Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 724.35 Billion |

| Market Size (2030) | USD 966.84 Billion |

| Growth Rate (2025 - 2030) | 5.98% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contract Manufacturing Market Analysis by Mordor Intelligence

The Contract Manufacturing Market size is estimated at USD 724.35 billion in 2025, and is expected to reach USD 966.84 billion by 2030, at a CAGR of 5.98% during the forecast period (2025-2030).

The contract manufacturing market is expanding as brand owners shift toward asset-light operating models, outsource specialized production steps, and diversify footprints to soften supply-chain shocks created by geopolitical frictions. Momentum stems from near-shoring incentives in North America, sovereign wealth investments in the Gulf, and automation upgrades across Asian electronics manufacturing services (EMS). Demand for end-to-end partners able to manage regulatory compliance, intellectual-property security, and rapid design iteration is reshaping vendor selection criteria. Meanwhile, consolidation among pharmaceutical contract development and manufacturing organizations (CDMOs) is raising barriers to entry, while EMS companies invest in AI-enabled factories to protect margins as labor arbitrage fades.

Key Report Takeaways

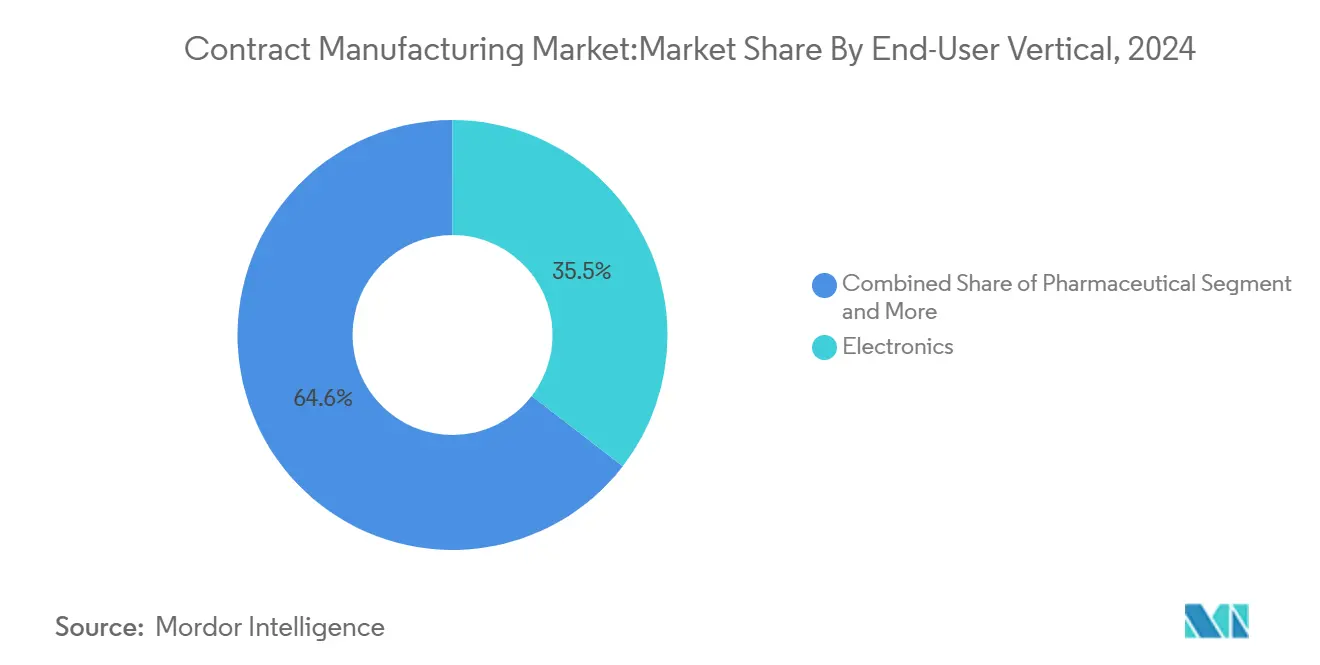

- By end-user vertical, electronics led with 35.45% of contract manufacturing market share in 2024; pharmaceuticals is forecast to expand at a 9.8% CAGR through 2030.

- By contract type, strategic partnerships commanded 60.54% of the contract manufacturing market in 2024, while project-based contracts are advancing at a 7.5% CAGR through 2030.

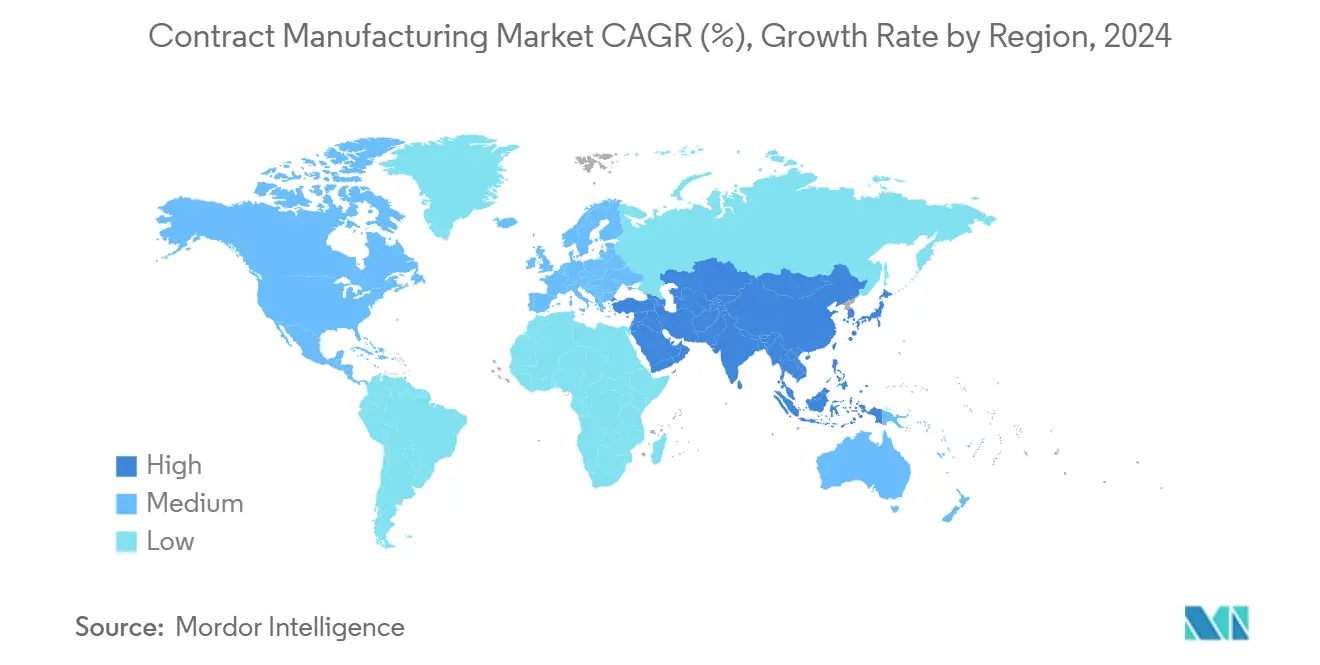

- By geography, Asia-Pacific held 45.67% of the contract manufacturing market share in 2024; the Middle East & Africa region is projected to grow at 9.2% CAGR to 2030.

Global Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-shoring mandates under USMCA | +1.2% | North America, Mexico | Medium term (2-4 years) |

| AI-enabled smart-factory retrofits in Asian tier-1 EMS | +0.9% | Asia-Pacific; global spill-over | Short term (≤ 2 years) |

| Pharmaceutical capacity crunch driving emergency CDMO outsourcing | +0.8% | Europe, North America | Short term (≤ 2 years) |

| EV battery thermal-management outsourcing in China and Korea | +0.6% | Asia-Pacific core; spill-over to North America | Medium term (2-4 years) |

| GCC localization funds under Vision 2030 | +0.4% | Middle East & Africa | Long term (≥ 4 years) |

| Micro-lot 3-D printing for rapid consumer-goods launches | +0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Near-shoring Mandates in USMCA Region

North American policy continuity through the USMCA agreement is driving migration of assembly lines from East Asia to Mexico, where 350,000 reshored jobs materialized in 2024 alone. Under the CHIPS Act, USD 52.7 billion in incentives for domestic semiconductor capacity is reinforcing this pivot[1]Joseph R. Biden, “Fact Sheet: CHIPS and Science Act Will Strengthen U.S. Manufacturing,” The White House, whitehouse.gov. Chinese battery firms announced USD 27 billion in overseas investments to bypass tariffs, underscoring the global realignment. Mexican exports to the United States grew 4.6% year on year in 2024 and overtook Chinese volumes, validating the shift[2]Raquel Buenrostro, “Mexico’s 2024 Manufacturing Export Performance,” Secretaría de Economía, economia.gob.mx. Proximity is delivering faster engineering change orders, tighter quality oversight, and lower logistics risk, although skilled-labor and infrastructure readiness remain gating factors.

AI-enabled Smart-factory Retrofits Among Asian Tier-1 EMS

Foxconn’s FoxBrain platform enabled 80% automation of new production set-up tasks, a milestone prompting peers to intensify AI deployments. World Economic Forum “Lighthouse” designations in Vietnam highlighted productivity gains of 190% and cost reductions of 45% at digitally transformed facilities. Larger EMS players are widening the capability gap as smaller firms struggle to finance successive upgrade cycles. Predictive maintenance, real-time defect detection, and autonomous intralogistics are becoming qualifiers rather than differentiators, pushing the contract manufacturing market toward a technology-centric competitive paradigm.

Pharmaceutical Capacity Crunch Driving Emergency CDMO Outsourcing

COVID-19 vaccine obligations diverted European biologics capacity and forced drug sponsors to offload non-core plants, accelerating reliance on CDMOs. Samsung Biologics secured more than USD 3.3 billion in new contracts during 2024 and lifted installed capacity to 784,000 liters with its fifth plant. Lonza’s USD 1.2 billion acquisition of Roche’s Vacaville facility added 330,000 liters of U.S. biologics space. CDMOs now integrate development, scale-up, and regulatory support, shifting pricing power in their favor and further consolidating the contract manufacturing market.

EV Battery Thermal-management Outsourcing in China & Korea

Automakers are spinning out thermal-management modules to contractors as next-generation chemistries demand semiconductor-grade assembly standards. Chinese battery makers broke ground on Illinois and Morocco plants worth USD 27 billion to preserve U.S. market access. Korean suppliers leverage compound-semiconductor expertise to design advanced interface materials that legacy automotive vendors cannot replicate. Heightened scrutiny under “foreign entity of concern” rules is prompting dual-sourcing, raising the strategic importance of specialist contractors inside the contract manufacturing market.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising IP-leakage litigation in cross-border tooling transfers | -0.7% | Global, especially U.S.–China corridors | Short term (≤ 2 years) |

| EU Green-Deal Scope-3 emission audits raising compliance cost | -0.5% | Europe; global spill-over | Medium term (2-4 years) |

| Semiconductor supply-chain volatility distorting EMS forecasting | -0.4% | Global; Asia-Pacific concentration | Short term (≤ 2 years) |

| Skilled-labor shortage in high-precision biologics fill-finish | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising IP-Leakage Litigation in Cross-border Tooling Transfers

Automotive patent suits jumped 150% between 2019 and 2024, with litigation awards exceeding USD 100 million becoming frequent. Non-practicing entities initiated 63% of 2024 cases, often targeting contract manufacturers with limited legal buffers. Heightened risk is driving costly escrow protocols, encrypted data rooms, and specialized insurance, eroding price advantages once derived from offshore tooling.

EU Green-deal Scope-3 Emission Audits Raising Compliance Cost

The Carbon Border Adjustment Mechanism could lift steel-intensive production costs by 16% per ton by 2026[3]Thomas Skordas, “Regulation (EU) 2023/956: Carbon Border Adjustment Mechanism,” Official Journal of the European Union, europa.eu. Scope-3 reporting rules compel suppliers worldwide to track upstream carbon content, requiring digital twins of entire value chains. Small manufacturers face disproportionate expense to certify emissions, prompting consolidation within the contract manufacturing market as compliance capabilities become a prerequisite for European market access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Vertical – Electronics Leadership with Pharmaceutical Acceleration

Electronics accounted for 35.45% of the contract manufacturing market share in 2024 and continues to anchor absolute revenue. Smartphone, server, and AI-accelerator volumes give EMS providers scale to amortize automation investments, bolstering profitability. Pharmaceuticals, however, charts the fastest 9.8% CAGR to 2030 as complex biologics drive outsourcing of sterile processing, analytics, and regulatory documentation. This tug-of-war produces a balanced growth profile for the contract manufacturing market. Automotive outsourcing expands in tandem with electric-vehicle adoption, especially for battery modules and power electronics that demand semiconductor-grade tolerances. Consumer-goods brands adopt micro-lot 3-D printing to personalize SKUs, a practice expected to lift mid-tier contract manufacturing market size segments at 5%-plus CAGR over the next five years. Aerospace and defense remain steady due to certification hurdles, whereas textiles leverage capacity-sharing models purely for cost smoothing.

Contract manufacturers with deep electronics-process know-how are leveraging cross-industry synergies. Surface-mount technology lines originally tuned for smartphones are increasingly build medical wearables and battery-management units. Conversely, biologics CDMOs apply single-use bioreactor expertise to veterinary vaccines and novel food proteins, diversifying client portfolios. Segment boundaries are blurring, drawing new entrants as technological convergence reshapes the contract manufacturing market.

By Contract Type – Strategic Partnerships Versus Project-based Flexibility

Strategic alliances retained 60.54% of 2024 revenue and reflect rising product complexity, qualification cycles, and regulatory rigor. Co-investment in dedicated cleanrooms, high-throughput screening, and continuous-manufacturing lines aligns incentives and drives long-tenor revenue visibility. For instance, Samsung Biologics secured multi-year biologics supply deals extending to 2037, ensuring capacity lock-in for its newest plant. Brands entrust quality-critical steps to partners embedded in their design workflows, protecting intellectual property through joint governance.

Project-based contracts, expanding at 7.5% CAGR, suit markets characterized by rapid technology refresh, such as AI inference accelerators and utility-scale battery modules. Clients favor modular line designs that pivot quickly between products. Contract manufacturers respond with flexible automation cells and digital twins that slash line-change time. The model offers entry points for regional specialists and remains vital for the contract manufacturing industry segments that value agility over deep integration.

Geography Analysis

Asia-Pacific maintained 45.67% of 2024 revenue, signaling entrenched advantages in cost, ecosystem density, and engineering talent. China’s orchestration of wafer fabs, substrate suppliers, and final assembly under one cluster sustains scale unrivaled elsewhere. Meanwhile, Vietnam, India, and Malaysia absorb overflow demand as brands diversify geopolitical exposure. Taiwanese giants such as Foxconn and Pegatron committed more than USD 1.2 billion to Mexican and U.S. plants to hedge against tariffs. These parallel footprints buffer risk yet preserve Asia-centric supply-chain synergies, ensuring the contract manufacturing market remains regionally anchored.

North America is benefiting from synchronized federal and state incentives that revive semiconductor and precision-machining capacity. Mexican industrial parks near the Texas border attract both Asian and U.S. investors who value tariff-free access under USMCA. Canadian aerospace and biologics hubs leverage established regulatory frameworks to secure high-value projects. The contract manufacturing market size for North America is poised for mid-single-digit growth, contingent on timely infrastructure upgrades and workforce skilling programs.

The Middle East & Africa region posts the fastest 9.2% CAGR as Saudi Arabia, the UAE, and Egypt channel sovereign wealth into industrial diversification[4]Hana Al Suwaidi, “Operation 300bn Progress Report 2025,” UAE Ministry of Industry and Advanced Technology, moiat.gov.ae. Renewable-energy megaprojects supply low-cost green electricity, enticing aluminum smelters and specialty-chemical plants. Pharmaceutical players eye free-zone incentives and proximity to emerging markets. Success, however, hinges on training local engineers and integrating the new capacity into global logistics corridors, challenges that multinationals address through joint ventures and knowledge-transfer clauses.

Europe remains constrained by high energy prices and stringent environmental rules yet commands premium niches in aerospace, life sciences, and industrial automation. CDMOs in Switzerland, Germany, and Ireland enjoy favorable tax and IP frameworks, sustaining project pipelines despite region-wide cost pressures. Strategic autonomy debates may spur localized production mandates in defense and medical goods, opening new pools of demand within the contract manufacturing market.

Competitive Landscape

The contract manufacturing market exhibits medium concentration overall but varies sharply by sector. The top five pharmaceutical CDMOs command more than 45% of biologics capacity following Novo Holdings’ USD 16.5 billion Catalent takeover. By contrast, the top five EMS vendors control only a quarter of electronics assembly revenue, reflecting a fragmented long-tail of regional specialists. Consolidators target technology gaps; Lonza’s acquisition of Roche’s Vacaville site added mammalian-cell capacity, while Flex invested in a Dallas power-infrastructure plant to chase AI data-center demand. Specialized players gain leverage through proprietary process platforms such as Samsung Biologics’ S-HiConTM, which enables high-concentration biologics fill-finish with minimal viscosity drift.

AI-driven automation raises capital intensity, favoring incumbents with balance-sheet strength. Yet high-mix, low-volume niches still reward agility. European EMS firms differentiate through advanced optical-photonics integration, serving quantum-computing hardware and high-speed telecoms. Gulf CMOs leverage subsidized energy and new port links to underprice competitors in energy-intensive processes. Geopolitical risk pushes OEMs to dual-source critical subsystems, handing mid-tier contractors share they previously struggled to secure. Meanwhile, environmental compliance capabilities emerge as a decisive procurement criterion, spurring alliances between manufacturers and carbon-accounting software vendors.

Regulatory tightening and rising IP-litigation costs are boosting the value of integrated QC, cybersecurity, and legal-support suites embedded within service offerings. Firms that can bundle manufacturing with validation, packaging, and global distribution enjoy premium pricing. Those lacking digital traceability systems risk relegation to commodity segments with eroding margins. Consequently, industry structure is migrating toward a barbell: scaled multinationals on one end and hyper-specialists on the other.

Contract Manufacturing Industry Leaders

Hon Hai Precision Industry Co., Ltd.

Jabil Inc.

Celestica Inc.

Flex Ltd

Wistron Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Pegatron approved USD 85 million investment for a Texas server-manufacturing subsidiary to neutralize tariff exposure.

- May 2025: Wistron allocated USD 1.2 billion for AI-server factories in the United States and Mexico, including Dallas land purchase.

- April 2025: Samsung Biologics posted KRW 1.3 trillion Q1 revenue and launched Plant 5, announcing plans for a sixth facility to meet demand.

- March 2025: Post Holdings acquired Potato Products of Idaho to deepen contract food-processing capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the contract manufacturing market as the total revenue earned by third-party plants that fabricate, assemble, test, and package products for brand-owning companies across electronics, pharmaceuticals, automotive, consumer goods, aerospace, industrial machinery, textiles, food, and personal-care sectors.

Scope Exclusion: Stand-alone design consultancies with no production lines are omitted.

Segmentation Overview

- By Industry / End-Use Sector

- Pharmaceuticals, Healthcare & Medical Devices

- API & FDF (Small-molecule)

- Biologics Manufacturing (Cell & Gene Therapy, mAbs)

- Nutraceuticals / OTC Drugs

- Medical Devices (diagnostics, surgical, etc)

- Others (consumables)

- Electronics & Semiconductors

- Consumer Electronics (smartphones, IoT devices, etc.)

- Industrial & IoT Electronics

- Telecommunication Equipment

- Computing & Data Infrastructure

- Semiconductor Assembly, Packaging & Testing (OSAT)

- Others (automotive electronics, Renewable & Power Electronics, etc.)

- Automotive

- Powertrain Components (ICE, Electric & Hybrid)

- EV Battery Packs

- Interior & Exterior Assemblies

- Embedded Electronics

- ADAS / Autonomous Modules

- Consumer Goods

- Home Appliances

- Personal Care & Wearables

- Others (Tools & Hardware, Toys & Recreation Equipment)

- Aerospace & Defense

- Industrial Machinery

- Textiles & Apparel

- Garment Manufacturing

- Others (Technical Textile, Home Textile)

- Food & Beverage

- Food Processing

- Beverage Bottling

- Packaging & Labeling

- Personal Care & Cosmetics

- Pharmaceuticals, Healthcare & Medical Devices

- By Contract Type

- Long-term Strategic Partnership

- Project-based / Short-term

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Peru

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Turkey

- Egypt

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed sourcing heads at original-equipment manufacturers, senior executives inside tier-one contract manufacturers, equipment suppliers, and regional trade association officials across Asia-Pacific, the Americas, and Europe. These discussions refined prevailing outsourcing shares, blended average selling prices, and utilization patterns that public data alone cannot capture.

Desk Research

We map the demand pool through public datasets such as UN Comtrade, the US Census Annual Survey of Manufactures, Eurostat PRODCOM, China's National Bureau of Statistics, and trade bodies like IPC and PhRMA. Company filings, 10-Ks, and investor decks reveal outsourcing ratios, while Questel patent analytics and Dow Jones Factiva news feeds trace capacity additions, M&A, and green-field projects. The sources listed are illustrative; many additional publications underpin data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down rebuild converts end-sector manufacturing output into outsourced value using verified outsourcing ratios and blended ASPs. Select bottom-up roll-ups of public contract-manufacturer revenues calibrate totals. Key inputs include electronics export volumes, new drug approvals, light-vehicle production, global PMI indices, wage differentials, and announced capital-expenditure pipelines. A multivariate regression informed by these drivers feeds an ARIMA forecast that projects values through 2030. Data gaps are bridged with three-year moving averages agreed during expert calls.

Data Validation & Update Cycle

Outputs undergo variance checks against historical series, peer disclosures, and macro signals before senior analyst sign-off. Models refresh every twelve months, with interim updates triggered by material trade or capacity events so clients always receive our latest view.

Why Mordor's Contract Manufacturing Baseline Is Dependable

Published estimates often diverge because research firms apply different sector mixes, outsourcing ratios, refresh cadences, or currency bases. By aligning scope to nine end-use sectors, applying contract-type splits, and normalizing exchange rates at each update, Mordor Intelligence presents a balanced middle path that decision-makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 724.35 B | Mordor Intelligence | - |

| USD 686.40 B | Global Consultancy A | Excludes textiles and personal-care; 2024 forex lock |

| USD 779.82 B | Research Publisher B | Assumes flat 60 % outsourcing; aggressive ASP inflation |

| USD 648.50 B | Industry Journal C | Counts only long-term contracts |

These comparisons underline how our disciplined scope, transparent variables, and annual refresh deliver the most reproducible baseline for strategic planning.

Key Questions Answered in the Report

What is the projected value of the contract manufacturing market by 2030?

The contract manufacturing market is forecast to reach USD 966.84 billion by 2030 at a 5.98% CAGR.

Which end-user segment currently leads the contract manufacturing market?

Electronics commands 35.45% market share, reflecting high demand for consumer devices, industrial equipment, and AI infrastructure.

Why are pharmaceutical companies increasingly outsourcing manufacturing?

Capacity shortages and the complexity of biologics are pushing drug developers toward CDMOs that provide integrated development, manufacturing, and regulatory support.

How is near-shoring influencing contract manufacturing strategies?

USMCA incentives and supply-chain risk mitigation are encouraging firms to relocate production to Mexico and the broader North American region for faster turnaround and tariff advantages.

Page last updated on: