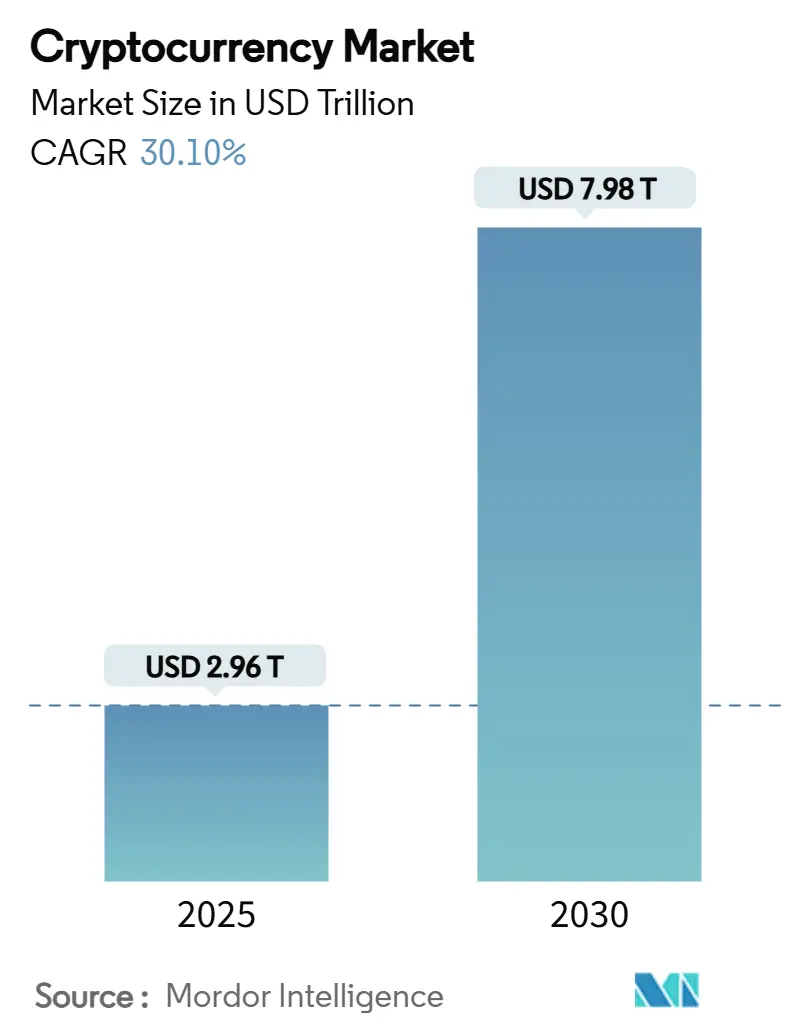

| Market Size (2025) | USD 2.96 Trillion |

| Market Size (2030) | USD 7.98 Trillion |

| Growth Rate (2025 - 2030) | 30.10% CAGR |

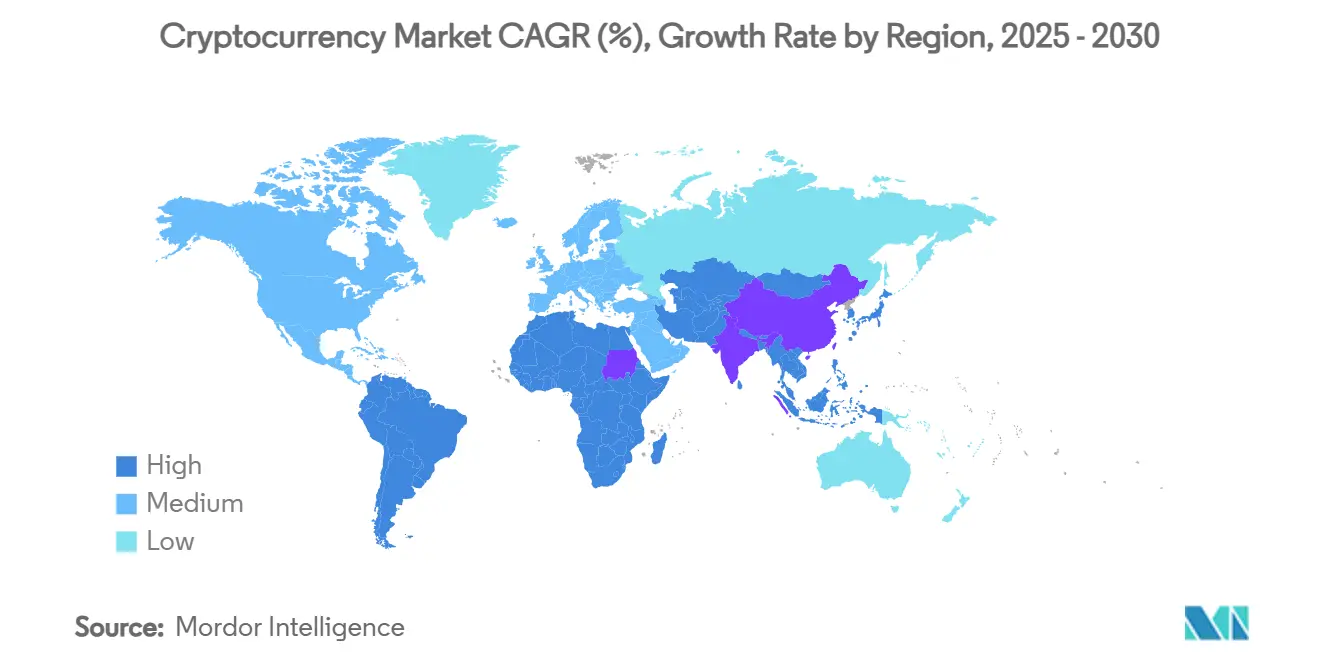

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

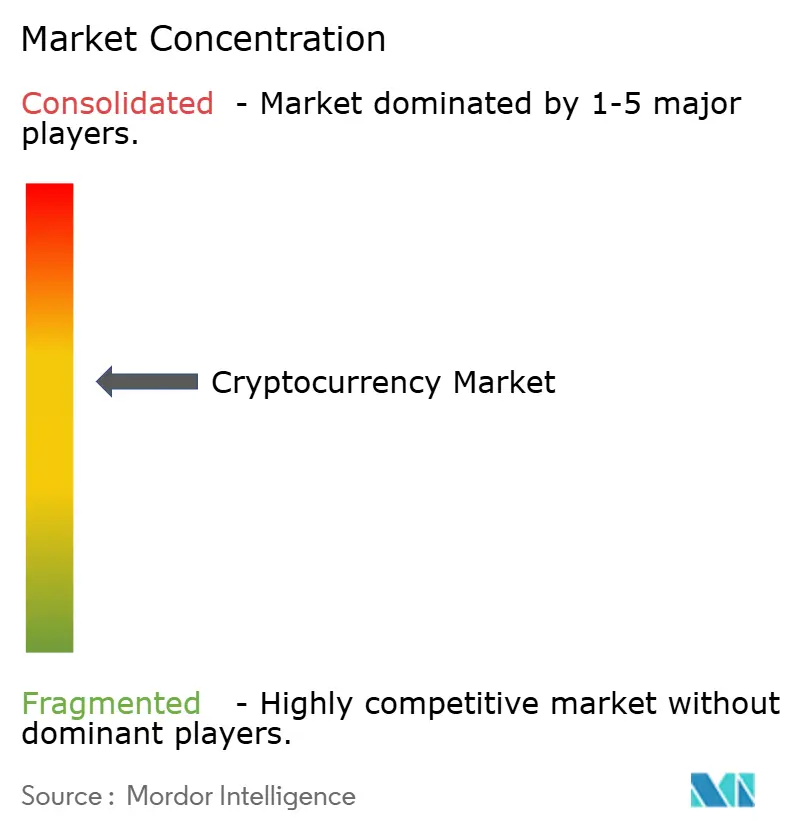

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cryptocurrency Market Analysis by Mordor Intelligence

The cryptocurrency market rose to USD 2.96 trillion in 2025 and is projected to reach USD 7.98 trillion by 2030, registering a vigorous 30.10% CAGR. This sharp climb reflects how regulatory clarity has intersected with institutional buy-in and rapid technical progress, upgrading digital-asset infrastructure from a retail niche to an integral component of global capital markets. Spot-Bitcoin exchange-traded funds (ETFs) authorised in early 2024 opened a door for pension schemes, insurers, and endowments to gain crypto exposure inside established portfolio workflows. Soon after, the US Securities and Exchange Commission permitted options trading on those ETFs, providing hedging tools and signaling that mature risk-management structures now surround the asset class. Europe’s Markets in Crypto-Assets (MiCA) regulation, live since December 2024, created a single passport for service providers across some member states, removing duplicate compliance burdens and smoothing cross-border activity. Equally important, Asia-Pacific central-bank digital-currency (CBDC) pilots—led by China’s multi-CBDC Bridge tests—are redefining cross-border payment rails and setting benchmarks that private networks must match on speed, cost, and transparency. Against this backdrop, artificial-intelligence (AI) compliance engines are slashing fraud-loss ratios, making participation safer for both retail users and large corporates and thereby reinforcing positive network effects.

Key Report Takeaways

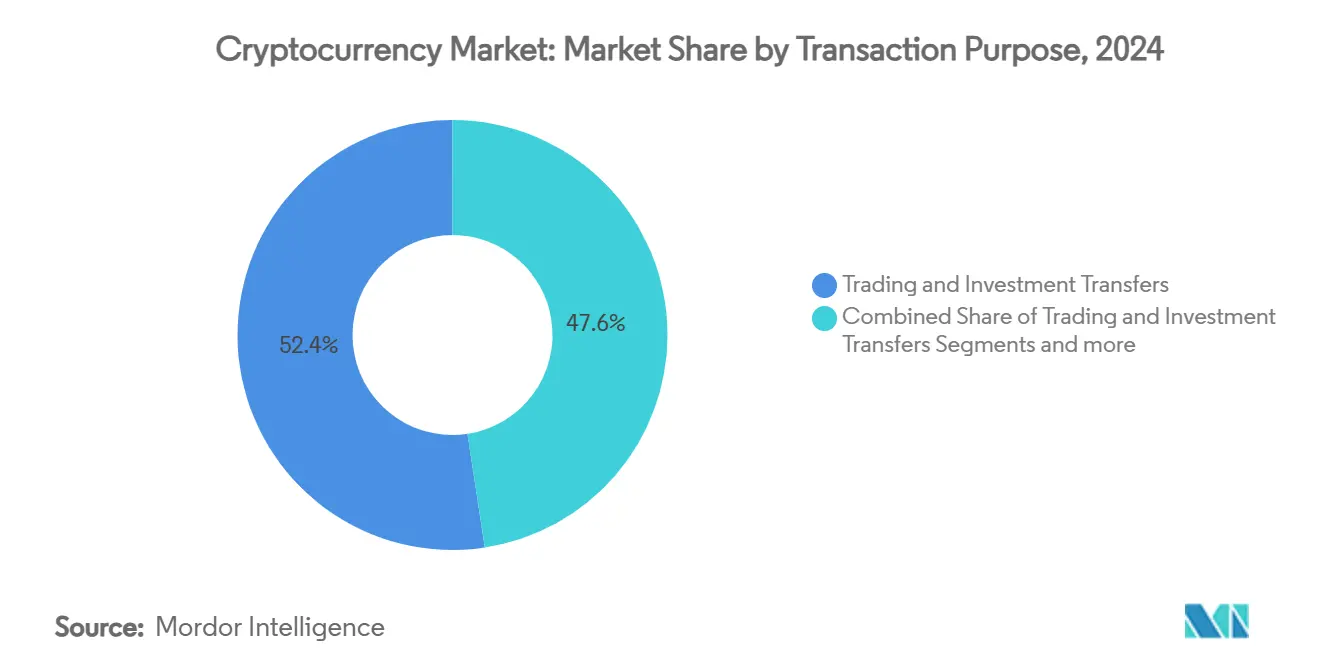

- By transaction purpose, Trading & Investment Transfers commanded 52.40% of the cryptocurrency market 2024 revenue; the same segment is projected to clock a 35.60% CAGR to 2030.

- By user type, Institutional players held 68.50% of the cryptocurrency market 2024 value, while Retail transactions are projected to grow at a 32.60% CAGR.

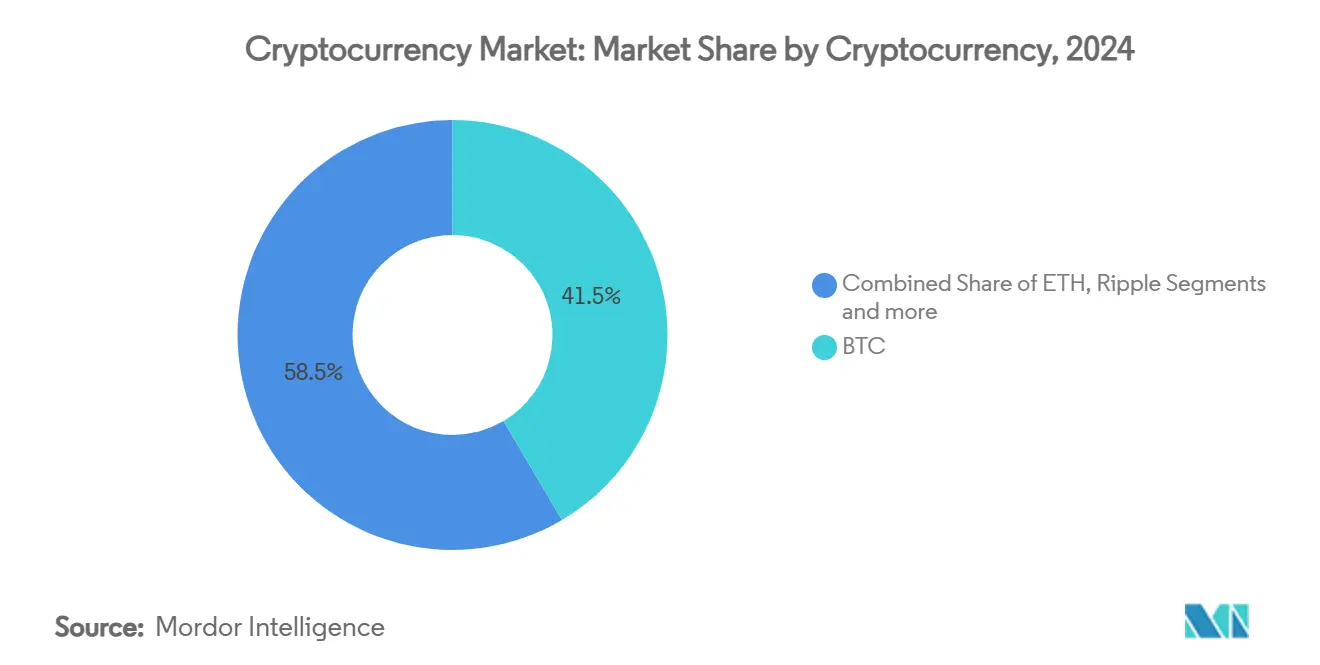

- By cryptocurrency, Bitcoin controlled 41.50% of the cryptocurrency market share in 2024 and is on pace for a 37.20% CAGR through 2030.

- By geography, North America led with 38.90% of the cryptocurrency market size in 2024; Asia-Pacific is expected to post the fastest 34.70% CAGR.

Global Cryptocurrency Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in regulated spot-Bitcoin ETFs (2024-25) | +8.5% | North America & EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Euro-wide MiCA roll-out unlocking cross-border crypto services | +6.2% | EU core, expansion to aligned jurisdictions | Long term (≥ 4 years) |

| Rapid CBDC pilots in APAC & GCC boosting settlement trials | +5.8% | Asia-Pacific & GCC core, global cross-border impact | Medium term (2-4 years) |

| AI-powered compliance tools lowering fraud-loss ratios | +4.1% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Corporate treasury adoption by NASDAQ-100 constituents | +3.7% | North America core, spreading to global corporates | Medium term (2-4 years) |

| Mobile-super-apps in Africa & SEA integrating USDC rails | +2.9% | Africa & SEA core, emerging market expansion | Long term (≥ 4 years) |

Source: Mordor Intelligence

Surge in regulated spot-Bitcoin ETFs transforms institutional access

Approvals for spot Bitcoin ETFs in 2024 eliminated custody hurdles that once discouraged public fund managers and life insurers from holding cryptocurrency assets. Within nine months of launch, cumulative ETF inflows surpassed USD 50 billion, illustrating that regulated wrappers can meet stringent mandate guidelines. When the SEC approved options on those ETFs in October 2024, with per-fund limits of 25,000 contracts, institutional desks gained price-discovery and hedging flexibility [1]Securities and Exchange Commission, “Order approving options on Bitcoin ETFs,” sec.gov . BlackRock’s BUIDL tokenized money-market fund amassed nearly USD 3 billion in assets during its first quarter, confirming that a wide pool of investors now views blockchain rails as operationally safe. The ETF milestone ripples beyond direct fund inflows: treasurers at NASDAQ-100 constituents have started evaluating Bitcoin allocations for cash-management diversity, and several insurance firms are applying for policy rider approvals that reference crypto holdings. Each new allocation deepens liquidity and helps the cryptocurrency market integrate with traditional price-formation venues.

Euro-wide MiCA implementation enables seamless cross-border operations

MiCA became fully enforceable across the EU in December 2024, delivering the world’s first holistic crypto framework and granting firms a single licence to serve all 27 member states [2]European Commission, “Markets in Crypto-Assets Regulation,” european-commission.europa.eu . More than 40 crypto-asset service-provider licenses were issued within six months, a pace that underscores industry demand for uniform rulebooks. Key provisions—such as mandatory one-to-one reserve backing for stablecoins and detailed governance standards—raise issuer quality and, in turn, bolster user confidence. Harmonized disclosures also allow institutional investors to compare service-provider risk on common metrics, reducing due diligence cycles. Competitive effects are already visible: payment aggregators based in smaller EU economies are using passport rights to enter high-volume markets such as Germany without setting up separate entities, accelerating fee compression. Over the longer term, MiCA’s clarity should lower the cryptocurrency market’s cost of capital by reducing regulatory uncertainty premiums.

CBDC pilots accelerate cross-border settlement innovation

Asia-Pacific and GCC authorities have moved from trials to live pilots on multi-currency CBDC bridges. China’s first live multi-CBDC Bridge transaction in Guangdong province delivered instant cross-border trade settlement and transparent audit trails. Project mBridge—linking the monetary authorities of Hong Kong, Thailand, UAE, and China—processed more than USD 22 million during pilot runs, demonstrating operational feasibility for wholesale FX settlement [3]Bank for International Settlements, “Project mBridge progress report,” bis.org . Parallel moves in the UAE include a retail CBDC slated for launch by end-2025 and a dirham-backed stablecoin aimed at cross-border e-commerce. These trials are prompting commercial banks to adapt treasury workflows, which increases demand for interoperable private-sector rails that can plug into central-bank platforms. In effect, CBDC progress expands addressable volume for the broader cryptocurrency market by legitimising distributed-ledger-based settlement.

AI-powered compliance tools reduce operational-risk profiles

Partnerships between government agencies and analytics providers such as AnChain.AI have showcased how machine-learning algorithms can trace illicit flows across complex token networks. The US Secret Service reported seizing USD 225 million in USDT connected to romance investment scams after applying AI-enhanced chain-analysis software [4]CoinDesk, “Ripple to buy Hidden Road,” coindesk.com . Smart-contract security also benefits: automated code-auditing now flags re-entrance and overflow vulnerabilities that have caused more than USD 2 billion in losses since 2020. Improved risk scoring persuades insurers to underwrite larger crime-coverage limits at lower premiums, and that reduces fixed costs for exchanges onboarding institutional clients. Consequently, operational resilience climbs, reinforcing the appeal of the cryptocurrency market to conservative capital pools such as pension trustees.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-grid backlash & miner moratoria in Nordics & U.S. | -4.3% | Nordic countries & select U.S. states | Short term (≤ 2 years) |

| Fragmented KYC / AML enforcement outside MiCA scope | -3.1% | Non-EU jurisdictions, emerging markets | Medium term (2-4 years) |

| Stable-coin de-pegs triggering tighter reserve mandates | -2.7% | Global, with focus on major stablecoin issuers | Short term (≤ 2 years) |

| Blockchain-engineering talent drain to Gen-AI sector | -2.2% | Developed markets with AI industry concentration | Long term (≥ 4 years) |

Source: Mordor Intelligence

Energy-grid backlash constrains mining-capacity expansion

Norway’s draft measure to halt high-power crypto mining indicates that even renewable-rich regions are reallocating hydro resources to data centres or manufacturing projects viewed as higher priority. In the US, 34 large Bitcoin mines consumed 32.3 TWh from mid-2022 to mid-2023, with fossil fuels supplying much of the load and impacting roughly 1.9 million residents through air pollutants. Academic studies place Bitcoin’s electricity share at 0.6% of global demand, fuelling calls for performance standards and carbon-intensity caps. Rising scrutiny accelerates mergers such as CoreWeave’s USD 9 billion purchase of Core Scientific, which intends to repurpose 1.3 GW of mining power for AI compute workloads. While such conversions help grid planners, they trim transaction-processing headroom, potentially slowing capacity growth even as network usage climbs.

Fragmented compliance standards create operational complexity

Outside MiCA’s perimeter, houses must navigate patchy Know-Your-Customer (KYC) and Anti-Money-Laundering (AML) regimes. The Bank for International Settlements compared 11 authorities and found wide gaps in licensing thresholds, reserve-asset composition, and consumer redress. Canada extended its value-referenced crypto-asset compliance deadline to December 2024 and granted immediate clearance only to USDC, leaving other issuers in limbo. Each divergent rule set forces firms to run separate onboarding flows and reporting templates, raising fixed costs per jurisdiction. Smaller startups incur disproportionate burdens that deter geographic expansion, curbing competitive intensity and potentially slowing innovation in segments such as cross-border remittances, which rely on license coverage across multiple corridors.

Segment Analysis

By Transaction Purpose: Trading dominance drives infrastructure investment

Trading & Investment Transfers generated 52.40% of revenue in 2024 and are anticipated to grow at 35.60% CAGR, ensuring that this activity continues to anchor overall cryptocurrency market growth. Liquidity depth has improved because regulated ETFs allow asset managers to allocate billions without operating digital wallets. Coinbase’s USD 2.9 billion purchase of Deribit is projected to give it 85% of crypto options flow, securing margin-rich derivatives revenue. High-frequency trading firms are deploying co-located servers at major exchanges, reducing spread costs and stimulating order-book density.

Payments & Remittances stand as the second-largest avenue. Mobile super-apps across Southeast Asia and Africa, such as Grab, now permit users in Singapore to top up wallets with Bitcoin, Ether, and stablecoins, extending day-to-day utility. Partnerships with StraitsX and Alipay+ let merchants receive stablecoins while still settling in local fiat, cutting interchange expense. Meanwhile, JPMorgan’s Kinexys initiative to settle on-chain USD-EUR FX by early 2025 hints at corporate demand for same-day cross-border workflows.

Note: Segment shares of all individual segments available upon report purchase

By User Type: Institutional leadership meets retail acceleration

Institutional users accounted for 68.50% of value in 2024, reflecting how custody readiness and ETF vehicles have de-risked entry for large asset pools. MicroStrategy’s 226,500-bitcoin position, worth over USD 8.3 billion, has become a benchmark for treasury diversification. SEC filings reveal that more than 64 public companies collectively held 688,000 BTC by May 2025, and brokerage surveys predict that corporate treasuries could own 2.3 million BTC by 2026 if current adoption rates continue. Pension trustees are also piloting 1% allocation sleeves, citing positive Sharpe-ratio effects in portfolio simulations.

Retail activity, although smaller, is expanding at 32.60% CAGR, fuelled by seamless on-ramps. Mastercard’s partnership with Fiserv and Chainlink lets 3 billion cardholders purchase crypto assets directly on the chain with familiar card rails. Grab’s crypto features increased monthly active wallet users by 18% within two quarters, signalling sticky engagement. Declining swap fees on decentralised exchanges and simplified address-verification flows lower entry barriers further, widening the cryptocurrency market’s demographic footprint and diversifying liquidity away from a purely institutional core.

By Cryptocurrency: Bitcoin dominance amid diversification

In 2024, Bitcoin accounted for 41.50% of the cryptocurrency market, with a projected compound annual growth rate (CAGR) of 37.20%, indicating its market share could approach 50% by 2030. The stabilization of order books during periods of heightened volatility has been supported by increased ETF bids and growing corporate treasury adoption, which have mitigated the impact of sell-offs. Additionally, the forthcoming "Proto-Danksharding" upgrades are expected to significantly lower transaction costs, enhancing Bitcoin's utility in micro-payment transactions. These developments position Bitcoin as a resilient and competitive asset within the broader cryptocurrency market. The combination of technological advancements and institutional interest underscores its potential for sustained growth over the forecast period.

Ripple focuses on cross-border settlement and gained momentum when Mercado Bitcoin unveiled plans to tokenise USD 200 million of assets on the XRP Ledger. Bitcoin Cash carves out a niche in high-velocity payments owing to block-size economics, while Cardano emphasises formal methods and environmental efficiency, which resonates with ESG-oriented investors. Interoperability across 16 blockchains helps USDC penetrate regional payment corridors., showing that exchanges now build proprietary stacks to capture fee income outside spot trading.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America captured 38.90% of the cryptocurrency market in 2024, supported by the most advanced regulatory environment and deep institutional infrastructure. SEC approval of spot-Bitcoin ETFs catalysed capital inflows and provided a blueprint for other jurisdictions to study. Public companies in the region, led by MicroStrategy, collectively held over 688,000 BTC by May 2025, anchoring local liquidity. Canada’s granular stablecoin rules, which currently permit only USDC as a value-referenced asset, aim to balance innovation with systemic safeguards, fostering user trust. Liquidity concentration across exchanges headquartered in the United States and Canada feeds a virtuous circle, attracting market-making desks that prefer depth and predictable oversight.

Asia-Pacific is growing fastest at 34.70% CAGR, driven by CBDC pilots, super-app integrations, and supportive policy sandboxes. China’s live multi-CBDC Bridge trade in Guangdong showcased near-instant settlement, prompting regional banks to explore direct ledger integration. Project mBridge, which processed USD 22 million in pilot trades, reinforced the feasibility of multi-currency settlements without correspondent banks. In Southeast Asia, Grab’s stablecoin top-up feature increased daily active transactions across its financial services vertical, demonstrating that consumer demand exists when UX is uncomplicated. Australia’s Reserve Bank joined pilots on tokenised carbon credits, revealing that even highly regulated markets see strategic gains in distributed ledger adoption.

Europe benefits from MiCA’s harmonised licence regime, which removed 27 parallel rulebooks and cut time-to-market for service providers. Switzerland’s blockchain cluster grew from 300 companies in 2017 to 1,200 in 2025, employing over 6,000 staff even amid a talent shortage caused by stiff competition from other tech sectors. Venture funding is funneling into Zug-based custody providers that meet MiCA mandates, suggesting that the EU will remain a hub for regulated institutional solutions. The Middle East and Africa, though smaller today, show strong potential: the UAE’s digital dirham roadmap and Saudi Arabia’s involvement in mBridge reflect a determination to set regional payment standards. Many African fintechs are leapfrogging card networks by embedding USDC transfer rails directly into mobile wallets, further extending the global reach of the cryptocurrency market.

Competitive Landscape

The cryptocurrency market exhibits moderate concentration: five platforms processed the majority of global volume in 2024. Scale advantages revolve around liquidity depth, compliance infrastructure, and engineering talent. Coinbase’s USD 2.9 billion takeover of Deribit will likely grant it an 85% grip on global crypto options, cementing derivatives leadership and widening its revenue base beyond spot fees. Binance maintains the largest spot volumes but faces strategic re-positioning after the SEC lawsuit dismissal with prejudice in May 2025, which could spur governance reforms.

Ripple’s USD 1.25 billion acquisition of prime broker Hidden Road adds a platform that clears USD 3 trillion annually, integrating settlement and custody for institutional clients. Kraken joined Coinbase’s Base in the Superchain by launching Ink, allowing exchanges to own transaction pathways and monetise gas fees alongside trading spreads. Traditional banks are also entering: JPMorgan rebranded Onyx to Kinexys, planning on-chain FX for USD-EUR pairings, which threatens to siphon high-value flows from native crypto platforms.

Infrastructure conversion is another theme. CoreWeave’s USD 9 billion buyout of Core Scientific transfers 1.3 GW of mining power to AI computing, illustrating how rising AI demand competes with crypto for data-centre capacity. Such shifts may tighten Bitcoin hash-rate growth, benefiting miners that sustain renewable-energy footprints. On talent, Switzerland’s blockchain sector signals shortages that could hamper innovation pace if brain drain to generative AI continues. Yet venture capital is actively backing compliance-software startups, a niche becoming critical as regulations mature. Overall, rivalry continues to pivot toward scalable compliance tech and institutional distribution rather than purely on exchange fees.

Cryptocurrency Industry Leaders

-

Coinbase Global Inc.

-

Binance Holdings Ltd.

-

Tether Limited (USDT)

-

Circle Internet Financial LLC (USDC)

-

OKX (OK Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CoreWeave completed its USD 9 billion all-stock acquisition of Core Scientific, gaining 1.3 GW of power capacity and signaling a pivot of mining infrastructure toward AI workloads.

- July 2025: Coinbase bought token-management platform Liquifi, aiming to streamline token launches as US rules soften.

- June 2025: Robinhood introduced stock tokens, unveiled its own Layer-2 blockchain, and expanded perpetual futures and staking services in the EU and US.

- April 2025: Ripple agreed to acquire prime broker Hidden Road for USD 1.25 billion, extending its institutional settlement reach.

Global Cryptocurrency Market Report Scope

Cryptocurrencies are digital currencies that serve as an alternative form of payment, utilizing encryption algorithms for their creation. Cryptocurrencies are both currency and virtual accounting systems that leverage encryption technologies. To engage with cryptocurrencies, a cryptocurrency wallet is required. The report gives an understanding of the present status of the cryptocurrency market, along with detailed market analysis, their structural intricacies explained in simple terms, risks and opportunities, current regulatory frameworks, and impact on existing systems—an in-depth analysis of the implications for monetary and fiscal policies. The cryptocurrency market is segmented by market capitalization of cryptocurrencies and cryptocurrency adoption by geography. By market capitalization of cryptocurrencies, the market is segmented into Bitcoin, Ethereum, Ripple, Bitcoin Cash, Cardano, and others. By cryptocurrency adoption by geography, the market is segmented into the Middle East & Africa, the Americas, Europe, and APAC. The report offers the market sizes and forecast values (USD) for all the above segments.

| By Transaction Purpose | Payments & Remittances | ||

| Trading and Investment Transfers | |||

| Decentralized Finance (DeFi) Protocol Flows | |||

| Others (Cross-border B2B Settlements, Asset Tokenization & Settlements, NFT Purchases) | |||

| By User Type | Retail | ||

| Institutional | |||

| By Cryptocurrency | BTC | ||

| ETH | |||

| Ripple | |||

| Bitcoin Cash | |||

| Cardano | |||

| Others | |||

| By Geography | North America | Canada | |

| United States | |||

| Mexico | |||

| South America | Brazil | ||

| Peru | |||

| Chile | |||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| BENELUX | |||

| NORDICS | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| South East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Nigeria | |||

| Rest of Middle East and Africa | |||

| Payments & Remittances |

| Trading and Investment Transfers |

| Decentralized Finance (DeFi) Protocol Flows |

| Others (Cross-border B2B Settlements, Asset Tokenization & Settlements, NFT Purchases) |

| Retail |

| Institutional |

| BTC |

| ETH |

| Ripple |

| Bitcoin Cash |

| Cardano |

| Others |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the projected value of the cryptocurrency market by 2030?

The cryptocurrency market is forecast to reach USD 7.98 trillion by 2030, supported by a 30.10% CAGR.

Which segment contributes most to current revenue?

Trading & Investment Transfers contribute 52.40% and are also the fastest-growing segment at 35.60% CAGR.

How dominant is Bitcoin within the cryptocurrency market?

Bitcoin held 41.50% of the cryptocurrency market share in 2024 and is expected to grow at a 37.20% CAGR through 2030.

Why is Asia-Pacific the fastest-growing region?

CBDC pilots, mobile-super-app integrations, and supportive regulatory sandboxes drive a 34.70% CAGR for Asia-Pacific.

How concentrated is the competitive landscape?

The five largest exchanges handle the majority of global volume, which signals moderate but not excessive dominance.

What role does MiCA play in Europe’s growth?

MiCA replaced 27 separate rulebooks with a single licence passport, lowering compliance costs and accelerating cross-border service expansion.

Page last updated on: July 8, 2025