Corrugation Materials Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

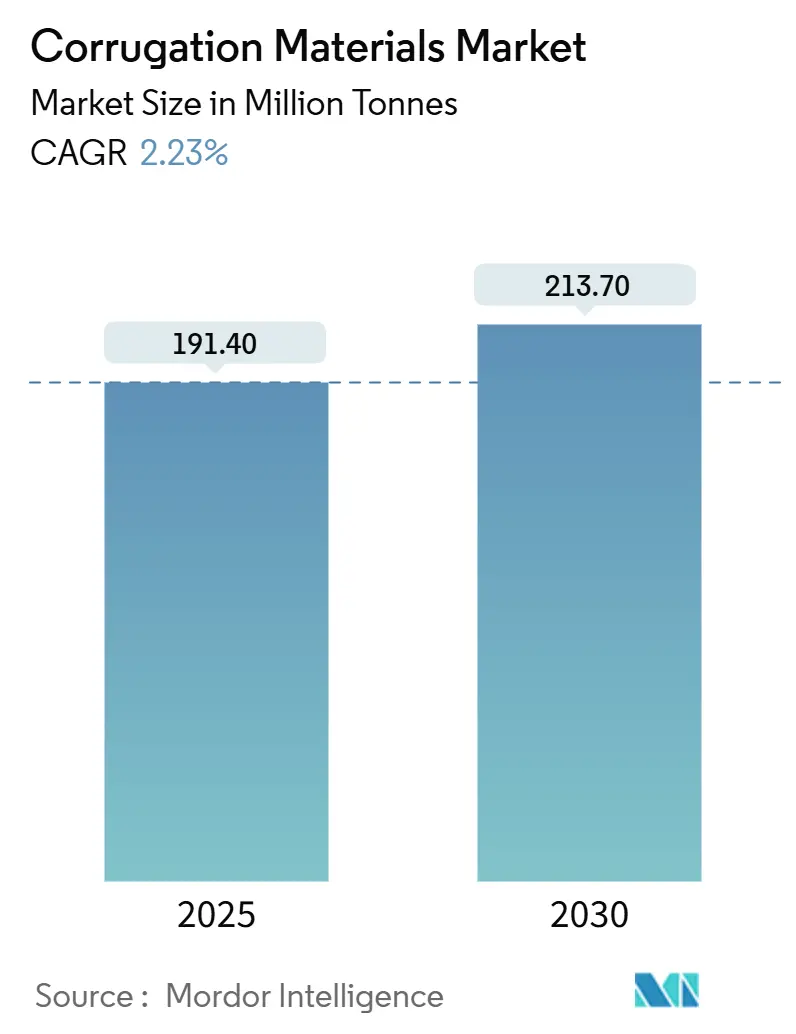

| Market Volume (2025) | 191.40 Million tonnes |

| Market Volume (2030) | 213.70 Million tonnes |

| Growth Rate (2025 - 2030) | 2.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corrugation Materials Market Analysis by Mordor Intelligence

The corrugation materials market size reached 191.4 million tonnes in 2025 and is forecast to attain 213.7 million tonnes by 2030, advancing at a 2.23% CAGR over the period. This outlook is underpinned by e-commerce fulfilment growth, stricter recyclability mandates, and an industry-wide pivot from commodity tonnage to value-engineered grades that balance lightweighting with performance. Asia-Pacific remains the engine of demand thanks to manufacturing rebounds and digital-commerce logistics upgrades, while Europe and North America continue to shape global specification trends through sustainability legislation. Competitive intensity is rising as integrated producers acquire regional players to secure fibre streams and digital‐printing know-how. Micro-flute innovations, barrier-enhanced liners, and automation-ready board designs are opening premium niches that support pricing resilience even when recovered-paper volatility compresses margins. Sustainability credentials now influence contract awards as major brands adopt science-based climate targets and require verifiable circularity across packaging supply chains.

Key Report Takeaways

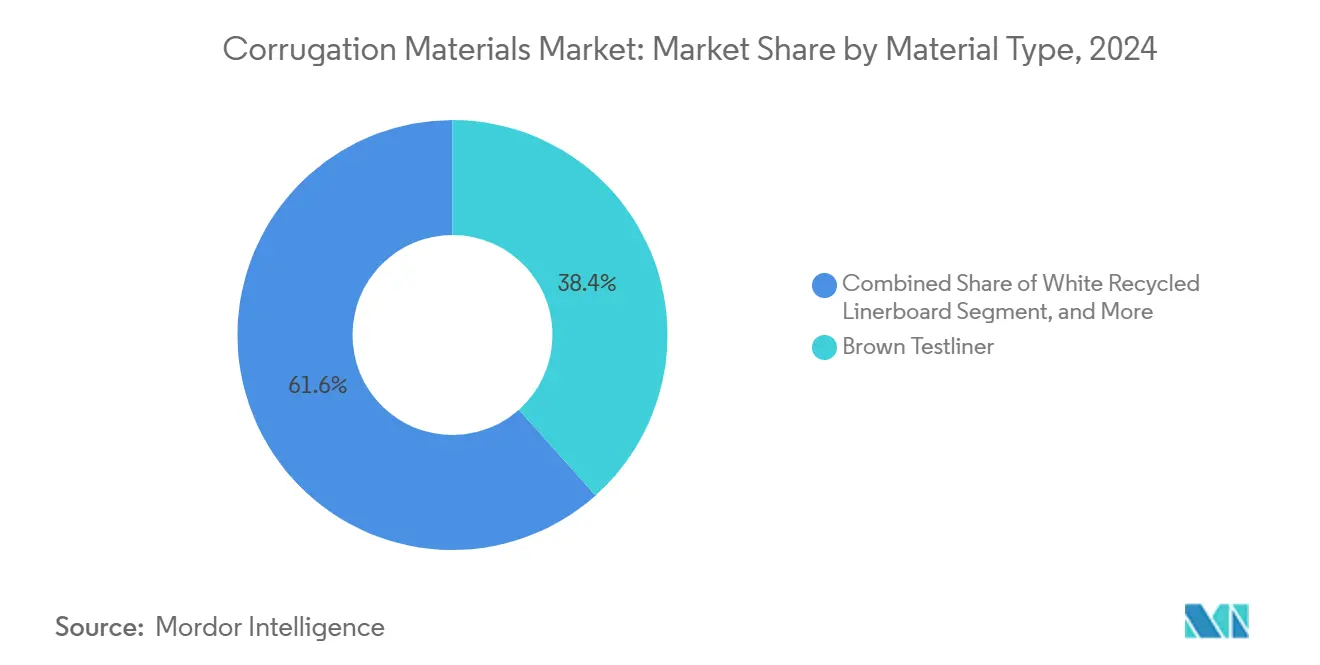

- By material type, Brown Testliner led with 38.42% corrugation materials market share in 2024.

- By flute type, C Flute held 31.63% of the corrugation materials market size in 2024.

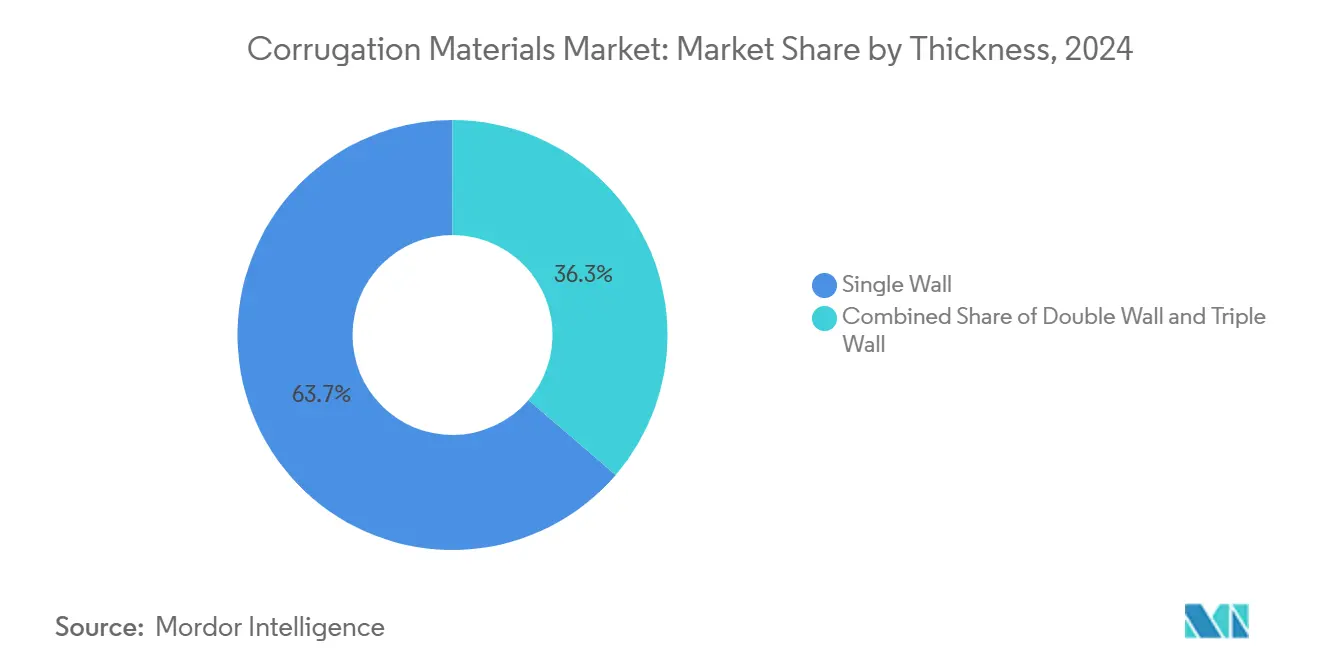

- By thickness, Single Wall accounted for 63.72% share of the corrugation materials market size in 2024.

- By end-use, the corrugation materials market size for e-Commerce and Retail is projected to grow at a 5.46% CAGR between 2025-2030.

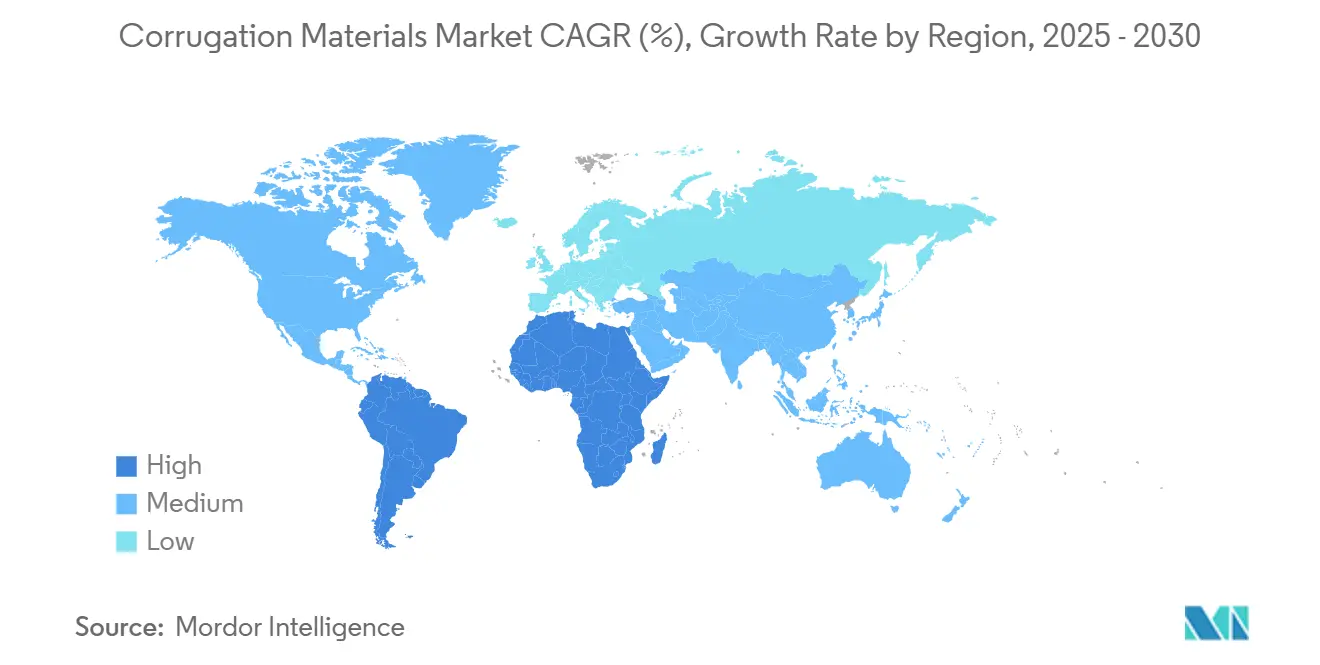

- By geography, the corrugation materials market size for Asia-Pacific is projected to grow at a 5.03% CAGR between 2025-2030.

Global Corrugation Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfilment surge post-2025 | +0.8% | Global, North America and Asia-Pacific | Medium term (2-4 years) |

| Sustainability mandates and recyclability targets | +0.6% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Food-grade lightweighting initiatives | +0.4% | Global, developed markets first | Medium term (2-4 years) |

| Manufacturing output recovery in emerging markets | +0.5% | Asia-Pacific core, spill-over to Latin America | Short term (≤ 2 years) |

| Next-gen lightweight high-performance fluting grades adoption | +0.3% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Digital print-ready corrugated substrates | +0.2% | Global premium markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Fulfilment Surge Post-2025

Parcel shipping growth is reshaping flute geometry, board basis weight, and print-surface demands as brands optimise mail-order pack formats. Packaging Corporation of America recorded a 2.5% increase in corrugated shipment volume during Q1 2025, attributing the rise to direct-to-consumer flows. Smaller, more frequent deliveries need boards that withstand automated sortation yet minimise fibre per pack, accelerating micro-flute uptake that offers higher edge-crush strength and vivid graphics. Asia-Pacific remains pivotal because cross-border e-commerce is on track to reach 6.4% of global GDP in 2025. The resulting throughput pressures are compelling converters to expand digital printing lines that enable late-stage customisation without slowing fulfilment nodes. Material vendors able to supply consistent, lightweight, high-printability substrates are gaining preferred-supplier status in omnichannel contracts.

Sustainability Mandates and Recyclability Targets

The European Union’s circular-economy package and the United States’ state-level extended-producer-responsibility laws require minimum recycled content and transparent life-cycle reporting, prompting mills to boost recovered-fibre integration. WestRock now reports 97.8% of its output as recyclable or reusable and has allocated more than USD 1 billion to forestry initiatives that safeguard supply continuity. Multinational brand owners demand harmonised packaging across regions, so compliance pressures in Europe cascade into Asia and Latin America. Regulatory timelines favour mills that can verify chain-of-custody and deliver downgauged liners without compromising box performance. Consequently, research into fibre-strength additives and refined pulping has intensified as producers look to trim basis weight while maintaining stacking strength.

Food-Grade Lightweighting Initiatives

Brands in chilled and ambient food categories are reducing secondary-pack weight to curb transport emissions and meet science-based targets. The U.S. FDA’s clearance of advanced cellulose derivatives for food contact unlocks new barrier technologies that keep grease and moisture at bay. Graphic Packaging generated more than USD 200 million in innovation-related sales by commercialising barrier-coated corrugated trays that displace plastic clamshell. Moisture-tolerant liners are gaining favour in fresh-produce channels where airflow and water-vapour transport dictate shelf life. Developed economies lead adoption, yet global food exporters are following suit to comply with destination-market regulations. Suppliers that combine virgin-fibre purity with recycled-fibre economics are positioned to win multi-year supply agreements.

Manufacturing Output Recovery in Emerging Markets

Industrial production in Asia and Oceania (excluding China) grew 1.7% in Q2 2024, boosting downstream need for shipping containers. China’s corrugating-medium output rose 12.34% in 2021 to 26.85 million tonnes. Mexico’s packaging-machinery imports climbed to USD 906 million in 2022, reflecting capital inflows into agribusiness and near-shoring. This resurgence shortens supply routes and incentivises local board conversions to lower freight spend and greenhouse-gas footprints. Corrugation materials suppliers are fast-tracking capacity in Southeast Asia and Northern Mexico to capture industrial migration from higher-cost regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered paper and virgin pulp price volatility | -0.4% | Global, import-dependent regions | Short term (≤ 2 years) |

| Plastics and flexible packaging substitution threat | -0.3% | Global, cost-sensitive niches | Medium term (2-4 years) |

| Freight surcharges and logistics bottlenecks | -0.2% | Global, trade-dependent regions | Short term (≤ 2 years) |

| Water-stress limitations on pulp/corrugating mills | -0.2% | Water-scarce areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Paper and Virgin Pulp Price Volatility

The Producer Price Index for recycled paperboard hit 412.949 in March 2025, while wood-pulp pricing peaked at 219.835 in May 2024, underscoring cost swings that erode converter margins. Smurfit WestRock flagged elevated recovered-fibre expenses among the main drags on Q2 2024 earnings. Import-reliant regions face an extra currency risk overlay when hedging contracts, complicating budget planning. Larger integrated players better absorb turbulence because captive recycling loops dampen exposure. Smaller independents resort to surcharge clauses or shorter quotation validity, which in turn pressures customer relationships.

Plastics and Flexible Packaging Substitution Threat

Continuous improvements in monomaterial polyethylene and high-barrier films threaten corrugated in moisture-sensitive and high-visibility SKUs. While regulatory sentiment in Europe tilts toward fibre, cost-driven buyers in emerging markets still opt for bags or pouches that undercut box prices by up to 30%. Corrugated suppliers therefore extend R&D into barrier-coated liners and humidity-stable starch to match performance metrics. Failure to meet these benchmarks risks volume leakage to plastics precisely in high-growth consumer verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Content Drives Innovation

Brown Testliner, at 38.42% corrugation materials market share in 2024, anchors global supply thanks to cost advantage and broad corrugator compatibility. White Recycled Linerboard shows a 4.28% CAGR, reflecting brand owners’ preference for high-print surfaces paired with circular-economy credentials. White Fresh Fibre Linerboard retains niche strength in food-contact formats where purity trumps cost. Brown Kraftliner and Fresh Fibre Fluting serve industrial and heavy-duty shippers that tolerate price premiums for burst resistance. Recycled Fluting remains the largest fluting sub-segment, aided by quality gains that match virgin grades for edge-crush and flat-crush metrics. The corrugation materials market size for Recycled Fluting is set to widen as integrated mills reach 93% OCC recycling performance, insulating supply chains against virgin-pulp variability. Integrated producers leverage closed-loop collection networks that guarantee feedstock and support emissions targets.

Upcycling initiatives now explore enzymatic deinking and fibre-length preservation to unlock higher-value white recycled liners. Multinational converters standardise on recycled grades to limit regulatory discrepancies across regions, accelerating demand convergence. Producers that scale bleach-free whitening chemistries could trim energy use and lift brightness without adding chlorine. Material differentiation is thus tilting from commodity tonnage to engineered fibre blends aligned with downstream print and barrier specifications.

By Flute Type: Micro-Flutes Gain Traction

C Flute retained 31.63% of shipments in 2024 by balancing cushioning, rigidity, and fibre economy. Yet F and G micro-flutes are forecast to grow 3.61% CAGR through 2030 as e-commerce, cosmetics, and consumer-electronics brands favour slim profiles that fit automated pick-and-pack frames. The corrugation materials market size for micro-flute grades is expanding because thin calipers reduce dimensional weight fees while preserving crush strength. A Flute dominates appliance and industrial components where void fill matters, whereas E Flute services litho-laminated displays that demand offset-grade graphics. B Flute occupies retail multipacks that need space efficiency but modest cushioning.

Mid-range corrugators are retrofitted with high-speed slotters and precision pre-heaters to limit flute washboarding at lower calipers. FEFCO’s R&D in nano-fibrillated cellulose and starch crosslinking upgrades micro-flute rigidity, letting converters down-gauge paper yet achieve equivalent performance. As digital printing proliferates, fine-flute smoothness becomes a brand asset, reinforcing the migration trend away from legacy flute sizes.

By Thickness: Single Wall Dominance Persists

Single Wall commanded 63.72% of global tonnage in 2024 as it meets most shipping durability thresholds at the lowest cost. Double Wall’s 3.07% CAGR is propelled by heavy e-commerce loads and industrial users switching to fibre from wood or EPS crates. The corrugation materials market size for Double Wall boxboard is projected to grow as automation requires consistent stackability. Triple Wall, though niche, secures contracts in specialized machinery export and construction panels where drop-test criteria are stringent.

Automation on packing lines rewards board that runs flat and square; hence, mills invest in tighter moisture-profile controls to boost converting yields. Single Wall grades now incorporate high-freeness fluting and light-basis liners to shed mass without losing compression. Double Wall variants see hybrid builds micro over C Flute pairings to merge graphics with beefy structural cores, illustrating how design flexibility stretches across thickness categories.

By End-Use Industry: E-commerce Reshapes Demand

Food and Beverages retained 46.31% share in 2024, testament to corrugated boxes’ role in safeguarding perishables while offering retail display real estate. E-commerce and Retail orders are climbing at 5.46% CAGR, underpinning the corrugation materials market size trajectory through 2030 as consumer doorstep delivery habits persist. Consumer-electronics shipments adopt die-cut inserts and micro-flute wraps for in-box presentation. Industrial and Automotive Parts rely on heavy-duty double and triple wall to guard precision components. Agriculture and Fresh Produce segments opt for breathable, coated boxes that inhibit condensation during cold-chain transits. Personal-care SKUs want photo-quality graphics, while Healthcare and Pharmaceutical orders require tamper-evident seals and validated traceability.

Direct-to-consumer brand strategies prioritise unboxing aesthetics, pushing converters to blend water-based inks, varnishes, and embossing on recycled liners. Food safety regulations drive demand for mineral-oil-free inks and certified allergen-barrier coatings. Suppliers that bundle design labs with global distribution networks win multi-year partnerships because they guarantee consistency across regional fulfilment hubs.

Geography Analysis

Asia-Pacific’s corrugation materials market size topped 97 million tonnes in 2025 and will likely exceed 124 million tonnes by 2030, driven by electronics export volumes and regional fulfilment hubs. China accounts for roughly 47% of regional consumption, followed by India at 18%, yet Indonesia and Vietnam show the fastest incremental gains due to footwear and apparel near-shoring. Government incentives for recycled-paper imports and tax holidays on new corrugators accelerate capacity additions, smoothing supply chains that previously relied on linerboard imports.

North America consumed 43 million tonnes in 2025, with a balanced split between integrated majors and sheet-feeder independents. E-commerce remains the main growth lever; parcel-volume forecasts point to double-digit carton demand for at least three years. Brands now demand porch-pirate-resistant, tamper-evident constructions, prompting converters to introduce hidden tear strips and RFID tags. Regulatory shifts toward extended producer responsibility in states such as California introduce cost-recovery fees that nudge fibre content optimisation.

Europe trails North America in tonnage but leads the adoption of high-recycled grades. The corrugation materials market share for recycled linerboard in Europe exceeds 80% thanks to robust collection networks. Southern and Eastern Europe recorded stronger box demand in 2024 than mature Western markets as consumer packaged goods growth outstripped GDP. Investment continues in Poland and Turkey for sheet plants that feed regional export corridors into Germany and France.

Latin America reached 12 million tonnes in 2025, bolstered by agribusiness. Mexican tomato exporters specify water-resistant board to survive cold-chain shock between farm and U.S. supermarkets. Brazil’s forestry giants leverage FSC-certified plantations to compete on virgin-fibre kraftliner exports. Meanwhile, Middle East and Africa use cases cluster around processed food and FMCG imports packed in single-wall boxes shipped from Asia. Rising local food-processing capacity is expected to spark micro-flute adoption for retail snack packs.

Competitive Landscape

Global capacity is moderately consolidated: the five largest groups held roughly 45% of shipments in 2024, while numerous regionals and speciality mills account for the balance. International Paper’s USD 8.5 billion purchase of DS Smith secured European reach and integrated digital-printing assets. Packaging Corporation of America bought Greif’s containerboard mills for USD 1.8 billion, adding 800,000 tonnes of kraftliner output in July 2025. Smurfit WestRock shuttered 500,000 tonnes of legacy capacity in 2025, redeploying capex into lightweight recycled grades.

Competitive moats derive from integrated fibre loops, patented barrier coatings, and large-scale converting footprints. WestRock highlights that 60% of its box plants now run high-automation gluer lines, cutting per-unit labour cost by 15%. Mondi is investing EUR 0.6 billion to expand Eastern-European corrugated capacity, betting on near-shoring of consumer-durables assembly [1]Mondi Group, “Interim Mondi Group Half-Year Results 2024,” mondi.com. Billerud’s strategy emphasises lighter, stronger board aimed at displacing plastic trays in quick-service restaurants [2]Billerud, “Billerud CMD 2024,” billerud.com.

Disruptors include specialty recyclers producing high-brightness deinked pulp and technology firms offering AI-driven demand forecasting that slashes inventory. Patent filings in cellulose-ester film by Eastman Chemical aim to merge paper rigidity with plastic clarity [3]Google Patents, “Cellulose and Cellulose Ester Film,” patents.google.com . Contract negotiations increasingly weigh carbon-footprint disclosures, nudging laggard mills toward renewable-energy conversions.

Corrugation Materials Industry Leaders

International Paper Company

Mondi plc

Stora Enso Oyj

Smurfit WestRock plc

Oji Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Packaging Corporation of America completed its USD 1.8 billion acquisition of Greif’s containerboard business, adding 800,000 tonnes of capacity

- May 2025: Smurfit WestRock reported Q1 net sales of USD 7.656 billion and confirmed the closure of 500,000 tonnes of paper capacity in North America

- April 2025: International Paper posted USD 5.9 billion in Q1 sales following the DS Smith acquisition and opened a European headquarters in London

- December 2024: Billerud detailed its focus on lighter, stronger corrugated materials during its Capital Markets Day

Global Corrugation Materials Market Report Scope

| White Fresh Fibre Linerboard |

| White Recycled Linerboard |

| Brown Kraftliner |

| Brown Testliner |

| Fresh Fibre Fluting |

| Recycled Fluting |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F and G (Micro) Flutes |

| Single Wall |

| Double Wall |

| Triple Wall |

| Food and Beverages |

| E-commerce and Retail |

| Consumer Electronics |

| Industrial and Automotive Parts |

| Agriculture and Fresh Produce |

| Personal Care and Household Goods |

| Healthcare and Pharmaceuticals |

| Other End-Use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | White Fresh Fibre Linerboard | ||

| White Recycled Linerboard | |||

| Brown Kraftliner | |||

| Brown Testliner | |||

| Fresh Fibre Fluting | |||

| Recycled Fluting | |||

| By Flute Type | A Flute | ||

| B Flute | |||

| C Flute | |||

| E Flute | |||

| F and G (Micro) Flutes | |||

| By Thickness | Single Wall | ||

| Double Wall | |||

| Triple Wall | |||

| By End-Use Industry | Food and Beverages | ||

| E-commerce and Retail | |||

| Consumer Electronics | |||

| Industrial and Automotive Parts | |||

| Agriculture and Fresh Produce | |||

| Personal Care and Household Goods | |||

| Healthcare and Pharmaceuticals | |||

| Other End-Use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the corrugation materials market in 2025?

The corrugation materials market size stands at 191.4 million tonnes in 2025.

What is the forecast CAGR for corrugated materials from 2025 to 2030?

Shipments are projected to rise at a 2.23% CAGR through 2030.

Which region generates the highest demand for corrugation materials?

Asia-Pacific leads with 51.27% of global volume in 2024 and is growing the fastest through 2030.

Which flute type is gaining the most traction in e-commerce packaging?

F and G micro-flutes are expanding at 3.61% CAGR because they meet lightweighting and printability requirements.

Why are recycled liners growing faster than virgin liners?

Sustainability mandates and brand recyclability targets are pushing adoption of White Recycled Linerboard, currently the fastest-growing material segment.

What recent acquisition reshaped the competitive landscape?

International Paper’s USD 8.5 billion takeover of DS Smith expanded its European footprint and digital-printing capacity.

Page last updated on: